Authors:

Avinash Singh, Amit Patil

Download free PDF

Europe Secondhand Camera and Lens Market Size & Share 2026-2035

Report ID: GMI13299

|

Published Date: February 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Europe Secondhand Camera and Lens Market

Get a free sample of this report

Get a free sample of this report Europe Secondhand Camera and Lens Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Europe Secondhand Camera and Lens Market Size

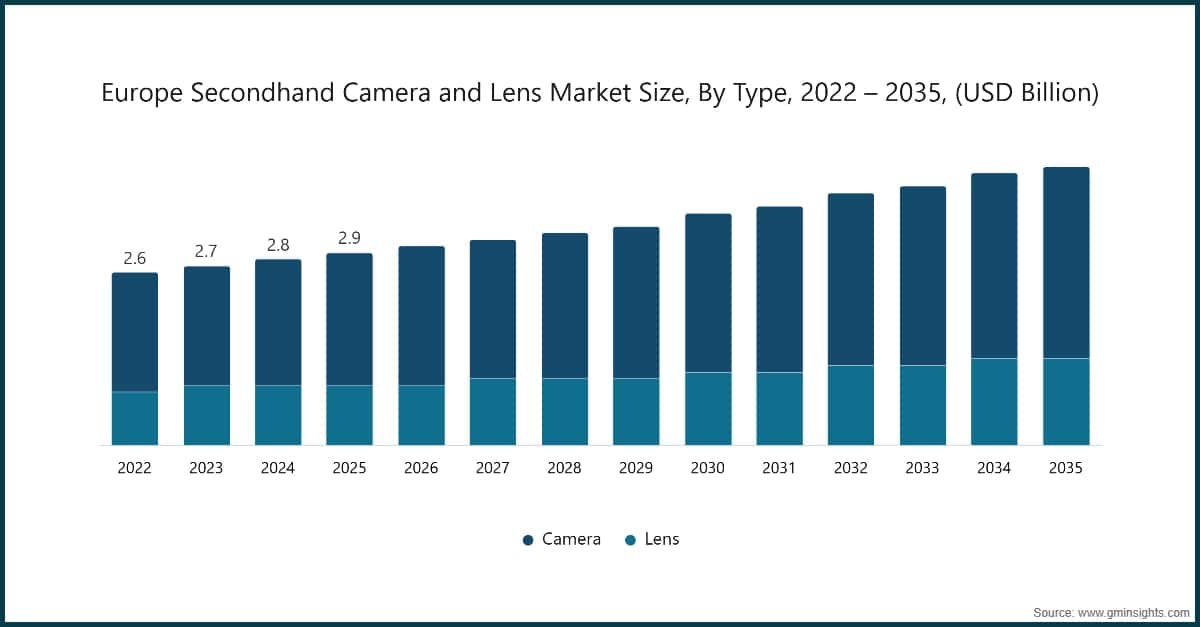

The Europe secondhand camera and lens market was estimated at USD 2.9 billion in 2025. The market is expected to grow from USD 3 billion in 2026 to USD 4.25 billion in 2035, at a CAGR of 3.9% according to latest report published by Global Market Insights Inc.

Europe Secondhand Camera and Lens Market Key Takeaways

Second-hand cameras and lenses: These are pre-owned cameras and lenses for resale once they are initially used and come at a discounted cost because they are second-hand. This market includes second-hand digital cameras and lenses, second-hand film cameras and lenses, and second-hand professional cameras and lenses because they come with plenty of working life left in them. Clients would like second-hand cameras and lenses because they are cheap and come in lots. Clients can also buy second-hand cameras and lenses to move up to higher levels in their products.

The European market for second-hand cameras and lenses has come up as a vibrant and swiftly growing segment, driven by the need for affordability, sustainability, and changing consumer behaviors. The market has gained immense popularity with the increasing need for affordable solutions compared to the high costs associated with the purchase of new products. The need for affordable options has moved in tandem with the worldwide market for second-hand imaging equipment, in which the concern for sustainability has driven the interest in photography. Europe has been at the forefront of the global shift towards circular economy, advocating the reuse of photography equipment to achieve sustainability.

Another highly influential factor that has impacted the market is the transition from DSLRs to mirrorless camera systems. Mirrorless cameras have gained immense popularity, even surpassing DSLRs in terms of sales in new, as well as secondhand, markets. This has mainly been driven by young photographers, YouTubers, or video makers, who appreciate the versatility, portability, and advanced capabilities associated with mirrorless cameras. Based on consumer behavior and market search trends, it has been observed that people have been preferring to buy used mirrorless cameras, which has increased steadily, even surpassing DSLRs. Consequently, this has resulted in an increase in the availability of secondhand DSLRs, along with lenses, in the market, but simultaneously increasing the turn-over rate, or even the price, for mirrorless camera systems.

According to the Camera & Imaging Products Association (CIPA), it is discovered that the total number of lenses and camera bodies shipped in 2024 was 8% above year on year, and this is indicative of growing demand for high end photographic equipment. Moreover, the average retail price of lenses and cameras has increased by 3%, which shows the premium trend of the market. Sustainability and environmental consciousness are the factors propelling the Europe secondhand camera and lens market growth. Most photographers desire to have sustainable options in this age due to global warming. Since the need for second-hand cameras is increasing, users can limit electronic waste and contribute to a circular buying method. According to the most recent MPB impact report, MPB generated 35% of electricity from renewable sources, achieved 100% plastic-free packaging throughout the year and delivered zero waste to landfill.

MPB's approach to sustainability is founded on three themes across which the business invests and monitors its performance such as circular and renewable, inclusive and diverse, and trusted and ethical. Throughout its Circular and Renewable objectives, MPB announced that it is recycling 570,000 cameras, lenses and accessories annually. MPB remains a zero-waste-to-landfill company. Through its strong recycling and reuse initiatives throughout its four locations, MPB recycled an average of 69% of office and warehouse waste.

Lenses play a crucial role in the growth of the second-hand camera and lens market in Europe. Standard and prime lenses continue to dominate the market, holding the largest share due to their versatility and widespread use across various photography styles. However, telephoto and zoom lenses are emerging as the fastest-growing segments, driven by increasing interest in wildlife, sports, and long-range photography. The growing popularity of these lenses is supported by advancements in sensor technology and the availability of adapter systems, which enhance compatibility and usability across different camera models. These factors contribute to the long-term resale value of lenses, making them a vital component of the second-hand market. The accessibility of online marketplaces has further facilitated the growth of this segment, enabling consumers to explore a wide range of options and make informed purchasing decisions.

Europe Secondhand Camera and Lens Market Trends

The Europe pre‑owned imaging market is mid‑transition from a fragmented, listing‑led space to a trust‑engineered, platform‑driven ecosystem that emphasizes grading rigor, warranties, and rapid cross‑border logistics. The best in the business is putting out into the marketplace solutions that are at the bleeding edge of innovation in the form of automatic condition and solutions that come with properties like intelligent MEMS sensors, AI-powered algorithms, and edge analytics.

Europe Secondhand Camera and Lens Market Analysis

Based on the type, the market is segmented into camera and lens. In 2025, the camera segment holds the largest market share of 68.6% with generating a revenue of USD 2.92 billion.

Based on the product condition, the Europe secondhand camera and lens market is segmented into used/pre-owned cameras & lenses and refurbished cameras & lenses. In 2025, used/pre-owned cameras & lenses held the major market share of 68%, reflecting the industry’s heavy reliance on high-value asset protection.

Based on the end user, the Europe secondhand camera and lens market is segmented into professional photographers, semi-professional, amateur/hobbyist and institutional/educational. In 2025, professional photographers held the major market share of 30%, reflecting the industry’s application for camera and lens.

The Europe secondhand camera and lens market dominate with a revenue share of 68.6% in 2025. This growth is increasingly influenced by sustainability initiatives and reached USD 2.9 billion in 2025.

Europe Secondhand Camera and Lens Market Share

Europe Secondhand Camera and Lens Market Companies

Major players operating in the Europe secondhand camera and lens industry are:

Fnac Darty strengthened its strategic position in Southern Europe through the acquisition of Unieuro, Italy’s leading consumer electronics and appliances retailer; this transaction expanded the Group’s regional footprint, enhanced purchasing synergies exceeding 22 million USD, and reinforced its omnichannel capabilities across key European markets.

Europe Secondhand Camera and Lens Market News

The Europe secondhand camera and lens market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Billion) and volume (Thousand Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market By Type

Market By Product Condition

Market By Price Range

Market By End User

Market By Distribution Channel

Market By Country

Table of Contents

Chapter 1 Methodology and Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Type, 2022 – 2035 (USD Million) (Thousand Units)

Chapter 6 Market Estimates and Forecast, By Product Condition, 2022 – 2035 (USD Million) (Thousand Units)

Chapter 7 Market Estimates and Forecast, By Price Range, 2022 – 2035 (USD Million) (Thousand Units)

Chapter 8 Market Estimates and Forecast, By End User, 2022 – 2035 (USD Million) (Thousand Units)

Chapter 9 Market Estimates and Forecast, By Region, 2022 – 2035 (USD Million) (Thousand Units)

Chapter 10 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →