Market Size - By Type (Products, Software, Services), By Application (Reproductive Health, Pregnancy Care, Maternal/Post-Partum and Nursing Care, Integrative Physical and Mental Health & Overall Well-Being, Other Applications), By End Use (Direct-to-Consumer, Hospitals, Fertility Clinics, Surgical Centers, Diagnostic Centers, Other End Users), Growth Forecast. The market forecasts are provided in terms of revenue (USD Million).

Report ID: GMI4442

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Femtech Market Size

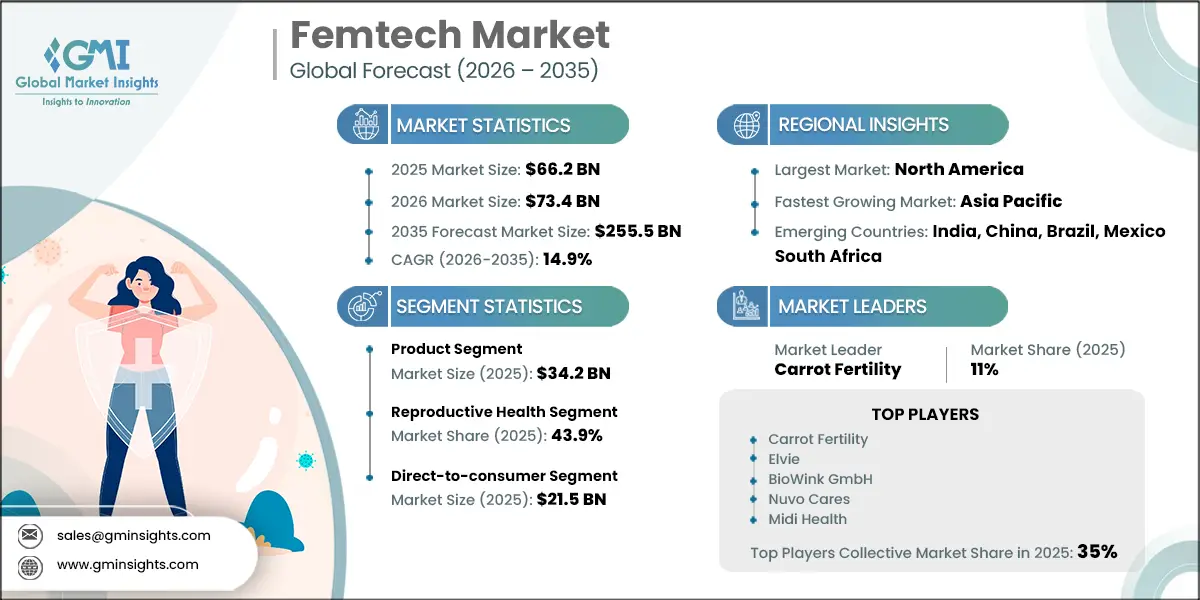

The global femtech market was valued at USD 66.2 billion in 2025 and is projected to grow from USD 73.4 billion in 2026 to USD 255.5 billion by 2035, expanding at a CAGR of 14.9%, according to the latest report published by Global Market Insights Inc.

Digital Health Adoption Accelerates Growth of the Femtech Market

This substantial growth is driven by usage of digital technology to manage women health in developed countries, improving access to women care in remote areas and growing awareness regarding women health and wellness in developing countries.

The market increased from USD 55.1 billion in 2023 to USD 60.2 billion in 2024.The growing adoption of digital technologies to manage women’s health is a major driver of the market in developed countries. High smartphone penetration, widespread internet access, and advanced digital health infrastructure are enabling women to actively monitor and manage their health across different life stages. Mobile health applications, wearable devices, and connected platforms are increasingly used for menstrual cycle tracking, fertility planning, pregnancy monitoring, menopause management, and chronic condition management such as PCOS and endometriosis. In developed economies, rising health awareness and a strong preference for personalized, data-driven healthcare solutions further accelerate Femtech adoption.

Preventive Care and Telehealth Strengthen Technology Adoption in Women's Health

Digital tools empower women with real-time insights, predictive analytics, and evidence-based recommendations, improving early detection, prevention, and treatment outcomes. Integration of artificial intelligence, remote monitoring, and telehealth platforms also enhances clinical decision-making while reducing reliance on in-person visits. Additionally, supportive regulatory frameworks, growing investments in digital health startups, and increasing acceptance of virtual care models among healthcare providers strengthen market growth. As healthcare systems in developed countries prioritize preventive care and patient-centric models, digital women’s health solutions are becoming essential, positioning technology usage as a critical growth driver for the market.

Additionally, improving access to women’s healthcare in remote and underserved areas is a significant driver of the femtech market. Digital solutions such as teleconsultations, mobile health applications, and remote monitoring devices help overcome limitations caused by shortages of specialists, long travel distances, and inadequate healthcare infrastructure. Femtech platforms enable women to access reproductive health advice, prenatal care, menstrual health management, and mental health support without frequent hospital visits. By delivering affordable, discreet, and timely care through digital channels, Femtech reduces health disparities and improves outcomes, making technology-driven women’s healthcare solutions increasingly essential for global market growth.

Femtech, also referred to as female technology, encompasses a wide range of products, services, and software tailored to address women's health concerns. This includes advances in reproductive health, fertility, pregnancy, menopause, menstrual health apps, sexual wellness, and general healthcare for women. The aim of femtech is to bridge gaps in women’s healthcare by offering more targeted, personalized, and accessible solutions through technology.

Femtech Market Trends

Growing awareness around women’s health and wellness in developing countries is emerging as a key driver for the femtech industry. Increased education, public health campaigns, and advocacy by governments and non-governmental organizations are encouraging women to actively seek information and solutions related to reproductive health, maternal care, menstrual hygiene, and mental well-being. This shift is gradually reducing long-standing stigmas and enabling more open conversations around women’s healthcare needs.

Improved access to smartphones and affordable internet connectivity has further amplified this awareness. Women in developing economies are increasingly turning to mobile applications and digital platforms for health education, symptom tracking, remote consultations, and self-care guidance. Femtech solutions provide discreet, accessible, and cost-effective options, making them particularly attractive in regions where traditional healthcare access remains limited.

Rising global investments in Femtech also reinforce this trend. For example, according to Statista, the U.S. led global Femtech investments in 2022 with over USD 11.2 billion, followed by Israel with USD 1.3 billion. These investments highlight the strong confidence in Femtech’s potential to transform women’s healthcare delivery worldwide, including high-growth developing markets.

As awareness increases, women in developing countries are becoming more proactive healthcare consumers, driving demand for digital, personalized, and preventive care solutions. This growing consciousness, supported by global innovation and investment momentum, positions awareness-led adoption as a critical growth driver for the market.

Femtech Market Analysis

Based on type, the femtech market is segmented into products, software, and services. The product segment held revenue of USD 34.2 billion in 2025 and the segment is poised for significant growth at a CAGR of 14.9% during the forecast period.

Software dominates the femtech industry due to its scalability, affordability, and ease of deployment across geographies. Mobile applications and cloud-based platforms allow women to access health insights without reliance on physical devices, making software solutions more widely adopted than hardware-based offerings.

Furthermore, software leverages data analytics, artificial intelligence, and machine learning to deliver tailored insights for menstrual tracking, fertility planning, pregnancy monitoring, and menopause management, improving user engagement and long-term retention.

For instance, Clue offers a data-driven menstrual and ovulation tracking app, while Flo Health uses AI-powered analytics to provide personalized reproductive health guidance. Similarly, Natural Cycles delivers software-based fertility monitoring using algorithm-led predictions, reducing dependence on complex medical devices.

Additionally, software solutions align well with telehealth integration and remote care models. Continuous updates, regulatory flexibility compared to hardware, and easier integration with wearables and electronic health records further strengthen software’s position, making it the leading segment within the market.

Based on application, the femtech market is segmented into Pregnancy care, reproductive health, Maternal/post-partum and nursing care, Integrative physical and mental health & overall well-being, and other applications. The reproductive health segment accounted for a revenue share of 43.9% and with revenue of USD 29.1 billion in 2025.

Reproductive health dominates the market due to its broad scope, covering menstruation, fertility, pregnancy, postpartum care, and menopause. These areas represent recurring and long-term healthcare needs, driving consistent demand for digital solutions that support prevention, monitoring, and decision-making across a woman’s life cycle.

The growing preference for personalized and preventive reproductive healthcare further strengthens this segment. Femtech platforms offer cycle tracking, fertility planning, prenatal monitoring, and postnatal support through data-driven insights, enabling women to manage their reproductive health proactively and conveniently.

The scale of unmet need highlights this dominance. For instance, according to the World Health Organization (WHO), around 15% of couples experience infertility globally, while maternal conditions account for 14.5% of the global disease burden. Additionally, over one-third of women face long-term health issues after childbirth, and 87%–94% report at least one complication in the immediate postpartum period.

As a result, Femtech companies focus heavily on reproductive health to address high-impact clinical gaps and large patient populations. Continuous innovation in AI-driven analytics, teleconsultations, and digital therapeutics has positioned reproductive health applications as the most mature and revenue-generating segment within the market.

Based on end use, the femtech market is segmented into direct-to-consumer, hospitals, fertility clinics, surgical centers, diagnostic centers, and other end-users. The direct-to-consumer segment held the largest revenue of USD 21.5 billion in 2025.

The market is witnessing robust growth as consumers increasingly seek healthcare solutions tailored to their individual needs. Femtech companies are addressing this demand by offering customized products for menstrual health, fertility management, menopause, and chronic conditions through direct-to-consumer (DTC) channels. By leveraging user-generated health data, these companies continuously refine and personalize their offerings, leading to improved product effectiveness and higher consumer satisfaction.

Leading Femtech players are actively launching targeted solutions to address unmet women’s health needs. For instance, in 2024, U.S.-based women’s health startup ELANZA Wellness expanded its portfolio by introducing a dedicated endometriosis care division. Its Endo app enables women to manage symptoms from home through personalized care plans, therapeutic sessions, educational content, and virtual access to support communities and healthcare professionals.

The direct-to-consumer model further strengthens Femtech adoption by offering convenience, accessibility, and discretion. Women can explore and purchase health solutions from the privacy of their homes, which is particularly important for sensitive conditions such as reproductive, sexual, and mental health. This approach removes traditional barriers associated with in-person consultations and retail dependency.

Additionally, DTC platforms allow companies to build direct relationships with users, facilitating continuous feedback and real-time product optimization. These insights enable faster innovation cycles and more responsive care solutions that align with evolving user needs. As digital engagement increases, this model enhances brand loyalty and long-term user retention.

Overall, the combination of personalization, privacy, and seamless digital access has significantly accelerated demand for Femtech products. The expanding use of DTC channels, supported by data-driven innovation, continues to play a critical role in driving sustained growth across the market.

North America Femtech Market

The North America region accounted for 32.4% of the market in 2025. The femtech industry in North America is experiencing robust expansion.

The high penetration of smartphones, wearables, and digital health platforms has transformed women’s healthcare management in North America. Femtech solutions are widely used for menstrual tracking, fertility planning, pregnancy monitoring, and menopause management. These technologies enable continuous engagement and improved health awareness.

Advanced tools such as AI-driven analytics, telehealth services, and remote patient monitoring support personalized and preventive care. Digital platforms facilitate early diagnosis, reduce hospital visits, and enhance treatment adherence. This shift supports efficiency across the healthcare delivery system.

Strong regulatory support, high digital literacy, and increasing investments reinforce Femtech adoption across the region. Digital health is becoming an integral component of women-centric care models. This trend continues to drive sustained growth in the North America femtech market.

The U.S. market benefits from widespread acceptance of digital health solutions focused on women’s reproductive and maternal health. Women increasingly rely on mobile applications and connected devices for preventive care and self-monitoring. These tools align with the country’s push toward value-based healthcare.

Technological advancements such as AI-enabled diagnostics and cloud-based health platforms enable personalized treatment pathways. Telemedicine integration further improves access to specialist care and follow-up services. These developments enhance clinical outcomes while lowering healthcare costs.

Strong startup activity, venture capital funding, and favorable digital health policies accelerate innovation. Digital solutions are rapidly moving from supplementary tools to core healthcare services. This evolution firmly positions technology as a key growth driver of the U.S. market.

Europe Femtech Market

Europe femtech industry accounted for USD 17.4 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

The rising incidence of chronic diseases such as diabetes, and hormonal conditions among women is elevating demand for continuous health management solutions in Europe. Femtech platforms support long-term monitoring and lifestyle management. These tools help address gaps in traditional care pathways.

Infectious diseases impacting reproductive and maternal health further drive the need for early detection technologies. Digital health platforms enable symptom tracking and timely clinical intervention. This improves disease management while reducing strain on public healthcare systems.

Growing focus on preventive and personalized care across European healthcare frameworks supports Femtech adoption. Digital solutions offer scalable and cost-effective disease management capabilities. These factors collectively strengthen the growth trajectory of the Europe market.

Germany femtech market is projected to experience steady growth between 2026 and 2035.

Germany’s advanced healthcare infrastructure and high digital adoption accelerate the use of Femtech solutions. Women increasingly use digital platforms for fertility tracking, pregnancy care, and hormonal health management. These tools enhance patient engagement and informed decision-making.

Integration of telemedicine and electronic health records improves access to gynecological and specialist care. Remote consultations reduce waiting times and optimize resource use within the healthcare system. This digital integration improves continuity of care.

Policy support for digital health innovation and strong data security frameworks further promote adoption. Patients and providers show growing confidence in digital healthcare solutions. This environment continues to drive steady expansion of the Germany market.

Asia Pacific Femtech Market

The Asia Pacific region is projected to show a lucrative growth of about 15.3% during the forecast period.

Rising awareness regarding women’s health and wellness is significantly influencing Femtech adoption across Asia Pacific. Education initiatives and improved health literacy encourage proactive health management. Digital platforms offer privacy and convenience, which are critical adoption factors.

Increasing smartphone usage and internet connectivity enhance access to women-focused health applications. Femtech solutions address unmet needs related to reproductive health, fertility, and maternal care. These platforms play a crucial role in early intervention and self-care.

Support from governments and non-government organizations strengthens awareness and acceptance of digital healthcare. Women are increasingly empowered to manage their health independently. These trends collectively fuel rapid growth in the Asia Pacific market.

India femtech market is poised to witness lucrative growth between 2026 – 2035.

Limited healthcare infrastructure in rural and semi-urban areas has increased reliance on digital health solutions in India. Femtech platforms provide remote consultations, health education, and monitoring services. These tools reduce geographical and socioeconomic barriers.

Mobile-based applications improve access to maternal care, menstrual health management, and chronic disease monitoring. Digital solutions also help overcome cultural stigma and awareness gaps. This enhances early diagnosis and treatment adherence.

Government-led digital health initiatives and expanding mobile penetration further support adoption. Technology bridges access gaps between urban and rural healthcare systems. These factors position Femtech as a critical driver of women’s healthcare transformation in India.

Latin America Femtech Market

Brazil is experiencing significant growth in the market

Brazil’s growing digital health ecosystem supports the increasing use of Femtech platforms. Urban populations actively adopt mobile applications for reproductive health, pregnancy care, and wellness tracking. These technologies promote preventive healthcare behavior.

Wearable devices and remote monitoring tools aid in early risk identification and chronic disease management. Digital solutions help optimize healthcare delivery in an overburdened system. This improves efficiency and patient outcomes.

Rising private investment and digital innovation strengthen the Femtech landscape. Women increasingly prefer technology-enabled health management solutions. This shift continues to drive growth in the Brazil market.

Middle East and Africa Femtech Market

Women’s health awareness initiatives are gaining momentum in Saudi Arabia, with a growing emphasis on preventive care and early treatment for conditions such as menopause, maternal health concerns, and fertility‑related issues. National health programs and public education campaigns are increasingly encouraging women to take a proactive role in managing their reproductive and long‑term health.

Femtech applications play a critical role by enabling early intervention through continuous health tracking, personalized insights, and access to reliable reproductive health information. These digital tools support women in recognizing symptoms earlier, understanding hormonal changes, and making informed decisions about their health.

Additionally, femtech platforms promote reproductive health education and lifestyle modifications, helping users reduce the risk of chronic conditions and improve overall well‑being. By combining technology with preventive healthcare, femtech solutions are becoming an essential component of Saudi Arabia’s evolving women’s health ecosystem.

Femtech Market Share

The top players in the market include Carrot Fertility, Elvie, BioWink, Nuvo Cares, and Midi Health. These companies collectively accounted for an estimated 65% share of the market in 2025.

Leading femtech companies are increasingly focusing on digital innovation, user‑centric design, and platform scalability to enhance health insights, user engagement, and care delivery efficiency. Manufacturers are incorporating advanced capabilities such as AI‑driven health analytics, app‑based symptom tracking, wearable device integration, cloud‑enabled data storage, and real‑time health monitoring across reproductive, maternal, and hormonal health use cases. These advancements enable non‑invasive, continuous health tracking, reduce dependence on in‑person consultations, and support seamless use across clinical, workplace, and home‑based care settings. Improved data visualization, personalized alerts, and automated health recommendations further strengthen product differentiation and drive adoption among consumers and healthcare providers.

Femtech companies are actively expanding collaborations with healthcare providers, digital health platforms, and wellness stakeholders to accelerate market penetration and clinical integration. Partnerships with gynecologists, fertility clinics, maternity centers, employers, and insurance providers support clinical validation, user onboarding, and integration of femtech solutions into routine preventive and chronic care pathways. In parallel, alliances with telehealth providers, government health programs, and public healthcare systems are improving access to women’s digital health services, particularly in emerging regions where awareness and demand for accessible reproductive and maternal health solutions are growing rapidly.

Regional and emerging‑market femtech players are prioritizing affordable, scalable, and localized solutions to address accessibility challenges in cost‑sensitive healthcare environments. By leveraging mobile‑first platforms, subscription‑based pricing, local language support, and regional distribution partnerships, these companies are expanding reach across underserved populations. The development of reliable, easy‑to‑use, and culturally tailored femtech applications and devices is enabling broader adoption across public health systems, smaller clinics, and individual users, supporting more inclusive access to essential women’s health services.

Femtech Market Companies

Few of the prominent players operating in the femtech industry include:

Amara Therapeutics

Athena Feminine Technologies

Baby Billy

BioWink GmbH

Carrot Fertility

Cofertility

Conceivable, Inc.

Elvie

HeraMED

iSono Health

Midi Health

Minerva Surgical

Nuvo Cares

Sera Prognostics

Trellis Health

Univfy

Elvie

Elvie strengthens its competitive positioning in the femtech market through women‑centric medical wearables that combine clinical functionality with consumer‑grade usability. The company’s strength lies in translating intimate areas of women’s health such as breastfeeding and pelvic floor rehabilitation into discreet, connected, and data‑enabled devices that fit seamlessly into everyday life. By focusing on quiet operation, ergonomic design, and app‑based insights, Elvie bridges the gap between regulated medical devices and direct‑to‑consumer wellness technology. Its ability to normalize previously under‑addressed maternal and pelvic health needs, while maintaining compliance with clinical and regulatory expectations, supports strong brand recognition and sustained adoption across maternity, postpartum, and pelvic health segments of the market.

BioWink GmbH

BioWink GmbH reinforces its role in the femtech market by anchoring its strategy around data‑driven menstrual and reproductive health intelligence through the Clue platform. The company’s strength lies in its ability to aggregate large‑scale, longitudinal user data and convert it into evidence‑based cycle tracking, fertility insights, and hormonal health understanding. By prioritizing clinical validation, transparent algorithms, and regulatory‑compliant digital health positioning, Clue differentiates itself from lifestyle‑oriented tracking apps. Its focus on user trust, scientific rigor, and global scalability enables BioWink to function as a foundational digital layer within the femtech ecosystem, supporting both individual women and broader research‑driven women’s health advancements.

Nuvo Cares

Nuvo Cares strengthens its presence in the femtech market by addressing high‑risk and routine pregnancy monitoring through FDA‑cleared, remote fetal surveillance technologies. The company’s strength lies in enabling clinical‑grade antepartum monitoring outside traditional hospital settings, supporting improved access, workflow efficiency, and patient convenience. By combining wearable biosensors, AI‑driven signal processing, and clinician‑focused dashboards, Nuvo delivers reliable fetal and maternal data while maintaining medical‑grade accuracy. Its integration with provider workflows and payer‑focused value propositions positions Nuvo Cares as a critical femtech solution for modernizing maternity care delivery, particularly in underserved, rural, and high‑volume obstetric environments.

Femtech Industry News:

In March 2021, BioWink announced the FDA approval of Clue Birth control, a digital contraceptive integrated within the Clue period-tracking app. This approval enhanced the company’s market presence by providing a new innovative solutions to the consumers and also expanding its product portfolio.

In June 2024, HeraMED limited announced the launched of HeraCARE within the Telstra Health Smart Connected Care Ecosystem. HeraCAREis the first remote maternity solution. This partnership aided HeraCARE by expanding its accessibility in the healthcare industry.

The femtech market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 – 2035 for the following segments:

Market, By Type

Products

Software

Services

Market, By Application

Reproductive health

Menstrual cycle and fertility

Menopause

Pregnancy care

Maternal/post-partum and nursing care

Integrative physical and mental health & overall well-being

Other applications

Market, By End use

Direct-to-consumer

Hospitals

Fertility clinics

Surgical centers

Diagnostic centers

Other end users

The above information is provided for the following regions and countries:

North America

U.S.

Canada

Europe

Germany

UK

France

Italy

Spain

Netherlands

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

Middle East and Africa

Saudi Arabia

South Africa

UAE

Authors: Monali Tayade, Jignesh Rawal

Femtech Market Scope

Femtech Market Size

Femtech Market Trends

Femtech Market Analysis

Femtech Market Share

Report Content

Chapter 1 Research Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.2.1.1 Source consistency protocol

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.5.1.1 Sources, by region

1.6 Base estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.7.1 Quantified market impact analysis

1.7.1.1 Mathematical impact of growth parameters on forecast

1.8 Research transparency addendum

1.8.1 Source attribution framework

1.8.2 Quality assurance metrics

1.8.3 Our commitment to trust

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Type trends

2.2.2 Application trends

2.2.3 End Use trends

2.2.4 Regional trends

2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Usage of digital technology to manage women health in developed countries

3.2.1.2 Improving access to women care in remote areas

3.2.1.3 Growing awareness regarding women health and wellness in developing countries

3.2.1.4 Increasing burden of chronic and infectious diseases among the female population

3.2.2 Industry pitfalls and challenges

3.2.2.1 Growing investments in femtech industry

3.2.2.2 Lack of awareness about femtech products and applications

3.2.3 Market opportunities

3.2.3.1 Corporate wellness and employer-sponsored programs

3.3 Growth potential analysis

3.4 Regulatory landscape (Driven by primary research)

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East and Africa

3.5 Technology landscape (Driven by primary research)

3.5.1 Current technological trends

3.5.1.1 Wearable and sensor based femtech devices

3.5.1.2 Advanced imaging & minimally invasive women’s health technologies

3.5.2 Emerging technologies

3.5.2.1 Next-generation AI & machine learning

3.5.2.2 Digital twin technology for women's health

3.6 Future market trends (Driven by primary research)

3.7 Impact of AI and Generative AI on the market (Driven by primary research)

3.8 Pricing analysis, 2025 (Driven by primary research)

3.9 Porter’s analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 Global

4.2.2 North America

4.2.3 Europe

4.2.4 Asia Pacific

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers and acquisitions

4.6.2 Partnerships and collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 – 2035 ($ Mn)

5.1 Key trends

5.2 Products

5.3 Software

5.4 Services

Chapter 6 Market Estimates and Forecast, By Application, 2022 – 2035 ($ Mn)

6.1 Key trends

6.2 Reproductive health

6.2.1 Menstrual cycle and fertility

6.2.2 Menopause

6.3 Pregnancy care

6.4 Maternal/post-partum and nursing care

6.5 Integrative physical and mental health & overall well-being

6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 – 2035 ($ Mn)

7.1 Key trends

7.2 Direct-to-consumer

7.3 Hospitals

7.4 Fertility clinics

7.5 Surgical centers

7.6 Diagnostic centers

7.7 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 – 2035 ($ Mn)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 UK

8.3.3 France

8.3.4 Spain

8.3.5 Italy

8.3.6 Netherlands

8.4 Asia Pacific

8.4.1 China

8.4.2 Japan

8.4.3 India

8.4.4 Australia

8.4.5 South Korea

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.6 Middle East and Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 UAE

Chapter 9 Company Profiles

9.1 Amara Therapeutics

9.2 Athena Feminine Technologies

9.3 Baby Billy

9.4 BioWink GmbH

9.5 Carrot Fertility

9.6 Cofertility

9.7 Conceivable, Inc.

9.8 Elvie

9.9 HeraMED

9.10 iSono Health

9.11 Midi Health

9.12 Minerva Surgical

9.13 Nuvo Cares

9.14 Sera Prognostics

9.15 Trellis Health

9.16 Univfy

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Regional or domestic-only leaders not in the global top tier

Distributors and channel partners who control market access

Emerging disruptors, startups, or adjacent-industry entrants

Niche players focused on a specific application or end-use

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Authors: Monali Tayade, Jignesh Rawal

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at[email protected]

Explore our licensing options:

Starting at: $2,450

Premium Report Details

Base Year: 2025

Companies Profiled: 16

Tables and Figures: 299

Countries covered: 16

Pages: 130

Download Free PDF

Premium Report Details

Base Year: 2025

Companies Profiled: 16

Tables and Figures: 299

Countries covered: 16

Pages: 130

Download Free PDF

Share Content

Add Citations

Monali Tayade. 2026, April. Femtech Market – By Type, By Application, By End Use, Growth Forecast, 2026 – 2035 (Report ID: GMI4442). Global Market Insights Inc. Retrieved August 8, 2026, from https://www.gminsights.com/toc/details/femtech-market

Femtech Market

Get a free sample of this report

Get a free sample of this report Femtech Market

Is your requirement urgent? Please give us your business email for a speedy delivery!

Femtech Market Size

The global femtech market was valued at USD 66.2 billion in 2025 and is projected to grow from USD 73.4 billion in 2026 to USD 255.5 billion by 2035, expanding at a CAGR of 14.9%, according to the latest report published by Global Market Insights Inc.

Digital Health Adoption Accelerates Growth of the Femtech Market

This substantial growth is driven by usage of digital technology to manage women health in developed countries, improving access to women care in remote areas and growing awareness regarding women health and wellness in developing countries.

The market increased from USD 55.1 billion in 2023 to USD 60.2 billion in 2024.The growing adoption of digital technologies to manage women’s health is a major driver of the market in developed countries. High smartphone penetration, widespread internet access, and advanced digital health infrastructure are enabling women to actively monitor and manage their health across different life stages. Mobile health applications, wearable devices, and connected platforms are increasingly used for menstrual cycle tracking, fertility planning, pregnancy monitoring, menopause management, and chronic condition management such as PCOS and endometriosis. In developed economies, rising health awareness and a strong preference for personalized, data-driven healthcare solutions further accelerate Femtech adoption.

Preventive Care and Telehealth Strengthen Technology Adoption in Women's Health

Digital tools empower women with real-time insights, predictive analytics, and evidence-based recommendations, improving early detection, prevention, and treatment outcomes. Integration of artificial intelligence, remote monitoring, and telehealth platforms also enhances clinical decision-making while reducing reliance on in-person visits. Additionally, supportive regulatory frameworks, growing investments in digital health startups, and increasing acceptance of virtual care models among healthcare providers strengthen market growth. As healthcare systems in developed countries prioritize preventive care and patient-centric models, digital women’s health solutions are becoming essential, positioning technology usage as a critical growth driver for the market.

Additionally, improving access to women’s healthcare in remote and underserved areas is a significant driver of the femtech market. Digital solutions such as teleconsultations, mobile health applications, and remote monitoring devices help overcome limitations caused by shortages of specialists, long travel distances, and inadequate healthcare infrastructure. Femtech platforms enable women to access reproductive health advice, prenatal care, menstrual health management, and mental health support without frequent hospital visits. By delivering affordable, discreet, and timely care through digital channels, Femtech reduces health disparities and improves outcomes, making technology-driven women’s healthcare solutions increasingly essential for global market growth.

Personalized Femtech Innovations Redefine Women's Healthcare

Femtech, also referred to as female technology, encompasses a wide range of products, services, and software tailored to address women's health concerns. This includes advances in reproductive health, fertility, pregnancy, menopause, menstrual health apps, sexual wellness, and general healthcare for women. The aim of femtech is to bridge gaps in women’s healthcare by offering more targeted, personalized, and accessible solutions through technology.

Femtech Market Trends

Femtech Market Analysis

Based on type, the femtech market is segmented into products, software, and services. The product segment held revenue of USD 34.2 billion in 2025 and the segment is poised for significant growth at a CAGR of 14.9% during the forecast period.

Based on application, the femtech market is segmented into Pregnancy care, reproductive health, Maternal/post-partum and nursing care, Integrative physical and mental health & overall well-being, and other applications. The reproductive health segment accounted for a revenue share of 43.9% and with revenue of USD 29.1 billion in 2025.

Based on end use, the femtech market is segmented into direct-to-consumer, hospitals, fertility clinics, surgical centers, diagnostic centers, and other end-users. The direct-to-consumer segment held the largest revenue of USD 21.5 billion in 2025.

North America Femtech Market

The North America region accounted for 32.4% of the market in 2025. The femtech industry in North America is experiencing robust expansion.

Europe Femtech Market

Europe femtech industry accounted for USD 17.4 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

Germany femtech market is projected to experience steady growth between 2026 and 2035.

Asia Pacific Femtech Market

The Asia Pacific region is projected to show a lucrative growth of about 15.3% during the forecast period.

India femtech market is poised to witness lucrative growth between 2026 – 2035.

Latin America Femtech Market

Brazil is experiencing significant growth in the market

Middle East and Africa Femtech Market

Femtech Market Share

Femtech Market Companies

Few of the prominent players operating in the femtech industry include:

Elvie strengthens its competitive positioning in the femtech market through women‑centric medical wearables that combine clinical functionality with consumer‑grade usability. The company’s strength lies in translating intimate areas of women’s health such as breastfeeding and pelvic floor rehabilitation into discreet, connected, and data‑enabled devices that fit seamlessly into everyday life. By focusing on quiet operation, ergonomic design, and app‑based insights, Elvie bridges the gap between regulated medical devices and direct‑to‑consumer wellness technology. Its ability to normalize previously under‑addressed maternal and pelvic health needs, while maintaining compliance with clinical and regulatory expectations, supports strong brand recognition and sustained adoption across maternity, postpartum, and pelvic health segments of the market.

BioWink GmbH reinforces its role in the femtech market by anchoring its strategy around data‑driven menstrual and reproductive health intelligence through the Clue platform. The company’s strength lies in its ability to aggregate large‑scale, longitudinal user data and convert it into evidence‑based cycle tracking, fertility insights, and hormonal health understanding. By prioritizing clinical validation, transparent algorithms, and regulatory‑compliant digital health positioning, Clue differentiates itself from lifestyle‑oriented tracking apps. Its focus on user trust, scientific rigor, and global scalability enables BioWink to function as a foundational digital layer within the femtech ecosystem, supporting both individual women and broader research‑driven women’s health advancements.

Nuvo Cares strengthens its presence in the femtech market by addressing high‑risk and routine pregnancy monitoring through FDA‑cleared, remote fetal surveillance technologies. The company’s strength lies in enabling clinical‑grade antepartum monitoring outside traditional hospital settings, supporting improved access, workflow efficiency, and patient convenience. By combining wearable biosensors, AI‑driven signal processing, and clinician‑focused dashboards, Nuvo delivers reliable fetal and maternal data while maintaining medical‑grade accuracy. Its integration with provider workflows and payer‑focused value propositions positions Nuvo Cares as a critical femtech solution for modernizing maternity care delivery, particularly in underserved, rural, and high‑volume obstetric environments.

Femtech Industry News:

The femtech market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 – 2035 for the following segments:

Market, By Type

Market, By Application

Market, By End use

The above information is provided for the following regions and countries: