Video Surveillance Market Size & Share 2026-2035

Market Size – By Offering (Hardware, Software, Services), By Deployment (On-premise, Cloud, Hybrid), By System Type (Analog Video Surveillance Systems, IP Video Surveillance Systems, Hybrid Video Surveillance Systems), By Application (Commercial, Residential, Industrial, Infrastructure & Transportation, Institutional, Others) - Growth Forecast. The market forecasts are provided in terms of revenue (USD).

Report ID: GMI10380

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Authors:

Suraj Gujar, Ankita Chavan

Video Surveillance Market Size

The video surveillance market was valued at USD 63.1 billion in 2025. The market is expected to grow from USD 68.5 billion in 2026 to USD 107.5 billion in 2031 & USD 162.4 billion in 2035, at a CAGR of 10.1% during the forecast period according to the latest report published by Global Market Insights Inc.

Video Surveillance Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

The growing use of edge-based Artificial Intelligence (AI) has also emerged as a new growth factor in the video surveillance market, considering the growing importance of edge-based AI in terms of real-time analytics, lower latency, and improved data privacy. This has become increasingly important in terms of immediate analytics and response, such as smart cities, transportation hubs, and critical infrastructures, among others. Keeping a pace with this growing importance, in March 2026, i-PRO introduced its X-series fisheye cameras, which were unveiled during ISC West 2026, incorporating generative AI functions fully on the edge. This has been enabled through Ambarella’s CV72 SoC, allowing for natural language-based, free text detection, such as “person lying down,” without cloud connectivity, thereby underlining the growing sophistication and independence of edge-based AI-enabled video surveillance.

The increasing rates of crime, terrorism, and security hazards are the key factors fueling the growth of the video surveillance market. As people are becoming more security-conscious, the need for effective video surveillance has risen manifold. This has led to an increased awareness among governments, businesses, and the general public about the need to install effective video surveillance solutions to avoid the threat of security hazards in the future. A trend is being developed to integrate video surveillance with other smart technologies, such as access control and alarm systems, to form an integrated security system. Organizations are realizing the importance of adhering to legal requirements related to safety and security, hence the need to adopt video surveillance systems.

Video Surveillance Market Trends

Video Surveillance Market Analysis

Based on the system type, the video surveillance market is segmented into analog video surveillance systems, IP video surveillance systems, and hybrid video surveillance systems.

The IP video surveillance systems market is projected to grow at a CAGR of 11.1% by 2035. IP video surveillance systems are experiencing strong growth driven by rapid advancements in artificial intelligence, cloud computing, and real-time video analytics. These systems offer superior image quality, scalability, and intelligent functionalities such as facial recognition, object tracking, and behavioral analysis, making them highly suitable for modern security requirements.

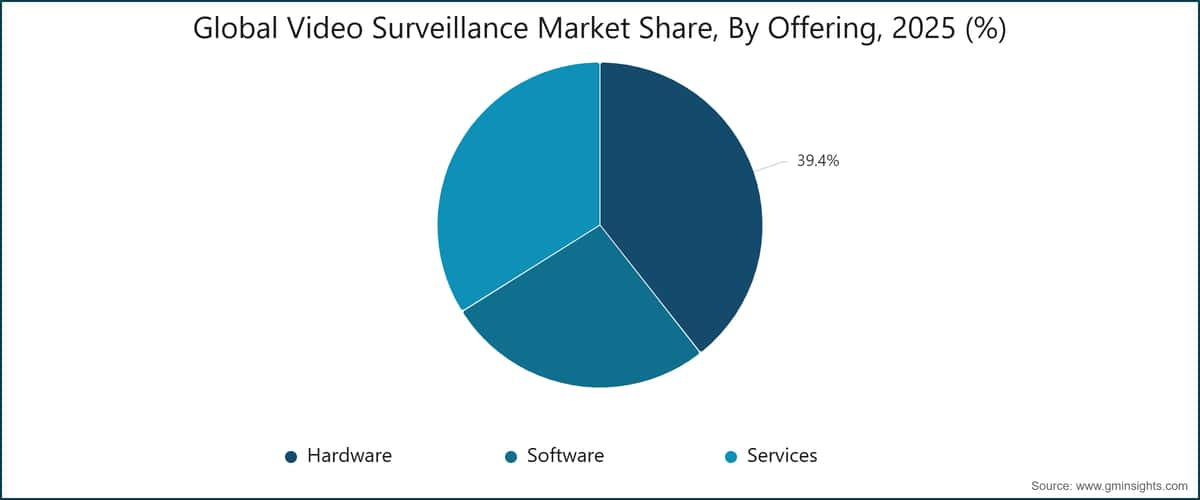

Based on offering, the market is segmented into hardware, software, and services.

Based on the deployment, the global video surveillance market is divided into on-premise, cloud, and hybrid.

North America Video Surveillance Market

North America held a share of 31.1% of video surveillance industry in 2025.

The U.S. video surveillance market was valued at USD 13.2 billion and USD 14.5 billion in 2022 and 2023, respectively. The market size reached USD 17.3 billion in 2025, growing from USD 15.9 billion in 2024.

Europe Video Surveillance Market

Europe market accounted for USD 13.9 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

Germany dominates the Europe video surveillance industry, showcasing strong growth potential.

Asia Pacific Video Surveillance Market

The Asia Pacific market is anticipated to grow at the highest CAGR of 10.9% during the forecast period.

China video surveillance market is estimated to grow with a significant CAGR, in the Asia Pacific market.

Middle East and Africa Video Surveillance Market

UAE video surveillance industry to experience substantial growth in the Middle East and Africa.

Video Surveillance Market Share

The major players in the video surveillance industry are Qualcomm Inc., ViewSonic Corporation, Looking Glass Factory Inc., RealFiction Holding AB and MDH Hologram Ltd. are the major players accounting for a significant share of 29.6% in the market. These companies compete across a diverse range of end-use industries with offerings such as AI-enabled cameras, video management software, cloud-based surveillance platforms, and advanced analytics solutions for applications in public safety, transportation, retail, commercial, and critical infrastructure sectors. Competition is primarily driven by technological advancements, particularly in artificial intelligence, edge computing, and real-time video analytics, along with pricing pressures and system scalability. Key growth factors include continuous innovation in intelligent surveillance capabilities, increasing demand for automated threat detection, and the integration of video systems with IoT and smart city ecosystems. Additionally, several niche and emerging players focus on specialized solutions such as facial recognition, behavioral analytics, and cybersecurity-enhanced surveillance, enabling them to compete effectively through differentiation.

Video Surveillance Market Companies

Prominent players operating in the video surveillance industry are as mentioned below:

Hangzhou Hikvision Digital Technology Co., Ltd.

Hikvision is a dominant player in the video surveillance market, offering a comprehensive portfolio of cameras, video management systems, and AI-driven analytics solutions. The company’s strength lies in its large-scale manufacturing capabilities, cost competitiveness, and rapid integration of AI and deep learning technologies. Its focus on smart city projects, public safety, and enterprise surveillance solutions has enabled strong global penetration, particularly in emerging markets, although it faces regulatory and geopolitical challenges in certain regions.

Honeywell

Honeywell plays a significant role in the video surveillance market through its integrated security and building management solutions. The company leverages its expertise in automation and IoT to offer advanced surveillance systems combined with access control, fire safety, and analytics platforms. Its strong presence in commercial buildings, critical infrastructure, and industrial facilities, along with a focus on cybersecurity and system integration, positions it well in high-value enterprise and government segments.

Axis Communications AB

Axis Communications is a key innovator in IP-based video surveillance, recognized for pioneering network cameras and continuously advancing edge-based analytics. The company emphasizes high-quality imaging, cybersecurity, and open-platform solutions, enabling seamless integration with third-party software and systems. Its strong focus on research and development, along with premium product positioning, has established it as a leading player in enterprise-grade and smart city surveillance deployments globally.

Hanwha Vision Co., Ltd.

Hanwha Vision is a prominent player known for its advanced AI-powered surveillance solutions and high-performance imaging technologies. The company focuses on delivering intelligent video analytics, cybersecurity-enhanced systems, and edge-based processing capabilities. With a growing presence in global markets, Hanwha Vision is expanding its footprint across transportation, retail, and critical infrastructure sectors, supported by continuous innovation and strategic partnerships.

Motorola Solutions, Inc.

Motorola Solutions is a leading provider of end-to-end video surveillance and public safety solutions, integrating cameras, video analytics, and command center software. The company’s strength lies in its ecosystem approach, combining video security with communication systems and emergency response platforms. Its focus on AI-driven analytics, cloud-based solutions, and mission-critical applications has enabled strong adoption across law enforcement, government, and enterprise sectors, reinforcing its leadership in high-security and public safety markets.

13.3% market share in 2025

Collective market share in 2025 is 29.6%

Video Surveillance Industry News

The video surveillance market research report includes in-depth coverage of the industry with estimates and forecast in terms of revenue (USD Million) from 2022 – 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Offering

Market, By Deployment

Market, By System Type

Market, By Application

The above information is provided for the following regions and countries:

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →