Market Size - By Product (Guidewires, Drainage Tubes, Nephrostomy Catheters, Sheath Dilators, Other Products), By Application (Kidney Stones, Urinary Tract Infections, Bladder Cancer, Other Applications), By Patient Type (Adult, Pediatric), and By End Use (Hospitals, Clinics, Ambulatory Surgical Centers, Other End Users), Growth Forecast. The market forecasts are provided in terms of revenue (USD Million) & volume (Units).

Report ID: GMI4325

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Nephrostomy Devices Market Size

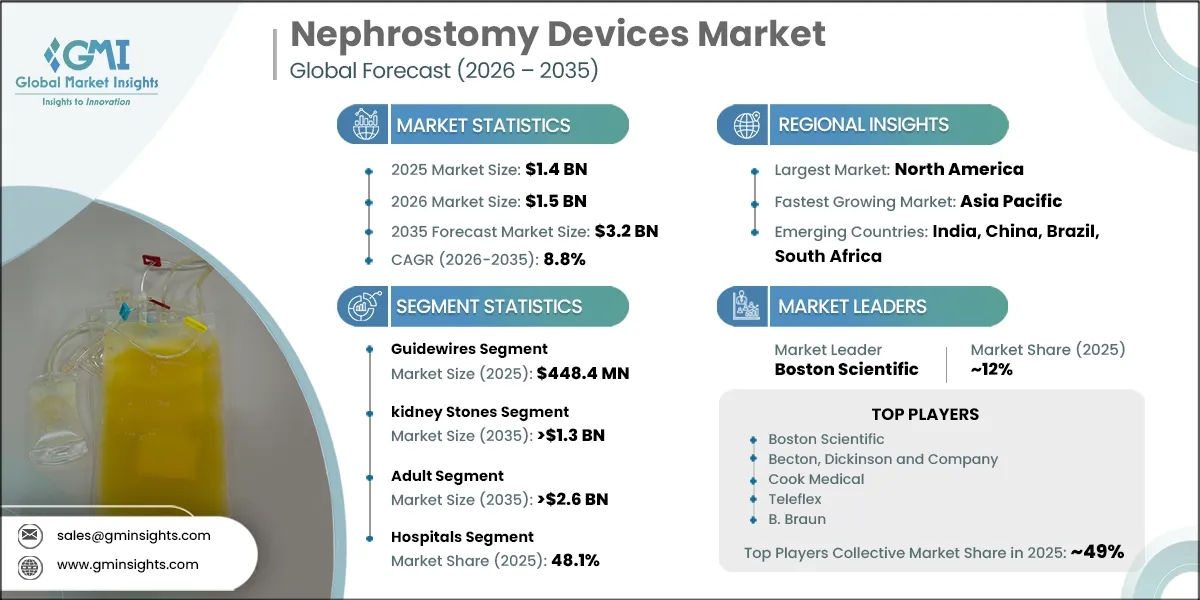

The global nephrostomy devices market was valued at USD 1.4 billion in 2025 and is expected to reach from USD 1.5 billion in 2026 to USD 3.2 billion by 2035, growing at a CAGR of 8.8%, according to the latest report published by Global Market Insights Inc.

The market growth is attributed to the rising prevalence of kidney-related disorders such as kidney stones, hydronephrosis, and urinary tract infections. Also, increasing adoption of minimally invasive procedures and advancements in nephrostomy technologies are further fueling market expansion.

Nephrostomy devices are medical instruments used to drain urine from the kidneys when the normal flow of urine is obstructed due to conditions like kidney stones, tumors, or bladder obstructions. These devices typically consist of a catheter inserted through the skin into the renal pelvis to bypass the urinary tract blockage and allow for the safe drainage of urine. Nephrostomy devices are commonly used in cases of hydronephrosis or when a percutaneous nephrostomy procedure is required.

The major players in the global nephrostomy devices market are Cook Medical, Boston Scientific, Becton, Dickinson and Company, Teleflex, and B. Braun. These companies maintain their competitive position through ongoing product innovation, global market presence, and substantial investment in research and development.

The market has increased from USD 1.1 billion in 2022 and reached USD 1.3 billion in 2024, with a historic growth rate of 8.3%. The growth of the market was driven by the expanding geriatric population, increasing volume of emergency urinary drainage procedures, improved access to interventional radiology services, and rising hospitalization rates for acute renal complications.

Kidney stones affect approximately 10% of men and 7% of women worldwide, with recurrence rates reaching up to 50% within 10 years. Conditions such as hydronephrosis, resulting from urinary tract obstructions, often require nephrostomy to relieve renal pressure and prevent long-term damage.

Furthermore, innovations in device design, including flexible guidewires with hydrophilic coatings and balloon catheters with enhanced inflation control, have improved procedural efficiency and patient safety. These advancements not only reduce complications but also enhance patient comfort during and after procedures. The growing preference for minimally invasive techniques is particularly evident in advanced healthcare regions such as North America and Europe, where outpatient nephrostomy procedures are increasingly adopted.

Nephrostomy Devices Market Trends

The growing preference for minimally invasive nephrostomy procedures is transforming urological care pathways by improving clinical outcomes while reducing hospital stays and procedure-related complications. Percutaneous nephrostomy, supported by real-time imaging guidance, is increasingly replacing open surgical approaches, particularly for patients with urinary obstructions, kidney stones, and impaired renal function.

In parallel, manufacturers are advancing nephrostomy device design through the use of biocompatible polymers, hydrophilic coatings, and enhanced catheter flexibility. These material innovations improve patient comfort during long-term catheterization and reduce infection risks by limiting biofilm formation and tissue irritation, thereby strengthening procedural safety and post-operative outcomes.

Additionally, the market is witnessing increased specialization, with a growing focus on pediatric-specific innovations. Miniaturized catheters, softer materials, and size-appropriate PCN kits are being developed to address pediatric anatomical and clinical needs, creating a distinct niche segment within the broader market.

Nephrostomy Devices Market Analysis

Based on product, the market is segmented as guidewires, drainage tubes, nephrostomy catheters, sheath dilators, and other products. The guidewires segment generated revenue of USD 448.4 million in 2025.

Guidewires dominate the nephrostomy devices market due to their pivotal role in facilitating safe and accurate catheter placement. Their flexibility, ease of navigation, and compatibility with various nephrostomy catheters make them indispensable during procedures.

Recent advancements, such as hydrophilic coatings, have enhanced their maneuverability, reducing procedural complications.

Additionally, the increasing focus on precision and patient safety has led to the development of specialized guidewires for pediatric and geriatric patients.

Their high demand across hospitals and ambulatory surgical centers is attributed to their versatility in treating diverse urological conditions, including kidney stones and urinary obstructions.

The drainage tubes segment accounted for significant revenue in 2025 and is anticipated to grow at a CAGR of 9% over the forecast period, driven by their widespread use in both acute and long‑term urinary drainage, high adoption across hospitals and interventional radiology settings, and continuous design improvements that enhance flow efficiency, durability, and patient comfort.

The nephrostomy catheters segment held a revenue of USD 281.3 million in 2025, with projections indicating a steady expansion at a CAGR of 9.5% from 2026 to 2035, supported by their critical role in percutaneous renal drainage, increasing adoption in minimally invasive urological and oncology procedures, and ongoing design advancements focused on improved retention, biocompatibility, and long‑term patient comfort.

The sheath dilators segment accounted for significant revenue in 2025 and is anticipated to grow at a CAGR of 8.3% over the forecast period, driven by their essential role in facilitating safe and precise tract dilation during percutaneous nephrostomy procedures, increasing procedural volumes, and rising adoption of minimally invasive, image‑guided renal access techniques.

Based on application, the market is segmented as kidney stones, urinary tract infections, bladder cancer, and other applications. The kidney stones segment is expected to drive business growth reach over USD 1.3 billion by 2035.

The kidney stones segment accounts for a significant share of the nephrostomy devices market, driven by the rising prevalence of nephrolithiasis globally. Kidney stones often cause severe urinary blockages, necessitating nephrostomy procedures for effective drainage.

The increasing incidence of sedentary lifestyles, poor dietary habits, and dehydration are further contributing to the growing burden of kidney stones, thereby fueling product demand.

In addition, advancements in imaging techniques and minimally invasive procedures have increased the success rates of nephrostomy for kidney stone management. Hospitals and clinics rely heavily on these devices for efficient treatment, ensuring their dominance in the application segment.

The urinary tract infections segment held a revenue of USD 423.6 million in 2025, with projections indicating a steady expansion at a CAGR of 9% from 2026 to 2035, driven by the high incidence of infection‑related urinary obstructions, increasing use of nephrostomy devices for emergency and long‑term drainage, and growing emphasis on timely intervention to prevent renal complications and sepsis.

The bladder cancer segment accounted for significant revenue in 2025 and is anticipated to grow at a CAGR of 8.7% over the forecast period, driven by the increasing incidence of bladder cancer–related urinary obstructions, frequent need for nephrostomy procedures to manage malignancy‑associated hydronephrosis, and growing reliance on minimally invasive drainage solutions in oncology care pathways.

Based on patient type, the nephrostomy devices market is segmented as adult and pediatric. The adult segment is expected to drive business growth and expand, reaching over USD 2.6 billion by 2035.

The adult segment dominates the market, primarily due to the higher prevalence of kidney‑related disorders among the adult population. Adults are more susceptible to conditions such as kidney stones, hydronephrosis, urinary tract obstructions, and bladder or prostate cancers, often driven by lifestyle factors, occupational exposure, dietary habits, and the presence of comorbidities such as diabetes and hypertension. These conditions frequently necessitate percutaneous nephrostomy for urinary diversion or renal decompression, thereby sustaining strong demand for nephrostomy devices.

In addition, the ageing adult population, particularly across developed regions, contributes significantly to procedure volume, as older adults face a higher risk of urological complications requiring repeated or long‑term nephrostomy interventions. This demographic trend further reinforces the dominance of the adult segment within the overall market.

Moreover, increasing awareness regarding urological health, combined with improved access to advanced diagnostic imaging and minimally invasive treatment options, has encouraged adults to seek earlier medical intervention. Early diagnosis and proactive management of urinary obstructions often lead to higher utilization of nephrostomy devices in both emergency and elective clinical settings.

The pediatric segment accounted for significant revenue in 2025 and is anticipated to grow at a CAGR of 8.3% over the forecast period, driven by the rising incidence of congenital urological abnormalities, growing use of nephrostomy devices in pediatric oncology and infection‑related obstructions, and increasing availability of pediatric‑specific catheter designs focused on safety, anatomical suitability, and long‑term patient comfort.

Based on end use, the market is segmented as hospitals, clinics, ambulatory surgical centers, and other end users. The hospitals segment dominated the market with a revenue share of 48.1% in 2025.

Hospitals dominate the end use segment of the market, owing to their ability to handle complex procedures and provide specialized care. Hospitals are equipped with advanced imaging technologies and skilled professionals, ensuring the success of nephrostomy procedures. Their capacity to manage high patient volumes further reinforces their position as key end-users.

Additionally, the availability of reimbursement policies for hospital-based nephrostomy treatments in many regions has bolstered the adoption of these devices. The preference for hospital settings for critical urological interventions ensures their continued dominance in the market.

The clinics segment accounted for significant revenue in 2025 and is anticipated to grow at a CAGR of 9.3% over the forecast period, driven by increasing patient preference for outpatient urological care, improved access to diagnostic and interventional services at specialty clinics, and wider adoption of nephrostomy procedures for infection‑ and obstruction‑related conditions in non‑hospital settings.

The ambulatory surgical centers segment accounted for significant revenue in 2025 and is anticipated to grow at a CAGR of 8.5% over the forecast period, driven by the growing shift toward outpatient and minimally invasive urological procedures, shorter recovery times, lower procedural costs compared to hospitals.

North America Nephrostomy Devices Market

North America accounted for the largest share of the market in 2025, supported by well‑established healthcare infrastructure, high procedure volumes in urology and interventional radiology, and widespread adoption of minimally invasive treatments for urinary tract obstructions and renal disorders.

The region benefits from a high prevalence of kidney‑related conditions, which continues to drive procedure demand. In Canada alone, approximately 1 in 10 individuals is expected to develop a kidney stone during their lifetime, underscoring the substantial burden of urolithiasis across the region. Similar trends are observed in the U.S., where lifestyle factors, dietary habits, and an ageing population contribute to rising incidences of kidney stones, hydronephrosis, and malignancy‑related urinary obstructions.

The U.S. nephrostomy devices market was valued at USD 414.4 million and USD 445.1 million in 2022 and 2023, respectively. The market size reached USD 491.1 million in 2025, growing from USD 479.9 million in 2024, and is anticipated to grow at a CAGR of 8.2% from 2026 to 2035.

A key factor supporting the U.S. market’s dominance is the high burden of renal diseases, particularly kidney stones and chronic kidney disease. According to the Centers for Disease Control and Prevention, approximately 15% of U.S. adults are affected by chronic kidney disease, many of whom require advanced urinary drainage or renal decompression interventions. This high disease prevalence drives sustained demand for nephrostomy devices across hospitals and specialty clinics.

With continued investment in advanced device technologies, expansion of outpatient care models, and increasing awareness of early urological intervention, North America is expected to maintain its leading position in the market throughout the forecast period.

Europe Nephrostomy Devices Market

Europe market accounted for USD 401.2 million in 2025 and is anticipated to show lucrative growth over the forecast period.

Europe held a strong and well-established position in the nephrostomy devices industry in 2025, supported by its mature healthcare infrastructure, extensive hospital networks, and widespread availability of urology and interventional radiology services.

The region benefits from high procedural standards and strong adoption of minimally invasive urological interventions across both public and private healthcare systems.

European healthcare systems emphasize early diagnosis, structured disease management, and standardized clinical pathways, particularly for kidney stones, urinary obstructions, and malignancy-related renal complications. These practices support the routine use of nephrostomy devices in both emergency decompression and planned urological procedures.

With continued investment in hospital modernization, increased adoption of minimally invasive techniques, and cross-border healthcare initiatives, Europe is expected to maintain a stable and significant position in the market throughout the forecast period.

Asia Pacific Nephrostomy Devices Market

The Asia Pacific region is projected to show lucrative growth during the forecast period.

Asia Pacific is rapidly emerging as one of the fastest‑growing regions in the nephrostomy devices industry, driven by its large population base, rising incidence of kidney stones and urinary tract obstructions, and expanding access to urology and interventional radiology services across both developed and emerging economies.

The region encompasses mature healthcare markets such as Japan, South Korea, Australia, and China, where advanced imaging infrastructure and minimally invasive urological procedures are routinely adopted, alongside high‑growth countries including India, and Southeast Asia, which are actively strengthening hospital capacity and procedural capabilities.

The clinical burden of kidney‑related disorders, including urolithiasis, hydronephrosis, infection‑related obstructions, and malignancy‑associated urinary complications, remains substantial across Asia Pacific. Rising prevalence of lifestyle‑related risk factors, ageing populations, and increasing diagnostic awareness are collectively driving higher demand for nephrostomy interventions.

Latin America Nephrostomy Devices Market

Brazil is experiencing significant growth in the nephrostomy devices industry.

Brazil represents one of the most important and rapidly expanding nephrostomy devices markets in Latin America, driven by its large population base, rising incidence of kidney stones and urinary tract obstructions, and increasing demand for minimally invasive urological interventions across both public and private healthcare systems.

The country’s healthcare landscape is increasingly characterized by modernization of hospital infrastructure and broader availability of urology and interventional radiology services, particularly in urban and tertiary-care centers. This expansion is enabling wider adoption of image‑guided percutaneous nephrostomy procedures for both emergency and elective urological conditions.

As Brazil continues to adopt cost‑effective, minimally invasive treatment models for managing complex urological disorders and malignancy‑related urinary obstructions, nephrostomy devices are being increasingly utilized to reduce surgical risk, shorten hospitalization duration, and improve overall clinical outcomes. This aligns with national healthcare objectives focused on efficiency, patient safety, and optimized resource utilization.

Middle East and Africa Nephrostomy Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

Saudi Arabia is rapidly emerging as a key regional market for nephrostomy devices, driven by national efforts to strengthen healthcare infrastructure and expand access to advanced urological and interventional radiology services under the Vision 2030 framework. The country’s focus on reducing reliance on overseas medical treatment is accelerating the adoption of specialized minimally invasive procedures.

Strong government investment in healthcare modernization, hospital expansion, and advanced medical technologies is creating a favorable environment for the broader use of nephrostomy devices across tertiary hospitals and specialized care centers. These investments enhance diagnostic capabilities, procedural precision, and the availability of trained specialists required for nephrostomy interventions.

With sustained healthcare investment, expanding specialized care capacity, supportive policies under Vision 2030, and increasing awareness of early urological intervention, Saudi Arabia is well positioned to become an influential nephrostomy devices industry in the Middle East, reinforcing its role as a regional hub for advanced urological care over the forecast period.

Nephrostomy Devices Market Share

The global nephrostomy devices industry is characterized by moderate to strong competition among established medical device manufacturers and specialized urology players, driven by continuous product innovation, procedural advancements, and expanding adoption of minimally invasive urinary drainage techniques. Companies are focused on developing advanced nephrostomy catheters, percutaneous nephrostomy (PCN) sets, and drainage systems that enhance procedural accuracy, reduce infection risk, and improve long-term patient comfort.

Market participants compete through product differentiation, clinical performance, regulatory approvals, and expansion into high-growth emerging markets. Increasing emphasis on antimicrobial coatings, improved locking mechanisms, hydrophilic materials, and compatibility with advanced imaging technologies is intensifying competition. Strategic initiatives such as product launches, geographic expansion, and collaborations with hospitals and urology centers continue to shape market dynamics.

Key players include Boston Scientific, Becton, Dickinson and Company, Cook Medical, Teleflex, and B. Braun, collectively accounting for approximately ~49% of the total market share. As the global burden of kidney stones, urinary tract obstructions, and urological malignancies rises, competition in the market is expected to intensify. Manufacturers are likely to prioritize innovation, infection prevention, outpatient-friendly device designs, and strategic partnerships with healthcare providers.

Nephrostomy Devices Market Companies

Some of the prominent market participants operating in the nephrostomy devices industry include:

BD holds a strong position in the nephrostomy devices, particularly in nephrostomy balloon dilation catheters and access devices. The company’s emphasis on procedural reliability, imaging compatibility, and clinician‑validated designs supports safe and efficient percutaneous renal access, reinforcing its adoption across hospitals and interventional radiology settings globally.

Teleflex is a prominent player in the nephrostomy devices market which includes nephrostomy catheters, puncture sets, and exchange systems. The company differentiates itself through user‑friendly catheter designs, hydrophilic coatings, and solutions optimized for minimally invasive procedures.

B. Braun maintains a solid presence in the nephrostomy devices market through its structured approach to urological drainage systems and percutaneous access solutions. The company’s focus on high‑quality biomaterials, infection‑control technologies, and integrated procedural sets supports safe nephrostomy placement and long‑term drainage management.

Nephrostomy Devices Industry News:

In October 2025, TubeX launched Nephro-Safe, a nephrostomy tube stabilization solution designed to improve the safety and reliability of external drainage systems. The product integrated precision engineering with a focus on patient comfort and clinical efficiency. This development is expected to support the market by enhancing device stability and reducing dislodgement risks, improving patient outcomes, and strengthening innovation-driven competition in nephrostomy device design.

In March 2024, Calyxo, Inc. received FDA approval for its redesigned CVAC System, a next‑generation kidney stone removal platform designed to advance minimally invasive urological care. The updated system integrates ureteroscopy, laser lithotripsy, irrigation, and aspiration into a single procedural workflow, enabling more complete stone clearance during a single intervention. This regulatory milestone supported broader clinical adoption of aspiration‑assisted stone management techniques and contribute to market growth by promoting more efficient, patient‑centric, and minimally invasive kidney stone treatment solutions.

The nephrostomy devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2022 – 2035 for the following segments:

Market, By Product

Guidewires

Drainage tubes

Nephrostomy catheters

Sheath dilators

Other products

Market, By Application

Kidney stones

Urinary tract infections

Bladder cancer

Other applications

Market, By Patient Type

Adult

Pediatric

Market, By End Use

Hospitals

Clinics

Ambulatory surgical centers

Other end users

The above information is provided for the following regions and countries:

North America

U.S.

Canada

Europe

Germany

UK

France

Spain

Italy

Netherlands

Asia Pacific

China

Japan

India

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

Middle East and Africa

South Africa

Saudi Arabia

UAE

Authors: Monali Tayade, Jignesh Rawal

Nephrostomy Devices Market Scope

Nephrostomy Devices Market Size

Nephrostomy Devices Market Trends

Nephrostomy Devices Market Analysis

Nephrostomy Devices Market Share

Report Content

Chapter 1 Research Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.2.1.1 Source consistency protocol

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.5.1.1 Sources, by region

1.6 Base estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.7.1 Quantified market impact analysis

1.7.1.1 Mathematical impact of growth parameters on forecast

1.8 Research transparency addendum

1.8.1 Source attribution framework

1.8.2 Quality assurance metrics

1.8.3 Our commitment to trust

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Product trends

2.2.3 Application trends

2.2.4 Patient type trends

2.2.5 End use trends

2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising prevalence of kidney disorders

3.2.1.2 Increased adoption of minimally invasive surgical procedure

3.2.1.3 Technological advancements in nephrostomy devices

3.2.1.4 Increasing awareness among patients and healthcare professionals

3.2.2 Industry pitfalls and challenges

3.2.2.1 Risks associated with the nephrostomy devices

3.2.2.2 Availability of substitute procedures

3.2.3 Market opportunity

3.2.3.1 Development of infection-resistant and antimicrobial devices

3.3 Growth potential analysis

3.4 Regulatory landscape (Driven by Primary Research)

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Technological landscape (Driven by Primary Research)

3.5.1 Current technologies

3.5.1.1 Increased use of single use, sterile, pre configured nephrostomy kits

3.5.1.2 Expansion of nephrostomy use beyond acute care

3.5.2 Emerging technologies

3.5.2.1 Increasing focus on pediatric specific nephrostomy devices

3.5.2.2 Customized and 3D-printed devices for patient-specific anatomical needs

3.6 Future market trends (Driven by Primary Research)

3.7 Impact of AI and Generative AI on the market

3.8 Pricing analysis, 2025 (Driven by Primary Research)

3.9 Patent analysis

3.10 Porter’s analysis

3.11 PESTEL analysis

3.12 Investment landscape

3.13 Gap analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis (Driven by Primary Research)

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Merger and acquisition

4.6.2 Partnership and collaboration

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022-2035 ($ Mn)

5.1 Key trends

5.2 Guidewires

5.3 Drainage tubes

5.4 Nephrostomy catheters

5.5 Sheath dilators

5.6 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 ($ Mn)

6.1 Key trends

6.2 Kidney stones

6.3 Urinary tract infections

6.4 Bladder cancer

6.5 Other applications

Chapter 7 Market Estimates and Forecast, By Patient Type, 2022-2035 ($ Mn)

7.1 Key trends

7.2 Adult

7.3 Pediatric

Chapter 8 Market Estimates and Forecast, By End Use, 2022-2035 ($ Mn)

8.1 Key trends

8.2 Hospitals

8.3 Clinics

8.4 Ambulatory surgical centers

8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 ($ Mn)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 France

9.3.4 Spain

9.3.5 Italy

9.3.6 Netherlands

9.4 Asia Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 Australia

9.4.5 South Korea

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.6 Middle East and Africa

9.6.1 South Africa

9.6.2 Saudi Arabia

9.6.3 UAE

Chapter 10 Company Profiles

10.1 AngioDynamics

10.2 Argon Medical Devices

10.3 B. Braun

10.4 Becton, Dickinson and Company

10.5 Boston Scientific

10.6 Coloplast

10.7 Cook Medical

10.8 Galt Medical

10.9 Meditech Devices

10.10 Merit Medical

10.11 Nipro

10.12 Rocamed

10.13 Teleflex

10.14 Uresil

10.15 UROMED

10.16 Urovision-Urotech

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Regional or domestic-only leaders not in the global top tier

Distributors and channel partners who control market access

Emerging disruptors, startups, or adjacent-industry entrants

Niche players focused on a specific application or end-use

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Authors: Monali Tayade, Jignesh Rawal

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at[email protected]

Explore our licensing options:

Starting at: $2,450

Premium Report Details

Base Year: 2025

Companies Profiled: 17

Tables and Figures: 166

Countries covered: 19

Pages: 135

Download Free PDF

Premium Report Details

Base Year: 2025

Companies Profiled: 17

Tables and Figures: 166

Countries covered: 19

Pages: 135

Download Free PDF

Share Content

Add Citations

Monali Tayade. 2026, April. Nephrostomy Devices Market – By Product, By Application, By Patient Type, By End Use, Growth Forecast, 2026 to 2035 (Report ID: GMI4325). Global Market Insights Inc. Retrieved June 29, 2026, from https://www.gminsights.com/toc/details/nephrostomy-devices-market

Nephrostomy Devices Market

Get a free sample of this report

Get a free sample of this report Nephrostomy Devices Market

Is your requirement urgent? Please give us your business email for a speedy delivery!

Nephrostomy Devices Market Size

The global nephrostomy devices market was valued at USD 1.4 billion in 2025 and is expected to reach from USD 1.5 billion in 2026 to USD 3.2 billion by 2035, growing at a CAGR of 8.8%, according to the latest report published by Global Market Insights Inc.

The market growth is attributed to the rising prevalence of kidney-related disorders such as kidney stones, hydronephrosis, and urinary tract infections. Also, increasing adoption of minimally invasive procedures and advancements in nephrostomy technologies are further fueling market expansion.

Nephrostomy devices are medical instruments used to drain urine from the kidneys when the normal flow of urine is obstructed due to conditions like kidney stones, tumors, or bladder obstructions. These devices typically consist of a catheter inserted through the skin into the renal pelvis to bypass the urinary tract blockage and allow for the safe drainage of urine. Nephrostomy devices are commonly used in cases of hydronephrosis or when a percutaneous nephrostomy procedure is required.

The major players in the global nephrostomy devices market are Cook Medical, Boston Scientific, Becton, Dickinson and Company, Teleflex, and B. Braun. These companies maintain their competitive position through ongoing product innovation, global market presence, and substantial investment in research and development.

The market has increased from USD 1.1 billion in 2022 and reached USD 1.3 billion in 2024, with a historic growth rate of 8.3%. The growth of the market was driven by the expanding geriatric population, increasing volume of emergency urinary drainage procedures, improved access to interventional radiology services, and rising hospitalization rates for acute renal complications.

Kidney stones affect approximately 10% of men and 7% of women worldwide, with recurrence rates reaching up to 50% within 10 years. Conditions such as hydronephrosis, resulting from urinary tract obstructions, often require nephrostomy to relieve renal pressure and prevent long-term damage.

Furthermore, innovations in device design, including flexible guidewires with hydrophilic coatings and balloon catheters with enhanced inflation control, have improved procedural efficiency and patient safety. These advancements not only reduce complications but also enhance patient comfort during and after procedures. The growing preference for minimally invasive techniques is particularly evident in advanced healthcare regions such as North America and Europe, where outpatient nephrostomy procedures are increasingly adopted.

Nephrostomy Devices Market Trends

Nephrostomy Devices Market Analysis

Based on product, the market is segmented as guidewires, drainage tubes, nephrostomy catheters, sheath dilators, and other products. The guidewires segment generated revenue of USD 448.4 million in 2025.

Based on application, the market is segmented as kidney stones, urinary tract infections, bladder cancer, and other applications. The kidney stones segment is expected to drive business growth reach over USD 1.3 billion by 2035.

Based on patient type, the nephrostomy devices market is segmented as adult and pediatric. The adult segment is expected to drive business growth and expand, reaching over USD 2.6 billion by 2035.

North America Nephrostomy Devices Market

Europe Nephrostomy Devices Market

Europe market accounted for USD 401.2 million in 2025 and is anticipated to show lucrative growth over the forecast period.

Asia Pacific Nephrostomy Devices Market

The Asia Pacific region is projected to show lucrative growth during the forecast period.

Latin America Nephrostomy Devices Market

Brazil is experiencing significant growth in the nephrostomy devices industry.

Middle East and Africa Nephrostomy Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

Nephrostomy Devices Market Share

Nephrostomy Devices Market Companies

Some of the prominent market participants operating in the nephrostomy devices industry include:

BD holds a strong position in the nephrostomy devices, particularly in nephrostomy balloon dilation catheters and access devices. The company’s emphasis on procedural reliability, imaging compatibility, and clinician‑validated designs supports safe and efficient percutaneous renal access, reinforcing its adoption across hospitals and interventional radiology settings globally.

Teleflex is a prominent player in the nephrostomy devices market which includes nephrostomy catheters, puncture sets, and exchange systems. The company differentiates itself through user‑friendly catheter designs, hydrophilic coatings, and solutions optimized for minimally invasive procedures.

B. Braun maintains a solid presence in the nephrostomy devices market through its structured approach to urological drainage systems and percutaneous access solutions. The company’s focus on high‑quality biomaterials, infection‑control technologies, and integrated procedural sets supports safe nephrostomy placement and long‑term drainage management.

Nephrostomy Devices Industry News:

The nephrostomy devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2022 – 2035 for the following segments:

Market, By Product

Market, By Application

Market, By Patient Type

Market, By End Use

The above information is provided for the following regions and countries: