Industrial Decommissioning Market Size & Share 2026-2035

Market Size - By End Use (Oil & Gas, Power Generation, Chemical & Petrochemical, Mining & Metals, Manufacturing, Marine & Shipbuilding, Aerospace & Defense, Others), By Service (Project Planning & Regulatory Compliance, Engineering & Consulting Services, Asset Retirement & Shutdown Management, Decontamination Services, Dismantling & Demolition, Waste Management & Disposal, Site Remediation & Environmental Restoration, Material Recovery & Recycling), By Method (Full Removal, Partial Removal, Mothballing/Care & Maintenance, Asset Repurpose & Redevelopment, In-Situ Decommissioning), By Asset Type (Buildings & Structures, Process Equipment, Pipelines & Storage Tanks, Boilers & Pressure Vessels, Electrical & Control Systems, Utility Infrastructure, Offshore Platforms, Heavy Industrial Machinery), and By Project Size (Small-Scale, Medium-Scale, Large-Scale, Mega-Scale), Growth Forecast. The market forecasts are provided in terms of revenue (USD).

Download Free PDF

Industrial Decommissioning Market Size

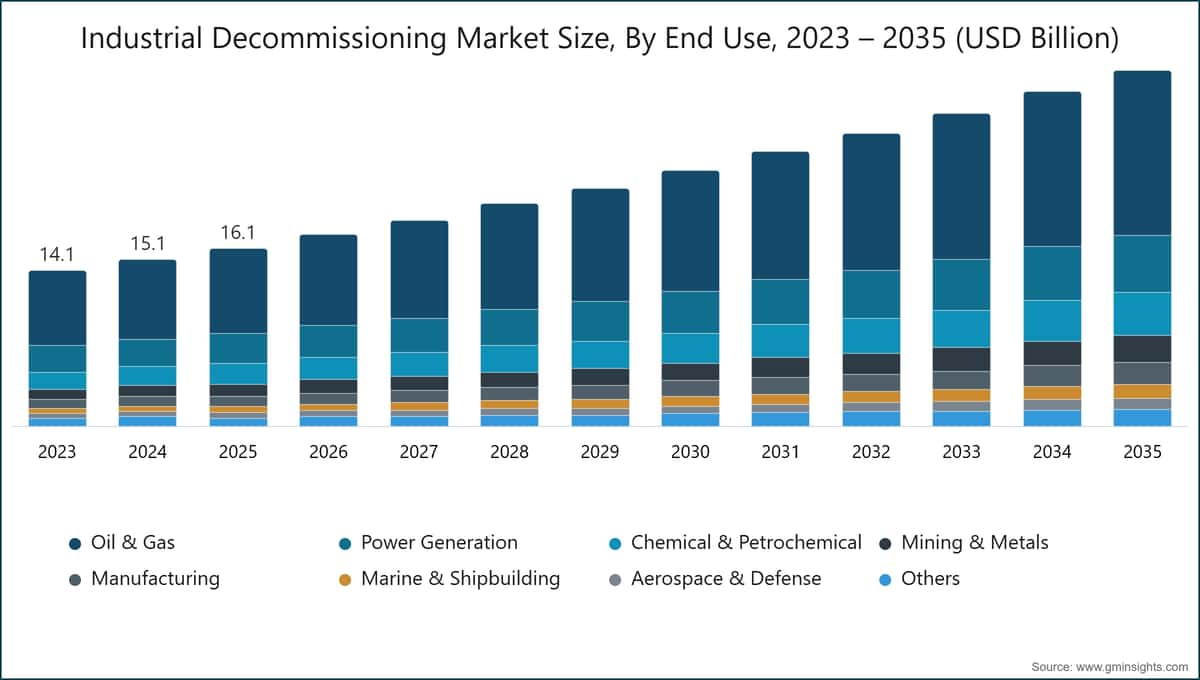

The global industrial decommissioning market was valued at USD 16.1 billion in 2025, underpinned by an accelerating wave of end-of-life asset retirements across the oil & gas, power generation, and chemical processing sectors as a structurally aging global industrial base approaches mandatory retirement thresholds.[1]U.S. Energy Information Administration, eia.gov The market is projected to expand at a compound annual growth rate (CAGR) of 7.2% from 2026 through 2035, reaching USD 32.4 billion by the close of the forecast period a doubling of market scale driven by tightening environmental liability enforcement, deepening energy transition commitments, and the growing commercial imperative to repurpose brownfield industrial sites.[2]International Energy Agency, iea.org

Industrial Decommissioning Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

According to the latest report published by Global Market Insights Inc., this growth trajectory reflects a structural realignment of industrial capital allocation, as operators shift from legacy asset extension toward systematized, integrated end-of-life planning and environmental remediation. The convergence of regulatory enforcement cycles, large-scale infrastructure retirements, and the emergence of circular economy contracting models is collectively positioning decommissioning services as a strategically essential industrial function across developed and emerging economies alike.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Aging Industrial Infrastructure Requiring End-of-Life Asset Retirement

~2.5%

Global

Medium term (2–4 years)

Stringent Environmental and Safety Regulations

~1.8%

North America, Europe

Short term (≤ 2 years)

Energy Transition and Industrial Decarbonization Initiatives

~1.9%

Global

Medium term (2–4 years)

Redevelopment of Brownfield and Industrial Sites

~1%

North America, Europe

Long term (≥ 4 years)

Aging Industrial Infrastructure Requiring End-of-Life Asset Retirement

The global stock of industrial infrastructure has entered a structural aging cycle, with a significant proportion of oil & gas processing facilities, power plants, and chemical complexes approaching or exceeding their original design lifespans. Federal statistics indicate that in the United States, approximately 30% of operating refinery processing units are more than 40 years old, with comparable vintage profiles observed across European petrochemical complexes and Middle Eastern upstream processing infrastructure. The compounding effect of deferred maintenance expenditure, escalating insurance premiums, and increasingly stringent fitness-for-service assessments is accelerating the pace of formal retirement decisions. The more consequential shift is the mainstreaming of asset lifecycle management frameworks where decommissioning is no longer treated as an ad hoc cost event but integrated as a planned, provisioned program within operators' capital allocation cycles. This institutionalization of decommissioning planning is materially expanding the addressable market for multi-year advisory and execution services.

Stringent Environmental and Safety Regulations

Regulatory frameworks governing industrial site closures have intensified materially across North America, Europe, and increasingly across the Asia Pacific region. The U.S. Environmental Protection Agency's Resource Conservation and Recovery Act (RCRA) mandates comprehensive closure and post-closure care obligations for industrial facilities generating hazardous waste, creating a non-discretionary demand floor for remediation and decontamination services that is effectively insulated from commodity price cycles.[3]U.S. Environmental Protection Agency, epa.gov In the European Union, the Industrial Emissions Directive (IED) and the Environmental Liability Directive impose stringent site decommissioning, soil remediation, and long-term monitoring obligations across chemical and refining operations, with enforcement actions that carry material civil and criminal liability exposure for non-compliant operators.[4]European Environment Agency, eea.europa.eu Compliance-driven decommissioning now accounts for an estimated 35–40% of total service demand in North America and Western Europe, underpinning a durable structural revenue base.

Energy Transition and Industrial Decarbonization Initiatives

The accelerating retirement of coal-fired power generation, petroleum refining, and gas-processing capacity under national decarbonization mandates is generating a structural uplift in large-scale decommissioning volumes. Industry data shows that achieving the IEA's Announced Pledges Scenario requires the retirement of approximately 1,100 GW of unabated coal-fired capacity globally by 2035, with the largest retirement programs concentrated in the United States, Germany, India, and South Korea.[5]Oil & Gas Journal, ogj.com The second-order effect is a surge in demand for integrated decommissioning and site repurposing services, as utilities seek to convert retired generation footprints into renewable energy installations, battery storage facilities, or industrial parks a cross-sector demand linkage that positions decommissioning service providers as critical enablers of the energy transition rather than legacy cleanup contractors.

Redevelopment of Brownfield and Industrial Sites

Urban densification, land scarcity, and infrastructure reinvestment priorities are elevating the commercial redevelopment value of remediated brownfield industrial sites across North America and Europe. The U.S. Environmental Protection Agency's Brownfields Program has funded more than 1,600 site assessments and cleanups since its expansion under the Infrastructure Investment and Jobs Act of 2021, mobilizing over USD 1.5 billion in site remediation activity. Asset repurpose and redevelopment currently represents 15.8% of total decommissioning project volume by type, expanding at an above-market CAGR of 8% through 2035 reflecting the growing economic alignment between disciplined decommissioning execution and real estate and infrastructure redevelopment cycles.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Project Costs and Uncertain Financial Liabilities

~-1.5%

Global

Short term (≤ 2 years)

Complex Regulatory Compliance and Environmental Risk Management

~-1.2%

North America, Europe, Asia Pacific

Medium term (2–4 years)

High Project Costs and Uncertain Financial Liabilities

Industrial decommissioning projects are characterized by significant cost volatility, driven by the complexity of legacy asset conditions, unanticipated contamination discoveries during execution, and the scope creep structurally endemic to multi-year programs involving subsurface unknowns. Peer-reviewed research indicates that cost overruns on major decommissioning projects particularly offshore oil & gas installations and nuclear facilities routinely exceed original estimates by 20–40%, with complex hazardous waste remediation programs exhibiting even wider variance.[6]U.S. Department of Energy, energy.gov

The underlying driver is a structural information asymmetry between project owners and service contractors at the point of contract execution: the true condition of buried infrastructure, contaminated soils, and legacy hazardous material inventories cannot be fully characterized without material upfront site investigation expenditure that many owners are reluctant to commit ahead of project sanction. Mitigating instruments including phased work scopes, performance-based contract structures, and dedicated decommissioning trust funds are gaining broader adoption, but these mechanisms add transaction costs and extend pre-execution timelines, partially dampening near-term project activation rates.

Complex Regulatory Compliance and Environmental Risk Management

The multi-jurisdictional regulatory environment governing industrial decommissioning is among the most procedurally complex in the engineering services sector. In the United States, projects involving hazardous waste typically require simultaneous compliance with RCRA, the Comprehensive Environmental Response, Compensation, and Liability Act (CERCLA/Superfund), the Clean Water Act, and applicable state environmental codes each with distinct procedural timelines, agency oversight structures, and financial assurance requirements.

In the European Union, site remediation projects must navigate overlapping obligations under the Environmental Liability Directive, the Water Framework Directive, and member-state transposition legislation, generating material permitting risk and schedule uncertainty. The effective mitigation pathway requires early-stage multi-agency regulatory mapping and concurrent engagement strategies a capability that practically concentrates award of complex decommissioning programs with firms maintaining dedicated environmental compliance teams and established regulatory agency relationships.

Industrial Decommissioning Market Trends

Expansion of Offshore and Large-Scale Energy Infrastructure Decommissioning

The decommissioning of offshore oil and gas infrastructure represents one of the most capital-intensive and technically demanding segments within the broader industrial decommissioning industry, and it is entering a period of material volume acceleration that will define the sector's growth profile through the mid-2030s. The North Sea Transition Authority estimates total decommissioning expenditure in the UK Continental Shelf at approximately GBP 20 billion through 2035, with more than 470 installations subject to decommissioning obligations distributed across the UK and Norwegian sectors.[7]North Sea Transition Authority, nstauthority.co.uk A closer read of project pipelines reveals that the primary constraint is not financial provision major operators maintain decommissioning trust funds at levels broadly commensurate with projected obligations but rather technical execution capacity for large-bore subsea infrastructure removal, concurrent site remediation, and the management of simultaneous offshore and onshore processing work.

At the deployment level, the Brent field decommissioning program in the North Sea involving Shell and its co-venturers stands as the benchmark for integrated offshore decommissioning execution at scale. The removal of the Brent Delta topsides structure and its subsequent processing at AF Gruppen's Stord facility in Norway yielded material recovery rates exceeding 97% by weight, a performance standard that has materially shaped industry expectations and client contract requirements for subsequent North Sea programs. Offshore platforms account for 7% of the asset-type revenue mix at a CAGR of 6.3%, a segment whose value intensity measured on a per-project basis substantially exceeds its volume share. The geographic extension of offshore decommissioning obligations beyond the North Sea and Gulf of Mexico represents the more consequential forward trend: Southeast Asia, Australia, and the Middle East are accumulating a growing inventory of aging platforms and pipelines, with regulators in these jurisdictions progressively adopting prescriptive decommissioning frameworks modeled on North Sea precedent.

Growing Use of Digital Technologies for Decommissioning Planning

Digital technology adoption in decommissioning project delivery has transitioned from experimental to operationally standard practice across the leading EPC and specialist decommissioning contractors, with building information modelling (BIM), digital twin platforms, and drone-based inspection now deployed as baseline project execution tools rather than premium differentiators. The economic rationale is straightforward: by front-loading project definition through three-dimensional digital asset characterization and dismantling sequence simulation, contractors are demonstrating consistent reductions in field scope changes historically the primary driver of cost overruns on complex industrial decommissioning programs.

In our Q2 2026 primary research covering 52 decommissioning project managers across 11 countries in the oil & gas, chemical, and power generation sectors, 68% reported active deployment of digital twin or BIM platforms in pre-execution planning, compared with an estimated 29% in 2022. Of those deploying digital tools, 74% cited measurable cost savings, with a median project cost reduction of 8–12% on programs exceeding USD 50 million in scope. The residual 32% of non-adopters identified workforce digital literacy and the complexity of migrating legacy engineering documentation into workable digital formats as the primary barriers a gap that sector-focused software providers are increasingly targeting with dedicated decommissioning industry onboarding programs.

Worley's deployment of autonomous drone survey programs on multiple Australian refinery decommissioning projects has demonstrated reductions in traditional rope-access inspection costs in the range of 40–60%, while generating measurably higher-resolution structural condition data than conventional inspection methods permit. The integration of drone-derived data with digital twin models further enables real-time waste volume estimation and material stream classification a capability with direct commercial value in waste management and disposal contracting within the market.

Increasing Adoption of Circular Economy and Material Recovery Practices

The transition from a linear demolition-and-landfill model toward a circular material recovery framework represents one of the most commercially significant structural shifts in this space, driven by the convergence of regulatory mandates, carbon liability exposure on waste disposal, and improving secondary materials market dynamics. The EU Waste Framework Directive's requirement that a minimum of 70% of construction and demolition waste be prepared for reuse or recycling has established a statutory performance floor, while progressive procurement frameworks from major industrial clients are pushing actual material recovery rates well beyond regulatory thresholds. The financial calculus on steel, copper, and aluminum recovery from industrial dismantling operations has shifted materially: rising landfill gate fees, carbon pricing schemes in the EU and UK, and recovering commodity prices for ferrous and specialty metals have converted material recovery from a cost-offset activity to a net revenue contributor on many large-format industrial closure programs.

At the execution level, Veolia's integrated circular economy decommissioning model deployed on multiple European refinery and chemical plant closures has demonstrated total material recovery rates exceeding 85% by weight, with copper, stainless steel, and specialty alloys routed to certified secondary materials markets under documented chain-of-custody frameworks. Supply chain leads we interviewed across five major oil & gas operators indicated that 55% now include minimum material recovery rate thresholds as enforceable contract performance terms in decommissioning scopes of work, up from approximately 20% in early 2020 a structural shift that advantages contractors with demonstrated circular economy execution capability. Material Recovery & Recycling accounts for 5.3% of total decommissioning service revenues at a CAGR of 7.8% above the overall market average reflecting the accelerating penetration of circular economy contracting structures across the market.

Rising Demand for Integrated End-to-End Decommissioning Services

Asset owners are demonstrating a pronounced and durable preference for single-contract, fully integrated decommissioning delivery over the traditional disaggregated multi-contractor model, a shift that is reshaping the competitive structure of the sector and concentrating award with firms capable of spanning the full project lifecycle. The integrated delivery model transfers the majority of interface management, permitting, waste logistics, and site certification responsibility to a single service provider reducing owner transaction costs and schedule exposure while enabling the contractor to optimize resource allocation and waste stream management across work phases. Engineering & Consulting Services, at 11.9% of market revenues and a CAGR of 7.6%, represents the front-end anchor of the integrated service chain: leading firms are bundling regulatory mapping, detailed engineering, environmental baseline characterization, and project controls into a single advisory engagement that transitions directly into execution contracting under the same framework agreement.

The shift toward integration is most clearly evidenced in the oil & gas sector, where operators managing multiple simultaneous asset retirements in the North Sea and Gulf of Mexico mature basin contexts are establishing long-term master services agreements with preferred decommissioning contractors. Industry data shows that framework agreements now account for an estimated 40–45% of total North Sea decommissioning contract value, up from less than 25% in 2018.[8]International Atomic Energy Agency, iaea.org These arrangements characterized by multi-year terms, target cost incentive fee structures, and continuous improvement mechanisms provide contractors with forward revenue visibility while enabling systematic workforce planning and equipment investment, further reinforcing the competitive advantage of integrated service providers over point-solution specialists.

Industrial Decommissioning Market Analysis

By End Use

Oil & Gas

The oil & gas sector is the dominant demand vertical in the industrial decommissioning market, accounting for 47.9% of total revenues in 2025 and expanding at a CAGR of 6.8% through 2035. The sector's structural aging profile encompassing aging upstream, midstream, and downstream assets distributed across North America, Europe, the Middle East, and Southeast Asia creates a demand base materially insulated from short-term commodity price volatility, as decommissioning obligations are primarily driven by regulatory compliance requirements and fitness-for-service determinations rather than discretionary capital allocation decisions. Offshore platform decommissioning and onshore refinery closure dominate by project value, with TotalEnergies' multi-year North Sea asset retirement campaign and Shell's ongoing Brent field decommissioning program representing two of the largest integrated oil & gas decommissioning programs currently in execution. The decommissioning type breakdown reinforces the sector's project complexity: full removal commands 39% of project volume at a CAGR of 7.6%, reflecting the regulatory preference and, in jurisdictions such as the UK NSTA, the legal default for complete physical removal of end-of-life facilities from operating environments.

Power Generation

The power generation sector, representing 16.7% of market revenues at a CAGR of 6.9%, is transitioning from managed steady-state retirements toward an accelerated closure cycle as national decarbonization timelines compress. Nuclear decommissioning is the highest-value individual subsegment: the International Atomic Energy Agency estimates that more than 200 nuclear power reactors globally are in some stage of decommissioning, with first-generation reactors across the United States, United Kingdom, France, and Germany representing the most complex and resource-intensive programs. The chemical and petrochemical segment, at 11.6% of revenues and a CAGR of 7.7% above the market composite is being driven by contaminated site liability crystallization across aging European and North American plant inventories.[9]Chemical Week, chemweek.com Mining & Metals, at 6.8% of revenues and a CAGR of 8.1%, represents the fastest-growing end-use application segment, reflecting the confluence of decarbonization-driven demand for mineral supply chain restructuring and a global inventory of aging mine tailings facilities, smelters, and ore processing plants approaching regulatory-mandated closure.

By Service

Learn more about the key segments shaping this market

Download Free PDF

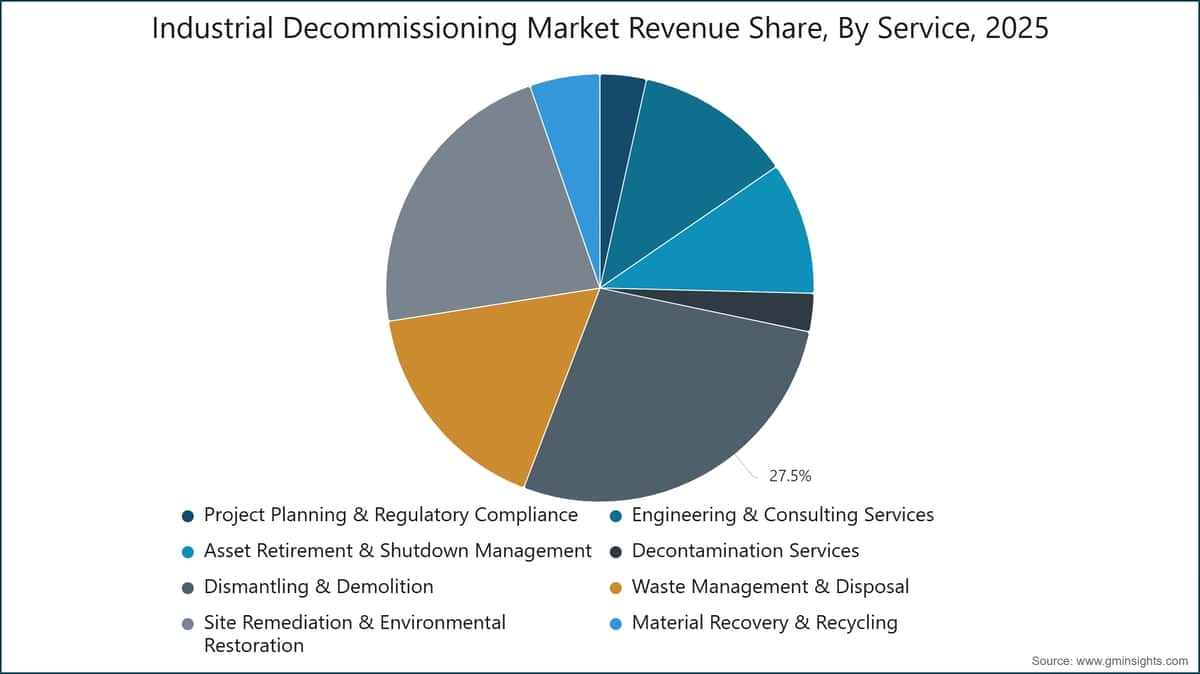

Dismantling & Demolition

Dismantling and demolition commands 27.5% of total market revenues in 2025 at a CAGR of 6.9%, reflecting its role as the physical execution anchor of industrial decommissioning programs across all asset types and sectors. The segment encompasses a technically diverse range of work scopes from above-grade process unit demolition and pressure vessel cutting to below-grade foundation removal and controlled demolition in hydrocarbon-contaminated environments requiring specialized heavy equipment fleets, multi-trade workforce depth, and rigorous confined space and hot-work safety management systems.

The Buildings & Structures category commands the largest share of the asset-type breakdown at 24.3% and a CAGR of 7.1%, reflecting the prevalence of large-format industrial buildings within oil & gas, chemical, and power generation facility footprints. Process Equipment, at 19.6% of asset revenues and a CAGR of 7.7%, is the second-largest and highest-growth asset category, driven by the complexity and value of specialty alloy recovery from high-specification reactors, heat exchangers, and distillation columns. Leading practitioners in the dismantling segment including Fluor Corporation's industrial services division and Bechtel Corporation's plant services group differentiate on the basis of heavy lift crane capacity exceeding 1,000 tonnes, proprietary demolition sequencing methodologies for hot-work environments, and integrated waste stream management capability embedded within the dismantling contract structure.

Site Remediation & Environmental Restoration

Site remediation and environmental restoration, at 22.2% of revenues and a CAGR of 7%, is the second-largest service segment and the one most directly exposed to regulatory enforcement intensity and escalation cycles. The segment encompasses soil and groundwater remediation, in-situ chemical treatment, permeable reactive barrier installation, bioremediation, and long-term environmental monitoring a technical service spectrum that demands environmental engineering expertise, regulatory agency interface capability, and specialist technology deployment in combination. Decontamination Services, at 2.9% of total revenues but commanding an above-average CAGR of 8.3%, represents the fastest-growing individual service subsegment, reflecting heightened regulatory and client expectations for thorough radiological, chemical, and biological contaminant removal prior to demolition a requirement that applies particularly to petrochemical, pharmaceutical, and nuclear facility closures.

Tetra Tech's environmental and radiological decontamination platform and CLEAN HARBORS' industrial services division have both made targeted technology investments and workforce development commitments in this area over the review period, positioning them as preferred specialty subcontractors within integrated decommissioning programs. Engineering & Consulting Services, at 11.9% and a CAGR of 7.6%, anchors the front-end of the service chain: the growing demand for integrated delivery is pulling advisory firms further into project execution roles, effectively collapsing the traditional boundary between consulting and contracting.

By Region

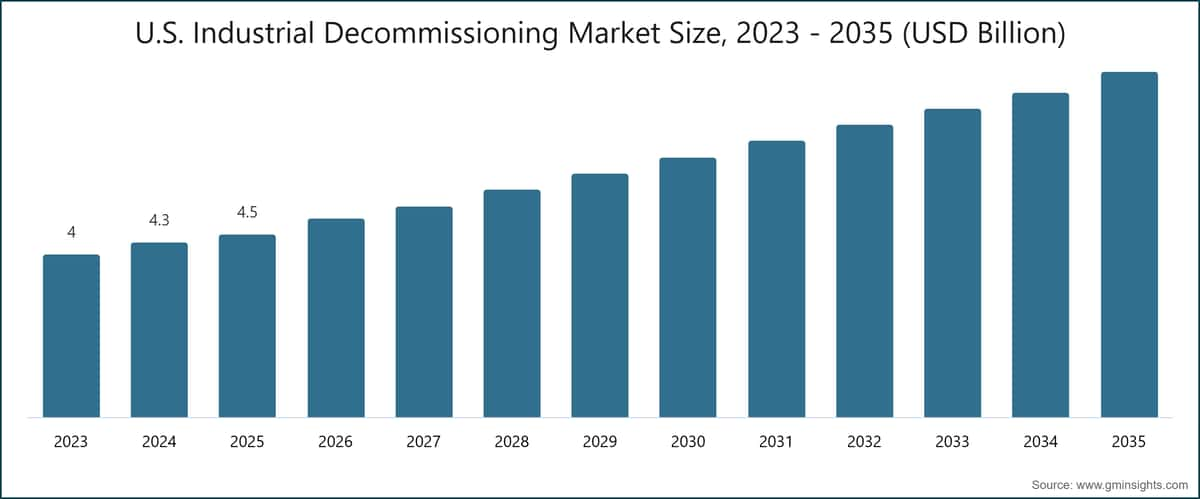

North America Industrial Decommissioning Market

North America commands the largest regional market share at 34.9% of global revenues in 2025, expanding at a CAGR of 6.2% through the forecast period a growth rate that reflects the region's status as a mature but structurally active decommissioning market rather than an emerging one. The United States drives regional demand across all primary end-use sectors: the EPA's RCRA Corrective Action program currently oversees more than 3,700 industrial facilities subject to active corrective action obligations, representing a sustained multi-year remediation and decommissioning pipeline with non-discretionary regulatory timelines.

The U.S. Department of Energy's Office of Environmental Management responsible for the decontamination and decommissioning of the nation's former nuclear weapons production complex maintains an annual budget exceeding USD 7.5 billion, positioning the federal government as the single largest decommissioning project owner in North America. Canada contributes materially to regional demand through the decommissioning of oil sands extraction and upgrading facilities in Alberta, where the Alberta Energy Regulator's tightening Liability Management Framework is progressively reducing operators' ability to defer closure obligations. Across both countries, the dominant project scale is shifting toward large and mega-scale programs, as multi-asset corporate decommissioning campaigns and integrated federal environmental management contracts displace smaller, facility-specific work orders.

Europe Industrial Decommissioning Market

Europe holds 31.6% of global market revenues in 2025, expanding at a CAGR of 5.4% a measured pace that reflects the region's mature regulatory infrastructure and the established domestic capacity of European decommissioning contractors, both of which moderate the supply-demand tension that drives more rapid growth in developing markets. The United Kingdom's North Sea program is the region's highest-profile demand driver: the North Sea Transition Authority's GBP 20 billion decommissioning cost estimate through 2035 represents a clearly defined project pipeline distributed across AECOM, Worley, Aker Solutions, Wood, and multiple specialized subsea and onshore contractors.

Germany's Energiewende policy which resulted in the shutdown of the country's last three nuclear power plants in April 2023 has transferred a complex, multi-site nuclear decommissioning program to operators including EnBW, RWE, and E.ON, with the German federal government's provisioned nuclear decommissioning liability estimated at approximately EUR 47 billion. France's 56-reactor nuclear fleet represents the largest single national nuclear decommissioning obligation in Europe, with Électricité de France (EDF) managing decommissioning provisioning levels subject to active regulatory scrutiny by the French Nuclear Safety Authority (ASN). Italy and Spain are generating decommissioning demand from the closure of aging petrochemical complexes and legacy industrial sites under tightening EU Environmental Liability Directive enforcement, with Veolia, REMONDIS, and Tradebe Environmental Services well positioned across these national programs.

Asia Pacific Industrial Decommissioning Market

Asia Pacific is the market's highest-growth region, expanding at a CAGR of 10.4% a rate more than four percentage points above the global composite driven by the accelerating industrial aging cycle across China and India, the rapid buildup of offshore decommissioning obligations in Australian and Southeast Asian waters, and the progressive strengthening of environmental enforcement frameworks across the region. China's industrial base, constructed at scale during the 1980s and 1990s, is entering a phase of systematic asset retirement, with the government's dual carbon targets mandating the closure of sub-threshold coal power capacity and the remediation of thousands of legacy chemical and manufacturing sites under the Soil Pollution Prevention and Control Law enacted in 2018.[10]Ministry of Ecology and Environment People's Republic of China, mee.gov.cn In our Q4 2025 expert panel with nine senior decommissioning practitioners actively operating across China and India, participants converged on a common assessment: the primary bottleneck constraining project delivery growth over the next 24–36 months is not regulatory capacity or capital both of which are improving but rather certified workforce depth in hazardous waste handling, advanced soil remediation, and radiological decontamination, a gap that multinational contractors are beginning to address through joint venture structures and domestic training partnerships. India's decommissioning market is being driven by the National Green Tribunal's increasingly stringent site closure orders, the Ministry of Environment's expanding hazardous site inventory, and the growing recognition by major industrial conglomerates of end-of-life financial liabilities across their legacy manufacturing footprints. SLB and Halliburton have both signaled accelerated investment in Asia Pacific decommissioning service lines, targeting the region's rapidly growing offshore well plug and abandonment market across Malaysian, Indonesian, and Australian basins.

Industrial Decommissioning Market Share

The market exhibits moderate concentration at the leadership tier, with the five largest players Fluor Corporation, AECOM, Bechtel Corporation, Worley, and Jacobs collectively holding approximately 36% of total global revenues in 2025. Fluor Corporation leads the competitive hierarchy with an estimated 8% market share, a position sustained by the firm's integrated EPC heritage, its dominant position in U.S. federal nuclear and chemical site decommissioning, and its long-term framework contract base with major multinational oil & gas operators. The remaining 64% of market revenues is distributed across a fragmented competitive landscape of regional specialists, environmental services firms, subsea contractors, and sector-specific decommissioning providers a structure that reflects the market's inherent geographic and technical diversity and the persistent preference of many project owners for local execution knowledge combined with international technical oversight.

Fluor Corporation's competitive position is built on the breadth and depth of its integrated project delivery model, spanning the full lifecycle from regulatory pre-planning and detailed engineering through physical execution and final site certification. The firm's government and defense decommissioning division which executes programs for the U.S. Department of Energy and the U.S. Department of Defense provides a stable, high-value revenue base structurally differentiated from commercially competed industrial work. AECOM's decommissioning practice is grounded in its environmental engineering and nuclear heritage, with particular strength in U.S. federal environmental management programs and European nuclear decommissioning advisory a combination that positions the firm strongly across the two highest-value regulatory-driven demand segments. Bechtel Corporation contributes deep project management capability and heavy civil construction capacity to large-scale process plant and nuclear facility decommissioning, with a track record on some of the most technically complex closure programs in the U.S. government portfolio.

Worley's decommissioning and brownfield services capability was materially expanded by its 2019 acquisition of the Jacobs energy, chemicals, and resources business, which added significant North Sea, Australian, and Middle Eastern project capacity. Jacobs following its subsequent strategic portfolio reorganization has concentrated decommissioning capabilities within its critical mission solutions and people & places solutions divisions, maintaining a strong competitive position in U.S. federal environmental management and complex infrastructure remediation. Below the top five, KBR has established a focused position in nuclear decommissioning through its role as managing contractor for elements of the UK Nuclear Decommissioning Authority's legacy estate, while TechnipFMC brings subsea engineering and deepwater installation withdrawal expertise specifically applicable to the growth segment of offshore infrastructure decommissioning.

M&A activity within the sector has been strategically targeted rather than broadly consolidative. Amentum Services originally spun out of AECOM's government services division in 2020 and subsequently repositioned through additional combination has emerged as a specialized pure-play in U.S. government and defense environmental management. The broader competitive dynamic reflects a progressive capability bundling imperative: firms able to offer regulatory compliance management, multi-discipline engineering, physical execution, waste management, and site certification within a single contract vehicle are consistently capturing premium pricing, preferred contractor designations, and long-term framework agreements across the market. The data indicates that firms continuing to offer point-solution services face increasing commercial pressure as integrated contract structures displace disaggregated procurement models across the market's highest-value segments.

Industrial Decommissioning Market Companies

Major players operating in the industrial decommissioning industry are:

AECOM, AF Gruppen, Aker Solutions, Amentum Services, AtkinsRéalis, Babcock International Group, Baker Hughes Company, Bechtel Corporation, CLEAN HARBORS, Enviri Corporation, Fluor Corporation, Halliburton, Jacobs, KBR, Ramboll, REMONDIS, SLB, Stantec, TechnipFMC, Tetra Tech, Tradebe Environmental Services, Veolia, Wood, Worley.

AECOM is a global infrastructure and environmental services firm with deep capabilities across nuclear decommissioning, contaminated land remediation, and U.S. federal environmental management. The company has been a long-standing prime contractor and subcontractor to the U.S. Department of Energy's Office of Environmental Management and maintains a material European presence on nuclear decommissioning programs in the United Kingdom and the broader EU. AECOM's environmental services division is one of the most technically diversified in the market, spanning radiological characterization, soil treatment technology selection, and long-term environmental monitoring.

AF Gruppen is a leading Norwegian construction and industrial services group with specialized capabilities in offshore structure reception, materials processing, and circular economy decommissioning. The company's Stord facility on the western Norwegian coast is one of the world's foremost onshore reception and recycling yards for decommissioned offshore structures, having processed multiple North Sea platform topsides with total material recovery rates exceeding 97% by weight a benchmark that has materially shaped North Sea decommissioning contracting standards.

Aker Solutions is a Norwegian energy services firm providing engineering, late-life asset management, and integrated decommissioning services to the offshore oil & gas sector. The company has been actively involved in the development and commercialization of cost-efficient well plugging and abandonment methodologies and platform removal concepts for the Norwegian Continental Shelf, and maintains framework agreement positions with major North Sea operators.

Amentum Services is a U.S.-based government services and environmental management specialist with a primary focus on U.S. federal nuclear and hazardous waste decommissioning programs. The company manages multiple long-term programs under the U.S. Department of Energy's Environmental Management portfolio, including complex multi-year facility decontamination, waste characterization, and site closeout programs at former weapons production facilities.

AtkinsRéalis (formerly SNC-Lavalin) offers integrated engineering and project delivery services across industrial and nuclear decommissioning in Canada, the United Kingdom, and internationally. The firm's nuclear decommissioning capability encompasses both CANDU reactor systems in Canada and UK Advanced Gas-cooled Reactor (AGR) and Magnox station decommissioning programs, supported by a dedicated nuclear services practice with regulatory interface capability in multiple jurisdictions.

Babcock International Group is a UK-based defense and critical technology services company with substantial nuclear decommissioning capabilities, particularly in the UK civil and naval nuclear sectors. Babcock supports the UK Nuclear Decommissioning Authority on multiple legacy Magnox station closure programs and provides specialist decommissioning engineering, project management, and radiological waste handling services across the UK nuclear estate.

Baker Hughes Company provides oilfield services including well decommissioning, plug and abandonment (P&A), and late-life production management services to upstream oil & gas operators globally. The company's intervention and decommissioning technology platforms are deployed across the North Sea, Gulf of Mexico, and Middle Eastern operating basins, with a growing focus on rig less P&A solutions that reduce the cost and carbon footprint of offshore well closure programs.

Bechtel Corporation is a global engineering, procurement, and construction firm with a dedicated decommissioning capability concentrated within its nuclear and environment division and its government services group. Bechtel has managed some of the most technically complex industrial and environmental remediation programs within the U.S. government portfolio, including nuclear weapons facility closure programs at Department of Energy sites, and has an expanding international industrial decommissioning practice.

CLEAN HARBORS is the largest environmental services company in North America, with core capabilities in hazardous waste collection, treatment, and disposal, industrial cleaning, emergency response, and complex site remediation. The company's industrial services division provides decontamination, tank and vessel cleaning, vacuum services, and industrial waste management support across multiple decommissioning sectors, and its permitted hazardous waste disposal infrastructure represents a critical end-destination asset within integrated decommissioning program supply chains.

Enviri Corporation (formerly Harsco Corporation) provides industrial environmental solutions including byproduct processing, material recovery, and on-site waste management services. The company's expertise in industrial waste stream management and circular economy service delivery positions it as a specialist complementary service provider within complex industrial decommissioning programs, particularly in the steel, metals, and minerals processing sectors.

Fluor Corporation is the market leader in industrial decommissioning, operating across government nuclear, petrochemical, oil & gas, and industrial manufacturing sectors. The firm's integrated EPC delivery model and dedicated federal environmental management division which holds long-term prime contracts with the U.S. Department of Energy provide a structurally differentiated competitive position combining technical depth, scale, and a demonstrated track record on high-complexity, high-consequence programs.

Halliburton provides well decommissioning, P&A, and late-life well management services to upstream oil & gas operators across all major producing basins globally. The company's completion and production segment includes specialized P&A engineering and execution services for both offshore and onshore wells, with active programs in the Gulf of Mexico, North Sea, Middle East, and the growing Asia Pacific decommissioning market.

Jacobs operates in decommissioning through its Critical Mission Solutions division which serves U.S. federal nuclear and defense environmental management and its People & Places Solutions division, which addresses commercial industrial and infrastructure remediation. The firm's analytical laboratory services, environmental monitoring systems, and digital project controls platforms provide meaningful technical differentiation within complex, multi-phase decommissioning programs.

KBR is a global engineering and government services firm with a focused nuclear decommissioning franchise built principally around its role as a managing contractor for the UK Nuclear Decommissioning Authority's legacy nuclear estate. KBR's decommissioning capability spans technical project management, complex radiological waste characterization and packaging, regulatory authority interface, and nuclear decommissioning asset management skills developed over decades of continuous engagement with the UK nuclear program.

Ramboll is a Danish professional services and engineering consulting firm with capabilities across environmental impact assessment, site remediation strategy, contaminated groundwater management, and decommissioning planning advisory. The company's Nordic heritage provides particular strength in North Sea decommissioning advisory, regulatory pre-approval process navigation, and environmental baseline assessment for major offshore decommissioning programs.

REMONDIS is a Germany-headquartered waste management and industrial services group with core capabilities in hazardous waste treatment, contaminated soil management, and industrial facility decontamination. The company's extensive European waste treatment and disposal infrastructure including specialized facilities for persistent organic pollutants, heavy metal-contaminated soils, and process chemicals provides critical treatment and disposal end-destination capacity for industrial decommissioning waste streams across the EU.

SLB (formerly Schlumberger) provides technology-enabled oilfield services including well decommissioning, P&A, and late-field production management. SLB's rig less P&A technology platforms are enabling measurable cost and cycle time reductions in offshore well decommissioning, with deployment programs in the North Sea, Gulf of Mexico, and Asia Pacific. The company's expanding decommissioning services line is strategically aligned with the growing global inventory of mature oil & gas assets.

Stantec is a Canadian professional services firm with environmental engineering and contaminated site remediation capabilities concentrated in North America. The company's contaminated site assessment, remedial design, and environmental monitoring practice serves a broad spectrum of industrial decommissioning clients across the oil & gas, mining, and manufacturing sectors in Canada and the United States.

TechnipFMC is a subsea technology and services company with specialized capabilities in offshore well decommissioning, pipeline decommissioning, subsea infrastructure removal, and deepwater engineering. The company's integrated subsea engineering, installation, and services model encompassing reel-lay systems and advanced subsea intervention tools is specifically relevant to the deepwater offshore decommissioning segment, which represents a high-growth, high-value component of the global market.

Tetra Tech is a U.S.-based environmental services and consulting firm with deep capabilities in contaminated site remediation, radiological cleanup, and federal environmental management. The company's nuclear and radiological services division has executed decommissioning programs for the U.S. Nuclear Regulatory Commission, the Department of Energy, and commercial nuclear operators, with expertise in radiological characterization, decontamination technology selection, and waste classification and disposal.

Tradebe Environmental Services is a Spanish-origin environmental services company providing hazardous waste collection, physicochemical treatment, solvent recovery, and industrial waste disposal services across Europe and North America. The company's integrated waste management capabilities serve as essential ancillary services within large-format industrial decommissioning programs, particularly where legacy chemical inventories and process waste streams require specialized treatment prior to disposal.

Veolia is a global environmental services leader with capabilities spanning industrial waste management, water and wastewater treatment, site remediation, and integrated circular economy decommissioning. Veolia's end-to-end decommissioning model combining hazardous waste management, industrial decontamination, material recovery, and site environmental certification has been deployed on multiple major European refinery and chemical complex closures, establishing the company as one of the most integrated environmental service providers in the sector.

Wood is a UK-headquartered engineering and consulting firm with established capabilities in brownfield engineering, late-life asset management, and decommissioning project delivery across the oil & gas, power generation, and industrial manufacturing sectors. Wood's Operations division provides integrated late-life and decommissioning advisory and execution services to clients across the North Sea, Australia, and the Americas, with a particular focus on cost-efficient and schedule-reliable delivery of large multi-discipline programs.

Worley is an Australian-headquartered engineering and industrial services company with a comprehensive decommissioning and brownfield services capability spanning concept development, regulatory pre-approval, detailed engineering, execution management, and final site certification. Worley's Advisian consulting arm provides strategic decommissioning planning, cost benchmarking, regulatory strategy, and independent project review services to major industrial asset owners globally, positioning the firm as both an advisory and delivery partner across the full project lifecycle.

Market Share of 8%

Collective Market Share of 30%

Industrial Decommissioning Industry News

Jun 2026: Worley was awarded a multi-year decommissioning framework agreement by a major North Sea operator, covering well P&A engineering, topsides removal planning, and onshore waste management logistics coordination across five end-of-life offshore installations.

Mar 2026: TechnipFMC completed the first commercial deployment of its standardized rig less P&A intervention system on a deepwater well in the Gulf of Mexico, demonstrating a 30% reduction in well decommissioning cycle time relative to conventional rig-based methods.

Feb 2026: Veolia announced the expansion of its industrial decommissioning and circular economy services platform in Germany, commissioning a dedicated specialty metals recovery facility co-located with its existing hazardous waste treatment infrastructure in Leverkusen to serve major industrial closure programs across Central Europe.

Jan 2026: KBR was awarded an extension of its managing contractor role for the UK Nuclear Decommissioning Authority's legacy Magnox estate, with an expanded scope including accelerated fuel removal and building decontamination programs at three additional sites.

Nov 2025: AECOM and Amentum Services announced a strategic teaming agreement targeting U.S. federal environmental management decommissioning programs, combining AECOM's environmental engineering and site remediation capability with Amentum's government program management infrastructure and cleared workforce.

Oct 2025: Fluor Corporation was selected as the prime contractor for a large-scale chemical plant decommissioning program on the U.S. Gulf Coast, encompassing full removal of processing units, contaminated soil remediation, groundwater treatment, and site certification across a 450-acre industrial footprint.

Sep 2025: The UK North Sea Transition Authority published its updated decommissioning cost estimate for the UK Continental Shelf, projecting total sector expenditure of GBP 20 billion through 2035 a formal revision that establishes the definitive scope reference for operator decommissioning programs and contractor pipeline planning.

Aug 2025: Aker Solutions secured an engineering and planning contract with Equinor for the Statfjord late-life and decommissioning program on the Norwegian Continental Shelf, one of the largest integrated offshore asset retirement programs currently in pre-execution development in the North Sea.

Market Concentration Score

The industrial decommissioning market scores 4 out of 10 on the market concentration scale, reflecting moderate-to-low consolidation at the leadership tier where the top five players collectively hold approximately 36% of global revenues offset by a highly fragmented competitive base of regional specialists, environmental services firms, and subsea contractors that collectively account for the remaining 64% of the market.

The industrial decommissioning market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

By End Use

Oil & gas

Power generation

Chemical & petrochemical

Mining & metals

Manufacturing

Marine & shipbuilding

Aerospace & defense

Others

By Service

Project planning & regulatory compliance

Engineering & consulting services

Asset retirement & shutdown management

Decontamination services

Dismantling & demolition

Waste management & disposal

Site remediation & environmental restoration

Material recovery & recycling

By Method

Full removal

Partial removal

Mothballing/ care & maintenance

Asset repurpose & redevelopment

In-situ decommissioning

By Asset Type

Buildings & structures

Process equipment

Pipelines & storage tanks

Boilers & pressure vessels

Electrical & control systems

Utility infrastructure

Offshore platforms

Heavy industrial machinery

By Project Size

Small-scale

Medium-scale

Large-scale

Mega-scale

The above information has been provided for the following regions & countries:

North America

U.S.

Canada

Mexico

Europe

UK

Germany

France

Italy

Spain

Netherlands

Norway

Denmark

Poland

Sweden

Asia Pacific

China

Japan

India

South Korea

Australia

New Zealand

Indonesia

Malaysia

Thailand

Middle East & Africa

Saudi Arabia

UAE

Qatar

Kuwait

Oman

Latin America

Brazil

Argentina

Chile

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →