Authors:

Preeti Wadhwani, Satyam Jaiswal

Download free PDF

Automotive Over-the-Air Testing System Market Size & Share 2026-2035

Report ID: GMI11479

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Automotive Over-the-Air Testing System Market

Get a free sample of this report

Get a free sample of this report Automotive Over-the-Air Testing System Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Automotive Over-the-Air Testing System Market Size

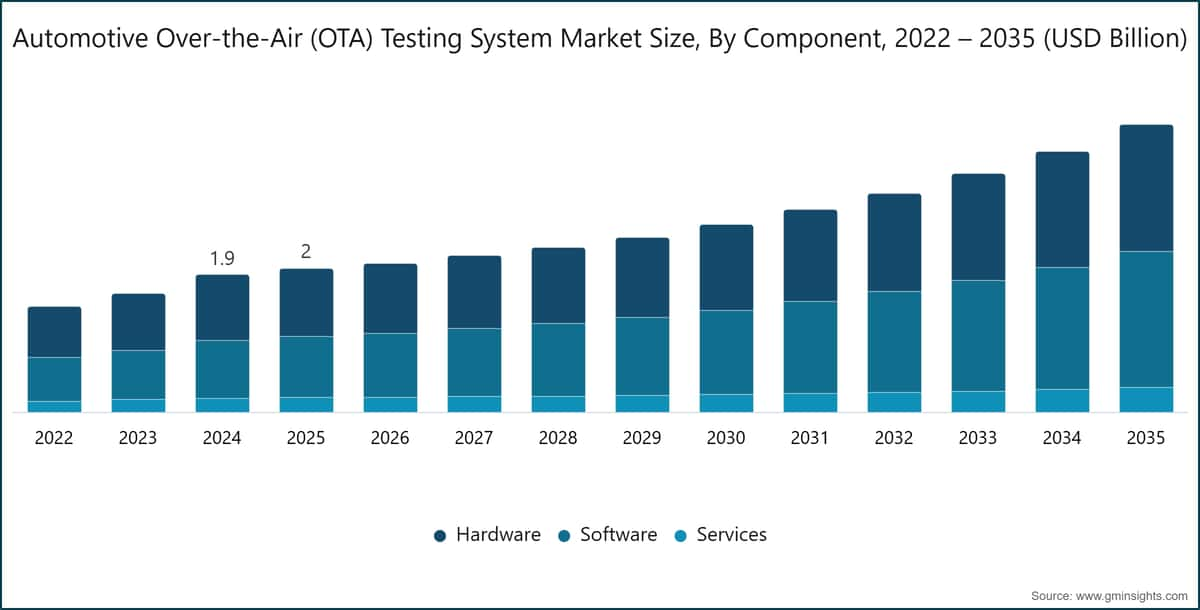

The global automotive over-the-air (OTA) testing system market reached USD 2 billion in 2025. The market is projected to grow from USD 2.1 billion in 2026 to USD 4 billion by 2035, expanding at a 7.6% CAGR over 2026–2035. These estimates are according to latest report published by Global Market Insights Inc.

Automotive Over-the-Air Testing System Market Key Takeaways

Market Leader: Continental led with over 10.6% market share in 2025.

Leading Players: Top 5 players in this market include Continental, Bosch, Intertek, Keysight Technologies, Vector Informatik, which collectively held a market share of 45.7% in 2025.

Growth reflects the automotive sector’s shift from dealership-based software flashing to cloud-mediated validation pipelines that must verify security, compatibility, and functional behavior before each remote update. Demand is strongest where connected vehicle penetration, electric vehicle software complexity, and regulatory scrutiny converge, led by North America, Western Europe, and urban Asia Pacific markets.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Increasing Adoption of Connected Vehicles

+2.3%

Global

Medium term (2-4 years)

Rapid Growth of Electric Vehicles (EVs)

+1.8%

Asia Pacific, Europe, North America

Medium term (2-4 years)

Stringent Vehicle Cybersecurity and Software Compliance Regulations

+2%

Europe, North America, Asia Pacific

Short term (≤ 2 years)

Rising Complexity of Vehicle Software Ecosystems

+1.5%

Global

Long term (≥ 4 years)

Increasing Adoption of Connected Vehicles

Connected vehicle penetration is widening the addressable base for OTA validation. GSMA estimates that connected car penetration in new vehicle sales will exceed 80% in developed markets by 2027.[1]GSMA, https://www.gsma.com The operational consequence is direct: OTA testing systems must validate releases across different model years, telematics control units, network operators, and regional software configurations. For OEMs, the core issue is not only the number of connected vehicles; it is the cadence of update campaigns moving closer to enterprise software release cycles.

Rapid Growth of Electric Vehicles (EVs)

Electric vehicles carry larger software stacks than internal combustion platforms because battery management, thermal control, regenerative braking, charging logic, and power electronics depend on frequent calibration updates. The International Energy Agency reported that global EV sales surpassed 17 million units in 2024, equal to roughly one-fifth of new vehicle sales.[2]International Energy Agency, https://www.iea.org Each EV added to the connected fleet creates recurring testing demand across its operating life. The automotive over-the-air (OTA) testing system market benefits directly as automakers move from isolated ECU validation toward system-level validation across powertrain, HMI, and charging interfaces.

Stringent Vehicle Cybersecurity and Software Compliance Regulations

Regulation has become a central purchasing trigger. UNECE WP.29 R156 requires certified software update management systems, while R155 requires cybersecurity management systems for connected vehicles; the framework applies across EU type approval and has influenced rules in other automotive markets.[3]United Nations Economic Commission for Europe, https://www.unece.org ISO/SAE 21434:2021 gives OEMs and suppliers the engineering framework for road vehicle cybersecurity, including threat analysis and validation practices.[4]International Organization for Standardization, https://www.iso.org The automotive over-the-air testing system market therefore captures compliance spending that cannot be postponed without affecting type approval and market access.

Rising Complexity of Vehicle Software Ecosystems

ACEA estimates indicate that modern premium vehicles can contain more than 150 million lines of code across 100 or more electronic control units.[5]European Automobile Manufacturers' Association, https://www.acea.auto As OEMs move toward domain controllers and zonal architectures, the number of ECUs may decline, but each compute node handles more software dependencies. OTA testing infrastructure must reproduce bus behavior, middleware interfaces, firmware dependencies, and application-layer interactions. This is pushing demand toward hardware-in-the-loop, software-in-the-loop, and cloud-based orchestration platforms that can validate an update before it reaches a vehicle fleet.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Cost and Complexity of Testing Infrastructure

-1.5%

Global, most acute in Latin America and Middle East & Africa

Short term (≤ 2 years)

Fragmented Vehicle Architectures and ECU Diversity

-1.2%

Global

Medium term (2-4 years)

High Cost and Complexity of Testing Infrastructure

A complete OTA testing environment can include HIL rigs, network simulators, RF chambers, security tooling, orchestration software, and audit reporting systems. The investment range runs from several hundred thousand dollars to multiple millions of dollars per installation, depending on scope. This cost profile limits adoption among Tier-2 suppliers, regional laboratories, and smaller service providers. Cloud-based virtual validation and shared certification infrastructure partly reduce the capital burden, although data residency, latency, and test-fidelity concerns remain unresolved.

Fragmented Vehicle Architectures and ECU Diversity

Vehicle architecture fragmentation keeps validation matrices large. A single OEM can support multiple bootloader versions, ECU generations, communication stacks, and real-time operating systems across a global vehicle portfolio. AUTOSAR and Automotive Grade Linux are improving standardization at the middleware level, yet convergence remains gradual rather than immediate.[6]Automotive Grade Linux, https://www.automotivelinux.org For testing vendors, this challenge supports demand for configurable platforms but increases implementation effort and post-sale engineering support.

Automotive Over-the-Air Testing System Market Trends

The shift toward software-defined vehicles is the most important structural trend in the automotive over-the-air (OTA) testing system market. Under older distributed architectures, many updates were limited to individual ECUs or tightly defined functional domains. Zonal and domain-controller designs change that boundary because one OTA package can affect several vehicle functions through shared compute, Ethernet backbones, and middleware. Automotive Grade Linux adoption by Toyota, Subaru, Mazda and other OEMs is helping standardize parts of the middleware layer, but it also raises expectations that test frameworks can operate across OEM-specific implementations. The timeline is medium to long term because architecture migration occurs by vehicle platform generation, not by annual model-year refresh alone. The market implication is a gradual movement away from point tools toward validation platforms that link HIL, SIL, regression automation, OTA backend simulation and compliance evidence in a single workflow.

AI-driven test automation is becoming relevant because full regression testing becomes costly when OTA campaigns move from annual updates toward monthly or bi-weekly releases. Machine learning models can process prior failure logs, dependency maps, ECU telemetry, and release history to identify test cases most likely to expose defects. In our Q1 2026 survey of 280 embedded software engineers and validation managers at automotive OEMs and Tier-1 suppliers across North America and Europe, 58% reported that AI-assisted test prioritization had reduced pre-deployment validation lead time by more than 20% compared with full-suite regression runs. The quantifiable impact appears in software demand: the software component is projected to expand at an 8.7% CAGR, outpacing hardware. The commercial implication is direct. Vendors that can combine explainable test selection, traceable audit output, and integration with tools such as Vector CANoe.OTA, dSPACE VEOS and ETAS ISOLAR will have stronger procurement relevance than vendors offering automation without compliance-grade reporting.

OTA updates transmitted across 5G and C-V2X channels face network behaviors that basic connectivity tests do not capture. Latency variance, cell handoff, bandwidth throttling, Doppler effects in high-speed driving, packet interruption, and recovery logic all need to be tested before a release reaches vehicles. ETSI GS MEC standards influence performance expectations for mobile edge computing in automotive applications, while C-V2X Rel-16 and Rel-17 deployment is raising test complexity in China, South Korea, Germany and the United States. Keysight Technologies’ UXM 5G Wireless Test Platform and Anritsu’s MT8000A Radio Communication Test Station are representative platforms used for cellular protocol and 5G OTA evaluation. The timeline is short to medium term because 5G automotive network buildout is already underway, but the full market effect depends on OEM adoption of C-V2X-enabled update channels. Testing vendors with multi-band, multi-condition RF simulation will gain share as performance validation becomes inseparable from functional validation.

Security testing accounted for USD 558.5 million in 2025, equal to 28.1% of global revenue, and is growing at an 8% CAGR. UNECE WP.29 R155 and R156 have made cybersecurity and software update management evidence part of the type-approval process, especially for connected vehicles sold into Europe. ISO/SAE 21434:2021 adds the technical engineering framework for cybersecurity risk management across the vehicle lifecycle. In our Q4 2025 expert panel with eight automotive cybersecurity specialists from European OEMs and independent testing laboratories, participants converged on the view that security testing will remain the highest-growth OTA testing sub-segment through at least 2028, driven by wider regulatory adoption in Japan, Korea and Canada. TÜV SÜD, DEKRA, SGS, AUTOCRYPT and Intertek are positioned to capture this category because OEMs need penetration testing, authentication validation, vulnerability assessment and documented evidence packages.

The remote testing segment gained momentum when physical lab access constraints accelerated OEM investment in cloud-connected vehicle representations and digital twins. Stellantis, working with dSPACE, deployed a cloud-based OTA validation architecture in 2024 that supports parallel campaign testing across simulated representations of more than 40 vehicle configurations. That example shows why remote testing matters: it scales compatibility validation faster than physical HIL rigs can when vehicle variants multiply. The constraint is fidelity. Digital twins still struggle to reproduce the full RF and electromagnetic environment of a physical vehicle, keeping lab-based RF validation and HIL infrastructure central to safety-critical and certification-sensitive use cases.

Automotive Over-the-Air Testing System Market Analysis

By Component

The hardware sub-segment held the largest 2025 position in the automotive over-the-air (OTA) testing system market, with USD 940.6 million in revenue and 47.4% share. It is projected to reach USD 1.75 billion by 2035 at a 6.8% CAGR. Hardware demand covers anechoic and semi-anechoic chambers, network impairment appliances, HIL benches, scanner arrays, and cellular protocol test systems used to validate OTA antenna performance and update delivery behavior. Rohde & Schwarz’s CMX500 OBT platform and R&S ATS chamber systems address RF and antenna test needs, while Keysight’s UXM 5G platform supports multi-band OTA simulation for C-V2X and cellular conditions. Hardware growth is slower than software because many North American and European labs already have baseline infrastructure, but refresh demand remains tied to 5G mmWave, 5G Sub-6 GHz, and more complex multi-antenna vehicle designs.

Software is the fastest-growing component, expanding from USD 847.8 million in 2025 to USD 1.89 billion by 2035 at an 8.7% CAGR. This includes test orchestration, AI-assisted regression selection, digital twin simulation, audit trail generation, API integration layers, and cloud-based campaign management. Vector Informatik’s CANoe.OTA and dSPACE’s VEOS platform are widely used in validation workflows because they integrate with existing automotive engineering toolchains rather than forcing a separate testing environment. Services accounted for USD 197.6 million in 2025 and are projected to reach USD 341.4 million by 2035, supported by managed testing, certification preparation, and compliance documentation needs. Within this segment, the stronger long-term economics favor vendors that bundle software, certification evidence, and expert services around existing lab assets.

By Offering

Learn more about the key segments shaping this market

Download Free PDF

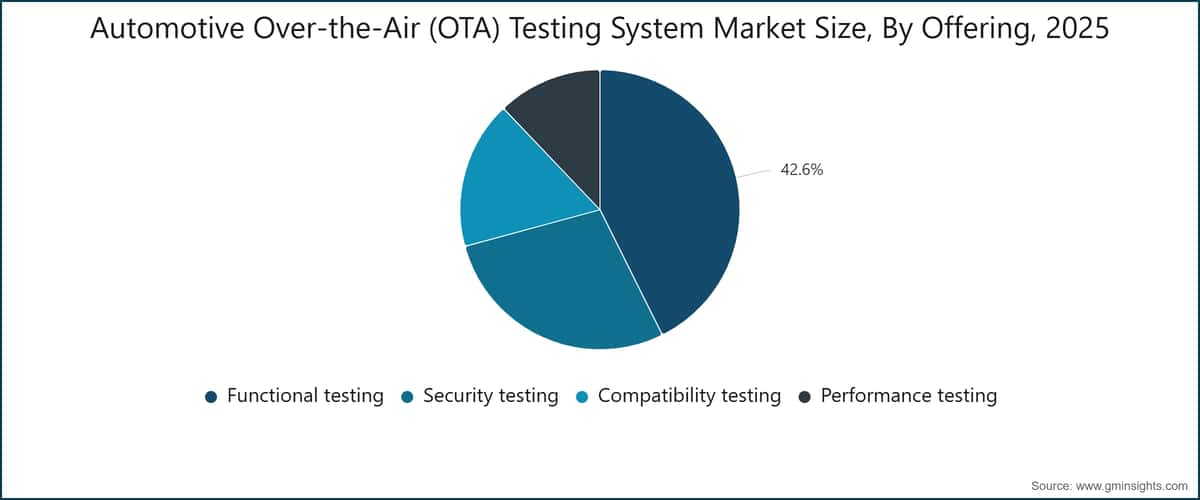

Functional testing remains the largest offering, with USD 846.6 million in 2025 revenue, 42.6% of automotive over-the-air testing system market share, and a forecast value of USD 1.61 billion by 2035 at a 7% CAGR. Functional testing verifies installation success, correct execution, rollback behavior, ECU interaction, and absence of regression across target vehicle populations. NI VeriStand and ETAS ISOLAR are representative platforms used in functional validation because they support HIL workflows, integration testing, and software behavior verification. Compatibility testing is the fastest-growing offering, increasing from USD 340 million in 2025 to USD 795.5 million by 2035 at a 9.2% CAGR. Its growth reflects fleet heterogeneity: OTA campaigns often target multiple model years, hardware revisions, firmware states, and regional variants at the same time.

Security testing represented USD 558.5 million in 2025, or 28.1% share, and is projected to expand at an 8% CAGR. This category includes penetration testing, authentication validation, certificate-chain verification, backend update-server assessment and vulnerability testing of the firmware being delivered. Performance testing accounted for USD 240.9 million in 2025, equal to 12.1% share, with a 6.1% CAGR. Performance testing remains necessary for throughput, update latency, and transfer reliability metrics, but its growth is more incremental because RF methodologies are more mature than compatibility and cybersecurity workflows. Across all offerings, the automotive over-the-air (OTA) testing system market is moving toward integrated platforms that produce a single evidence trail across functional, security, compatibility, and performance requirements.

By Testing Method

Lab testing remains the technical anchor of OTA validation because safety-relevant updates need controlled, repeatable and auditable test conditions. HIL rigs, SIL environments, anechoic chambers, RF simulators, and network impairment systems allow engineers to validate boundary conditions that cannot be safely reproduced in open-road settings. Keysight UXM 5G, Anritsu MT8000A, Rohde & Schwarz CMX500 and ETS-Lindgren chamber systems are examples of platforms used in lab-based OTA and RF testing. Lab testing is especially relevant for UNECE WP.29 evidence generation because certification submissions require documentation, repeatability, and traceable test outcomes.

Field testing remains necessary where real-world network behavior, vehicle motion, climate, and driver usage patterns affect OTA delivery. This method is used to confirm that laboratory assumptions hold under operating conditions, particularly for C-V2X handoff, degraded signal environments, and fleet-level campaign staging. Remote testing is the fastest-growing method, reaching USD 331.9 million in 2025 and forecast to reach USD 771.1 million by 2035 at a 9.1% CAGR. dSPACE Cloud Automotive Testing and Stellantis’ 2024 deployment show how remote validation can scale variant coverage across simulated vehicle configurations. The market will not shift entirely to remote testing, however, because RF-sensitive and certification-sensitive scenarios still require physical test assets.

By Application

Software updates are the core application for OTA testing systems because every remote release must be assessed for installation integrity, rollback behavior, compatibility, and post-installation function. In passenger EV programs, a battery management update may affect charging behavior, thermal management, regenerative braking, range estimates and HMI indicators. Tesla fleet updates, General Motors Ultium-based platforms, and Ford Mustang Mach-E programs illustrate the operational reality of vehicles that require ongoing software validation after sale. The automotive over-the-air (OTA) testing system market therefore expands in parallel with post-delivery vehicle software management.

Security patches are gaining strategic weight as connected vehicles become exposed to remote attack surfaces. AUTOCRYPT’s OTA security testing portfolio, TÜV SÜD’s WP.29 R156 certification practice, and DEKRA’s automotive cybersecurity services address this application directly. Diagnostic testing is another important application because remote diagnostics often precede an OTA campaign and help identify affected ECUs, firmware states, or vehicle cohorts. The “others” category includes infotainment updates, telematics tuning, ADAS calibration support, and connectivity-stack adjustments. Application demand is increasingly bundled: a single release can require functional checks, security assessment, diagnostic validation, and performance testing before deployment approval.

By Vehicle

Passenger vehicles form the primary demand base because they represent the largest connected vehicle population and include the highest concentration of infotainment, ADAS, EV powertrain, and telematics update requirements. Tesla’s full fleet, Ford’s Mustang Mach-E, and General Motors’ Ultium-based models require ongoing OTA validation infrastructure as software functions expand after sale. In this segment, validation complexity comes from fleet scale and configuration diversity. A release may need to cover different model years, battery packs, regional regulatory settings, and hardware revisions while preserving consistent driver-facing performance.

Commercial vehicles create a different OTA testing profile. Fleet operators place greater emphasis on uptime, predictable campaign scheduling, telematics integration, and cybersecurity because failed updates can disrupt revenue-generating assets. In our H2 2025 survey of 190 fleet operators and automotive service providers across China, South Korea, and India, 67% reported that the frequency of OTA testing campaigns had increased by more than 30% over the prior 18 months, with cybersecurity validation identified as the main incremental test category. Commercial vehicle validation also intersects with route-specific connectivity, depot-based update staging, and vehicle health monitoring. These requirements support demand for managed services and remote testing workflows that can validate updates before fleetwide rollout.

By End User

Automotive OEMs are the dominant end users because they own the vehicle software release process, type-approval obligations, and customer experience risk. OEM teams use platforms such as Vector CANoe.OTA, dSPACE VEOS, NI VeriStand, and ETAS ISOLAR to validate updates across development, pre-production, and post-sale workflows. Telecommunication companies enter the market through C-V2X performance validation, cellular conformance testing, and network operator certification. ETSI GS MEC standards and C-V2X Rel-16/Rel-17 deployment make telecom participation more relevant as OTA delivery depends on edge computing, latency management, and cellular network reliability.

Automotive service providers, testing laboratories, and certification bodies occupy a growing part of the end-user base. Intertek, TÜV SÜD, DEKRA, SGS, Applus+ IDIADA, and GAES Testing & Certification provide third-party testing evidence, cybersecurity assessments, and type-approval support. Research and development institutes use OTA testing systems for early architecture validation, ADAS update assessment, and connected vehicle experimentation. The end-user split is therefore moving beyond OEM engineering departments toward a broader validation chain. That broadening supports market growth because compliance, network performance, and cybersecurity evidence often require independent verification.

By Region

North America Automotive Over-the-Air (OTA) Testing System Market

North America is the largest regional market, generating USD 852.2 million in 2025, equal to 42.9% of global revenue, and it is projected to reach USD 1.64 billion by 2035 at a 7.1% CAGR. The United States automotive over-the-air testing system market accounted for USD 738.8 million in 2025, supported by NHTSA cybersecurity guidance, high connected vehicle penetration, and the OTA requirements of Tesla, Ford Mustang Mach-E, and General Motors Ultium-based platforms. Canada contributed USD 113.3 million in 2025, with testing activity concentrated around supplier facilities in Ontario and Quebec. Keysight Technologies’ lab network across Michigan and California reflects the region’s demand for co-located RF, 5G, and protocol validation support. The market remains mature, but software renewal, EV fleet expansion, and cybersecurity evidence requirements keep spending active.

Europe Automotive Over-the-Air (OTA) Testing System Market

Europe generated USD 599.4 million in 2025 and is projected to reach USD 1.25 billion by 2035 at an 8% CAGR. Germany accounted for USD 171.1 million in 2025, supported by OEM and Tier-1 concentration across Munich, Stuttgart, and Wolfsburg. UNECE WP.29 R155 and R156 enforcement across EU-produced vehicles from July 2024 converted OTA validation into a production compliance obligation rather than a program-specific engineering choice. TÜV SÜD’s March 2024 dedicated OTA software update certification practice in Munich and Berlin, together with SGS’s Frankfurt cybersecurity testing center, shows how certification bodies are responding to demand. The United Kingdom remains aligned with WP.29 principles through its UKCA framework, while France, Italy, Spain, and CEE markets are included in the Rest of Europe segment growing at an 8.3% CAGR.

Asia Pacific Automotive Over-the-Air (OTA) Testing System Market

Asia Pacific is the fastest-growing region, advancing from USD 319.7 million in 2025 to USD 738.8 million by 2035 at a 9.1% CAGR. China is the principal growth engine, rising from USD 150.8 million in 2025 to USD 366.4 million by 2035 at a 12.1% CAGR, supported by EV deployment, C-V2X infrastructure, and more than 3,000 kilometers of smart highway corridors under the Ministry of Transport’s 2025 connected vehicle deployment program. India is the leading emerging opportunity in the region, with AIS 189 establishing a national cybersecurity basis for connected vehicles and supporting OTA testing demand among Tata Motors, Mahindra & Mahindra, and other domestic OEMs. Japan and South Korea are more technology-led, with Toyota’s Woven City project in Susono, Japanese OEM engineering centers in Aichi Prefecture, Accuver’s C-V2X testing position, and AUTOCRYPT’s security testing portfolio contributing to advanced OTA validation use cases. The region combines volume growth in China and India with high-specification validation demand in Japan and South Korea.

Automotive Over-the-Air Testing System Market Share

The automotive over-the-air (OTA) testing system industry is moderately concentrated. The top seven players held 52.2% of global revenue in 2025, while the remaining 47.8% was distributed across specialist equipment suppliers, certification bodies, regional test laboratories and cybersecurity vendors. This structure gives leading vendors pricing power in integrated programs, but it still leaves room for niche firms that solve narrow RF, security, or compliance problems.

Continental leads with 11.6% share. Its advantage comes from the ability to address OTA backend infrastructure, ECU bootloader technology, and validation services within a single supplier relationship. Bosch holds 10.6% share, and ETAS GmbH adds another 2.8% as a Bosch Group business focused on automotive development toolchains and middleware. The combined Bosch Group presence is therefore approximately 13.4%, although ETAS competes as a distinct brand in toolchain procurement. This matters for OEMs because ECU hardware familiarity and software validation tooling often influence each other during platform-level sourcing decisions.

Intertek holds 9.4% share and represents the independent testing and certification side of the automotive over-the-air (OTA) testing system market. OEMs use third-party validation evidence when regulatory submissions, customer audits, or internal governance require independent review. Keysight Technologies holds 7.3% share, with strength in RF simulation, cellular protocol testing, and 5G OTA performance validation. Its acquisition of Anite in 2015 gave the company a strong cellular testing base, which remains relevant as OTA delivery moves toward 5G and C-V2X channels.

Vector Informatik, at 6.8% share, benefits from deep installation of CANoe across European and North American engineering teams. The CANoe.OTA module extends that installed base into OTA validation without forcing OEMs to rebuild their tool environment. dSPACE GmbH holds 3.7% share and is strongest in simulation, HIL, SIL, and cloud-hosted validation through VEOS and Cloud Automotive Testing. M&A activity has reshaped the competitive base as well. Emerson’s 2023 acquisition of National Instruments for approximately USD 8.1 billion created NI (Emerson Test & Measurement), adding PXI hardware, VeriStand software, and automotive HIL relationships to a broader industrial automation platform.

Competitive strategy is moving in four directions. First, hardware vendors are adding software orchestration to protect margins as chambers and RF platforms mature. Second, software vendors are strengthening cybersecurity reporting and compliance documentation. Third, certification bodies are building dedicated WP.29 R155/R156 practices, as seen with TÜV SÜD, DEKRA, SGS, and Intertek. Fourth, cybersecurity specialists such as AUTOCRYPT are integrating PKI, intrusion detection simulation and V2X security testing into OTA validation workflows. The automotive OTA testing system market will likely remain moderately concentrated because buyers prefer integrated, audit-ready platforms for regulated releases, but specialized vendors can still win where technical depth matters more than scale.

Automotive Over-the-Air Testing System Market Companies

Major players operating in the automotive over-the-air (OTA) testing system industry are:

• Rohde & Schwarz

• Keysight Technologies

• Anritsu

• NI (Emerson Test & Measurement)

• ETS-Lindgren

• Microwave Vision (MVG)

• Vector Informatik

• dSPACE GmbH

• DEKRA

• TÜV SÜD

Rohde & Schwarz competes through RF and cellular test depth, including the CMX500 OBT platform and R&S ATS anechoic systems used for radiated performance, antenna behavior, and cellular conformance testing. Keysight Technologies is one of the strongest 5G OTA protocol testing vendors, with the UXM 5G platform supporting sub-6 GHz and mmWave scenarios for connected vehicle validation. Anritsu’s MT8000A Radio Communication Test Station gives the company a role in 5G NR OTA evaluation, especially in Japanese automotive engineering programs.

NI (Emerson Test & Measurement) brings PXI hardware and VeriStand software into OTA validation through Emerson’s broader test and measurement division. ETS-Lindgren focuses on EMC and antenna test systems, making it relevant where vehicle-level RF behavior needs chamber-based validation. Microwave Vision Group serves antenna measurement and OTA testing needs through StarLab and STARGATE systems, with relevance in both R&D and certification environments. Bluetest’s RTS65 and RTS75 reverberation chambers support compact antenna characterization for telematics development.

Vector Informatik and dSPACE GmbH are central software and simulation vendors. Vector’s CANoe.OTA capability supports OTA validation across CAN, LIN, Ethernet, and wireless layers, while dSPACE’s VEOS and Cloud Automotive Testing environments support SIL and cloud-hosted execution. ETAS, although discussed under Bosch Group in market share, is also important through ISOLAR and automotive middleware validation. These companies benefit from existing engineering workflow adoption, which lowers friction when OEMs expand into OTA-specific testing.

Certification and services companies address the compliance side of the automotive over-the-air (OTA) testing system market. DEKRA, TÜV SÜD, SGS, Applus+ IDIADA, Intertek, and GAES Testing & Certification provide independent testing evidence, cybersecurity assessment, and type-approval support. TÜV SÜD’s 2024 dedicated OTA certification practice for UNECE R156 and SGS’s Frankfurt cybersecurity testing center point to growing demand for independent WP.29 evidence. AUTOCRYPT focuses on security testing for PKI-based update authentication, intrusion detection, and V2X protocol validation, aligning directly with R155 cybersecurity requirements.

Regional specialists round out the competitive field. General Test Systems serves Chinese OEMs and technology companies with GB/T-aligned OTA test equipment. Accuver is active in C-V2X protocol conformance and OTA performance testing for Korean and Japanese markets. S.E.A. Datentechnik supports telematics and field data acquisition validation in the DACH region, while RanLOS and EMITE provide antenna and MIMO OTA systems for LTE and 5G automotive use cases. The company base is therefore diverse, but procurement increasingly favors vendors that can connect equipment, software, cybersecurity, and compliance evidence into a coherent validation workflow.

10.6% market share

Collective Market Share in 2025 is 45.7%

Automotive Over-the-Air Testing System Industry News

Apr 2025: TÜV SÜD expanded its automotive cybersecurity testing laboratory in Munich to include OTA software update campaign validation capabilities, adding four HIL testing stations for UNECE R156 compliance programs.

Feb 2025: Keysight Technologies expanded its UXM 5G Wireless Test Platform with automotive-specific OTA test profiles supporting C-V2X Rel-17 protocol scenarios for validation labs in Germany and South Korea.

Market Concentration Score

The automotive over-the-air (OTA) testing system market scores 6 out of 10 for concentration because the top seven players hold 52.2% of 2025 revenue, creating moderate leader influence while leaving 47.8% of demand open to specialist equipment vendors, cybersecurity firms, certification bodies, and regional laboratories.

The Automotive Over-the-Air testing system market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Component

Market, By Testing Method

Market, By Offering

Market, By Application

Market, By Vehicle

Market, By End User

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

Chapter 6 Market Estimates & Forecast, By Testing Method, 2022 - 2035 ($Mn)

Chapter 7 Market Estimates & Forecast, By Offering, 2022 - 2035 ($Mn)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

Chapter 10 Market Estimates & Forecast, By End User, 2022 - 2035 ($Mn)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

Chapter 12 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →