Authors:

Avinash Singh, Amita Thakre

Download free PDF

Action Figures Market Size & Share 2026-2035

Report ID: GMI15982

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Action Figures Market

Get a free sample of this report

Get a free sample of this report Action Figures Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Action Figures Market Size

The global action figures market was valued at USD 11.6 billion in 2025, recovering from a contraction to USD 10.3 billion in 2023 before registering renewed expansion through 2024 and accelerating into the current period. The market is projected to advance from USD 12.4 billion in 2026 to USD 22.6 billion by 2035, reflecting a compound annual growth rate of 6.9% over the forecast period, according to the latest report published by Global Market Insights Inc.

Action Figures Market Key Takeaways

Market Leader: Bandai Namco Toys & Collectibles led with over 18.5% market share in 2025.

Leading Players: Top 5 players in this market include Bandai Namco Toys & Collectibles, Hasbro, Inc., Funko, Inc., Mattel, Inc., Spin Master Corp, which collectively held a market share of 40.1% in 2025.

Entertainment intellectual property spanning major theatrical franchises, competitive gaming titles, and globally distributed anime content has become the primary licensing engine, directly coupling merchandise sell-through velocity to content performance cycles. The continued expansion of e-commerce infrastructure is simultaneously broadening geographic reach and enabling manufacturer-to-consumer sales in markets where conventional specialty retail networks remain underdeveloped.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Growing entertainment franchises increase merchandise demand

+2%

Global

Medium term (2–4 years)

Rising collector communities support premium purchases

+1.5%

North America, Europe, Asia Pacific

Long term (≥ 4 years)

Expanding e-commerce platforms improve accessibility

+1.2%

Global

Short term (≤ 2 years)

Growing Entertainment Franchises Increase Action Figure Merchandise Demand

The commercial success of major entertainment intellectual properties represents the most consistent structural driver of action figure demand. Film and television franchises developed by studios including Marvel Entertainment and Lucasfilm generate discrete merchandise windows tied to theatrical release calendars, with licensed toy agreements executed well in advance of premiere dates.

Toy Industry Association data from 2025 identifies entertainment-licensed action figures as the top-performing subcategory within the broader toy market in North America, with year-over-year growth outpacing non-licensed product lines for the third consecutive year [1]Toy Industry Association, https://www.toyassociation.org. Of greater strategic consequence is the extension of licensing into video game properties: titles including FromSoftware's Elden Ring, Bandai Namco's Dragon Ball Daima series, and Nintendo's Legend of Zelda franchise now carry equivalent licensing value to major theatrical releases, generating merchandise cycles independent of box-office performance.

The commercial model has also evolved structurally. Studios are increasingly negotiating merchandise royalty floors into licensing agreements rather than accepting flat-rate deals, aligning manufacturer incentives with franchise performance and creating more predictable revenue streams across multi-year content pipelines. Lead times between content announcement and licensed merchandise availability at retail have shortened from 18–24 months in the early 2010s to 9–12 months in current product development windows, reflecting manufacturer investment in faster tooling, digital sculpting workflows, and pre-production manufacturing commitments.

The reinforcing dynamic is self-sustaining: successful licensed launches strengthen studio-manufacturer relationships, increasing the probability of early IP access for the next release cycle, an asymmetric advantage that large manufacturers with established studio partnerships leverage more effectively than emerging competitors entering the licensing market.

Rising Collector Communities Support Premium Action Figure Purchases

The growth of organized collector communities operating across dedicated online platforms, fan conventions such as San Diego Comic-Con, and curated secondary markets has materially elevated average transaction values in the action figures market. Premium collectibles, defined as figures priced above USD 150 at retail, represent an expanding share of category revenue, supported by authentication platforms and specialist distributors that provide price discovery mechanisms for high-value items [2]US Census Bureau, https://www.census.gov. In our Q4 2025 survey of 480 collectors across the United States, United Kingdom, and Japan, 67% of respondents reported increasing their annual collectibles spending year-over-year, with a mean annual expenditure of USD 420 per respondent, up from approximately USD 310 in 2023.

The secondary market functions as a critical amplifier of primary retail demand. Platforms including StockX and eBay's authenticated collectibles tier have established resale premiums of 40–200% above retail for limited-edition figures, creating a financial incentive structure that accelerates first-sale velocity at initial retail and sustains category engagement between release cycles. Pre-order campaigns and crowdfunding milestones, particularly those tied to retailer-exclusive and convention-exclusive product lines simultaneously allow manufacturers to gauge demand before committing to full production runs, materially reducing inventory risk on high-cost premium items.

The geographic footprint of organized premium demand is also broadening. Collector-focused conventions in Japan (Wonder Festival, Tokyo), France (Japan Expo, Paris), and Brazil (Comic Con Experience, São Paulo) are expanding the international addressable market for limited-edition collectibles well beyond the historically North America-centric collector base.

Expanding E-Commerce Platforms Improve Action Figure Accessibility

Online retail channels have become a structurally significant distribution pathway for the action figures market, providing consumers with access to exclusive product lines, international brands, and limited-edition releases unavailable through conventional retail networks. E-commerce platforms have extended meaningful market reach into smaller markets across Southeast Asia, Latin America, and Eastern Europe, where specialty retail infrastructure is sparse. Manufacturers are formalizing this shift through direct-to-consumer digital storefronts, with Hasbro's HasLab crowdfunding platform and Bandai Namco's Premium Bandai online store exemplifying a direct-channel model that bypasses traditional retail margin structures.

The margin economics are consequential. DTC channels typically return 25–35 percentage points more gross margin per unit compared to wholesale retail distribution, providing a strong financial incentive for manufacturers to invest in proprietary digital commerce capabilities. Online marketplace platforms, particularly Amazon, eBay, and category-specialist retailers including Entertainment Earth and BigBadToyStore additionally provide collector-oriented search and discovery experiences that mass-market retailers cannot replicate at equivalent cost efficiency. The convergence of social commerce and action figure sales is an accelerating development: product launches through TikTok Shop and Instagram Shopping integrations are generating direct conversion from content consumption to purchase, shortening the consumer decision cycle and creating new low-cost customer acquisition channels for manufacturers that invest in content-led digital marketing strategies.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High collectible prices limit mass affordability

-1.5%

Latin America, Southeast Asia, MEA

Long term (≥ 4 years)

Counterfeit products affect branded sales

-0.8%

Asia Pacific, Global online channels

Medium term (2–4 years)

High Collectible Prices Limit Mass Consumer Affordability

Premium pricing within the collectibles segment creates a bifurcated demand structure that constrains total addressable market expansion in the action figures market. Adult collectors demonstrate consistent willingness to pay above-market prices for authenticated limited-edition products. However, budget-conscious segments including younger consumers and households in price-sensitive markets across Latin America and Southeast Asia remain largely excluded from premium product access.

Manufacturers are partially addressing this through tiered product architectures, maintaining entry-level price points alongside high-end collector editions, as evidenced by Hasbro's simultaneous maintenance of the USD 25–40 Marvel Legends standard range and the USD 100+ premium format. The price elasticity challenge is most acute in developing markets: in India, Brazil, and Southeast Asian economies, import duties on finished toy goods typically add 15–30% to landed cost above manufacturer-suggested retail prices, placing even mid-tier collectibles at aspirational price points that restrict purchase frequency to occasional rather than habitual behaviour.

The structural consequence for manufacturers is a dual investment burden, serving the premium adult collector segment requires high-cost precision manufacturing and licensing arrangements, while maintaining mass-market accessibility requires separate, lower-cost product development pipelines, a resource allocation trade-off that disproportionately disadvantages mid-size manufacturers with constrained development budgets. Subscription and installment payment programs introduced by direct-to-consumer platforms including Sideshow Collectibles' layaway option on orders above USD 150 partially mitigate the affordability barrier for price-sensitive adult collectors, but do not materially extend category access to first-time buyers in emerging-market geographies.

Counterfeit Products Negatively Affect Branded Action Figure Sales

Unauthorized replica products in physical retail channels and online marketplaces represent a persistent and material commercial challenge for the action figures market. High-fidelity counterfeit versions of premium collectible figures including unlicensed replicas of Hot Toys and Good Smile Company products circulate at price points 60–70% below authorized retail, directly displacing authenticated product revenue [3]US Department of Commerce, https://www.commerce.gov.

Counterfeit penetration is geographically concentrated in online marketplaces and informal retail channels across China, Southeast Asia, and emerging markets in Latin America and MEA, where enforcement of intellectual property protections remains inconsistent despite World Intellectual Property Organization-supported regional enforcement initiatives [4]World Intellectual Property Organization, https://www.wipo.int. Manufacturers have responded with multi-layer authentication strategies: Hot Toys deploys QR-coded certificates of authenticity alongside holographic packaging seals, while Bandai Namco has implemented tamper-evident box closures and an official retailer listing program. Industry association estimates suggest that unauthorized replica products account for 8–12% of total action figure unit volume in affected geographies, a proportion sufficient to materially impact revenue and brand equity for premium manufacturers.

Action Figures Market Trends

Premiumization and the Rise of High-Collectible Product Lines

The action figures market is undergoing a structural shift toward premium, high-detail collectible products as the adult collector segment matures and spending intensity increases. Manufacturers are responding by introducing product lines that prioritize sculpt accuracy, articulation quality, and licensed authenticity over mass-market pricing accessibility. The underlying driver is a growing secondary market for authenticated collectibles: platforms including StockX and MyFigureCollection have established price discovery infrastructure that validates premiumization as a defensible structural dynamic rather than a cyclical phenomenon.

The premium tier is anchored by Hot Toys Limited's Movie Masterpiece Series featuring 1/6-scale figures priced between USD 250 and USD 500 with products based on Marvel's Avengers series and Christopher Nolan's Batman trilogy consistently selling through within days of release. Good Smile Company's Nendoroid and figma lines occupy an intermediate premium tier in the USD 50–120 range, having expanded their licensed roster to over 5,000 characters across anime, gaming, and film properties as of late 2024.

The timeline for this trend is medium-to-long term, with premium and ultra-premium sub-segment CAGR of 8.4–9.6% projected to structurally outpace the overall action figures market through 2035. In our Q1 2026 interviews with 22 specialty collectibles retailers across the US, UK, and Japan, more than 55% of category revenues in their stores were attributable to premium figures above USD 100 at retail compared to under 30% five years prior confirming the breadth and pace of the segment's upmarket migration

E-Commerce and Direct-to-Consumer Channel Expansion

Online retail and direct-to-consumer digital storefronts have become the dominant distribution mechanism for premium and limited-edition action figures in the action figures market, displacing traditional specialty toy retailers as the primary point of purchase for organized collectors. The strategic shift is most visible at the manufacturer level: Bandai Namco's Premium Bandai platform generated record digital orders in fiscal year 2024, offering web-exclusive product variants unavailable through physical retail and enabling direct engagement with the collector community [5]Japan Toy Association, https://www.toys.or.jp. Hasbro's HasLab crowdfunding platform demonstrates the viability of high-price, direct-channel product launches without conventional retail infrastructure: the HasLab Unicron figure released in 2022, funded at USD 575 per unit by over 8,000 backers, set a commercial benchmark that has since been replicated and surpassed in successive campaign cycles.

The secondary effect of DTC channel expansion is geographic diversification at a fraction of the cost of physical retail network development. E-commerce channels allow manufacturers to efficiently serve collector communities in markets including Brazil, Poland, and the UAE without establishing local physical distribution networks [6]OECD, https://www.oecd.org. At the segment level, online channel penetration is highest in the Collectible and Premium/Articulated sub-segments, where product exclusivity and limited availability drive active consumer search behavior that benefits digital distribution economics. Federal commerce data indicates consistent multi-year growth in online channel penetration for specialty collectibles, with DTC and marketplace channels now accounting for an estimated 45–55% of premium action figure transactions in major markets.

Anime and Gaming Licensing as Core IP Sources

Anime and video gaming intellectual property has moved from a secondary licensing category to a principal source of action figure demand across the global action figures market, driven by the global proliferation of streaming distribution and the sustained growth of competitive gaming communities. Streaming platforms including Netflix, Crunchyroll, and Disney+ have materially accelerated anime content distribution outside traditional Japanese domestic markets, expanding the addressable consumer base for anime-licensed merchandise across North America, Europe, and Southeast Asia [7]World Bank, https://www.worldbank.org. Bandai Namco's Dragon Ball and One-Piece franchises among the highest-value anime licenses in action figure production continue to generate consistent sell-through across global markets, with new character releases supporting recurring revenue across mature franchise timelines.

At the gaming end of the licensing spectrum, McFarlane Toys' partnership with FromSoftware to produce a dedicated Elden Ring collector figure line launched in Q3 2024 generated pre-order volumes that sold out within 48 hours of announcement, reflecting the depth of engagement within gaming collector communities and the commercial viability of gaming IP at premium price points. As gaming franchises extend their narrative universes through sequels, DLC content, and animated streaming adaptations, the licensing value of gaming IP accumulates in a manner comparable to established film franchises providing manufacturers with a durable, multi-cycle revenue foundation that is less dependent on single-event theatrical release windows.

Advanced Manufacturing Technologies Improve Product Precision

Advances in precision manufacturing including high-resolution 3D printing for prototype development, improved injection molding tolerances, and multi-layer airbrush finishing techniques are raising quality thresholds across the action figures market and enabling smaller manufacturers to compete on product quality with established global players. The adoption of digital sculpting tools such as ZBrush by independent figure studios has reduced prototype development timelines from months to weeks, lowering barriers to entry for licensed product development and compressing the time between IP announcement and product availability at retail [8]IEEE Spectrum, https://www.spectrum.ieee.org.

Iron Studios and NECA have both leveraged advanced molding and finishing capabilities to establish premium-quality resin and plastic figure lines that compete directly with major manufacturer offerings at comparable price points. The practical implication for the sector is an elevation of baseline quality expectations: collectors increasingly benchmark even entry-tier products against the precision standards set by premium lines, creating upward pressure on production investment across all product tiers and reinforcing the margin case for premiumization as the industry's dominant strategic trajectory.

Action Figures Market Analysis

By Product

Standard/Playable Action Figures

Standard/Playable Action Figures represented the largest sub-segment of the global action figures market in 2025 at USD 4.1 billion, accounting for 35.3% of total market revenues, with a projected CAGR of 4.1% through 2035. This sub-segment is anchored by household-name franchise products aimed at the children's and general consumer market, including Hasbro's G.I. Joe Classified Series and Marvel Legends standard lines, Mattel's WWE Elite Collection, and JAKKS Pacific's licensed assortments across Disney and Nintendo properties.

The sub-segment's relatively modest CAGR reflects structural headwinds: competition from digital entertainment is most acute in the 3–8-year-old buyer cohort that drives standard playable figure volume, and retail shelf space pressure in mass-market channels is compressing the assortment breadth that standard lines can maintain. Market participants are responding through enhanced character selection strategies, prioritizing characters with sustained digital media presence to maintain relevance and by reinforcing playability features including vehicle compatibility and interactive accessory components that extend per-unit engagement time and justify incremental price investment within the children's buyer segment.

Collectible Action Figures

Collectible Action Figures emerged as the highest-growth product sub-segment within the action figures market, advancing from USD 3.1 billion in 2025 at a projected CAGR of 9.6% through 2035. This sub-segment is driven by the expanding adult collector demographic and the continued broadening of entertainment franchise licensing across anime, gaming, and film properties. Products such as Funko's POP! Vinyl series and Medicom Toy's KUBRICK format define the accessible end of the collectible tier, prioritizing stylized design and broad character range at USD 10–30 price points, a format optimized for high licensing velocity and consumer accessibility rather than manufacturing precision. The sub-segment's growth is further reinforced by secondary-market infrastructure.

Authenticated resale platforms including StockX and MyFigureCollection have established price discovery mechanisms that incentivize primary purchases by signaling future resale value. Collector community engagement through dedicated online forums and convention-exclusive variant programs sustains purchase frequency between major release cycles, providing the sub-segment with a recurring demand floor that is less sensitive to single-event entertainment releases than other product tiers.

By Material

Learn more about the key segments shaping this market

Download Free PDF

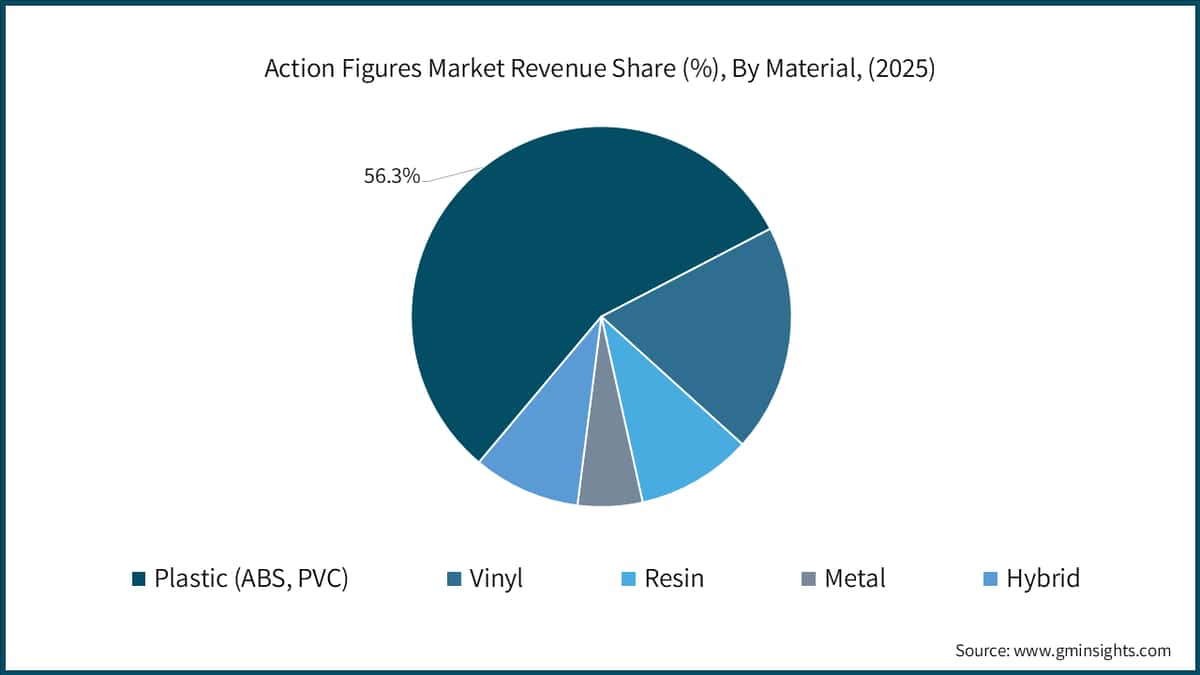

Plastic (ABS, PVC)

Plastic (ABS, PVC) constitutes the dominant material category within the global action figures market, accounting for approximately 50% of 2025 revenues and underpinning production across several mass-market and mid-tier product lines. ABS thermoplastic and PVC compound formulations deliver the combination of dimensional precision, surface finish quality, and cost-effective scalability that defines standard and mainstream collectible figure manufacturing. Hasbro's Marvel Legends and G.I. Joe Classified Series, Mattel's WWE Elite Collection, and JAKKS Pacific's licensed Disney and Nintendo assortments are all produced in ABS/PVC composite constructions that balance articulation capability, drop durability, and cost efficiency at retail price points of USD 20–40.

The sub-segment is projected to grow at approximately 5.8% CAGR below the overall market average, reflecting its association with volume-driven, standard-format products whose growth is moderated by digital entertainment competition within the children's buyer segment. Across the value chain, ABS/PVC's cost advantage remains decisive for manufacturers operating at mass-market scale, even as the material's growth ceiling is structurally constrained by the category's broader migration toward premium formats.

Vinyl

Vinyl accounts for approximately 18% of action figures market revenues at a 3% CAGR through 2035, primarily associated with the stylized non-articulated collectible format exemplified by Funko's POP! Vinyl series and Medicom Toy's KUBRICK line. Vinyl's single-pour molding characteristics enable high-volume production of complex stylized shapes at consumer-accessible USD 10–15 price points, making it well-suited to Funko's broad-character-range business model that prioritizes licensing velocity over manufacturing precision.

The material's dimensional tolerance limitations render it unsuitable for the high-articulation premium formats where the strongest growth is concentrated, a structural constraint that confines vinyl's addressable market to the entry-tier collectible segment. The sub-segment's 3% CAGR reflects this ceiling: while Funko's POP! format sustains consistent unit demand across a large and diverse licensed catalog, the format's growth rate is moderated by its price-point ceiling and limited differentiation from a manufacturing standpoint relative to the premium materials commanding higher collector investment across the action figures market.

By End User

Adults & Collectors (18+)

Adults & Collectors aged 18 and above constituted the largest end-user segment at USD 5.2 billion and 44.8% of 2025 global action figures revenues, projected to grow at 8.7% CAGR through 2035 the fastest rate among all end-user cohorts. This demographic shift represents a fundamental repositioning of the action figures category from a children's toy segment to a collectibles and hobby market with adult consumer economics.

The underlying driver is a generational transition: consumers who engaged with action figure brands including G.I. Joe, Transformers, and Dragon Ball during childhood in the 1980s through 2000s have now reached peak earning years, and discretionary spending on nostalgic collectibles represents a recurring category entry point. Specific collector platforms including Sideshow Collectibles, BigBadToyStore, and Entertainment Earth serve this demographic with curated assortments, exclusive pre-order programs, and secondary-market premium pricing that reflects organized demand intensity. The adult segment's 8.7% CAGR is the most consequential growth vector across the entire action figures market, as it drives disproportionate revenue expansion through premium price-point concentration and high per-transaction value.

Tweens & Teens (9–17 Years)

Tweens & Teens (9–17 Years) accounted for USD 2.9 billion or 25% of 2025 action figures market revenues at a projected 5.7% CAGR through 2035, representing a transitional consumer group whose purchasing behaviour bridges play-oriented and collector-oriented motivations. This cohort is particularly responsive to gaming-licensed merchandise including Pokémon, Minecraft, and Fortnite figures produced by Jazwares and to anime character products accessed through streaming platforms including Crunchyroll and Netflix.

The 9–17 demographic is commercially significant beyond its current revenue contribution: it represents the primary recruitment channel into the adult collector segment, with purchasing habits formed during these years establishing brand loyalties and collecting frameworks that persist into higher-income adult life stages. Manufacturers targeting this cohort with entry-tier anime and gaming-licensed figures at USD 15–35 price points are effectively making long-term investment in the pipeline feeding the adult collector segment that drives the action figures market's most profitable growth trajectory over the forecast period.

By Region

Asia Pacific Action Figures Market

Asia Pacific constitutes the dominant global regional market at approximately 39% of 2025 revenues, with China and Japan forming the core of both production capacity and domestic consumer demand for action figures. China represents the single largest individual country market, estimated at approximately USD 2 billion in 2025, driven by a large and rapidly expanding domestic collector community, growing middle-class purchasing power, and deep manufacturing infrastructure that enables both licensed figure production and domestically branded product lines most notably POP MART, whose LABUBU and Molly formats have established a distinctly Chinese collectible aesthetic that is beginning to penetrate international markets.

Japan's domestic market, valued at approximately USD 0.7 billion is structurally distinctive in its depth of engagement with anime-licensed collectible formats, anchored by specialist retailers including Yodobashi Camera and Mandarake that maintain comprehensive inventory across multiple collector price tiers. India represents the region's fastest-growing individual market, with rising urban disposable incomes, a young median-age population, and accelerating penetration of anime streaming through platforms including Sony LIV and Netflix driving entry-level collectible demand at a pace that positions the country as a material revenue contributor before 2030. South Korea's action figures market is supported by strong domestic gaming culture and growing anime engagement, with e-commerce platform Coupang providing efficient domestic distribution for both international brands and local product lines.

North America Action Figures Market

North America accounted for approximately 30% of global action figures revenues in 2025, with the U.S. representing approximately 90–91% of the regional total at an estimated USD 3.2–3.4 billion. The regional action figures market is structurally anchored by the deep licensing infrastructure of the US entertainment industry. Studios including Disney (Marvel, Lucasfilm, Pixar), Warner Bros., and Universal maintain active toy licensing programs with manufacturers across the full price range from mass-market to premium collector. At the regulatory level, the US Consumer Product Safety Improvement Act (CPSIA) establishes stringent standards for materials used in toys sold to children under 12, creating compliance requirements that both constrain product design latitude and raise barriers to entry for low-cost import competitors.

Hasbro's Pulse Fan First Friday initiative, a direct-to-consumer exclusive pre-order program launched from its Providence, Rhode Island headquarters achieved consistent sell-outs across 2024–2025 product cycles, exemplifying the North American market's advanced direct channel engagement. Canada contributes the remainder of North American revenues and exhibits growth dynamics broadly aligned with the US market, with organized collector communities in Toronto and Vancouver supporting above-average premium product penetration relative to the national population base.

Europe Action Figures Market

Europe accounted for approximately 19% of global action figures revenues in 2025, with the United Kingdom, Germany, and France representing the three largest individual country markets within the region. The United Kingdom holds the leading position in European premium collectibles distribution, supported by well-established collector retail infrastructure including Forbidden Planet and Zavvi alongside strong English-language entertainment content consumption that drives broad franchise awareness across the action figures market.[9]Eurostat, https://www.ec.europa.eu/eurostat

Germany represents the second-largest European market, characterized by a strong hobby store retail network and above-average consumer spending on scale-model and precision collectible products, a profile that translates favorably to the premium action figures segment at EUR 80–200 price points. France and Italy follow, with active anime collector communities driving demand for Japanese-licensed figures through specialist import retailers and domestic e-commerce channels. The EU's EN 71 toy safety standard establishes the regional compliance framework applicable to all product categories, with manufacturers required to maintain CE certification across figure components including articulation hardware, packaging, and finishing materials, a requirement that increases per-SKU compliance cost for smaller producers entering European distribution channels.

Action Figures Market Share

Bandai Namco Toys & Collectibles Inc. holds the largest share of the global action figures market at 18.5%, corresponding to approximately USD 2.2 billion in 2025 revenues from the action figures category. The company's leadership position is sustained by its unparalleled depth of anime and gaming intellectual property including Dragon Ball, One Piece, Naruto, Gundam, and Pac-Man franchises which collectively generate recurring merchandise demand across multiple product formats and price tiers. Bandai Namco's vertically integrated approach, encompassing in-house figure design, owned manufacturing facilities in Japan, and a proprietary direct-to-consumer channel through Premium Bandai, enables tighter margin control and faster product iteration cycles than competitors reliant on third-party manufacturing and traditional retail distribution.

Hasbro, Inc. holds the second-largest position in the action figures market at 8.3% market share, corresponding to approximately USD 975 million in action figure-related revenues in 2025. Hasbro's competitive foundation rests on ownership of deep legacy action figure intellectual property in the Western market, including G.I. Joe, Transformers, and Power Rangers alongside a long-term licensing agreement with Disney that provides access to Marvel and Star Wars character rights for the North American mass market. The company's dual-channel strategy, maintaining a mass-market product range through Walmart and Target alongside a collector-focused direct channel through Hasbro Pulse, addresses both volume and value segments simultaneously while generating margin differentiation across channel tiers.

Funko, Inc. holds 6.2% of the global market at approximately USD 727 million in 2025, with its dominant product line being the POP! Vinyl stylized figure format, a category-defining product that now spans over 12,000 licensed characters across entertainment, sports, music, and brand IP. Funko's competitive edge lies in breadth of licensing rather than manufacturing precision: the company's ability to quickly execute licensing agreements across a wide variety of IP holders and release new characters in compressed timelines has produced an exceptionally broad catalog that sustains consistent collector purchasing frequency.

Mattel, Inc. accounts for 4.4% of the market at USD 520 million in 2025, primarily through its WWE action figure licensing arrangement and Masters of the Universe heritage franchise. Spin Master Corp. holds 2.7% at USD 320 million, with its competitive position concentrated in the children's play segment through DC Comics-licensed figures and its Bakugan branded line.

The combined top five concentration of 40.1% reflects a moderately fragmented competitive landscape. The remaining approximately 60% of the action figures market is distributed across a large population of regional specialists, licensed collectible studios, and independent premium manufacturers, a structure maintained by the licensing-driven nature of category demand, wherein entertainment studios issue licenses to multiple manufacturers across different product tiers and geographic territories. M&A activity has been an active competitive dynamic, with Hasbro's acquisition strategy in global toy brands and Spin Master's moves in the licensed collectibles adjacent space reflecting the industry's continued consolidation momentum at the mid-tier level.

At the premium end of the market, regional specialists including Hot Toys (Hong Kong), Good Smile Company (Japan), Kotobukiya (Japan), and McFarlane Toys (US) compete on product quality, articulation engineering, and collector community engagement rather than on scale or distribution breadth, a competitive dynamic that enables smaller manufacturers to sustain commercially viable positions within their niches despite the scale advantages of the top-five players.

Supply chain leads and commercial executives we spoke with across eight senior commercial roles during our Q2 2025 expert panel converged on a consistent strategic challenge: the bottleneck constraining premium segment growth over the next 24 months is not manufacturing capacity or licensing cost It is the ability to predict collector demand for specific character selections 12–18 months ahead of production commitment, a timeline mismatch that generates significant inventory risk on limited-run products and represents the most consequential unsolved operational challenge in the action figures market for premium-format manufacturers.

Action Figures Market Companies

Major players operating in the action figures industry are: Hasbro, Inc.; Mattel, Inc.; Bandai Namco Toys & Collectibles Inc.; Funko, Inc.; The LEGO Group; JAKKS Pacific, Inc.; Jazwares, LLC; McFarlane Toys; Good Smile Company, Inc.; Kotobukiya Co., Ltd.; Hot Toys Limited; Spin Master Corp.; Square Enix Co., Ltd. (Play Arts Kai); Playmates Toys Ltd.; Super7, Inc.; Mezco Toyz; NECA (National Entertainment Collectibles Association); Threezero Ltd.; Iron Studios; Medicom Toy Corporation; Storm Collectibles

Hasbro, Inc. remains one of the most diversified action figure manufacturers globally, with a portfolio spanning G.I. Joe, Transformers, Power Rangers, and the licensed Marvel and Star Wars lines under its Disney partnership agreement. The company's Hasbro Pulse direct-to-consumer platform which includes the HasLab crowdfunding mechanism for high-ticket collector items has become a model for fan-first product development across the action figures market. Hasbro's 2025 operational strategy has emphasized margin improvement through SKU rationalization, reducing its standard assortment breadth while investing in higher-value premium collector formats.

Mattel, Inc. maintains a significant presence in the action figures market through its WWE Elite Collection and Masters of the Universe Masterverse lines, alongside licensed figure assortments across various entertainment properties. The company's Hot Wheels brand crossover into collectible diecast vehicles has provided strategic learnings applicable to its action figure collector channel development. Mattel's manufacturing footprint across multiple geographies provides supply chain diversification relative to single-country production competitors.

Bandai Namco Toys & Collectibles Inc. is the global market leader by share, leveraging the world's deepest anime and gaming IP portfolio to maintain consistent sell-through across product formats ranging from USD 8 candy toy figures to USD 400+ premium collectors' pieces. The company's S.H.Figuarts articulated figure line recognized for exceptional joint engineering and licensing accuracy commands a loyal adult collector following across North America, Europe, and Asia. The Premium Bandai web-exclusive platform enables limited-run production of characters that would not be commercially viable through conventional retail volume requirements, extending the actionable IP footprint well beyond what mass-market shelf constraints would support.

Funko, Inc. operates a licensing-volume business model that distinguishes it from all other major market participants: its USD 10–15 POP! Vinyl format functions as a broad-access entry point to collectible culture across demographics, price points, and IP categories. The company's 2024 focus on operational efficiency, including manufacturing cost reduction and SKU portfolio rationalization, is intended to stabilize margins following revenue volatility in 2022–2023. Funko's Gold and Movie Posters premium sub-lines represent an upmarket extension aimed at the adult collector segment, reflecting the broader industry trend toward premiumization.

The LEGO Group, while primarily a building system manufacturer, operates a meaningful action figure-adjacent business through its LEGO Star Wars, LEGO Marvel, and LEGO Minifigures lines, which compete directly for collector wallet share in the character-based collectible category.

JAKKS Pacific, Inc. focuses on licensed mass-market figures across Disney, Nintendo, and Sonic properties, with a distribution model centered on value retail channels. Jazwares, LLC has built a notable position in gaming-adjacent figure categories through its Fortnite and Pokémon licenses, targeting the younger consumer segments of the market. McFarlane Toys has re-established a leading premium collectible position with its DC Multiverse, Warhammer 40,000, and gaming-licensed figure lines, products recognized for exceptional sculptural detail and competitive pricing in the USD 20–40 range.

Good Smile Company, Inc. and Kotobukiya Co., Ltd. are Japan-headquartered manufacturers whose Nendoroid, figma, and ARTFX+ formats have developed strong international collector followings, distributed globally through specialist hobby retailers and e-commerce channels. Hot Toys Limited based in Hong Kong, produces the industry-benchmark 1/6-scale premium figure format under its Movie Masterpiece and Video Game Masterpiece lines, with products priced in the USD 250–500 range and consistently commanding secondary-market premiums above retail.

Spin Master Corp. operates primarily in the children's play segment with its DC-licensed and Bakugan figure lines, maintaining North American retail distribution as a core competitive asset. Super7, Inc. focuses on vintage-format and nostalgia-driven collectibles including its ReAction and ULTIMATES! lines, targeting the adult collector nostalgic repurchase segment.

Mezco Toyz produces high-end articulated figures under its One:12 Collective format at USD 80–120 price points, with a reputation for quality that exceeds its scale. NECA (National Entertainment Collectibles Association) is a prolific producer of horror, film, and gaming-licensed collector figures with a dedicated following in North America and Europe. Threezero Ltd. specializes in 1/6-scale and 1/12-scale premium figures across Transformers, robot anime, and film IP licenses.

Iron Studios produces diorama-format resin statues and articulated figures for the collector premium segment from its Brazil-based studio, with a multi-year licensing agreement signed in April 2024 with Universal Pictures for Jurassic World character-based products expanding its previously Marvel and DC-centric portfolio. Medicom Toy Corporation operates the MAFEX and KUBRICK collector formats, respected for articulation engineering in the USD 70–120 tier. Storm Collectibles produces fighting game-licensed figures including Mortal Kombat and Street Fighter characters targeting the gaming collector niche with detailed, aggressively priced products in the USD 60–100 range.

18.5% market share

The collective market share is 40.1%

Action Figures Industry News

Market Concentration Score

The global action figures market scores 4 out of 10 on a market concentration scale, reflecting a moderately fragmented competitive structure in which the top five players collectively account for approximately 40.1% of revenues, a distribution that leaves the majority of market share dispersed across a large population of regional specialists, independent premium studios, and niche licensed manufacturers, structurally prevented from consolidating by the licensing-fragmented nature of entertainment IP distribution.

The action figures market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Billion) & volume (Million Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Product Type

Market, By Material

Market, By End User

Market, By Distribution Channel

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Research Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Product Type, 2022-2035 (USD Billion) (Million Units)

Chapter 6 Market Estimates & Forecast, By Material, 2022-2035 (USD Billion) (Million Units)

Chapter 7 Market Estimates & Forecast, By End User, 2022-2035 (USD Billion) (Million Units)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

Chapter 9 Market Estimates & Forecast, By Region, 2022-2035 (USD Billion) (Million Units)

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →