Summary

Table of Content

Organic Protein Hydrolysates Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Organic Protein Hydrolysates Market Size

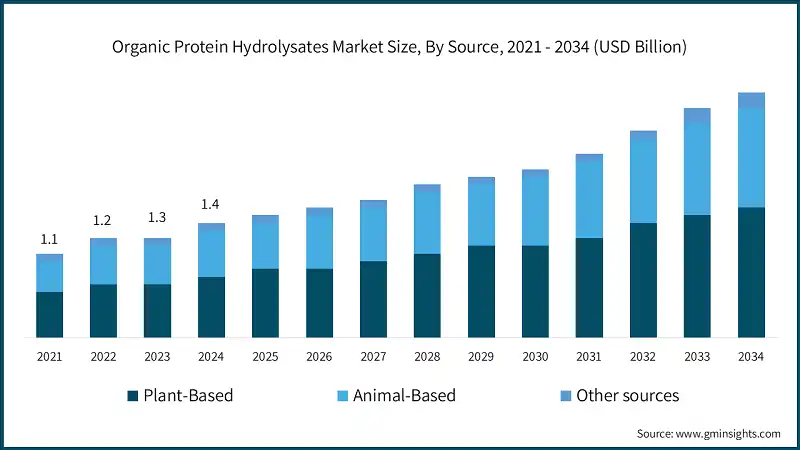

The global organic protein hydrolysates market size was valued at USD 1.4 billion in 2024. The market is expected to grow from USD 1.5 billion in 2025 to USD 3.1 billion in 2034, at a CAGR of 8.2% according to latest report published by Global Market Insights Inc.

To get key market trends

- Hydrolyzed organic proteins benefit from the simultaneous organic food, high protein value and precision nutrition trends. Sports nutrition, medical foods, infant formulas, specialized pet food, and bio stimulants all benefit from the hypoallergenic nature, bioactive peptides, and enhanced digestibility of these proteins which support continual pricing and innovation.

- This organic protein market represents an intersection of trending industries. In the decade from 2021 to 2024, the global sales of organic products grew by 50% - starting from 150 billion to 225 billion. This organic protein market also incentivized the launch of hydrolyzed organic protein products - particularly focusing on dairy, soy, and peas. In addition, demand for protein ingredients and hydrolyzed protein has risen sharply.

- Global markets are expected to absorb more concentrated and functional proteins, especially hydrolysates, within processed and functional foods. These trends serve to enhance demand for hydrolyzed proteins.

- During the past four years, the impact of the pandemic on health and wellness increases within the sports and lifestyle nutrition world, and the growing use of organic bio stimulants have all raised interest in organic protein hydrolysates. Further interest in product diversification and expansion is supported by regulatory support for organic farming such as the USDA organic programs and the EU Green Deal, and advances in enzymatic processing technologies.

Organic Protein Hydrolysates Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 1.4 Billion |

| Market Size in 2025 | USD 1.5 Billion |

| Forecast Period 2025 - 2034 CAGR | 8.2% |

| Market Size in 2034 | USD 3.1 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Rising demand for clean-label, organic proteins | Boosts premium positioning and adoption in nutrition |

| Growth in sports, infants, clinical nutrition | Increases use of highly digestible protein hydrolysates |

| Advances in enzymatic processing technologies | Enhances functionality, purity, and cost efficiency |

| Pitfalls & Challenges | Impact |

| High production costs versus conventional proteins | Limits affordability and penetration in price-sensitive segments |

| Limited raw material availability and certification | Constrains large-scale, globally harmonized supply |

| Opportunities: | Impact |

| Expansion into organic bio stimulants and Agri nutrition | Opens new revenue streams beyond food and feed |

| Plant-based and allergen-free formulation trends | Favors organic plant hydrolysate over animal proteins |

| Market Leaders (2024) | |

| Market Leaders |

14% market share |

| Top Players |

Collective market share in 2024 is 50% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | North America |

| Fastest growing market | Asia Pacific |

| Emerging countries | India, Brazil, China |

| Future outlook |

|

What are the growth opportunities in this market?

Organic Protein Hydrolysates Market Trends

- Shifts towards plant-clade and allergen hydrolysates: There is a widening consumer base for plant-based organic hydrolysates (namely pea, rice, and soy) due to rising interest in dairy-free and light allergenic products. This has led brands to commercially promote ‘plant protein + hydrolysate’ combinations for sports powders and ready-to-drink (RTD) beverages, reflecting the rising tide of plant-based foods in consumer packaged goods.

- Expansion of hydrolysates into the high-value nutrition sector: There is increased penetration of organic hydrolysates into the infant, pediatric, and medical nutrition sectors due to lower digestibility and allergenicity of the hydrolysates. As an illustration, organic whey or casein is partially hydrolyzed for use in sensitive infant formulas, while clinical nutrition beverages for recovery, malabsorption, elderly care in European and North American markets.

- Growing Adoption in Bio stimulants and Sustainable Agriculture Hydrolysates are being used to promote plant growth, nutrient uptake, and stress tolerance and are therefore used as bio stimulants. This has led to an adoption by European organic farmers of amino-acid-rich foliar sprays and soil treatments for organic farming which, because of lower regulatory thresholds for synthetic fertilizer use, promotes uptake of high quality, certified organic protein-based inputs which are supported by European Union (EU) sustainability goals and regulations.

- Producers are focusing on particular bioactive benefits: antioxidants, anti-fatigue, gut health, or muscle recovery—by customizing hydrolysis conditions and peptide profiles. This is in line with “precision nutrition” products featuring targeted results, such as recovery shakes, beauty-from-within powders, and joint-health supplements where collagens or dairy-derived organic hydrolysates are marketed as premium functional ingredients with scientific backing.

Organic Protein Hydrolysates Market Analysis

Learn more about the key segments shaping this market

Based on sources, the organic protein hydrolysates market is segments in plant-based, animal-based, and other sources. Plant-Based dominated the market with an approximate market share of 55% in 2024 and is expected to grow with a CAGR of 8% till 2034.

- Portfolio Sourcing Raw Material Diversification and Sustainability Positioning Organic protein hydrolysates market is widening its sourcing diversification in both plants and animals. Manufacturers now also target peas, rice, wheat, corn, and fish collagen, which helps obtain tailored amino acid profiles coupled with varied functionalities. In North America and Europe, sustainability, animal welfare, and non-GMO represent strong sourcing concerns.

- Functional specialization and application-driven development aspects of the business trend focus on the production of hydrolysates tailored for specific sources. Their use is for specific applications that include soluble and collagen-rich fish proteins for joints and beauty, and rice protein for plant-based beverages, as well as milk and egg proteins for infants and clinical nutrition. Companies focus on co-product valorization, integrating meat, poultry, and marine by-products, which strengthens the business case while supporting circularity narratives and the increasingly popular regulatory-aligned clean-label focus.

Based on protein type, the organic protein hydrolysates market is segmented into complete proteins (all essential amino acids), incomplete proteins, collagen & gelatin proteins, casein & whey proteins, specialty / functional proteins (bioactive peptides, tailored blends). Complete proteins segment dominated the market with an approximate market share of 34% in 2024 and is expected to grow with the CAGR of 8.6% till 2034.

- Demands for complete amino acid profiles and specific functionalities influence protein-type dynamics. In high-value nutrition, casein and whey dominate with strong clinical evidence while collagen and gelatin show rapid growth in joints, mobility, and beauty-from-within. In the market, specialization is emerging with peptide blends for condition-specific claims and unique IP.

- To adjust cost, functionality and label appeal, specialty and incomplete proteins are more increasingly combined. Formulators utilize complete dairy or plant proteins as a foundation, and then tier bioactive peptide fractions for muscle recovery, metabolic assistance, or gut health. This helps secure long-term agreements with suppliers with precise controls of hydrolysis and stable peptide fingerprints.

")

Learn more about the key segments shaping this market

Based on applications, the organic protein hydrolysates market is segmented into food & beverages, animal nutrition, agriculture & crop nutrition, cosmetics & personal care, pharmaceuticals & nutraceuticals, industrial & other applications. Food & beverages segment dominated the market with an approximate market share of 37.2% in 2024 and is expected to grow with the CAGR of 8.6% up to 2034.

- Protein type dynamics are influenced by the demand of certain functionalities and complete amino acid profiles. In value-added nutrition, the casein and whey are highly dominated with robust clinical backing, while the collagen, and gelatin are growing rapidly in the joint, mobility, and beauty-from-within spaces. In the market, a growing degree of specialization is observed, with the introduction of unique IPs and condition-specific claims for blended peptides.

- To achieve a more economical cost, functionality, and label appeal, the industry is increasingly using a greater proportion of specialty and incomplete proteins. Formulators pair a complete dairy or plant protein with tiered bioactive peptide fractions, leveraging those with muscle recovery, metabolic, or gut health benefits. This enables them to secure extended contracts with suppliers, necessitating strict controls of hydrolysis and the delivery of stable peptides.

")

Looking for region specific data?

North America is the largest organic protein hydrolysates market, projected to grow from USD 428 million in 2024 to USD 952 million in 2034, due to the understudied mature sectors of organic nutrition, sports, and pet foods. The organic penetration of retail, along with advanced clinical and sports nutrition brands and higher than average consumer willingness to pay for clean-label, high-performance protein, benefits North America.

- As the innovation center of the world, the U.S. commercializes organic protein hydrolysates across all nutrition sectors and disciplines, especially for sports and medical applications. Demand is galvanized by the rapid incorporation of hydrolysates in tier-one pet foods and the growing suite of nutritional and performance-focused formulations in on-the-go beverages, meal replacements, and high protein snacks.

Over the next decade, Europe will continue to be the second largest organic protein hydrolysates market in organic adoption driven by stringent regulations. The adoption of organic regulation has led to a sector growth from USD 397 million in 2024 to USD 860 million in 2034 and is a result of the strict organic regulations and heightened focus on sustainability of the region. The robust segments of organic dairy, infant formulas, specialty food, and the strong environmental objectives of the EU Green Deal will lead to a more widespread use of organic protein hydrolysates.

- Germany serves as a primary technical and regulatory benchmark market for organic hydrolysates. Germany’s emphasis on certified-organic and clean-label goods as well as strong infant, sports, and clinical nutrition brands, drives the demand for organic hydrolysates in high-evidence and premium formulations aimed at health and sustainability conscious consumers.

The Asia Pacific organic protein hydrolysates market is the most rapidly evolving, growing from USD 387 million in 2024 to USD 870 million in 2034, due to urban development, income growth, and the protein fortification trend. The expanding middle class’s demand for sports nutrition, fortified foods, and premium pet foods, combined with the increasing initiatives in organic agriculture, is driving rapid growth in the region.

- As interest in premium infant formula, sports nutrition, and beauty-from-within products increases, as well as the development of domestic organic production, China is becoming the demand regional demand anchor. The integration of hydrolysates is increasing in developed and especially in imported products.

From USD 127 million in 2024 to USD 271 million in 2034, Latin America’s organic protein hydrolysates market is growing continuously. The organic foods, specialty feeds, and Agri nutrition inputs of the region are being gradually adopted. The region uses its strong agricultural production, growing organic supply chains oriented to exports, and increasing consumer health and sustainability awareness.

- Brazil is the primary provider of organic protein hydrolysates in the Latin American region. The expanding interest in organic farming, the East Central Brazil Region's interest in fortified foods and beverages, and the demand for sustainable Agri nutrition bio stimulants are contributing to the increasing use of hydrolysates across the various food, feed, and crop-input applications. This is especially the case for the urban consumers and food producers focused on the Brazil export markets.

The MEA markets are currently showing robust and incremental growth. The anticipated growth is from USD 86 million in 2024 to USD 193 million by 2034 owing to growth in niche markets, particularly premium nutrition, pet food, and aggrotech. There is an increased demand driven by the interest in health and the growing availability of halal-compliant, organic, water-efficient Agri nutrition products.

- The premium certified-organic nutrition and Agri nutrition products available in Saudi Arabia also attract a lot of attention. Organic protein hydrolysates are likely to perform well in the Saudi market, especially in imported nutrition products and the emerging local bio stimulant products, due to the Saudi demand being driven by high health and sports spending and an interest in specialty foods.

Organic Protein Hydrolysates Market Share

Major players in the market for organic protein hydrolysates industry include the Kerry Group, Glanbia, and Arla Foods, which holds 14%, 12%, and 10% market shares, respectively, while Friesland Campina, Glanbia, and Fonterra follow with 8% and 6% shares, respectively. Concentration in this market is the result of Kerry's, Arla's, and Friesland's global sourcing, superior enzymatic abilities, and strong application R&D, which resulted in strong their relationships in infant, sports, clinical, and specialized R&D nutrition. Together, these companies control about 50% of the global organic protein hydrolysates market.

- Kerry Group: Kerry leverages its broad nutrition portfolio, application labs, and global customer base to lead the organic protein hydrolysates space with about 14% share. It focuses on integrated solutions for sports, lifestyle, and clinical nutrition, often combining organic hydrolysates with flavor, stabilization, and clean-label systems to deliver turnkey concepts for major food and beverage brands.

- Arla Foods Ingredients: Arla Foods Ingredients holds roughly 12% share, underpinned by strong organic dairy sourcing and expertise in casein and whey hydrolysates. It is particularly influential in infants, pediatric, and medical nutrition, where safety, traceability, and clinical backing are critical. Recent efforts emphasize higher-protein, low-allergen organic concepts aligned with European and global regulatory requirements.

- FrieslandCampina Ingredients: FrieslandCampina Ingredients accounts for around 10% of the market, with a strong focus on early-life, performance, and active nutrition. Its capabilities in high-quality organic dairy proteins and specialized hydrolysates position it well in premium infant formulas and adult nutrition products. The company continues to expand its value-added, science-backed ingredient offerings and sustainability credentials.

- Glanbia Nutritionals: Glanbia Nutritionals, with approximately 8% share, combines dairy expertise with growing capabilities in plant-based and functional protein systems. It serves sports, lifestyle, and clinical nutrition brands, offering organic hydrolysates that integrate into ready-to-mix and ready-to-drink formats. Glanbia emphasizes formulation support, taste optimization, and global manufacturing footprints to support multinational and emerging brands.

- Fonterra Co-operative Group : Fonterra Co-operative Group holds about 6% share, driven by strong New Zealand dairy sourcing and established positions in global nutrition supply chains. Its organic whey and casein hydrolysates feed into infants, sports, and specialty nutrition applications. Fonterra’s focus on grass-fed, sustainability narratives and high-quality dairy credentials enhance the appeal of its organic hydrolysate ingredients worldwide.

Organic Protein Hydrolysates Market Companies

Major players operating in the organic protein hydrolysates industry include:

- Arla Foods Ingredients

- Kerry Group

- FrieslandCampina Ingredients

- Glanbia Nutritionals

- Hilmar Ingredients

- Fonterra Co-operative Group

- Lactalis Ingredients

- A. Costantino & C. S.p.A.

- Essentia Protein Solutions

- VITAMINAS, S.A. (Bioiberica Group)

- Armor Protéines

- AMCO Proteins

- Tate & Lyle

- ADM (Archer Daniels Midland)

- Cargill

- Ingredion Incorporated

- Roquette Frères

- Symrise

- Gelita AG

- Weishardt Group

Organic Protein Hydrolysates Industry News

- In October 2024, Kerry Group launched an expanded range of organic plant and dairy protein hydrolysates for sports and active nutrition brands, emphasizing cleaner labels, faster absorption, and customized peptide profiles for premium beverage and powder applications in Europe and North America.

- In June 2023, Arla Foods Ingredients announced capacity upgrades for organic whey and casein hydrolysates, targeting infant and clinical nutrition customers. The initiative focused on higher purity, improved traceability, and meeting tightening EU organic certification and quality requirements for sensitive nutrition applications.

- In November 2022, FrieslandCampina Ingredients introduced new organic dairy-based hydrolysate concepts for early-life and performance nutrition, highlighting mild taste and controlled allergenicity. The company positioned these ingredients for premium formulas in Europe and Asia, leveraging its established early-life nutrition expertise.

- In March 2022, Glanbia Nutritionals and Fonterra Co-operative Group separately expanded portfolios of organic-certified protein hydrolysates, including whey, casein, and emerging plant-based options. Both emphasized integrated formulation support for sports, lifestyle, and functional food brands seeking high-digestibility, clean-label protein solutions.

This organic protein hydrolysates market research report includes in-depth coverage of the industry, with estimates & forecasts in terms of revenue (USD Billion) and volume (Kilo Tons) from 2025 to 2034, for the following segments:

Market, By Source

- Plant-Based

- Soy

- Wheat

- Pea

- Rice

- Corn

- Oilseeds (e.g., sunflower, rapeseed)

- Other plant sources

- Animal-Based

- Milk (casein, whey)

- Egg

- Meat & Poultry

- Fish & Marine

- Collagen & Gelatin

- Other sources

Market, By Protein Type

- Complete Proteins (all essential amino acids)

- Incomplete Proteins

- Collagen & Gelatin Proteins

- Casein & Whey Proteins

- Specialty / Functional Proteins (bioactive peptides, tailored blends)

Market, By Application

- Food & Beverages

- Functional Foods

- Sports Nutrition & Performance Products

- Infant & Clinical Nutrition

- Bakery & Confectionery

- Dairy & Dairy Alternatives

- Meat Analogs & Meat Products

- Beverages (RTD, powdered drinks, smoothies)

- Snacks & Convenience Foods

- Animal Nutrition

- Pet Food (dogs, cats, others)

- Aquafeed (fish, shrimp, others)

- Livestock Feed (poultry, swine, ruminants)

- Specialty & Performance Feeds

- Agriculture & Crop Nutrition

- Biostimulants & Plant Growth Promoters

- Foliar Sprays

- Soil Amendments

- Seed Treatments

- Cosmetics & Personal Care

- Skin Care

- Hair Care

- Nutricosmetics / Beauty-from-within

- Pharmaceuticals & Nutraceuticals

- Dietary Supplements

- Medical & Clinical Nutrition

- Drug Delivery & Specialty Formulations

- Industrial & Other Applications

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of Middle East and Africa

Frequently Asked Question(FAQ) :

Who are the key players in the organic protein hydrolysates industry?

Key players include Arla Foods Ingredients, Kerry Group, FrieslandCampina Ingredients, Glanbia Nutritionals, Hilmar Ingredients, Fonterra Co-operative Group, Lactalis Ingredients, A. Costantino & C. S.p.A., Essentia Protein Solutions, VITAMINAS, S.A., Armor Protéines, and AMCO Proteins.

What are the upcoming trends in the organic protein hydrolysates market?

Trends include rising demand for plant-based hydrolysates, expansion into infant and medical nutrition, adoption in biostimulants for sustainable agriculture, and precision nutrition targeting gut health, muscle recovery, and antioxidant benefits.

What is the expected size of the organic protein hydrolysates industry in 2025?

The market size is projected to reach USD 1.5 billion in 2025.

What was the market share of the plant-based segment in 2024?

The plant-based segment dominated the market with an approximate share of 55% in 2024 and is expected to grow at a CAGR of 8% through 2034.

What was the market share of the complete proteins segment in 2024?

The complete proteins segment held a market share of approximately 34% in 2024 and is anticipated to witness 8.6% until 2034.

What was the market share of the food & beverages segment in 2024?

The food & beverages segment accounted for approximately 37.2% of the market in 2024 and is expected to grow at a CAGR of 8.6% up to 2034.

Which region leads the organic protein hydrolysates sector?

North America leads the market, projected to grow from USD 428 million in 2024 to USD 952 million in 2034. Growth is driven by mature sectors in organic nutrition, sports, and pet foods, along with high consumer willingness to pay for clean-label, high-performance protein products.

What is the market size of the organic protein hydrolysates in 2024?

The market size was USD 1.4 billion in 2024, with a CAGR of 8.2% expected through 2034. The market is driven by trends in organic foods, high protein value, and precision nutrition.

What is the projected value of the organic protein hydrolysates market by 2034?

The market is poised to reach USD 3.1 billion by 2034, supported by increasing demand in sports nutrition, medical foods, infant formulas, and bio stimulants.

Organic Protein Hydrolysates Market Scope

Related Reports