Authors:

Preeti Wadhwani, Satyam Jaiswal

Download free PDF

Fog Computing Market Size & Share 2026-2035

Report ID: GMI2295

|

Published Date: July 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Fog Computing Market

Get a free sample of this report

Get a free sample of this report Fog Computing Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Fog Computing Market Size

The global fog computing market was estimated at USD 405.3 million in 2025. It is expected to grow from USD 462 million in 2026 to USD 1.8 billion by 2035, registering a 16.4% CAGR during 2026–2035. This forecast is according to latest report published by Global Market Insights Inc.

Fog Computing Market Key Takeaways

Market Leader: Dell Technologies led with over 10.5% market share in 2025.

Leading Players: Top 5 players in this market include Dell Technologies, Cisco Systems, IBM, Microsoft, Intel, which collectively held a market share of 44.3% in 2025.

Demand is moving beyond early edge-computing pilots as enterprises add compute capacity between IoT endpoints and centralized cloud environments. The most important shift is architectural: organizations want latency control, bandwidth discipline, and local data governance in the same operating layer.

Key Drivers

Driver

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

IoT Data Volume

+3.2%

Global

Long term (≥ 4 years)

Ultra-Low Latency Demand

+2.9%

Global

Medium term (2-4 years)

Industry 4.0 Investments

+2.4%

North America, Europe, Asia Pacific

Medium term (2-4 years)

Bandwidth Cost Pressures

+1.8%

Global

Short term (≤ 2 years)

IoT Data Volume

The number of connected IoT devices is projected to exceed 32.1 billion by 2030, up from approximately 15.9 billion in 2023, creating a sharp increase in edge-generated data.[1]International Telecommunication Union, https://www.itu.int This data cannot be economically or operationally routed to centralized cloud environments in full. Fog nodes filter, preprocess, and analyze data locally, making the fog computing market a direct beneficiary of device proliferation.

Ultra-Low Latency Demand

Industrial automation, autonomous systems, robotic control, and clinical monitoring require response times that centralized architectures cannot consistently deliver. ITU-defined 5G performance targets for ultra-reliable low-latency communication reinforce the need for compute to sit close to the device layer. The resulting demand adds an estimated +2.9% to the market CAGR.

Industry 4.0 Investments

Manufacturing digitalization programs are pushing compute onto the shop floor. The European Commission’s Digital Decade agenda supports industrial digital infrastructure investment through 2030, and that policy support aligns closely with fog deployment in factories, utilities, and logistics facilities.

Bandwidth Cost Pressures

Video streams, industrial sensors, connected vehicles, and machine-vision systems generate large volumes of raw data. Processing that data locally reduces cloud transfer loads and lowers the cost exposure associated with centralized processing.

Key Challenges

Challenge

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Heterogeneous Integration Complexity

-1.6%

Global

Medium term (2-4 years)

Cybersecurity and Data Governance

-1.3%

Global

Long term (≥ 4 years)

Heterogeneous Integration Complexity

Fog deployments must connect sensors, industrial controllers, legacy OT systems, cloud platforms, and multiple network protocols. NIST guidance on edge and distributed systems highlights interoperability and security-management complexity as recurring implementation issues. Systems integrators mitigate this restraint by standardizing orchestration, device management, and security policy enforcement across multi-vendor environments.

Cybersecurity and Data Governance

Distributed fog nodes expand the attack surface because compute, storage, and application logic move outside centralized data centers. Enterprises must manage authentication, patching, encryption, data residency, and monitoring across geographically dispersed assets. The mitigation path is clearer than it was in the market’s early stage: secure boot, zero-trust access controls, encrypted workload processing, and unified lifecycle management are becoming baseline procurement requirements.

Fog Computing Market Trends

AI and machine learning inference are becoming central to the fog computing market because many industrial and operational decisions lose value when processed after a cloud round trip. In manufacturing, predictive maintenance systems need to classify vibration, temperature, acoustic, and machine-vision signals in real time. In healthcare, connected monitoring systems require local processing for privacy and response consistency.

IEEE work on edge AI deployment architectures has helped enterprises formalize how models should be placed, updated, and governed in distributed environments. In our Q1 2026 primary research covering 42 industrial IoT architects across the United States, Germany, Japan, and South Korea, respondents consistently described AI inference at fog nodes as a deployment prerequisite for predictive maintenance and closed-loop control, not a later software enhancement. The timeline is already active, with software growing at an 18.8% CAGR through 2035 as orchestration, analytics, and model-management tools become more valuable than basic device connectivity.[2]IEEE, https://www.ieee.org

A practical deployment example is Tampnet’s mid-2025 autonomous private 5G and edge-compute network for Aker BP’s offshore platform. The project illustrates why edge AI and fog computing are converging in harsh industrial environments: remote sites need local analytics, safety monitoring, and network resilience without depending on a distant data center. The implication for vendors is direct. Fog platforms that combine ruggedized hardware, GPU or neural processing support, secure boot, and model lifecycle management will command stronger pricing than generic gateway devices.

Private 5G is accelerating fog deployment because wireless reliability is no longer a secondary requirement for industrial operations. Factory floors, ports, mines, energy assets, and logistics hubs often contain mobile equipment that cannot rely on wired connectivity. ITU performance targets for 5G URLLC applications include latency objectives below 1 millisecond, creating a technical rationale for processing workloads near the device layer rather than routing them to centralized cloud infrastructure.[3]National Institute of Standards and Technology, https://www.nist.gov The impact is visible in the wireless connectivity segment, which generated USD 172.4 million in 2025 and is projected to reach USD 1.03 billion by 2035 at a 19.8% CAGR.

The market implication is not limited to telecom operators. Cisco, Nokia, Ericsson, Qualcomm Technologies, Cradlepoint, and private-network specialists are becoming important technology participants because the fog computing market increasingly depends on reliable local connectivity. FusionLayer and Cumucore demonstrated automated private 5G deployment in under two minutes at MWC Barcelona 2025, while Cisco released Meraki MG51 and MG51E 5G gateways in July 2024 in collaboration with T-Mobile. Those developments show the operational direction: faster site commissioning, more standardized connectivity templates, and tighter integration between network management and fog workload orchestration.

Hybrid cloud-fog orchestration is reshaping deployment models. Enterprises no longer evaluate fog computing as a binary alternative to the cloud. They are using orchestration platforms to decide which workloads should remain on fog nodes, which should be aggregated regionally, and which can move to centralized cloud resources. NIST’s work on edge computing and distributed infrastructure underscores the importance of standard management, security, and interoperability frameworks across heterogeneous nodes. The cloud-based deployment model, valued at USD 95.2 million in 2025, is forecast to grow at a 21.9% CAGR and reach USD 685.8 million by 2035.

Kubernetes extensions, Azure IoT Edge, Azure Industrial Edge, AWS Greengrass, IBM Edge Application Manager, and Red Hat tools all point toward the same operating model: distributed applications need consistent lifecycle management. A closer read reveals that this trend also changes purchasing behavior. Buyers are less likely to evaluate a single appliance and more likely to evaluate a full operating environment that includes device onboarding, workload placement, security policy enforcement, remote updates, observability, and cloud integration.

Smart-city programs are creating a broad public-sector use case for the fog computing market. Municipal deployments need real-time processing at traffic intersections, environmental monitoring stations, public safety installations, building systems, and utility networks. World Bank reporting on digital infrastructure investment across emerging economies reinforces the role of connectivity and computing infrastructure in urban modernization.[4] Nature Scientific Reports published research in 2025 validating multi-layered IoT-fog-cloud architectures for real-time smart-city applications such as intelligent parking management.[5]Nature, https://www.nature.com Smart Cities & Building Automation accounted for USD 74.1 million in 2025, equal to 18.3% of the total market, and is projected to grow at a 17.7% CAGR through 2035.

The second-order effect is the rise of localized systems integration. Municipal buyers often need platforms that can operate across traffic control, surveillance, utility monitoring, and emergency-response workflows. Interoperability matters as much as compute density. That is why smart-city fog projects tend to favor vendors and integrators with network engineering, cybersecurity, and application-integration capabilities rather than hardware-only suppliers.

Fog Computing Market Analysis

By Component

Hardware dominated the fog computing market in 2025, accounting for USD 188.3 million, or 46.5% of total revenue, and is projected to reach USD 693.5 million by 2035 at a 14.1% CAGR. The segment includes fog servers, ruggedized edge gateways, embedded computing modules, networking equipment, and purpose-built appliances deployed near endpoints. Dell Technologies’ PowerEdge XR series, Cisco IR1100 Rugged Series routers, Intel Xeon Scalable platforms, and Adlink Technology edge systems are examples of the hardware layer that supports industrial fog environments. Hardware remains essential because factories, substations, hospitals, and transportation hubs need devices that tolerate temperature variation, vibration, dust, and intermittent connectivity.

Software represented USD 138.3 million in 2025, or 34.1% of the fog computing market, and is expanding faster than hardware at an 18.8% CAGR through 2035. Services accounted for USD 78.7 million, or 19.4%, and are growing at a 16.8% CAGR as enterprises seek integration support. Our survey of 36 manufacturing automation leads across North America and Europe in Q4 2025 flagged ruggedized servers, edge gateways, and orchestration software as the first budget line items approved for factory-floor fog rollouts. The stronger software growth rate reflects enterprise demand for IBM Edge Application Manager, Azure IoT Edge, AWS Greengrass, Intel OpenVINO, and security middleware that can manage distributed applications at scale.

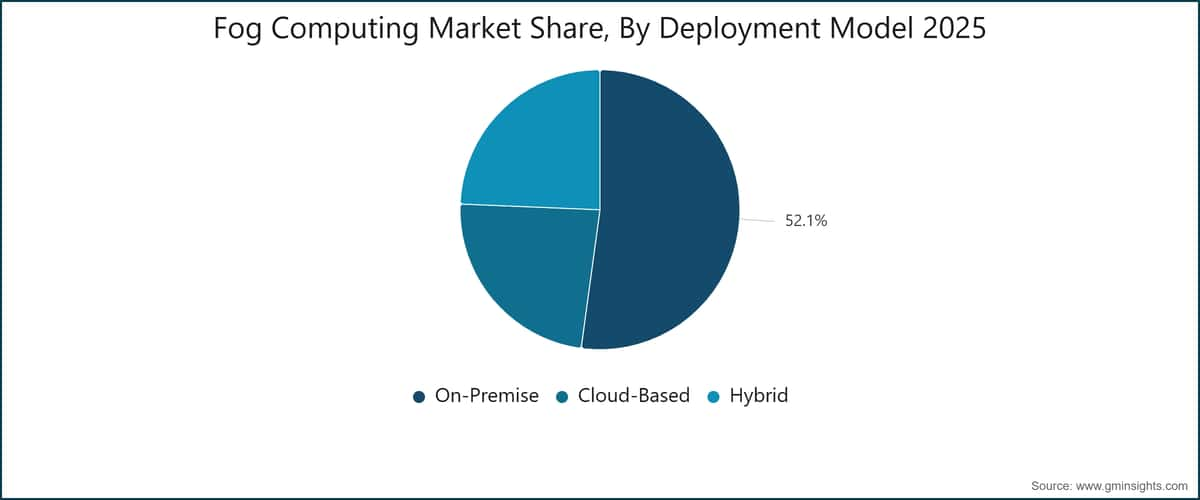

By Deployment Model

On-premise deployment led the fog computing market in 2025 with USD 211.3 million, equal to 52.1% of revenue, and is projected to grow at a 12.1% CAGR through 2035. This model remains preferred in healthcare, defense, financial services, and operational-technology environments where sensitive data must stay inside controlled networks. HIPAA and GDPR requirements strengthen the case for local processing in patient monitoring, diagnostics, and regulated enterprise workflows. On-premise fog deployments also fit manufacturing lines where downtime risk and deterministic latency outweigh the benefits of consumption-based cloud pricing.

Cloud-based fog computing generated USD 95.2 million in 2025, or 23.5% of revenue, and is the fastest-growing deployment model at a 21.9% CAGR through 2035, reaching USD 685.8 million. Hybrid deployments accounted for USD 98.7 million, or 24.4%, and are projected to reach USD 479.8 million by 2035 at a 17.4% CAGR. Microsoft Azure Industrial Edge, Azure Stack Edge, AWS Greengrass, and IBM Fog-as-a-Service illustrate how vendors are linking cloud management planes with distributed fog nodes. Pricing dynamics favor cloud-based and hybrid models where buyers want lower upfront capex, but regulated and latency-critical sectors will keep on-premise deployment structurally important.

By Application

Smart Manufacturing led the fog computing market by application in 2025, generating USD 115.4 million, or 28.5% of revenue, and is projected to reach USD 453.1 million by 2035 at a 14.9% CAGR. Factory deployments use fog computing for machine vision, predictive maintenance, quality inspection, autonomous robotics control, and production-line optimization. Springer Nature research published in 2025 documented improved predictive-maintenance outcomes when edge-fog computing architectures were deployed in Industrial IoT environments. Siemens MindSphere, Rockwell Automation FactoryTalk, Cisco Edge Intelligence, and Dell edge infrastructure all address this application layer through factory-level analytics and control.

Connected Vehicles & Transportation is the fastest-growing application, expanding from USD 55 million in 2025 to USD 324.1 million by 2035 at a 19.6% CAGR. Connected Healthcare also grows rapidly, rising from USD 41.1 million in 2025 to USD 234.6 million by 2035 at a 19.3% CAGR, while Smart Energy & Grids generated USD 49.7 million and Security & Emergency Systems generated USD 37.5 million in 2025. IEA analysis of grid modernization and renewable integration supports the need for real-time distributed computing in energy systems. Vehicle-to-everything processing, remote patient monitoring, substation analytics, and video-surveillance inference all require local compute because response time, data sensitivity, and resilience cannot be treated as afterthoughts.

By Network Connectivity

Wired connectivity dominated the fog computing market in 2025 at USD 232.9 million, representing 57.5% of total revenue, and is projected to reach USD 784.4 million by 2035 at a 13.1% CAGR. Ethernet, fiber optic, and industrial fieldbus connections remain preferred in fixed environments such as factories, data centers, hospitals, and energy infrastructure. Wired networks offer deterministic bandwidth and lower exposure to electromagnetic interference, which makes them suitable for closed-loop control systems and safety-critical applications. Industrial fog architectures built around Siemens Industrial Edge, Rockwell FactoryTalk, and Cisco rugged routing products commonly retain wired backbones even when wireless access is added for mobile assets.

Wireless connectivity accounted for USD 172.4 million in 2025, or 42.5% of the fog computing market, and is forecast to reach USD 1,032.6 million by 2035 at a 19.8% CAGR. Private 5G, Wi-Fi 6/6E, LPWAN, and MEC architectures are widening deployment options in ports, mining sites, smart cities, and transportation corridors. Cisco Meraki MG51/MG51E gateways, Nokia Digital Automation Cloud, Ericsson private-network offerings, Qualcomm edge platforms, and Cradlepoint connectivity systems are important products and platforms in this segment. The pricing dynamic favors bundled connectivity-and-compute solutions where customers can reduce commissioning time and manage distributed sites through a unified operating layer.

By Industry Vertical

Manufacturing was the leading vertical in the fog computing market in 2025, accounting for USD 97.7 million, or 24.1% of revenue, and is projected to reach USD 399.7 million by 2035 at a 15.4% CAGR. IT & Telecom generated USD 73.2 million, or 18.1%, and is growing at a 17.6% CAGR as operators deploy MEC infrastructure for low-latency applications. Healthcare & Life Sciences generated USD 40.3 million in 2025 and is the fastest-growing vertical at a 19.6% CAGR, reaching USD 236.2 million by 2035. WHO guidance supporting digital health infrastructure investment in emerging economies provides a broader policy backdrop for connected healthcare adoption.

Energy & Utilities contributed USD 48.6 million in 2025, BFSI and Transportation & Logistics each represented USD 32.4 million, Government & Defense contributed USD 36.5 million, and Retail & E-Commerce generated USD 28.4 million. Retail & E-Commerce is forecast to reach USD 145.4 million by 2035 at an 18% CAGR, supported by in-store AI analytics, inventory visibility, and checkout automation. BFSI deployments focus on fraud detection, branch modernization, and latency-sensitive transaction workflows, while government and defense use cases emphasize resilience and data sovereignty. The vertical mix shows that fog computing is not a single-sector technology; it is becoming a cross-industry infrastructure model where local data processing improves speed, compliance, and operating continuity.

By Region

North America Fog Computing Market

North America held the largest market position in 2025 at USD 168 million, equal to 41.5% of global revenue, and is projected to reach USD 778.7 million by 2035 at a 16.8% CAGR. The United States accounted for USD 148.4 million in 2025, supported by defense edge computing, smart-grid modernization, healthcare digitization, financial-services automation, and enterprise IoT deployments. Canada contributed USD 19.6 million and is expanding at a 19.8% CAGR, with Toronto, Vancouver, and Montreal supporting smart-city initiatives and industrial IoT adoption in energy and mining. The U.S. Department of Energy’s grid modernization programs and NIST’s cybersecurity framework for edge computing give buyers a clearer technical and regulatory reference point. Conversations with 24 channel partners and systems integrators across the United States, Germany, Singapore, and the UAE during our Q2 2026 expert panel pointed to vendor credibility, cybersecurity tooling, and post-deployment support as decisive factors in fog platform selection.

Europe Fog Computing Market

The Europe market generated USD 103.8 million in 2025, representing 25.6% of global revenue, and is forecast to reach USD 424.8 million by 2035 at a 15.4% CAGR. Germany led European demand at USD 33.8 million in 2025 and is projected to reach USD 151.5 million by 2035, reflecting its manufacturing base and Industrie 4.0 investment cycle. GDPR and the European Commission’s Digital Decade initiative are central policy forces because both strengthen demand for local data processing and industrial digital infrastructure. The United Kingdom, France, Italy, and Nordic countries contribute to the Rest of Europe segment, which generated USD 70 million in 2025. At the regional level, adoption is strongest where precision manufacturing, telecom investment, and data-sovereignty requirements intersect.[6]European Commission, https://commission.europa.eu

Asia Pacific Fog Computing Market

The Asia Pacific market generated USD 81.6 million in 2025 and is the fastest-growing regional market, with an 18.6% CAGR through 2035 and a forecast value of USD 442.2 million. China accounted for USD 45.8 million in 2025 and is projected to reach USD 223.9 million by 2035, supported by the New Infrastructure program targeting 5G networks, industrial internet platforms, and smart-city systems. India, Japan, South Korea and Southeast Asia make up the Rest of APAC segment, which generated USD 35.9 million in 2025 and is growing at a 20% CAGR. Japan’s Society 5.0 initiative, South Korea’s Digital New Deal, and India’s smart cities mission are creating demand for fog nodes in factories, public infrastructure, transport systems, and digital government platforms. Interviews we conducted with 31 telecom and smart-city program leads across China, India, the UAE, and Brazil in H1 2026 converged on one operating constraint: city-scale fog deployments require local systems integration capacity as much as network bandwidth, especially as Dubai, Abu Dhabi, Sao Paulo, and Rio de Janeiro expand connected infrastructure programs.

Fog Computing Market Share

The market showed moderate concentration in 2025, with the top five suppliers holding 44.3% of global revenue. Dell Technologies led the market with a 10.5% share, followed by Cisco Systems at 9.8%, IBM Corporation at 8.8%, Microsoft Corporation at 7.9%, and Intel Corporation at 7.3%. This structure reflects the market’s technical requirements. Large enterprises want vendors that can support hardware, networking, orchestration, cybersecurity, cloud integration, and services across multi-site deployments.

Dell Technologies holds the strongest position because its PowerEdge XR ruggedized servers and edge infrastructure portfolio fit industrial, telecom, government, and enterprise fog environments. The company benefits from a broad partner network and the ability to bundle compute, storage, networking, and deployment support. Cisco Systems competes from the network layer, using Edge Fog Fabric, Cisco Edge Intelligence, Meraki 5G gateways, Cisco IOx, and rugged routers to link connectivity with application hosting. Its March 2025 Cisco Secure AI Factory announcement with NVIDIA strengthened its positioning in AI-enabled fog infrastructure.

IBM remains a major competitor through IBM Edge Application Manager, consulting services, enterprise software relationships, and infrastructure automation. The January 2025 acquisition of HashiCorp for USD 7.1 billion deepened IBM’s automation capabilities and improved its ability to manage distributed fog resources across multi-cloud environments. Microsoft Corporation competes through Azure IoT Edge, Azure Stack Edge, and Azure Industrial Edge, giving customers a cloud-managed path for factory-edge analytics and AI inference. Intel Corporation occupies a foundational role because Xeon Scalable, Atom, and Core processors provide the compute substrate for a large portion of enterprise fog hardware, while OpenVINO supports edge AI inference optimization.

M&A activity is intensifying as vendors seek software, automation, and distributed-site management capabilities. Acumera’s July 2025 acquisition of Scale Computing created a larger edge platform provider managing deployments across more than 50,000 distributed enterprise locations. Nimble Gravity’s August 2025 acquisition of Fog Solutions expanded its data and AI consulting capabilities tied to Azure and Databricks. These moves indicate that scale in the fog computing market is not only about installed hardware; it also depends on the ability to manage applications, data pipelines, and customer outcomes across thousands of locations.

Competition outside the top five includes NVIDIA Corporation, AWS, HPE, Siemens AG, GE, Huawei Technologies, Ericsson, Nokia Corporation, Rockwell Automation, Schneider Electric, Bosch, Arm Holdings, Qualcomm Technologies, VMware (Broadcom), Red Hat, FogHorn Systems, Litmus Automation, MobiledgeX, Vapor IO, mimik Technology, Cradlepoint, Adlink Technology, Kontron, and Niobium. Specialist vendors can win where vertical knowledge matters, especially in manufacturing, smart energy, telecom, retail, and smart-city systems. Over the forecast period, the market is likely to consolidate gradually as buyers favor vendors that combine secure infrastructure, lifecycle management, AI support, and system-integration depth.

Fog Computing Market Companies

Major players operating in the fog computing industry are:

Major players operating in the fog computing market are: Dell Technologies, Cisco Systems, IBM Corporation, Microsoft Corporation, Intel Corporation, NVIDIA Corporation, Amazon Web Services (AWS), Hewlett Packard Enterprise (HPE), Siemens AG, General Electric (GE), Huawei Technologies, Ericsson, Nokia Corporation, Rockwell Automation, Schneider Electric, Bosch, Arm Holdings, Qualcomm Technologies, VMware (Broadcom), Red Hat (IBM), FogHorn Systems, Litmus Automation, MobiledgeX, Vapor IO, Scale Computing (Acumera), mimik Technology, Cradlepoint, Adlink Technology, and Kontron.

Dell Technologies is positioned around ruggedized infrastructure, hybrid management, and enterprise channel depth. Its PowerEdge XR series and Dell APEX Cloud Platforms support customers that need fog nodes in factories, telecom sites, transportation locations, and government facilities. Cisco Systems brings a network-centric strategy through Cisco Edge Intelligence, IR1100 Rugged Series routers, Meraki edge appliances, IOx application hosting, and 5G gateway products. That portfolio makes Cisco especially relevant where network operations and local compute need to be deployed together.

IBM focuses on orchestration, consulting, and enterprise software integration through IBM Edge Application Manager and its broader automation portfolio. The HashiCorp acquisition strengthens infrastructure automation, which is increasingly important as fog deployments scale across mixed cloud, edge, and on-premise systems. Microsoft Corporation is building the fog computing market through Azure IoT Edge, Azure Stack Edge, and Azure Industrial Edge, with a platform strategy centered on cloud-to-fog management and AI integration. AWS competes through AWS Greengrass and cloud-native edge services, while Red Hat and VMware (Broadcom) support enterprises that want containerized and virtualized distributed infrastructure.

Intel is the silicon anchor for much of the market. Xeon Scalable, Atom, and Core processors power fog servers and gateways, while OpenVINO helps optimize AI inference at the edge. NVIDIA Corporation extends the AI side of the market through GPU compute platforms used in video analytics, robotics, and industrial inference. Arm Holdings and Qualcomm Technologies matter in lower-power and wireless fog environments where energy efficiency, embedded processing, and device-level integration shape hardware choices.

Industrial and automation specialists give the market vertical depth. Siemens AG uses MindSphere and Industrial Edge to serve manufacturing and process industries, while Rockwell Automation integrates fog capabilities into FactoryTalk and its industrial IoT strategy. Schneider Electric, Bosch, GE, Litmus Automation, FogHorn Systems, Adlink Technology, and Kontron address operational environments where equipment integration, industrial protocols, and reliability carry more weight than general-purpose cloud functionality. Nokia Corporation, Ericsson, Cradlepoint, Huawei Technologies, and MobiledgeX compete around private networks, MEC, and telecom-aligned fog infrastructure.

Several smaller firms are widening the market’s technical range. mimik Technology is advancing device-first distributed AI through its Continuum AI platform and international expansion plans, including the November 2025 MOU to establish mimik UAE in Abu Dhabi. Niobium introduced The Fog in April 2026, using fully homomorphic encryption to support AI workloads on data that remains encrypted. Vapor IO and Scale Computing (Acumera) support distributed edge infrastructure and virtualization requirements. Collectively, these companies indicate that the fog computing market is becoming a layered supplier environment, with value distributed across silicon, hardware, networking, orchestration, cybersecurity, applications, and managed services.

10.5% Market Share

Collective Market Share in 2025 is 44.3%

Fog Computing Industry News

Fog Computing Market Concentration Score

The fog computing market concentration score is 5 out of 10, as the top five vendors held 44.3% share in 2025 while the remaining demand was distributed across cloud providers, telecom vendors, industrial automation firms, edge specialists, and systems integrators.

The fog computing market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Component

Market, By Deployment Model

Market, By Application

Market, By Industry Vertical

Market, By Network Connectivity

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

Chapter 6 Market Estimates & Forecast, By Deployment Model, 2022 - 2035 ($Mn)

Chapter 7 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

Chapter 8 Market Estimates & Forecast, By Network Connectivity, 2022 - 2035 ($Mn)

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2022 - 2035 ($Mn)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →