Authors:

Kiran Pulidindi, Kunal Ahuja

Download free PDF

Specialty Fiber Crop Seeds Market Size & Share 2026-2035

Report ID: GMI14612

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Specialty Fiber Crop Seeds Market

Get a free sample of this report

Get a free sample of this report Specialty Fiber Crop Seeds Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Specialty Fiber Crop Seeds Market Size

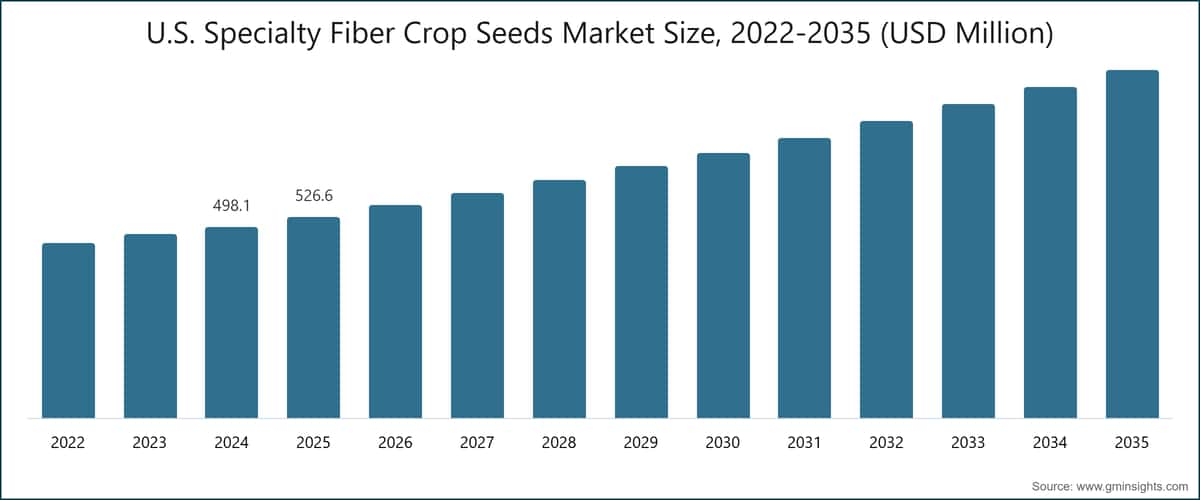

The global specialty fiber crop seeds market was valued at USD 2.4 billion in 2025, reflecting sustained demand across cotton, flax, hemp, jute, and kenaf cultivation systems in major agricultural economies worldwide.[1]Food and Agriculture Organization of the United Nations (FAO), https://www.fao.org The market is projected to expand at a compound annual growth rate of 5.6% from 2025 to 2035, reaching USD 4.16 billion by 2035, according to the latest report published by Global Market Insights Inc.

Specialty Fiber Crop Seeds Market Key Takeaways

Market Leader: Bayer AG (Deltapine) led with over 35% market share in 2025.

Leading Players: Top 5 players in this market include Bayer AG, Corteva Agriscience, The Jute Corporation of India Ltd., International Hemp, IND Hemp LLC, which collectively held a market share of 72% in 2025.

Cotton seeds continue to anchor the crop-type landscape at 92.4% of total market value - a concentration that underscores the central role of Bt cotton and hybrid varieties in global agricultural systems - while emerging bio-fiber crops including hemp, flax, and kenaf are attracting accelerating institutional investment.[2]United States Department of Agriculture – National Agricultural Statistics Service (USDA-NASS), https://www.nass.usda.gov The more consequential long-term structural shift lies in the convergence of sustainability mandates from downstream industries, policy-driven legalization of hemp cultivation, and precision breeding commercialization: these three forces are collectively reconfiguring the specialty fiber crop seeds market from a commodity seed supply system into an innovation-driven specialty agricultural input segment.[3]Organisation for Economic Co-operation and Development (OECD), https://www.oecd.org

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Sustainable Material Demand

+2.1%

Global

Medium term

Automotive & Construction Applications

+1.4%

Europe, NA, APAC

Long term

Government Support & Subsidies

+1%

NA, EU, India

Short term

Sustainable Material Demand

The structural shift from synthetic to natural fibers represents the primary growth engine for the specialty fiber crop seeds market. Fashion retailers, industrial manufacturers, and packaging companies are operating under intensifying pressure - from regulatory mandates, investor ESG frameworks, and consumer preference shifts - to reduce polyester and nylon content across their supply chains.[4]International Energy Agency (IEA), https://www.iea.org The EU Strategy for Sustainable and Circular Textiles, adopted in 2022, targets a significant reduction in virgin synthetic textile material use by 2030 - a directive that is already reshaping procurement decisions among European apparel manufacturers and generating structured upstream demand for certified natural fiber seed varieties.[5]European Commission, https://ec.europa.eu Cotton, hemp, and flax seeds are the direct upstream beneficiaries of this transition, with certified organic and low-input seed varieties commanding an increasing share of institutional purchasing volumes. This driver contributes an estimated +2.1% to forecast CAGR.

Expansion of Automotive & Construction Applications

Bio-composite applications in automotive interiors and structural construction panels represent one of the highest-growth demand channels for hemp, kenaf, and jute fiber - and by extension for the seed varieties supplying those fiber streams. Automotive OEMs have deployed natural fiber composites in door panels, trunk liners, and headliners under EU CO₂ emissions standards that impose cumulative lightweighting requirements across model lifecycles. Kenaf-polypropylene composite panels have attracted renewed OEM evaluation as a replacement for glass fiber in secondary structural applications, while hempcrete and flax insulation boards are scaling in parallel with green building certification requirements under BREEAM and LEED frameworks. Across both sectors, the critical path runs through the specialty fiber crop seeds market: variety performance in fiber length uniformity, tensile strength, and moisture management determines suitability for industrial processing, and seed developers with documented industrial-grade germplasm are capturing the premium end of the market. This driver contributes an estimated +1.4% to forecast CAGR.

Government Support & Subsidies

Hemp legalization and agri-input subsidy programs across the US, EU, Canada, and India are reducing the regulatory risk premium that historically suppressed hemp seed investment and commercial cultivation expansion.[6] The US 2018 Farm Bill removed industrial hemp from Schedule I classification, opening federal research funding and commercial cultivation licensing nationwide. Canada's hemp licensing framework - administered by Health Canada - has made the country the world's largest industrial hemp seed exporter, with commercial production supported by an established variety registration and certification infrastructure. India's hemp policy liberalization, including cultivation approvals in Uttarakhand and Himachal Pradesh, is extending the upstream seed market opportunity within the world's largest textile-producing economy. These converging policy tailwinds contribute an estimated +1% to forecast CAGR.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Regulatory Barriers

−1.2%

EU, NA, APAC

Short term

Supply Chain Limitations

−0.9%

LATAM, MEA, SEA

Medium term

Climate Variability

−0.6%

South Asia, Africa

Long term

Regulatory Barriers (Hemp & GMO)

Regulatory fragmentation across jurisdictions is the most significant near-term constraint on specialty fiber crop seeds market growth. Hemp cultivation remains subject to THC concentration thresholds that differ between the historic EU standard of 0.2%, the US Farm Bill limit of 0.3%, and varying national frameworks across Asia and Latin America — creating compliance uncertainty for seed developers and growers operating across multiple markets. GMO and biotechnology-enhanced seed approvals face multi-year regulatory timelines, particularly within the EU, where the European Food Safety Authority's authorization process can extend five to seven years for new trait applications. This regulatory complexity restricts market access for high-value biotechnology seed varieties and depresses investment in novel hemp and kenaf breeding programs. Estimated CAGR impact: −1.2%.

Supply Chain & Processing Limitations

The specialty fiber crop seeds market operates with pronounced infrastructure asymmetry. While cotton seed supply chains are mature and globally integrated, hemp, flax, kenaf, and jute processing infrastructure remains fragmented, regionally concentrated, and inadequate to support demand scaling. Retting facilities, decorticators, and primary fiber processing units — the downstream capital equipment required to convert raw fiber crops into usable industrial inputs - are absent or sub-scale across much of Sub-Saharan Africa, Southeast Asia, and Latin America. This gap suppresses grower adoption of specialty fiber crops, directly constraining upstream seed demand across regions where agricultural land suitability and labor economics are otherwise favorable. Estimated CAGR impact: −0.9%.

Climate & Yield Variability

Specialty fiber crops exhibit higher sensitivity to precipitation variability and temperature extremes than most staple commodity crops, creating systemic yield risk that depresses smallholder adoption rates. Cotton cultivation is water-intensive, accounting for approximately 3% of global agricultural water consumption. Jute production across South Asia is exposed to monsoon irregularity, with yield fluctuations of 15–25% documented in poor rainfall seasons by the FAO. Climate variability introduces seed demand volatility - poor harvest seasons compress replanting rates and shift grower purchasing toward lower-risk seed options, reducing demand for premium biotechnology-enhanced and certified varieties. Estimated CAGR impact: −0.6%.

Specialty Fiber Crop Seeds Trends

Sustainable and Bio-Based Fiber Demand Reshaping Seed Investment Priorities

Demand for bio-based and biodegradable materials has emerged as one of the most structurally transformative forces in the specialty fiber crop seeds market. Downstream industries such as textiles, automotive, and packaging are facing increasing regulatory and ESG-driven pressure to reduce synthetic fiber dependency, particularly polyester and nylon. This shift is translating into direct upstream demand for natural fiber crops including cotton, flax, hemp, and kenaf. Seed developers are increasingly aligning their R&D pipelines with sustainability-linked performance parameters such as lower pesticide requirements, reduced water consumption, and compatibility with organic certification frameworks. Procurement dynamics are also evolving; institutional buyers are prioritizing traceable, certified seed inputs capable of meeting lifecycle carbon reduction targets and supply chain transparency mandates. The resulting shift is driving premiumization within specialty seeds, especially certified organic cotton and EU-compliant flax and hemp varieties, and is reshaping long-term capital allocation strategies among leading agribusiness firms.

Dual-Use Seeds Expanding the Addressable Market

The emergence of dual-use seed varieties-particularly in hemp and flax-is significantly expanding the economic and application scope of the specialty fiber crop seeds market. These varieties are engineered to simultaneously produce high-quality fiber and commercially viable grain for food, nutraceutical, and oil applications, improving per-hectare returns for farmers. This dual-revenue model reduces dependency on a single downstream market and enhances resilience against demand fluctuations in textiles or industrial materials. In North America and Europe, seed developers are actively commercializing cultivars optimized for both fiber strength and seed oil composition, creating new pricing tiers and differentiated value propositions within the seed market. The impact extends beyond farm-level economics: dual-use traits are redefining procurement specifications across industries, enabling cross-sector adoption and strengthening demand from food, textiles, and industrial buyers concurrently. This trend is especially critical for hemp and flax, positioning them as high-growth segments compared to conventional single-use fiber crops.

Precision Breeding and Gene Editing Accelerating Trait Innovation

Advancements in precision breeding technologies, including CRISPR-based gene editing and marker-assisted selection, are significantly accelerating innovation cycles within the specialty fiber crop seeds market. Historically, variety development timelines ranged between 10–15 years; however, new genomic tools are compressing this cycle to approximately 5–7 years, enabling faster commercialization of improved seed traits. Key innovation areas include enhanced fiber length consistency, disease resistance, drought tolerance, and improved dual-use properties. In cotton, gene editing has been applied to reduce gossypol content, expanding its usability beyond fiber into feed and protein applications. Regulatory shifts, particularly in regions where gene-edited crops are not classified as traditional GMOs, are further supporting this trend by enabling faster approvals. As a result, biotechnology-enhanced seeds are expected to expand beyond cotton into hemp, flax, and kenaf segments, gradually transforming the market into a high-value, innovation-driven agricultural input industry.

Specialty Fiber Crop Seeds Market Analysis

By Crop Type

The crop-type composition of the specialty fiber crop seeds market is highly skewed toward cotton, which accounts for approximately 92.4% of total market value. This dominance is driven by the widespread adoption of Bt and hybrid cotton varieties across the US, India, China, Brazil, and Australia, supported by strong yield performance and integrated pest resistance traits. The cotton seed segment is characterized by high commercialization, structured supply chains, and strong pricing power for biotechnology-enhanced varieties, particularly stacked-trait seeds combining insect resistance and herbicide tolerance.

The remaining 7.6% of the market comprises non-cotton specialty crops including flax (4.2%), hemp (1.6%), jute (1.6%), and kenaf (0.1%). While these segments are relatively small in absolute terms, they represent the highest growth potential within the market. Flax seeds are widely cultivated across Canada and Europe, serving both textile and nutrition markets. Hemp seeds are experiencing rapid expansion driven by legalization and dual-use applications, while jute remains regionally concentrated in South Asia under government-supported procurement frameworks. Kenaf and other niche fibers, although nascent, are gaining attention in automotive composite applications, indicating long-term strategic importance despite their current limited scale.

By Seed Technology & Breeding Method

The technology structure of the specialty fiber crop seeds market reflects a balance between cost-sensitive conventional seeds and high-performance advanced varieties. Conventional seeds hold approximately 49.2% share, primarily driven by smallholder farming systems in emerging markets where cost efficiency remains the primary decision factor. These include open-pollinated varieties and improved traditional lines developed through marker-assisted selection programs.

Hybrid seeds account for approximately 31.9% of the specialty fiber crop seeds market and represent the most commercially dynamic segment within the established technology stack. Hybrid cotton and jute seeds deliver yield improvements of 15–30%, making them attractive in regions with favorable agronomy conditions. Biotechnology-enhanced seeds hold 16.9% share, largely concentrated in cotton, where Bt and stacked traits dominate commercial cultivation.

Organic-certified seeds, though accounting for only 1.9%, represent the fastest-growing high-value niche. Demand for these seeds is driven by sustainability commitments, organic textile certification requirements, and increased consumer awareness. This segment commands premium pricing and is expected to expand steadily, particularly in Europe and North America.

By Region

North America Specialty Fiber Crop Seeds Market

North America represents approximately 19.7% of the global market, driven by high-value cotton cultivation in the US and strong hemp and flax seed sectors in Canada. The US cotton market is characterized by advanced biotechnology adoption, with strong presence of leading seed brands and integrated digital agronomy solutions. Hemp cultivation has expanded following regulatory legalization, supported by structured licensing and quality compliance frameworks. The region is also a center for innovation in dual-use seed development.

Europe Specialty Fiber Crop Seeds Market

Europe accounts for approximately 17.8% of global market share, with a strong focus on flax, hemp, and sustainable fiber crops. The region benefits from supportive regulatory frameworks such as CAP subsidies and sustainability directives, which are accelerating demand for natural fibers. Flax cultivation is concentrated in France and Belgium, while hemp adoption is expanding across Germany, the Netherlands, and Eastern Europe. Regulatory mandates on sustainability and traceability are major demand drivers.

Asia Pacific Specialty Fiber Crop Seeds Market

Asia Pacific is the largest regional market, accounting for 46.8% of global value. The region’s dominance is driven by large-scale cotton and jute cultivation in India and China. Government initiatives supporting improved seed adoption, along with strong domestic demand for natural fibers, sustain growth. China’s increasing investment in domestic seed R&D and biotechnology is also strengthening regional competitiveness.

Latin America Specialty Fiber Crop Seeds Market

Latin America contributes approximately 11.2% of market share and represents the fastest-growing region. Brazil is the key growth engine, driven by agricultural expansion and integration of fiber crops into crop rotation systems. Increasing investment in sustainable agriculture and industrial fiber applications is boosting demand for specialty seeds.

Specialty Fiber Crop Seeds Market Share

The specialty fiber crop seeds industry exhibits a moderately high concentration, with the top five players accounting for approximately 72% of global market value. The market follows a dual-structure pattern: high consolidation in cotton seeds and fragmentation in non-cotton segments.

Bayer AG holds the leading position with approximately 35% share, supported by its extensive cotton germplasm portfolio and integrated digital agriculture solutions. Corteva Agriscience follows with around 18%, leveraging strong trait development capabilities. Institutional players such as The Jute Corporation of India maintain stable regional influence, while specialized hemp companies are emerging as key growth drivers.

The remaining market is fragmented among regional and niche players focused on specific crops, geographies, and application segments. Competitive dynamics are driven by trait innovation, certification compliance, and strategic partnerships with downstream industries.

Specialty Fiber Crop Seeds Market Companies

Major players operating in the Specialty Fiber Crop Seeds industry are:

Major players operating in the Specialty Fiber Crop Seeds market are: Bayer AG, Corteva Agriscience, The Jute Corporation of India Ltd., International Hemp, IND Hemp LLC, Horizon Specialty Seeds, Prairie Premium Products, Kenaf Green Industries, Legacy Hemp, Manitoba Flax Growers Association, Precision Plants, Kanda Hemp, NWG Genetics, Saluna AG, and FiberAgro.

Bayer AG - operating its seed business under the Deltapine brand following the 2018 Monsanto acquisition - holds the dominant commercial position in the specialty fiber crop seeds market. Deltapine's cotton germplasm portfolio encompasses more than 100 commercial varieties optimized for US, Indian, Australian, and West African cotton growing conditions, with stacked Bt/herbicide-tolerance trait packages representing the highest-margin commercial tier. Bayer's integration of the Climate FieldView digital agronomy platform with its seed sales model positions the company as an integrated input and data services provider - a strategy that creates multi-year grower retention dynamics beyond the annual seed purchasing cycle. Bayer AG's active investment in low-pesticide-input and organic transition cotton seed lines reflects a deliberate response to downstream apparel brand sustainability procurement requirements.

Corteva Agriscience markets cotton seeds through the PhytoGen brand, with commercial strength concentrated in the US Mid-South and Southwest cotton belt. The Enlist® cotton platform - combining 2,4-D choline and glufosinate herbicide tolerance with Bt insect resistance - provides one of the broadest stacked trait configurations in commercial US cotton seed. Corteva's CRISPR-based trait editing investments within its PhytoGen portfolio represent the company's forward investment in maintaining trait performance advantages as conventional Bt resistance management becomes increasingly complex in markets with high adoption history.

The Jute Corporation of India Ltd. is a Government of India enterprise under the Ministry of Textiles, responsible for jute seed procurement, distribution, and minimum support price administration across jute-growing states in eastern India. Its institutional market presence - maintaining certified seed multiplication farms in West Bengal and Bihar, and coordinating with ICAR's CRIJAF on improved variety release and extension services - provides structural stability to the jute seed market that commercial firms alone would not sustain given the thin economics of smallholder jute cultivation.[7]Indian Council of Agricultural Research (ICAR), https://www.icar.org.in

International Hemp is a vertically integrated hemp seed and fiber company operating in Montana, US, developing proprietary varieties optimized for industrial fiber applications including automotive bio-composites and construction materials. The company's strategy positions it at the intersection of seed supply and downstream material processing, enabling direct engagement with automotive OEM natural fiber procurement programs and providing supply chain transparency documentation that institutional industrial buyers increasingly require.

IND Hemp LLC operates as an emerging integrated hemp company in Montana, with commercial hemp seed multiplication, decortication, and fiber marketing operations. The commissioning of a new decortication facility in Conrad, Montana, in early 2026 - with design capacity of approximately 5,000 MT of raw hemp stalk annually - reflects the company's strategy of building processing-integrated seed demand rather than relying solely on grower seed sales.

Horizon Specialty Seeds and Prairie Premium Products represent the North American specialty seed tier with strengths in certified variety multiplication, export market access to European and Asian buyers, and agronomy service capabilities for transitioning growers entering specialty fiber crop production for the first time. Manitoba Flax Growers Association functions as both a grower-funded industry organization and a coordinating body for flax variety testing and agronomy research across Manitoba's commercial flax cultivation area, maintaining applied research partnerships with Prairie university breeding programs.

Kenaf Green Industries is among the small number of commercial kenaf seed developers globally, focused on kenaf fiber crop supply chain development for automotive and construction composite applications. The company's market position is niche in scale but strategically aligned with the longer-term demand trajectory for kenaf-polypropylene composite materials.

NWG Genetics, Saluna AG, and Kanda Hemp represent the European hemp seed development tier, with programs centered on EU-approved variety list registrations under the revised CAP framework and the NGT legislation. Saluna AG has commercialized monoecious hemp varieties - including the newly registered Santhica 70 and Saluna F1 - specifically developed to simplify mechanical harvesting and improve farm-level adoption economics for Central and Western European growers. Legacy Hemp, Precision Plants, and FiberAgro round out the competitive landscape as emerging regional players, each building differentiated positioning in organic certification, dual-use variety performance, or geographic market access in Latin America and the Asia Pacific frontier markets.

~35%

Collective Market Share of ~72%

Specialty Fiber Crop Seeds Industry News

Market Concentration Score

The specialty fiber crop seeds market scores 7.5 out of 10 on the concentration scale, reflecting the high dominance of Bayer AG (35% share) and Corteva Agriscience (18% share) within the cotton seed tier - which constitutes 92.4% of total market value - offset by pronounced fragmentation across the non-cotton specialty segment where no single participant commands more than 5% of sub-segment revenues.

The specialty fiber crop seeds market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Billion and (Kilo Tons) in volume from 2022 - 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Crop type

Market, By Seed Technology & Breeding Method

Market, By End-Use Application

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Crop Type, 2022–2035 (USD Million)

Chapter 6 Market Estimates and Forecast, By Seed Technology & Breeding Method, 2022–2035 (USD Million)

Chapter 7 Market Estimates and Forecast, By End-Use Application, 2022–2035 (USD Million)

Chapter 8 Market Estimates and Forecast, By Region, 2022–2035 (USD Million)

Chapter 9 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →