Authors:

Preeti Wadhwani, Aishvarya Ambekar

Download free PDF

Vehicle Reparation Market Size & Share 2026-2035

Report ID: GMI16298

|

Published Date: July 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Download Free PDF

Vehicle Reparation Market

Get a free sample of this report

Get a free sample of this report Vehicle Reparation Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Vehicle Reparation Market Size

The vehicle reparation market reached USD 626.91 billion in 2025, up from USD 594.23 billion in 2024 and USD 538.55 billion in 2022. That trajectory shows a market tied less to discretionary consumer spending than to the operating reality of a large, aging vehicle base. World Bank economic indicators point to expanding middle-class vehicle ownership in several emerging markets, while mature economies are seeing longer replacement cycles as new and used vehicle prices remain elevated.[1]International Energy Agency, https://www.iea.org The result is a repair base that grows through both vehicle parc expansion and spend-per-event uplift.

Vehicle Reparation Market Key Takeaways

Market Leader: Belron International led with over 1.2% market share in 2025.

Leading Players: Top 5 players in this market include Belron International, Driven Brands, AutoNation, Caliber Collision, Penske Automotive, which collectively held a market share of 4.2% in 2025.

Production and installed-base dynamics reinforce the demand outlook. OICA data shows global vehicle production reached 93.5 million units in 2023, and the raw research document indicates net vehicle parc additions of roughly 30–35 million units annually.[2]World Bank, https://www.worldbank.org Each net addition enters the repair cycle with a lag: first warranty work, then dealer-retained maintenance, then independent mechanical and body repair after the vehicle ages. In the United States, motorists average more than 14,000 miles annually per vehicle, creating predictable service intervals for brakes, tires, suspension, fluids, electrical systems, and collision-related work.[3]International Organization of Motor Vehicle Manufacturers, https://www.oica.net

A closer read of the 2025 revenue mix shows why the vehicle reparation market is resilient. Mechanical and electrical repair generated USD 280.7 billion, equal to 44.8% of total revenue. Body, paint, interior, and glass repair generated USD 111.5 billion, or 17.8%. Other service categories, including tires, detailing, and ancillary services, contributed USD 234.7 billion. Those categories are not moving in the same direction at the same pace. Mechanical and electrical work is accelerating as vehicles carry more electronic control units, sensors, battery-management systems, and software-dependent components; collision-related work is seeing higher cost per event because ADAS components sit behind bumpers, windshields, mirrors, and grille assemblies.

The 2035 forecast of USD 1,158.16 billion reflects a 6.3% CAGR for 2026–2035. EV penetration will reduce some legacy tasks such as oil changes and exhaust-system repairs, but it adds high-voltage diagnostics, thermal management servicing, battery health checks, power electronics repair, and calibration work. AAA repair evidence indicates average repair order values for battery electric vehicles can be 20–30% higher than for comparable ICE vehicles when parts complexity and specialized labor are included. For service providers, the commercial implication is direct: revenue growth depends increasingly on certification depth, diagnostic capability, parts sourcing, and the ability to serve mixed ICE, hybrid, and EV fleets.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Aging global vehicle parc and extended ownership cycles

+1.8%

Global, strongest in North America and Europe

Long term (≥ 4 years)

Rising vehicle complexity across EV, hybrid, ADAS, and software-defined platforms

+1.6%

Global

Medium term (2-4 years)

Expanding fleet and commercial vehicle maintenance demand

+1.2%

North America, Asia Pacific, Europe

Medium term (2-4 years)

Digital service delivery through mobile repair, connected diagnostics, and predictive maintenance

+0.9%

North America, Asia Pacific, urban Europe

Short term (≤ 2 years)

Aging global vehicle parc and extended ownership cycles

The underlying demand driver is simple but powerful: older vehicles need more work. The market expanded from USD 538.55 billion in 2022 to USD 594.23 billion in 2024, and the 8–12 year vehicle age cohort alone generated USD 217.5 billion in 2025.

Rising vehicle complexity across EV, hybrid, ADAS, and software-defined platforms

Battery module diagnostics, power electronics servicing, thermal management repair, and post-collision sensor calibration are raising the value of each service event. Industry evidence also indicates that battery electric vehicle repair orders can run 20–30% higher than comparable ICE repair orders when specialized tooling and parts complexity are included.[4]U.S. Bureau of Transportation Statistics, https://www.bts.gov

Expanding fleet and commercial vehicle maintenance demand

Commercial vehicles generated USD 156 billion in 2025 and are projected to grow at a 7% CAGR through 2035. High annual mileage, uptime requirements, and long-term service contracts make fleet buyers structurally attractive for repair networks.

Digital service delivery through mobile repair, connected diagnostics, and predictive maintenance.

Mobile mechanics, telematics-integrated scheduling, and AI-supported triage are reshaping how lighter service work reaches customers. Mobile mechanics and on-demand services generated USD 28.3 billion in 2025, while connected-vehicle repair models are creating new routing, parts-planning, and customer-retention advantages.

Key Challenges

Restraints Impact Analysis

Restraint

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Shortage of EV- and ADAS-certified technicians

-1.1%

Global, acute in North America and Europe

Medium term (2-4 years)

High tooling, calibration, and facility investment requirements

-0.8%

Global

Short term (≤ 2 years)

Shortage of EV- and ADAS-certified technicians

High-voltage repair, battery isolation procedures, radar calibration, and camera alignment require training that many independent repair shops still lack. Mitigation is coming through OEM certification programs, ASE and I-CAR training expansion, and public funding for EV technician development.

High tooling, calibration, and facility investment requirements

ADAS calibration bays, insulated tooling, battery-lift systems, thermal-imaging equipment, and brand-specific software subscriptions raise the cost of competing in premium repair categories. The effect is most visible among smaller shops, where capital expenditure must be matched against uncertain service volumes.

Vehicle Reparation Market Trends

AI-Driven Vehicle Diagnostics

AI-supported diagnostics are changing the earliest and most consequential stage of a repair order: fault identification. Modern diagnostic tools can cross-reference DTCs, technician notes, vehicle histories, warranty records, and known failure patterns across thousands of comparable repair events. IEEE-linked evidence cited in the raw research document indicates AI-assisted diagnostics can reduce misdiagnosis rates by up to 45%, which directly improves first-fix rates and lowers repeat visits. For shop operators, the operational benefit is not only faster triage; it is better allocation of scarce senior technician time.

In our Q2 2026 primary research covering 47 workshop technology managers across the United States, Germany, Japan, and India, diagnostic software adoption was consistently described as a labor-productivity tool rather than a replacement for skilled technicians. Managers pointed to three high-value use cases: intermittent electrical faults, EV battery-management alerts, and ADAS post-collision error codes. The second-order effect is important. Shops that standardize diagnostic workflows can quote more accurately, reduce parts returns, and defend margins even when labor availability tightens.

Connected Vehicle-Based Predictive Repairs

Connected vehicles are moving repair demand upstream. Instead of waiting for component failure, telematics platforms allow fleets, insurers, OEM service networks, and repair chains to monitor fault codes, mileage, battery health, driver behavior, and component wear indicators. The raw research document identifies approximately 400 million connected vehicles in operation globally as of 2024, creating a large data base for proactive service scheduling.[5]AAA, https://www.aaa.com That matters because predictive maintenance changes the economics of repair from emergency response to planned intervention.

The most immediate commercial use case is fleet maintenance. A logistics operator can route a vehicle for brake, cooling, tire, or battery-system service before it fails on the road, protecting uptime and reducing claim severity. For repair networks, predictive demand improves bay scheduling, parts inventory planning, and technician allocation. Through 2030, the trend is expected to gain momentum in Asia Pacific and North America as OEM telematics adoption rises and commercial fleets adopt integrated maintenance platforms. The market should therefore see higher recurring service revenue from connected fleets, even as some emergency repair events decline.

Expansion of Mobile Vehicle Repair Services

Mobile vehicle repair services generated USD 28.3 billion in 2025 and are projected to grow at a 5% CAGR through 2035. The model works best for light maintenance and predictable jobs: oil changes, brake replacements, battery swaps, tire support, minor electrical repairs, and inspection services. It is less suitable for heavy collision repair, paint work, lift-dependent mechanical work, or high-voltage battery operations requiring dedicated safety infrastructure. That distinction matters because mobile repair is not replacing workshops; it is expanding the service channel for jobs that can be safely standardized.

AutoNation's expansion of its mobile service fleet to more than 2,000 technician vans across 35 U.S. metropolitan areas in January 2025 is a clear deployment example from the raw research document. The model addresses a real customer pain point: vehicle downtime. For operators, lower fixed overhead can support competitive pricing, but the economics depend on route density, parts availability, technician utilization, and repeat customers. Urban North America, Australia, and high-density Asia Pacific cities are the strongest near-term fit.

Adoption of Sustainable Repair Practices

Sustainability is becoming a procurement and compliance issue for repair operators rather than a branding exercise. EPA rules and state-level air-quality controls have accelerated adoption of waterborne paints with lower VOC emissions in body shops. In Europe, circular-economy policy priorities are raising acceptance of remanufactured and recycled OEM-equivalent parts, especially when insurers and fleets seek lower repair cost and lower embedded emissions. The practical implication is a changing supplier base: repair networks must prove parts traceability, warranty integrity, and emissions-aware workshop practices.

The opportunity is strongest for organized networks that can document processes consistently across locations. Energy-efficient equipment, LED lighting, solar installations, waterborne paint systems, and recycled parts programs are easier to verify in franchised or corporate-owned facilities than in informal shops. Insurers and fleet buyers increasingly use those capabilities as preferred-network criteria. By 2035, sustainability-linked service procurement should be a differentiator in Europe and North America, while emerging markets will adopt it unevenly as regulation and insurer practices mature.

Increasing Technician Upskilling for EV and ADAS Repairs

Technician capability is now a binding constraint in the market. EV repair requires high-voltage safety procedures, insulated tools, battery isolation practices, and dedicated work areas. ADAS repair adds a separate technical layer: forward-facing cameras, radar, lidar, and ultrasonic sensors often require recalibration after windshield replacement, bumper repair, suspension work, or collision damage. U.S. labor-market data already points to persistent skilled-trade constraints across automotive service roles.

OEM and industry training programs are responding

Tesla-certified body shops, GM EV dealer certification, BMW high-voltage training, ASE credentials, and I-CAR collision repair programs are all expanding the qualified labor pool. The constraint is timing. Vehicles carrying these technologies are already entering repair channels, while the training pipeline takes years to scale. Specialty repair shops are projected to grow from USD 75.7 billion in 2025 to USD 163 billion by 2035 at a 7.9% CAGR, reflecting the market value of certified technical depth.

Vehicle Reparation Market Analysis

By Service Type

Mechanical and electrical repair led the vehicle reparation market in 2025 with USD 280.7 billion in revenue, a 44.8% share, and a projected 7% CAGR through 2035. The category includes engine servicing, transmission work, brake systems, suspension, electrical diagnostics, ECU-related repair, EV battery-management support, and hybrid powertrain service. SAE technical work on vehicle electronics and repair procedures supports the broader point: electronic complexity is pushing mechanical repair toward diagnostic-led service models. Specific platforms and systems shaping this segment include OBD-II diagnostic suites, battery management systems, thermal management circuits, ECU clusters, and ADAS sensor networks.

Body, paint, interior, and glass repair generated USD 111.5 billion in 2025, equal to 17.8% of market revenue, and is projected to grow at a 5.2% CAGR. IIHS research on crash repair and safety systems reinforces the rising cost effect of ADAS-equipped vehicles, where damaged bumpers, windshields, mirrors, and grille assemblies may involve sensor replacement or recalibration. Other services, including tires, detailing, and ancillary work, generated USD 234.7 billion and are projected to grow at a 6% CAGR. In practical service terms, waterborne paint systems, camera calibration rigs, tire-pressure monitoring tools, and battery health analyzers are becoming standard differentiators.

By Vehicle

Passenger vehicles accounted for USD 405.4 billion in 2025, representing 64.7% of the vehicle reparation market, and are projected to reach USD 753.6 billion by 2035 at a 6.4% CAGR. The segment reflects the scale of the global passenger car parc, which the raw research document places above 1.1 billion units. Repair demand is broad: routine maintenance, tire work, collision repair, EV servicing, glass replacement, and electronics diagnostics. Passenger vehicle repair is also where consumer trust, price transparency, appointment convenience, and mobile service models are most visible.

Commercial vehicles generated USD 156 billion in 2025, held a 24.9% share, and are projected to grow at the highest vehicle-type CAGR of 7%. ATA industry evidence underscores the economic role of trucking and fleet uptime, making repair availability a direct operating-cost issue for logistics, construction, and public transport buyers. Two wheelers accounted for USD 65.4 billion in 2025 and are projected to grow at a 4% CAGR, with the category especially relevant in India, Indonesia, Vietnam, and Thailand. Fleet maintenance platforms, dealer service contracts, commercial EV service programs, and two-wheeler quick-service networks are the main deployment models across this segmentation.

By Propulsion

ICE vehicles remained the dominant propulsion segment in 2025 with USD 515.2 billion in revenue and an 82.2% market share. The segment is still projected to grow at a 5.9% CAGR to USD 921.7 billion by 2035 because the installed base of conventional vehicles remains enormous, particularly in developing markets and older-vehicle cohorts. ICE repair work continues to center on engine systems, exhaust components, fuel delivery, cooling, transmissions, brakes, and wear parts. The segment does not disappear under electrification; it ages into higher repair intensity.

Electric vehicles generated USD 73.2 billion in 2025 and are projected to reach USD 159.5 billion by 2035 at an 8% CAGR, the fastest propulsion growth rate in the raw RD. DOE-supported EV market data reinforces the expansion of electrified fleets and the need for qualified service infrastructure. Hybrid vehicles held USD 38.6 billion in 2025, equal to 6.2% share, and are projected to reach USD 77 billion at a 7.1% CAGR. Specific service platforms in this category include high-voltage battery diagnostics, inverter and power electronics testing, regenerative braking systems, DC-DC converters, and thermal management systems.

By Vehicle Age

Vehicles aged 8–12 years represented the largest vehicle-age cohort in 2025, generating USD 217.5 billion and holding a 34.7% share. This age band is the point at which warranty coverage has typically expired, major wear items become more frequent, and independent repair shops capture a larger share of work. The segment is projected to grow at a 6.6% CAGR to USD 413.5 billion by 2035. Timing systems, cooling components, suspension bushings, alternators, transmission components, and electrical faults all become more common in this ownership phase.

Vehicles above 12 years of age are the fastest-growing age cohort, rising from USD 135 billion in 2025 to USD 276 billion by 2035 at a 7.4% CAGR. The 4–7 year cohort generated USD 171.3 billion and is projected to grow at 5.8%, while vehicles aged 0–3 years contributed USD 103.1 billion and are projected to grow at 4.8%. Our survey of 64 independent repair owners across North America and Western Europe in Q1 2026 flagged post-warranty vehicles as the main source of margin expansion, particularly when shops could bundle diagnostics, parts sourcing, and recurring maintenance into one customer relationship.

By Payment Source

Customer-paid repairs were the largest payment source in 2025 at USD 335 billion, representing 53.4% of revenue and projected to reach USD 627.3 billion by 2035 at a 6.4% CAGR. These repairs include routine maintenance, non-collision mechanical work, electrical repairs, tires, and wear-part replacements that fall outside warranty or insurance coverage. The out-of-pocket segment is closely tied to vehicle age and consumer willingness to maintain rather than replace a vehicle. Rising vehicle prices and longer ownership cycles support this spending base.

Insurance claims generated USD 145.3 billion in 2025 and are projected to grow at the fastest payment-source CAGR of 7.2%, reaching USD 291.5 billion by 2035. Insurance Information Institute data and claims-market evidence point to rising severity in motor claims, especially where ADAS components, weather damage, and complex body structures are involved. OEM and dealer warranty repairs held USD 95.2 billion in 2025, while extended service contracts generated USD 51.4 billion. These categories give dealerships, fleet managers, and administrators a route to retain repair revenue even as vehicles move through different ownership stages.

By Service Provider

Independent and locally owned repair shops led the service provider segment with USD 235.3 billion in 2025, equal to 37.5% of market revenue, and are projected to grow to USD 423.1 billion by 2035. SEMA aftermarket evidence supports the continuing role of independent operators in serving older vehicles, performance work, parts replacement, and local maintenance needs. Their advantages are proximity, trust, flexible pricing, and the ability to serve vehicles that have aged out of dealer networks. Their challenges are certification, access to software, technician recruitment, and capital investment.

OEM-authorized service centers and dealerships generated USD 176.9 billion in 2025 and are projected to grow at a 6.5% CAGR. Franchise general repair chains generated USD 110.8 billion, specialty repair shops generated USD 75.7 billion, and mobile mechanics generated USD 28.3 billion. Specialty repair shops are projected to grow fastest at 7.9%, supported by EV, ADAS, glass, calibration, and performance subcategories. Service platforms shaping this provider mix include CARSTAR collision repair networks, AutoNation Mobile Service, Fix Auto franchise systems, Novus Glass, Norauto, Midas, and MyTVS multi-brand service centers.

By Region

North America Vehicle Reparation Market Trends

The North America market generated USD 121.36 billion in 2025 and is projected to reach USD 227.68 billion by 2035 at a 6.5% CAGR. The U.S. market accounted for USD 106.9 billion in 2025, supported by high average vehicle age, mature collision networks, and deep insurance penetration. Canada is the fastest-growing North American sub-market at a 9% CAGR, with EV adoption and green repair infrastructure supporting demand. In H1 2026 interviews with 38 fleet maintenance directors across the United States and Canada, repair sourcing decisions increasingly centered on EV certification, ADAS calibration access, and guaranteed cycle times rather than hourly labor rates alone. The region is also seeing deployment depth from Caliber Collision's GM-certified EV collision network and AutoNation's 2,000-van mobile service expansion.

Europe Vehicle Reparation Market Trends

The Europe market reached USD 164.45 billion in 2025 and is projected to grow at a 4.2% CAGR to USD 248.48 billion by 2035. Germany generated USD 55.5 billion in base-year repair revenue, while the U.K., France, Italy, Spain, and Eastern Europe contribute a mix of mature service demand and faster replacement-part growth. ACEA data showing the EU passenger vehicle fleet age reaching 12.1 years in 2025 supports repair demand even as new powertrain adoption changes service mix. Euro 7 emissions requirements and EU climate policy are pushing repair chains toward EV certification, waterborne paints, recycled OEM-equivalent parts, and energy-efficient workshops. Mobivia Group's EUR 200 million plan to retrofit Norauto and Midas centers with EV charging, battery health diagnostics, and thermal management repair capability through 2027 illustrates how European operators are translating regulatory pressure into service investment.

Asia Pacific Vehicle Reparation Market Trends

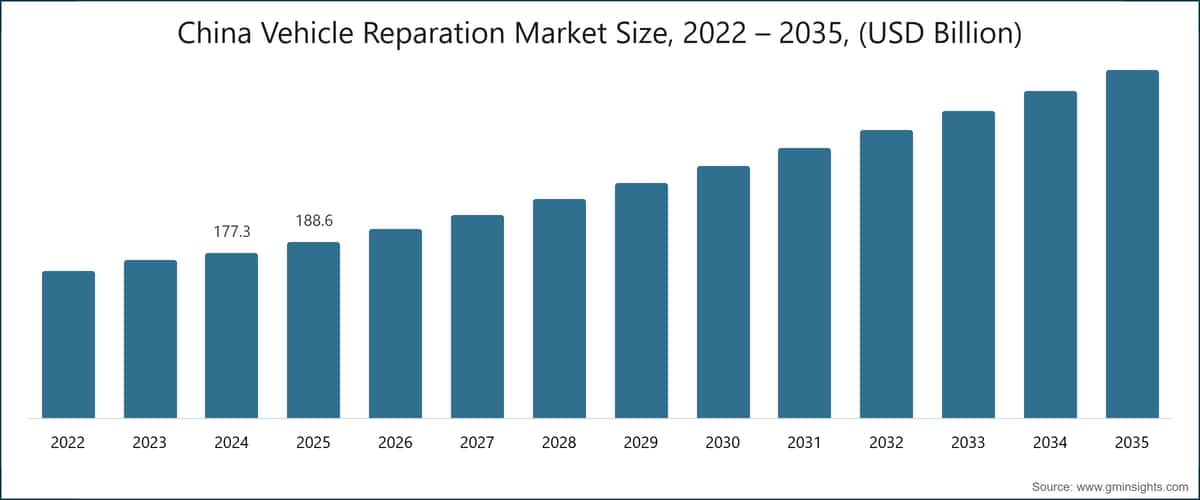

The Asia Pacific market was the largest regional market in 2025, generating USD 293.65 billion and holding 46.8% of global revenue. China alone accounted for USD 188.6 billion in base-year revenue at a 7% CAGR, supported by more than 300 million registered vehicles and a repair base that includes OEM networks, digital platforms such as Bitauto, and extensive independent operators. Ministry of Commerce data and national vehicle-market indicators support China's role as the region's repair demand anchor. India is a core growth market, with organized providers such as MyTVS expanding multi-brand service centers across more than 100 cities and moving into certified inspection and repair partnerships. The Rest of APAC is projected to grow at an 8.1% CAGR, with Japan, South Korea, Australia, Vietnam, Indonesia, and Thailand contributing demand through older fleets, two-wheeler service needs, and formalization of repair channels.

Latin America and Middle East & Africa remain smaller but strategically relevant. Latin America generated USD 25.37 billion in 2025, with Brazil contributing USD 8.5 billion. MEA generated USD 22.09 billion, with the UAE at USD 7.4 billion and Saudi Arabia emerging through vehicle ownership growth and Vision 2030 infrastructure investment.

Vehicle Reparation Market Share

The market is highly fragmented, with the top five players collectively holding approximately 4.2% of global revenue in 2025. Belron International led with an estimated 1.2% share, followed by Driven Brands Holdings at 0.9%, Caliber Collision at 0.8%, Fix Network World at 0.7%, and Penske Automotive Group at 0.6%. The remaining 95.8% of revenue is distributed across thousands of independent repair shops, dealer service departments, franchise chains, specialty providers, mobile mechanics, and regional networks.

This fragmentation is structural. Vehicle repair remains a local service category where proximity, trust, technician availability, parts access, insurer referral status, and brand familiarity often matter more than national scale. Independent shops remain essential because they serve older vehicles, price-sensitive customers, and post-warranty repair events. Dealer networks retain strength in warranty, software, recalls, OEM parts, and EV-certified work. Franchise chains and specialty providers occupy the middle ground, using process standardization and certification to compete for insurer, fleet, and consumer demand.

Conversations with 22 insurance network managers during our Q2 2026 claims-repair expert panel across the United States, Canada, the U.K., and Germany pointed to a consistent procurement shift. Insurers are placing greater weight on cycle time, calibration documentation, supplement control, parts availability, and OEM certification before assigning high-value collision work. That shift favors scaled collision groups such as Caliber Collision, Fix Network World, Crash Champions, and Driven Brands' CARSTAR network. It also creates pressure on smaller body shops to invest in calibration documentation and insurer-compatible workflow systems.

Competitive strategies are converging around four priorities. The first is acquisition-led expansion, visible in Driven Brands' continued CARSTAR footprint growth and Crash Champions' financing-backed national expansion strategy. The second is technology investment, including Belron's AI damage assessment deployment and Ayvens' predictive fleet maintenance platform. The third is EV and ADAS certification, illustrated by Caliber Collision's GM partnership and Fix Network World's ADAS calibration certification program. The fourth is emerging-market formalization, where MyTVS, Carro, CFAO, Jameel Motors, and Al-Futtaim Automotive are positioned to capture organized repair demand as vehicle ownership expands.

M&A activity should remain active because repair cash flows are recurring and less cyclical than vehicle sales. Private equity participation, including institutional backing for collision repair networks, reflects that thesis. Still, global consolidation will be slow. A 4.2% top-five share means even aggressive acquisition programs will create stronger regional champions before they create global control.

Vehicle Reparation Market Companies

Arval (BNP Paribas) operates as a fleet management and leasing company with maintenance and repair programs across more than 30 countries. Its competitive position comes from integrated fleet contracts, telematics-enabled maintenance planning, and the financial strength of BNP Paribas.

Belron International is the leading vehicle glass repair and replacement specialist, operating brands such as Autoglass, Safelite AutoGlass, Carglass, and O'Brien across more than 35 countries. The company processes high-volume glass jobs and uses insurer integration, mobile service routes, technician training, and AI-assisted damage assessment as differentiators.

Driven Brands operates one of North America's largest automotive services franchise networks, including Meineke, Maaco, Take 5 Oil Change, and CARSTAR. Its model combines recurring maintenance, collision repair, paint services, and acquisition-led expansion.

Inchcape is an international automotive distributor and retailer with aftersales services across more than 40 markets. OEM parts access, certified technician training, and premium vehicle representation support its repair economics.

Jameel Motors is an important automotive distributor and aftersales provider across the Middle East, North Africa, and South Asia. Its Toyota and Lexus relationships in Saudi Arabia and other markets anchor authorized service demand in the Gulf.

Penske Automotive operates over 300 franchised dealerships and service operations across the U.S., U.K., Germany, Australia, and Japan. Service and parts revenue is a high-margin business line that helps offset cyclicality in vehicle sales.

AutoNation is the largest automotive retailer in the United States and is expanding repair reach through dealership service departments and AutoNation Mobile Service. Its January 2025 expansion to more than 2,000 technician vans across 35 U.S. metropolitan areas shows how dealer groups are using mobile repair to retain aftersales customers.

Caliber Collision operates approximately 1,800 repair centers across 42 U.S. states. Its insurer relationships, OEM certification programs, and November 2025 partnership with General Motors for EV collision repair give it a strong position in complex collision work.

Kwik Fit operates more than 600 fast-fit service centers across the U.K. and Europe, focusing on tires, exhausts, brakes, and MOT testing. Its May 2025 pilot of 50 EV fast-fit centers with Volkswagen Group reflects a shift toward EV-specific maintenance categories.

MyTVS is a leading organized repair brand in India, with multi-brand service centers across more than 100 cities. Its January 2026 expansion to 250 centers and partnership with Maruti Suzuki strengthen its position in India's transition from informal to organized repair.

1.2% Market Share

Collective Market Share is 4.2%

Vehicle Reparation Industry News

Market Concentration Score

The vehicle reparation market scores 2 out of 10 for concentration because the top five players held only 4.2% of global revenue in 2025, leaving 95.8% of the market with independents, dealerships, franchise chains, specialty shops, and regional operators.

The Vehicle Reparation Market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Service Type

Market, By Vehicle

Market, By Propulsion

Market, By Vehicle Age

Market, By Payment Source

Market, By Service Provider

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Service Type, 2022 - 2035 ($Mn)

Chapter 6 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

Chapter 7 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

Chapter 8 Market Estimates & Forecast, By Vehicle Age, 2022 - 2035 ($Mn)

Chapter 9 Market Estimates & Forecast, By Payment Source, 2022 - 2035 ($Mn)

Chapter 10 Market Estimates & Forecast, By Service Provider, 2022 - 2035 ($Mn)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

Chapter 12 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →