Market Size By – Device Type (Diagnostic and Monitoring Devices, Therapeutic and Surgical Devices), By Application (Coronary Artery Disease, Cardiac Arrhythmia, Heart Failure, Other Applications), By End Use (Hospitals, Ambulatory Surgical Centers, Cardiac Centers, Other End Users) – Growth Forecast. The market forecasts are provided in terms of revenue (USD).

Report ID: GMI4949

|

Published Date: August 2026

|

Report Format: PDF

Download Free PDF

Cardiovascular Devices Market Size

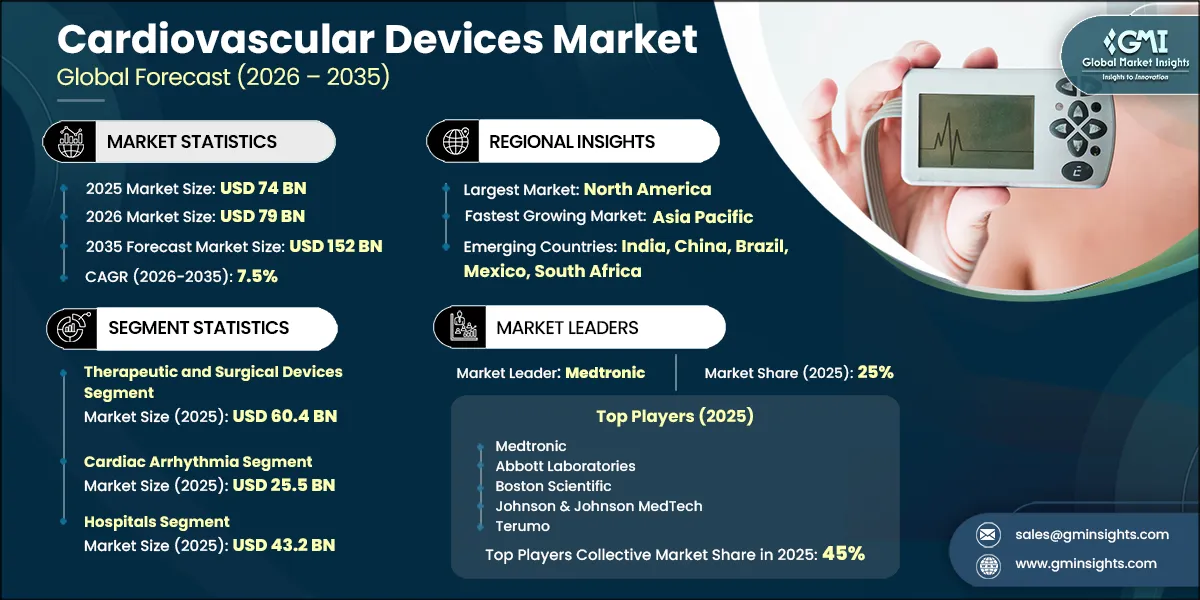

The global cardiovascular devices market was valued at USD 74 billion in 2025 and is projected to grow from USD 79 billion in 2026 to USD 152 billion by 2035, expanding at a CAGR of 7.5%, according to the latest report published by Global Market Insights Inc.

This substantial growth is driven by an increasing number of patients suffering from cardiovascular diseases, an expanding geriatric population, rising government initiatives, technological advancements in cardiovascular devices, and rising demand for minimally invasive procedures.

The increasing global burden of cardiovascular diseases (CVDs) is a significant catalyst driving the growth of the cardiovascular devices market. According to the World Health Organization, an estimated 19.8 million people died from CVDs in 2022, accounting for approximately 32% of all global deaths, with 85% of these fatalities caused by heart attacks and strokes. This alarming prevalence reflects the growing impact of sedentary lifestyles, rising obesity rates, unhealthy dietary patterns, tobacco use, and harmful alcohol consumption. As populations age and chronic disease risk factors become more widespread, healthcare systems face increasing demand for early diagnosis, continuous monitoring, and advanced treatment options. This trend is accelerating the adoption of minimally invasive cardiovascular devices, next-generation stents, implantable cardiac devices, wearable heart monitors, and AI-assisted diagnostic tools. Additionally, rising awareness of preventive cardiac care and expanding access to healthcare in emerging economies are further boosting device utilization. Collectively, the escalating global CVD burden and the urgent need for effective diagnostic and therapeutic solutions position this trend as a critical driver of sustained growth in the cardiovascular devices market.

The rising demand for minimally invasive procedures is a key driver of the cardiovascular devices market, as patients and healthcare providers increasingly prefer treatments that reduce surgical trauma, shorten hospital stays, lower complication risks, and enable faster recovery. Minimally invasive cardiovascular interventions, such as catheter-based angioplasty, transcatheter aortic valve replacement (TAVR), cardiac ablation, and percutaneous coronary interventions (PCI), are witnessing growing adoption due to their clinical effectiveness and improved patient outcomes compared to traditional open-heart surgeries. This trend is driving demand for advanced cardiovascular devices, including catheter systems, guidewires, coronary stents, transcatheter heart valves, and electrophysiology devices. Furthermore, continuous technological advancements in imaging, robotic-assisted procedures, and precision-guided catheter technologies are enhancing procedural accuracy and safety, further accelerating the growth of the cardiovascular devices market.

Cardiovascular devices are medical instruments, tools, and implantable or external systems designed to monitor, support, or restore the normal functioning of the heart and blood vessels. These devices help detect abnormalities, maintain circulation, regulate heart rhythm, improve blood flow, or assist in the diagnosis and long-term management of cardiovascular conditions.

Cardiovascular Devices Market Trends

Technological advancements are one of the drivers of growth in the global cardiovascular devices market. Innovations in device design, materials, miniaturization, and digital integration have significantly improved the accuracy, safety, and clinical usability of cardiovascular solutions.

Structural heart segment (TAVR, mitral) growth is a major trend driving expansion in the cardiovascular devices market. The increasing adoption of transcatheter therapies, particularly TAVR, is supported by expanding indications into low-risk patient populations and growing physician confidence in minimally invasive valve replacement procedures. In addition, the mitral and tricuspid intervention space is witnessing rapid innovation, with new repair and replacement technologies improving clinical outcomes. These advancements are shifting treatment from open-heart surgery to catheter-based approaches, thereby increasing procedure volumes and accelerating segment growth.

The electrophysiology (EP) and ablation segment is experiencing strong growth due to the rising prevalence of cardiac arrhythmias, particularly atrial fibrillation. Continuous technological advancements, including the development of high-precision mapping systems and next-generation ablation techniques such as pulsed field ablation, are enhancing procedural safety and effectiveness. These innovations enable shorter procedure times and improved success rates, driving higher adoption among electrophysiologists. As awareness and diagnosis of rhythm disorders increase, the demand for EP procedures continues to expand across global healthcare settings.

The pacing devices segment is characterized by steady growth, supported by the increasing incidence of bradycardia and other conduction disorders associated with aging populations. Technological advancements such as leadless pacemakers, MRI-compatible devices, and extended battery life are improving patient outcomes and device longevity. Additionally, the integration of remote monitoring and wireless connectivity is enhancing long-term patient management and reducing hospital visits. These developments are strengthening the clinical value of pacing systems and supporting their continued adoption across cardiac care environments.

Cardiovascular Devices Market Analysis

Based on device type, the market is segmented into diagnostic and monitoring devices, and therapeutic and surgical devices. The therapeutic and surgical devices segment held revenue of USD 60.4 billion in 2025.

The therapeutic and surgical devices segment includes a broad suite of life-sustaining cardiovascular tools such as catheters, coronary intervention devices, cardiac rhythm management devices, structural heart devices, and cardiac surgery tools. These devices directly restore or replace essential cardiac function, positioning them at the core of interventional cardiology and cardiac surgery.

Therapeutic and surgical devices dominate the market because they offer definitive treatment solutions, often required urgently in life-threatening heart conditions. Continuous innovation, such as minimally invasive catheters, next-generation stents, durable heart valves, and smaller, smarter cardiac rhythm devices, enhances procedural success, reduces hospital stays, and expands eligibility for high-risk patients.

For instance, in the U.S. alone, about 3 million people currently live with a pacemaker, and around 200,000 new pacemakers are implanted each year for patients suffering from bradycardia or abnormal heart rhythms. This sustained, high-volume implantation rate demonstrates the essential role of therapeutic and surgical cardiac devices in ongoing patient management and underscores why this segment commands the largest share of the market.

Therefore, the therapeutic and surgical devices segment maintains a dominant position in the cardiovascular devices market because it delivers indispensable, life-saving interventions that address the most critical cardiac conditions.

The diagnostic and monitoring devices segment is projected to expand at a 7.1% CAGR to reach USD 26.9 billion by 2035. The diagnostic and monitoring devices segment in the cardiovascular devices market is experiencing steady growth, supported by the increasing focus on early disease detection, continuous patient monitoring, and preventive care. This segment includes devices such as electrocardiograms (ECG), Holter monitors, event recorders, and implantable loop recorders, which are widely used across clinical and outpatient settings. Their ability to provide real-time insights into cardiac function enables timely diagnosis of arrhythmias and other cardiovascular abnormalities, improving clinical outcomes and reducing the risk of complications.

Advancements in digital health technologies have significantly enhanced the capabilities of diagnostic and monitoring devices. The integration of wireless connectivity, wearable formats, and AI-driven analytics allows for remote patient monitoring and more accurate interpretation of cardiac data. These innovations are driving greater adoption across home-care settings and ambulatory care centers, while also supporting more personalized and data-driven treatment approaches, thereby strengthening the role of this segment within the broader cardiovascular care ecosystem.

Based on application, the cardiovascular devices market is segmented into coronary artery disease, cardiac arrhythmia, heart failure, and other applications. The cardiac arrhythmia segment dominated the market with the largest revenue of USD 25.5 billion in 2025.

Cardiac arrhythmia accounts for a major share of the cardiovascular devices market because of its high global prevalence and the increasing number of patients requiring continuous monitoring and intervention. Irregular heart rhythms such as atrial fibrillation, tachycardia, and bradycardia are becoming more common as aging populations rise, and lifestyle-related risk factors such as obesity, hypertension, and diabetes increase worldwide. This creates sustained demand for diagnostic and therapeutic solutions.

Advancements in arrhythmia-related technologies further reinforce the strong market position of the cardiac arrhythmia segment. Innovations such as AI-enabled ECG interpretation, advanced catheter ablation systems, and remote monitoring platforms allow clinicians to diagnose arrhythmias earlier and manage them more effectively. Hospitals and cardiology centers increasingly prefer these technologies because they reduce procedure time, improve treatment accuracy, and support personalized care. These benefits drive higher adoption, pushing arrhythmia-related devices ahead of other cardiovascular device categories.

The coronary artery disease segment is projected to expand at a 7.1% CAGR to reach USD 41.4 billion by 2035. The coronary artery disease (CAD) segment represents a key application area within the cardiovascular devices market, encompassing devices used for diagnosis, intervention, and long-term management of coronary blockages. This segment includes technologies such as coronary stents, angioplasty balloons, atherectomy devices, and diagnostic imaging tools that support percutaneous coronary interventions (PCI). The increasing prevalence of atherosclerosis, rising adoption of minimally invasive procedures, and continuous advancements in device design and drug-eluting technologies are contributing to sustained demand. improvements in procedural outcomes and reduced recovery times are supporting broader adoption across healthcare settings.

The heart failure segment is projected to expand at a 7.7% CAGR to reach USD 45 billion by 2035. The heart failure segment is driven by the growing burden of chronic cardiac conditions requiring long-term management and advanced therapeutic interventions. This segment includes devices such as cardiac resynchronization therapy (CRT) devices, implantable defibrillators (ICDs), ventricular assist devices (VADs), and hemodynamic monitoring systems. Increasing focus on improving patient survival rates, reducing hospital readmissions, and enhancing quality of life is supporting the adoption of these technologies. Ongoing innovations in device miniaturization, remote monitoring capabilities, and integration with digital health platforms are further strengthening the clinical utility of these solutions.

The other applications segment is projected to expand at a 6.9% CAGR to reach USD 11 billion by 2035. The other applications segment comprises a broad range of cardiovascular conditions, including peripheral vascular diseases, structural heart disorders, and congenital heart conditions. This segment includes diverse devices such as electrophysiology systems, heart valves, occlusion devices, and vascular intervention tools. The expansion of treatment indications, advancements in minimally invasive techniques, and increasing access to cardiovascular care are supporting growth across these application areas. Continuous innovation and the development of specialized devices tailored to specific clinical needs are further driving adoption within this segment.

Based on end use, the cardiovascular devices market is segmented into hospitals, ambulatory surgical centers, cardiac centers, and other end users. The hospitals segment accounted for USD 43.2 billion with a revenue share of 58.3% in 2025.

Hospitals represent a major end user segment in the cardiovascular devices market due to their advanced infrastructure, availability of multidisciplinary cardiology teams, and ability to manage both routine and complex cardiovascular conditions. They play a critical role in diagnostic procedures, interventional cardiology, cardiac surgeries, and the administration of device-based therapies such as stents, pacemakers, and cardiac monitoring systems. Hospitals offer comprehensive cardiovascular care under one roof, integrating emergency response, acute care, and long-term disease management.

Hospitals play an essential role in the early detection and prevention of cardiovascular diseases by offering structured diagnostic pathways, including echocardiography, cardiac stress tests, angiography, and advanced imaging modalities such as CT angiography and cardiac MRI.

Hospitals also support public health initiatives and clinical research by serving as major centers for cardiovascular screening programs and clinical studies involving new cardiac devices. Their integration with electronic health record (EHR) systems and adherence to cardiology guidelines ensures accurate treatment tracking, continuous patient monitoring, and improved outcomes across diverse patient populations.

The ambulatory surgical centres segment is projected to expand at an 8.4% CAGR to reach USD 21.7 billion by 2035. Ambulatory surgical centres represent a growing end user segment within the cardiovascular devices market, driven by the increasing shift toward minimally invasive procedures and cost-efficient care delivery models. These facilities are primarily utilized for outpatient procedures such as angioplasty, diagnostic catheterization, and device implantation, supported by advancements in technology that enable shorter procedure times and faster recovery. Favorable reimbursement policies and reduced hospital burden are further accelerating the adoption of cardiovascular interventions in ASC settings.

The cardiac centers segment is projected to expand at 8% CAGR to reach USD 27.9 billion by 2035. These centers are equipped with advanced infrastructure and skilled professionals to perform complex procedures such as electrophysiology studies, valve replacements, and interventional cardiology procedures. High patient volumes, availability of specialized expertise, and access to advanced technologies support the strong utilization of cardiovascular devices in these settings, making them critical to comprehensive cardiac care delivery.

The other end users segment is projected to expand at a 7.6% CAGR to reach USD 17 billion by 2035. The other end users segment includes diagnostic laboratories, home healthcare settings, and academic and research institutes that contribute to the broader utilization of cardiovascular devices. Academic and research institutions contribute to clinical studies, device validation, and innovation, supporting advancements in cardiovascular technologies and expanding their future applications.

North America Cardiovascular Devices Market

The North America region accounted for 41.8% of the global cardiovascular devices market in 2025. The cardiovascular devices market in North America is experiencing robust expansion, driven by the rising burden of cardiovascular diseases.

The U.S. cardiovascular devices market was valued at USD 23 billion and USD 24.5 billion in 2022 and 2023, respectively. The market size reached USD 28 billion in 2025, growing from USD 26.2 billion in 2024, and is anticipated to grow at a CAGR of 7.2% from 2026 to 2035.

North America continues to witness a high burden of cardiovascular diseases (CVDs), driven by sedentary lifestyles, obesity, and hypertension. This rising patient pool increases the demand for advanced diagnostic and therapeutic cardiovascular devices. According to the CDC, heart disease remains the leading cause of death across every racial and ethnic group and in both men and women. One person dies from cardiovascular disease in the U.S. every 34 seconds, and there were 919,032 deaths from cardiovascular diseases in 2023, accounting for 1 in every 3 deaths. This substantial public health burden pushes healthcare providers to prioritize early detection and continuous management, thereby supporting strong and sustained uptake of cardiovascular devices across the country.

Technological innovation further strengthens the market, as manufacturers introduce increasingly sophisticated solutions such as minimally invasive cardiac devices, AI‑enabled diagnostic tools, smart implantable, and remote monitoring platforms. These innovations support improved patient outcomes, reduce procedure time, and enhance long‑term disease management, making them highly attractive to U.S. health systems.

Europe Cardiovascular Devices Market

Europe's cardiovascular devices market accounted for USD 21.1 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

Europe’s rapidly aging population significantly contributes to rising cardiovascular disease incidence. Older adults typically experience higher rates of heart failure, arrhythmias, and coronary artery disease, driving device utilization.

For instance, according to Eurostat, in 2025, the EU population was estimated at 450.6 million people, and more than one-fifth (22.0%) of it was aged 65 years and over.

Europe’s strong medical technology ecosystem, supported by advanced R&D capabilities, high healthcare spending, and rapid adoption of digital health tools, accelerates the introduction of cutting-edge solutions such as smart pacemakers, electrophysiology mapping systems, and image-guided interventional devices.

These innovations enable earlier diagnosis, reduce procedure complexity, and enhance long-term patient outcomes, driving widespread clinical adoption and strengthening the overall market for cardiovascular technologies.

Asia Pacific Cardiovascular Devices Market

The Asia Pacific region is projected to show a lucrative growth of about 8.4% during the forecast period.

The region is witnessing rapid growth due to the rising prevalence of cardiovascular diseases. For example, according to the NIH, cardiovascular mortality in APAC is projected to increase by 91.2% from 2025 to 2050, indicating that there is an immediate need for new cardiac monitoring solutions.

Therefore, as the prevalence of cardiovascular diseases increases in the region, so does the requirement for cardiovascular devices, positively contributing to the growth of the market.

For instance, Japan’s cardiovascular devices market continues to grow steadily, supported by the rising number of individuals affected by cardiovascular conditions and the country’s rapidly aging population. According to the World Economic Forum, more than 1 in 10 people in Japan are now aged 80 years or older, making Japan the nation with the world’s oldest demographic structure.

Collaboration between academic institutions, government bodies, and private-sector companies is significantly enhancing the development of cardiovascular devices. These partnerships are accelerating innovation in mobile monitoring systems, telemetry solutions, and AI-driven technologies designed for advanced cardiovascular detection and management.

Latin America Cardiovascular Devices Market

Latin America is experiencing significant growth in the cardiovascular devices market.

The expansion of the Latin America cardiovascular devices market is strongly linked to rapid technological progress and the launch of advanced solutions for cardiac monitoring, alongside the increasing burden of cardiovascular diseases across the region’s population. Improving healthcare infrastructure and growing adoption of digital monitoring solutions are further supporting market growth.

According to the Pan American Health Organization (PAHO), noncommunicable diseases (NCDs) remain a major public health challenge in Latin America, accounting for approximately 77% of all deaths across the region, with cardiovascular diseases (CVDs) representing the leading cause of mortality and contributing to nearly 34% of total deaths.

Together, these factors highlight a strong and sustained need for advanced cardiovascular solutions in Latin America, reinforcing continuous market expansion as healthcare providers increasingly focus on early diagnosis, enhanced monitoring, and effective long-term management of cardiovascular conditions.

Middle East and Africa Cardiovascular Devices Market

The cardiovascular devices market in the Middle East and Africa is significantly driven by the rising number of individuals affected by cardiovascular diseases (CVDs).

The expansion of the Middle East & Africa (MEA) cardiovascular devices market is strongly linked to the rising prevalence of lifestyle‑related risk factors such as obesity, diabetes, hypertension, and sedentary behavior, which significantly increase the likelihood of cardiovascular complications. As these chronic conditions continue to grow across the region, healthcare providers are increasingly investing in advanced cardiovascular diagnostic and treatment technologies to effectively manage the expanding patient population.

Demographic trends across MEA are also contributing to market growth, with a steadily increasing middle‑aged and elderly population that is more susceptible to heart disease and requires long‑term cardiac care. This shift is driving demand for a broad range of cardiovascular devices, including monitoring systems, interventional technologies, and implantable devices. In response, hospitals and specialized cardiac centers are expanding their capabilities and adopting advanced technologies to enhance early detection, improve clinical outcomes, and strengthen overall cardiac care delivery.

Cardiovascular Devices Market Share

The top players in the cardiovascular devices market include Medtronic, Abbott Laboratories, Boston Scientific, Johnson & Johnson MedTech, and Terumo, which together accounted for an estimated 45% of the global market in 2025.

Leading companies in the cardiovascular devices market are increasingly focusing on advanced technologies and optimized device engineering to enhance clinical performance and diagnostic accuracy. Manufacturers are integrating innovations such as AI enabled cardiac imaging, real time hemodynamic monitoring, robotic assisted intervention systems, and next generation implantable cardiac devices.

For instance, Medtronic expanded its electrophysiology portfolio with the Affera Mapping and Ablation System and Sphere-9 catheter, while also advancing adoption of its PulseSelect pulsed field ablation (PFA) platform for atrial fibrillation treatment. These advancements improve treatment precision, reduce procedural risks, and support continuous monitoring for conditions like arrhythmias, heart failure, and coronary artery disease. The emphasis on smarter, more connected devices is accelerating early diagnosis and expanding the adoption of high performance cardiovascular solutions.

Emerging regional manufacturers are developing cost-effective cardiovascular solutions and scalable production models to meet the needs of value-driven healthcare markets. These companies are building capabilities in essential device categories such as cardiac monitoring systems, stents, catheters, and diagnostic imaging accessories. Their affordable yet reliable offerings enable broader access to cardiovascular care across therapeutic areas, including coronary artery disease, arrhythmias, structural heart disease, and heart failure. As demand for accessible and high quality cardiac solutions continues to rise, these providers are becoming increasingly influential in shaping the regional market landscape.

Cardiovascular Devices Market Companies

Few of the prominent players operating in the cardiovascular devices industry include:

Abbott Laboratories

AngioDynamics

Biotronik

Boston Scientific

Edwards

Johnson & Johnson MedTech

Koninklijke Philips

Medtronic

Meril Life Sciences

MicroPort Scientific

Olympus

Pneumbra

Relisys Medical Devices

Sahajanand Medical Technologies

Terumo

Translumina Therapeutics

Boston Scientific

Boston Scientific enhances its competitive edge in the cardiovascular devices market through innovation in interventional cardiology, electrophysiology, and structural heart solutions. With strong capabilities in drug-eluting stents, cardiac ablation, and imaging-guided procedures, the company delivers consistent performance across high-growth segments. Boston Scientific’s focus on high-quality technologies and global collaboration strengthens its role as a major contributor to advancing minimally invasive cardiovascular therapies.

Terumo

Terumo strengthens its presence in the cardiovascular devices market through a diverse portfolio of interventional cardiology tools, including guidewires, catheters, and access devices. Its strong global share and sustained innovation reflect deep procedural expertise and reliability across coronary and peripheral interventions. Terumo’s commitment to precision engineering, operational consistency, and clinician-aligned product development supports improved outcomes in catheter-based cardiovascular therapies.

Koninklijke Philips

Koninklijke Philips strengthens its role in the cardiovascular devices market through advanced imaging, diagnostics, and interventional solutions used across catheterization labs and cardiology centers. The company’s strong presence in global cardiology technology rankings reflects its continued investment in high-precision imaging, workflow optimization, and clinician-focused platforms that support minimally invasive cardiovascular procedures. Philips’ commitment to integrated cardiac care and reliable device-software ecosystems reinforces its value among healthcare providers seeking efficient and data-driven cardiovascular solutions.

Cardiovascular Devices Industry News

In November 2024, Johnson & Johnson MedTech received FDA approval for its VARIPULSE Pulsed Field Ablation (PFA) Platform, designed for the treatment of drug-refractory paroxysmal atrial fibrillation (AFib). This significant development is based on promising results from the admIRE clinical trial, which demonstrated a remarkable 100% acute procedural success rate among participants.

The cardiovascular devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 – 2035 for the following segments:

Market, By Device Type

Diagnostic and monitoring devices

Electrocardiogram systems

Holter and event monitors

Remote cardiac monitoring devices

Cardiac diagnostic ultrasound

Other diagnostic and monitoring devices

Therapeutic and surgical devices

Catheters

Electrophysiology ablation catheters

Electrophysiology diagnostic and mapping catheters

Chapter 6 Market Estimates and Forecast, By Application, 2022 – 2035 ($ Mn)

6.1 Key trends

6.2 Coronary artery disease

6.3 Cardiac arrhythmia

6.4 Heart failure

6.5 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 – 2035 ($ Mn)

7.1 Key trends

7.2 Hospitals

7.3 Ambulatory surgical centers

7.4 Cardiac centers

7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 – 2035 ($ Mn)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 UK

8.3.3 France

8.3.4 Spain

8.3.5 Italy

8.3.6 Netherlands

8.4 Asia Pacific

8.4.1 China

8.4.2 Japan

8.4.3 India

8.4.4 Australia

8.4.5 South Korea

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.6 Middle East and Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 UAE

Chapter 9 Company Profiles

9.1 Abbott Laboratories

9.2 AngioDynamics

9.3 Biotronik

9.4 Boston Scientific

9.5 Edwards

9.6 Johnson & Johnson MedTech

9.7 Koninklijke Philips

9.8 Medtronic

9.9 Meril Life Sciences

9.10 MicroPort Scientific

9.11 Olympus

9.12 Pneumbra

9.13 Relisys Medical Devices

9.14 Sahajanand Medical Technologies

9.15 Terumo

9.16 Translumina Therapeutics

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Regional or domestic-only leaders not in the global top tier

Distributors and channel partners who control market access

Emerging disruptors, startups, or adjacent-industry entrants

Niche players focused on a specific application or end-use

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Authors: Monali Tayade, Shishanka Wangnoo

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at[email protected]

Explore our licensing options:

Starting at: $2,450

Premium Report Details

Base Year: 2025

Companies Profiled: 16

Tables and Figures: 199

Countries covered: 19

Pages: 180

Download Free PDF

Premium Report Details

Base Year: 2025

Companies Profiled: 16

Tables and Figures: 199

Countries covered: 19

Pages: 180

Download Free PDF

Share Content

Add Citations

Monali Tayade. 2026, August. Cardiovascular Devices Market - By Device Type, By Application, By End Use, Growth Forecast, 2026 - 2035 (Report ID: GMI4949). Global Market Insights Inc. Retrieved August 8, 2026, from https://www.gminsights.com/toc/details/cardiovascular-devices-market

Cardiovascular Devices Market

Get a free sample of this report

Get a free sample of this report Cardiovascular Devices Market

Is your requirement urgent? Please give us your business email for a speedy delivery!

Cardiovascular Devices Market Size

The global cardiovascular devices market was valued at USD 74 billion in 2025 and is projected to grow from USD 79 billion in 2026 to USD 152 billion by 2035, expanding at a CAGR of 7.5%, according to the latest report published by Global Market Insights Inc.

This substantial growth is driven by an increasing number of patients suffering from cardiovascular diseases, an expanding geriatric population, rising government initiatives, technological advancements in cardiovascular devices, and rising demand for minimally invasive procedures.

The increasing global burden of cardiovascular diseases (CVDs) is a significant catalyst driving the growth of the cardiovascular devices market. According to the World Health Organization, an estimated 19.8 million people died from CVDs in 2022, accounting for approximately 32% of all global deaths, with 85% of these fatalities caused by heart attacks and strokes. This alarming prevalence reflects the growing impact of sedentary lifestyles, rising obesity rates, unhealthy dietary patterns, tobacco use, and harmful alcohol consumption. As populations age and chronic disease risk factors become more widespread, healthcare systems face increasing demand for early diagnosis, continuous monitoring, and advanced treatment options. This trend is accelerating the adoption of minimally invasive cardiovascular devices, next-generation stents, implantable cardiac devices, wearable heart monitors, and AI-assisted diagnostic tools. Additionally, rising awareness of preventive cardiac care and expanding access to healthcare in emerging economies are further boosting device utilization. Collectively, the escalating global CVD burden and the urgent need for effective diagnostic and therapeutic solutions position this trend as a critical driver of sustained growth in the cardiovascular devices market.

The rising demand for minimally invasive procedures is a key driver of the cardiovascular devices market, as patients and healthcare providers increasingly prefer treatments that reduce surgical trauma, shorten hospital stays, lower complication risks, and enable faster recovery. Minimally invasive cardiovascular interventions, such as catheter-based angioplasty, transcatheter aortic valve replacement (TAVR), cardiac ablation, and percutaneous coronary interventions (PCI), are witnessing growing adoption due to their clinical effectiveness and improved patient outcomes compared to traditional open-heart surgeries. This trend is driving demand for advanced cardiovascular devices, including catheter systems, guidewires, coronary stents, transcatheter heart valves, and electrophysiology devices. Furthermore, continuous technological advancements in imaging, robotic-assisted procedures, and precision-guided catheter technologies are enhancing procedural accuracy and safety, further accelerating the growth of the cardiovascular devices market.

Cardiovascular devices are medical instruments, tools, and implantable or external systems designed to monitor, support, or restore the normal functioning of the heart and blood vessels. These devices help detect abnormalities, maintain circulation, regulate heart rhythm, improve blood flow, or assist in the diagnosis and long-term management of cardiovascular conditions.

Cardiovascular Devices Market Trends

Cardiovascular Devices Market Analysis

Based on application, the cardiovascular devices market is segmented into coronary artery disease, cardiac arrhythmia, heart failure, and other applications. The cardiac arrhythmia segment dominated the market with the largest revenue of USD 25.5 billion in 2025.

Based on end use, the cardiovascular devices market is segmented into hospitals, ambulatory surgical centers, cardiac centers, and other end users. The hospitals segment accounted for USD 43.2 billion with a revenue share of 58.3% in 2025.

North America Cardiovascular Devices Market

The North America region accounted for 41.8% of the global cardiovascular devices market in 2025. The cardiovascular devices market in North America is experiencing robust expansion, driven by the rising burden of cardiovascular diseases.

Europe Cardiovascular Devices Market

Europe's cardiovascular devices market accounted for USD 21.1 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

Asia Pacific Cardiovascular Devices Market

The Asia Pacific region is projected to show a lucrative growth of about 8.4% during the forecast period.

Latin America Cardiovascular Devices Market

Latin America is experiencing significant growth in the cardiovascular devices market.

Middle East and Africa Cardiovascular Devices Market

The cardiovascular devices market in the Middle East and Africa is significantly driven by the rising number of individuals affected by cardiovascular diseases (CVDs).

Cardiovascular Devices Market Share

Cardiovascular Devices Market Companies

Few of the prominent players operating in the cardiovascular devices industry include:

Boston Scientific enhances its competitive edge in the cardiovascular devices market through innovation in interventional cardiology, electrophysiology, and structural heart solutions. With strong capabilities in drug-eluting stents, cardiac ablation, and imaging-guided procedures, the company delivers consistent performance across high-growth segments. Boston Scientific’s focus on high-quality technologies and global collaboration strengthens its role as a major contributor to advancing minimally invasive cardiovascular therapies.

Terumo strengthens its presence in the cardiovascular devices market through a diverse portfolio of interventional cardiology tools, including guidewires, catheters, and access devices. Its strong global share and sustained innovation reflect deep procedural expertise and reliability across coronary and peripheral interventions. Terumo’s commitment to precision engineering, operational consistency, and clinician-aligned product development supports improved outcomes in catheter-based cardiovascular therapies.

Koninklijke Philips strengthens its role in the cardiovascular devices market through advanced imaging, diagnostics, and interventional solutions used across catheterization labs and cardiology centers. The company’s strong presence in global cardiology technology rankings reflects its continued investment in high-precision imaging, workflow optimization, and clinician-focused platforms that support minimally invasive cardiovascular procedures. Philips’ commitment to integrated cardiac care and reliable device-software ecosystems reinforces its value among healthcare providers seeking efficient and data-driven cardiovascular solutions.

Cardiovascular Devices Industry News

The cardiovascular devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 – 2035 for the following segments:

Market, By Device Type

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries: