Forestry Equipment Market Size & Share 2026-2035

Market Size By Equipment Type (Feller Bunchers, Skidders, Loaders, Chippers and Processors, Others), By Technology (Manual/Semi-Automatic, Fully Automatic), By Power Source (Diesel-Powered, Hybrid, Electric), By Application (Logging, Land Clearing, Construction), and By End Use (Forestry Companies, Government Agencies, Construction Companies, Individuals). The market forecasts are provided in terms of value (USD Billion) and volume (Units).

Report ID: GMI4580

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Authors:

Preeti Wadhwani, Aishvarya Ambekar

Forestry Equipment Market Size

The global forestry equipment market was estimated at USD 12.2 billion in 2025. The market is expected to grow from USD 12.3 billion in 2026 to USD 18.6 billion in 2035, at a CAGR of 4.7%, according to latest report published by Global Market Insights Inc.

Forestry Equipment Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

The market volume was estimated at 39,998 units in 2025. The market is projected to grow from 40,476 units in 2026 to 50,992 units by 2035, registering strong double-digit growth over the forecast period.

The growth of forestry and land development activities is significantly transforming the market, driven by rising demand for timber, pulpwood, and biomass resources. Increasing urbanization, infrastructure development, and commercial forestry expansion are accelerating the need for efficient and high-productivity logging equipment. Traditionally reliant on manual or semi-mechanized harvesting methods, the forestry industry has transitioned toward advanced mechanized solutions such as forestry market expertise, which enhance operational efficiency, reduce labor dependency, and improve safety standards in challenging environments.

Growing concerns around labor shortages and worker safety are further strengthening the adoption of forestry market expertise across key forestry regions. Logging operations are inherently hazardous, and companies are increasingly prioritizing mechanized equipment that minimizes human exposure to risks such as falling trees and heavy machinery accidents. Modern forestry market expertise are equipped with enclosed operator cabins, ergonomic controls, and advanced safety systems, ensuring safer and more controlled tree harvesting processes while maintaining high productivity levels.

Rising emphasis on operational efficiency and cost optimization is also reshaping the market landscape. Forestry companies are investing in high-capacity equipment capable of handling large volumes of timber with minimal downtime. Forestry market expertise enable faster tree cutting and accumulation, reducing cycle times and improving overall harvesting efficiency. Additionally, integration with other forestry equipment such as skidders and harvesters allows for streamlined workflows, optimized resource utilization, and reduced operational costs across logging operations.

For instance, in March 2025, John Deere introduced upgraded feller buncher models featuring enhanced hydraulic systems, improved fuel efficiency, and advanced telematics for real-time machine performance monitoring. These innovations are aimed at improving productivity, reducing fuel consumption, and enabling predictive maintenance across large-scale forestry operations.

The increasing scale and mechanization of forestry operations are driving demand for technologically advanced and high-performance forestry market expertise. Large forestry companies are adopting fleet-based approaches, deploying multiple machines across vast harvesting sites to maximize output and maintain consistent production levels. This trend is particularly prominent in regions with industrial forestry practices, where efficiency, speed, and reliability are critical to meeting growing timber demand.

Technological advancements are playing a transformative role in redefining feller buncher capabilities. Features such as GPS-based tracking, telematics systems, automated cutting controls, and real-time diagnostics are becoming standard in modern machines. These technologies enable better machine utilization, reduced downtime, and data-driven decision-making. Additionally, innovations in cutting heads, boom design, and hydraulic efficiency are improving precision, durability, and overall machine performance in diverse forestry conditions.

North America and Europe represent mature markets for forestry market expertise, supported by well-established forestry industries, high mechanization rates, and strong presence of leading equipment manufacturers such as Tigercat and Komatsu. These regions continue to witness steady demand driven by replacement cycles and technological upgrades.

Asia-Pacific is emerging as a high-growth market, fueled by increasing commercial forestry activities, infrastructure development, and rising adoption of mechanized logging practices. Countries such as China, India, and Southeast Asian nations are witnessing growing demand for efficient and cost-effective forestry equipment, supported by government initiatives promoting sustainable forest management and industrial development.

Forestry Equipment Market Trends

The adoption of telematics and Internet of Things (IoT) technologies is transforming feller buncher operations by enabling real-time monitoring of machine performance, fuel consumption, and location tracking. These systems provide actionable insights that help operators optimize productivity, schedule predictive maintenance, and reduce downtime. Forestry companies are increasingly leveraging data-driven decision-making to improve efficiency and lower operational costs, making connected machinery a standard requirement in modern logging environments.

Forestry operators are increasingly demanding high-capacity forestry market expertise capable of handling larger volumes of timber within shorter timeframes. Additionally, there is a growing preference for multi-functional machines that can perform multiple tasks, reducing the need for additional equipment. This trend enhances operational efficiency and lowers overall costs by streamlining workflows. Manufacturers are responding by developing machines with improved cutting heads, extended reach, and higher load-handling capabilities to meet evolving industry requirements.

In April 2025, Tigercat introduced the L857 feller buncher, engineered for steep terrain operations. The machine offers enhanced stability, improved traction, and higher productivity, enabling efficient harvesting in challenging landscapes while addressing growing demand for specialized, high-performance forestry equipment.

Improving operator comfort and safety has become a key priority in the design of modern forestry market expertise. Advanced cabin designs with ergonomic seating, climate control, reduced noise levels, and enhanced visibility are being incorporated to reduce operator fatigue during long working hours. Safety features such as reinforced structures, advanced control systems, and better stability are also being emphasized. These improvements not only enhance worker well-being but also contribute to increased productivity and reduced accident risks in demanding forestry environments.

The increasing cost of purchasing forestry market expertise is driving the adoption of rental and leasing models, particularly among small and medium-sized contractors. Rental services provide access to advanced machinery without requiring significant upfront investment, offering flexibility in operations. This trend is gaining traction in emerging markets were financial constraints limit equipment ownership. Additionally, rental models allow companies to scale operations based on project demand, improving cost efficiency and reducing financial risks associated with asset ownership.

Forestry Equipment Market Analysis

Based on equipment type, the market is divided into feller bunchers, skidders, loaders, chippers and processors, and others. The feller bunchers segment dominated the forestry equipment market, accounting for around 30.2% in 2025 and is expected to grow at a CAGR of more than 4.9% through 2035.

The skidders segment is expected to experience faster growth of more than 5.4% over the forecast period, driven by increasing demand for efficient timber extraction in challenging terrains. Skidders are essential for transporting felled logs from steep slopes and dense forests to landing areas, reducing manual labor and operational time. Their adaptability to different ground conditions, coupled with advancements in winching systems, all‑terrain mobility, and fuel efficiency, has made them increasingly preferred in both commercial and sustainable forestry operations.

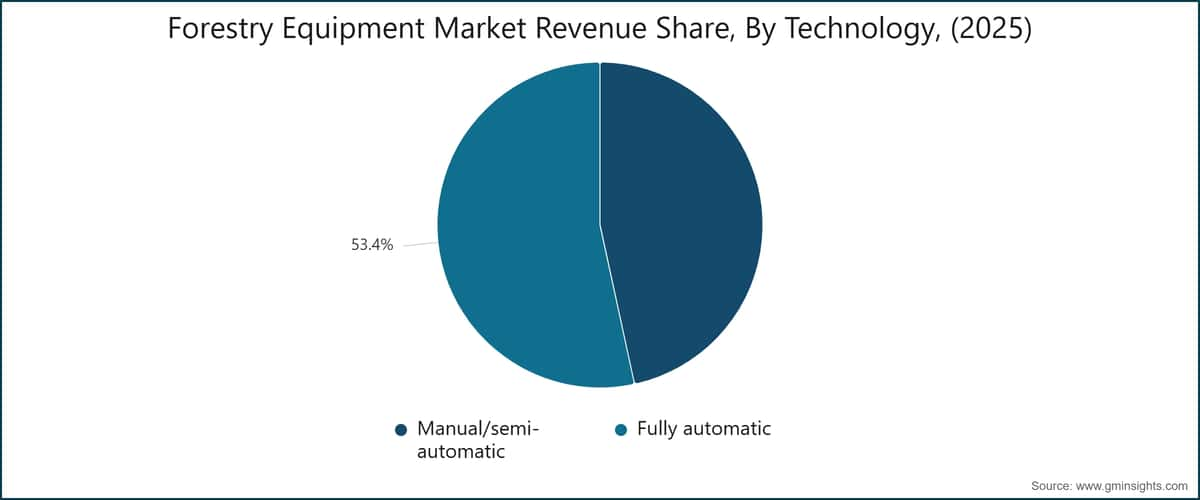

Based on technology, the market is categorized into manual/semi-automatic, and fully automatic. The manual/semi-automatic segment dominates the market accounting for around 53.4% share in 2025, and the segment is expected to grow at a CAGR of over 4% from 2026-2035.

Based on end use, the global forestry equipment market is divided into forestry companies, government agencies, construction companies, and individuals. The forestry companies segment held the major market share in 2025.

Based on application, the forestry equipment market is divided into logging, land clearing, and construction. The Logging segment dominated the market.

U.S. dominated the forestry equipment market in North America with around 83.58% share and generated USD 3.04 billion in revenue in 2025.

The forestry equipment market in Germany is expected to experience significant and promising growth from 2026 to 2035.

The forestry equipment market in China is expected to experience significant and promising growth from 2026-2035.

The forestry equipment market in Brazil is expected to experience significant and promising growth from 2026 to 2035.

The forestry equipment market in UAE is expected to experience significant and promising growth from 2026-2035.

Forestry Equipment Market Share

Forestry Equipment Market Companies

Major players operating in the forestry equipment industry are:

Forestry Equipment Industry News

The forestry equipment market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($Bn), Volume (Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Equipment Type

Market, By Technology

Market By Power Source

Diesel-powered

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries:

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →