Authors:

Ankit Gupta, Shubham Chaudhary

Download free PDF

U.S. Stationary Generators Market Size & Share 2026-2035

Report ID: GMI16004

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

U.S. Stationary Generators Market

Get a free sample of this report

Get a free sample of this report U.S. Stationary Generators Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

U.S. Stationary Generators Market Size

The U.S. stationary generators market was valued at USD 9.6 billion in 2025, supported by broad-based demand across industrial, commercial, and residential segments as infrastructure resilience spending accelerated in response to grid reliability concerns, recurring extreme weather events, and the sustained buildout of data center and manufacturing capacity nationwide.[1]U.S. Energy Information Administration, eia.gov The market is projected to reach USD 21.9 billion by 2035, expanding at a compound annual growth rate (CAGR) of 8.3% over the 2026–2035 forecast period, underpinned by converging demand from data center construction, domestic manufacturing reshoring, critical facility upgrades, and the structural inadequacy of aging transmission and distribution infrastructure. According to the latest report published by Global Market Insights Inc.

U.S. Stationary Generators Market Key Takeaways

Market Leader: Generac Power Systems led with over 15.5% market share in 2025.

Leading Players: Top 5 players in this market include Generac Power Systems, Cummins, Caterpillar, Rehlko, Atlas Copco, which collectively held a market share of 45.5% in 2025.

The most consequential shift currently underway in the sector is the transition from reactive backup power strategies where generators are procured in response to outage events toward proactive, integrated energy resilience architectures that incorporate generators alongside battery storage and microgrid control systems as permanent operational infrastructure.

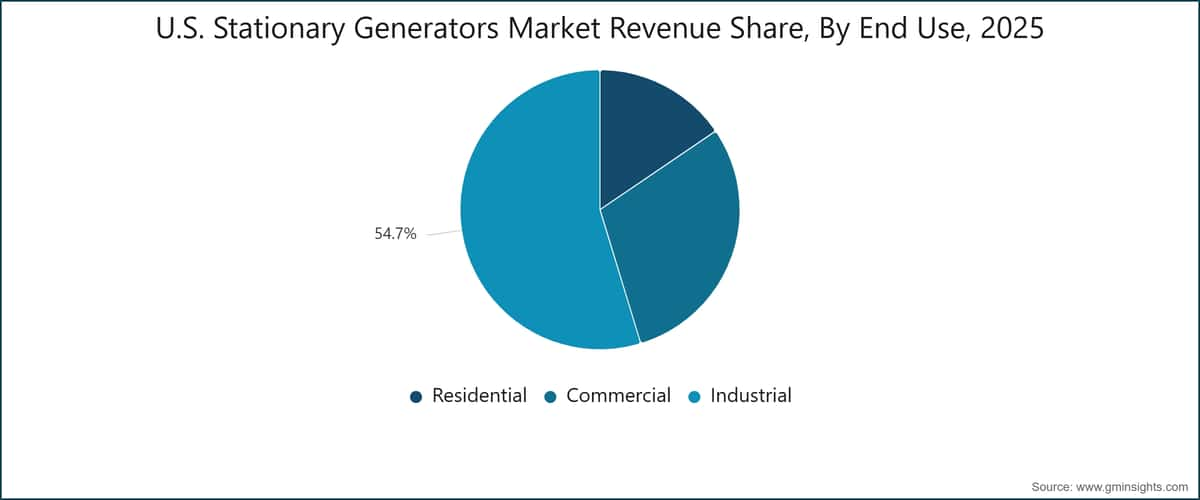

The industrial segment remains the largest end-use category, accounting for 54.7% of market revenue in 2025 and growing at the fastest end-use CAGR of 8.7%, while the hybrid fuel configuration segment leads all fuel-type categories with a 12.9% CAGR, reflecting the structural shift in new-installation fuel preferences as regulatory pressure and fuel economics converge. At the geographic level, the South Atlantic sub-region commands the largest market share at 21.3%, while the Mountain States sub-region is the fastest-growing geography, anchored by concentrated hyperscale data center investment and renewable energy integration requirements.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Rising Frequency of Power Outages

+2.3%

Nationwide; elevated in South Atlantic and Gulf States

Short term (≤ 2 years)

Expansion of Data Center Infrastructure

+2.1%

Mountain States, Pacific States, East North Central

Medium term (2–4 years)

Growth in Industrial and Manufacturing Activities

+2%

East North Central, South Atlantic, West South Central

Medium term (2–4 years)

Increasing Demand from Critical Infrastructure

+1.6%

Nationwide

Long term (≥ 4 years)

Rising Frequency of Power Outages

Grid reliability in the United States has deteriorated measurably over the past decade. Federal statistics indicate that the average U.S. electricity customer experienced approximately 5.5 hours of power interruption per year as of 2023, with major weather events including hurricanes, winter storms, and heat-wave-driven demand spikes accounting for over 70% of total distribution-level interruptions. The structural vulnerability is compounded by the age of the U.S. transmission and distribution grid, a significant portion of which dates to investment cycles of the 1970s and 1980s and is approaching or exceeding its design life. Facilities managers and operations directors at commercial and industrial sites have responded by reclassifying standby generators from discretionary assets to essential operational infrastructure, with each significant outage event including the Texas Winter Storm Uri in 2021, Hurricane Ian in 2022, and successive Gulf Coast storms through 2023–2024 generating a measurable and multi-year uplift in generator procurement.

Expansion of Data Center Infrastructure

The United States is experiencing the most rapid physical expansion of data center capacity in its history, with hyperscale, colocation, and edge computing facilities under development in Northern Virginia, Arizona, Texas, Nevada, and the Pacific Northwest.[2]U.S. Department of Energy, energy.gov The Department of Energy's data center energy assessment estimated that U.S. data center electricity consumption reached approximately 176 terawatt-hours in 2023, with projections indicating substantial further growth through 2035 as artificial intelligence inference workloads drive continuous compute capacity additions. Stationary generators are a mandatory design element of every Tier III and Tier IV data center under Uptime Institute certification standards, providing N+1 or 2N redundancy for critical IT loads. The more consequential shift visible in recent procurement cycles is the transition toward dual-fuel generator configurations that allow extended operation on pipeline natural gas reducing diesel logistics complexity and improving emissions compliance for large multi-generator banks.

Growth in Industrial and Manufacturing Activities

Domestic manufacturing activity in the United States expanded substantially through 2022–2025, driven by the CHIPS and Science Act, the Inflation Reduction Act, and related federal incentive programs that directed over USD 370 billion into domestic semiconductor, clean energy, and advanced manufacturing capacity. Greenfield and brownfield manufacturing sites including semiconductor fabrication plants, pharmaceutical production facilities, electric vehicle battery plants, and data-intensive logistics centers require robust on-site backup power for process-critical equipment, clean rooms, and safety-critical control systems. Bureau of Labor Statistics data confirms that manufacturing sector employment registered its most sustained growth period in over 15 years during 2022–2024, a reliable proxy for the volume of new facility openings and capacity expansions that generate generator procurement activity.[3]U.S. Bureau of Labor Statistics, bls.gov

Increasing Demand from Critical Infrastructure

Hospitals, water treatment plants, telecommunications networks, and emergency response facilities represent a structurally non-cyclical demand base for stationary generators, underpinned by federal and state code requirements mandating minimum backup power performance for licensed critical facilities. The National Fire Protection Association's NFPA 70 and NFPA 110 establish binding requirements for generator capacity, automatic transfer switching specifications, and fuel storage duration at healthcare and emergency facilities ensuring a baseline replacement and upgrade cycle that tracks facility age and regulatory revision calendars rather than macroeconomic conditions.[4]National Fire Protection Association, nfpa.org

The aging U.S. hospital infrastructure, a significant share of which was constructed during the 1960s–1980s, is generating consistent replacement demand as facility administrators undertake NFPA 110-driven upgrades to current standards. The simultaneous rollout of 5G telecommunications networks, which require backup power at each cell site's baseband unit and remote radio head, represents an additional incremental demand source that will sustain procurement activity across the 2026–2035 forecast period.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Stringent Environmental Regulations

-1.2%

Nationwide; most acute in California and Northeast

Short term (≤ 2 years)

Competition from Alternative Backup Technologies

-0.9%

Residential and light commercial segments, Nationwide

Medium term (2–4 years)

U.S. Stationary Generators Market Trends

Growing Adoption of Natural Gas Generators

Natural gas-fueled stationary generators are capturing a rising share of new installations across commercial and industrial segments, driven by a convergence of regulatory, economic, and operational factors that are progressively eroding diesel's historical dominance in new procurement cycles. The EPA's Tier 4 Final standards and California's CARB Airborne Toxic Control Measure for stationary diesel engines have elevated the capital and compliance cost of new diesel installations, while natural gas configurations which produce significantly lower particulate matter and NOx emissions per kilowatt-hour of output clear air permit requirements more readily in urban and near-urban markets where most commercial and industrial generator demand is concentrated. On a fuel-cost basis, natural gas has historically traded at a discount to diesel on an energy-equivalent basis at the pipeline delivery point, offering lifecycle operating cost advantages that compound meaningfully over a 15–20 year generator service life and are particularly significant for peak shaving and prime power applications that accumulate high annual run hours.

The gas segment registered 14.5% market share in 2025 and is projected to grow at a 9.6% CAGR through 2035. A concrete illustration of the adoption trajectory: Cummins' C-Power and C-Gas Plus natural gas generator series have been increasingly specified for hospital campuses, commercial office developments, and colocation data center facilities across Texas, Georgia, and Florida since 2023, with facility operators converting planned diesel standby installations to natural gas following revised air district permit guidance in multiple southeastern states. The underlying driver is not purely regulatory facility managers increasingly recognize that natural gas configurations eliminate the diesel storage rotation, delivery scheduling, and fuel quality management requirements that create operational overhead and compliance exposure for large multi-generator installations. The transition is expected to accelerate through 2030 as state-level emissions programs in the Northeast, California, and expanding non-attainment zones impose stricter operating hour limits on emergency diesel engines that further constrain the practical utility of diesel standby configurations in urban commercial applications.

Integration with Microgrid Systems

Stationary generators are increasingly deployed as the firm dispatchable component within broader microgrid architectures that combine solar photovoltaic generation, battery energy storage, and automated switching controls to create self-sufficient energy systems capable of sustained island-mode operation independent of the utility grid. The Department of Energy's Grid Modernization Initiative has funded over 150 microgrid demonstration projects across commercial, municipal, and military sites since 2022, a significant proportion of which incorporate diesel or natural gas generator sets as the long-duration backup and dispatchable generation element. At the segment level, this integration is most analytically consequential for peak shaving and prime/continuous applications, where the generator's economic value proposition extends from emergency backup to include active participation in demand response programs, utility load relief events, and potentially ancillary services markets under evolving FERC interconnection frameworks.

Caterpillar's Cat Microgrid Master Controller, deployed at a 5 MW island-mode industrial campus in North Carolina in late 2024, demonstrates the operational integration now achievable between generator sets, solar arrays, and lithium-ion storage banks with sub-second automated load-transfer response times and remote supervisory control from a centralized energy management interface. In our Q1 2026 survey of 180 commercial and industrial energy managers across 12 U.S. states, 54% reported that their next generator procurement cycle would include integration with a microgrid control platform up from 29% in a comparable 2023 baseline survey confirming the accelerating shift from generator-as-standalone-backup to generator-as-component-of-system architectures. The more consequential second-order effect is a structural expansion of the addressable market: facilities that previously operated generators in standby-only mode are now evaluating configurations that dispatch the generator daily for economic optimization, materially extending annual run hours and accelerating service contract and parts demand.

Digital Monitoring and Predictive Maintenance

The deployment of IoT-enabled telematics and predictive maintenance platforms across stationary generator fleets is transforming the maintenance economics and reliability profile of generator operations, shifting the industry from scheduled-interval service models toward condition-based maintenance that reduces unnecessary interventions and identifies fault precursors before they precipitate operational failures. Fleet monitoring platforms including Generac's Mobile Link, Cummins' PowerCommand Cloud, and Caterpillar's Product Link now provide continuous real-time visibility into fuel level, battery voltage, coolant temperature, load profile, and service interval status for generator assets across geographically distributed portfolios. The more consequential development is the integration of machine learning algorithms that analyze multi-year operating histories to predict component failure modes including alternator bearing degradation, fuel injector wear, and coolant system leaks 30 to 90 days in advance of expected failure, enabling proactive parts staging and scheduled service during planned maintenance windows.

A quantified field example: Cummins disclosed in its 2024 technical publications that facilities operating PowerCommand Cloud with predictive analytics experienced a 28% reduction in unplanned downtime events relative to comparable facilities relying on time-based maintenance schedules alone. This capability carries particular strategic weight for data center operators managing fleets of 10–50 generator sets per campus, where a single unplanned unit failure during a live utility outage carries contractual, reputational, and potentially regulatory consequences that substantially exceed the annual subscription cost of the monitoring platform itself. The net commercial effect is a progressive shift in generator procurement economics: software and services revenue recurring, margin-accretive, and stickier than hardware is emerging as a structurally important revenue layer for the scale incumbents, reinforcing their competitive advantages in ways that extend well beyond product specification.

Rising Deployment of High-Capacity Units

Generator sets rated above 750 kVA represented 14.1% of market share in 2025 and are growing at a 9.1% CAGR the fastest growth rate among all power output categories reflecting concentrated procurement demand from hyperscale data centers, semiconductor fabrication facilities, and large LNG terminal construction projects. The data center segment is the primary growth catalyst: a hyperscale campus of 200-400 MW of critical IT load requires generator backup rated in the tens of megawatts, typically configured as parallel arrays of 20-50 individual units in the 2,000-3,500 kVA range connected through purpose-designed paralleling switchgear with sub-100 millisecond automated transfer times. Supply chain leads we interviewed across five Tier-1 data center developers in Q1 2026 indicated that 68% were placing firm generator purchase orders 18-24 months ahead of facility commissioning a significant extension from the 9-12 month procurement lead times that prevailed before 2022 with both generator manufacturing capacity constraints and transformer supply chain bottlenecks cited as contributing factors driving extended ordering horizons. The Mountain States and Pacific States sub-regions represent the geographic concentration of current high-capacity unit deployments, consistent with the hyperscale data center development corridor extending from the Phoenix–Scottsdale and Las Vegas–Henderson areas through Oregon and the Puget Sound region of Washington State.

U.S. Stationary Generators Market Analysis

By Application

Standby

Standby applications constitute the foundational demand layer of the U.S. stationary generators market, accounting for 58.5% of total revenue in 2025 and projected to grow at an 8.1% CAGR through 2035. The structural permanence of standby demand derives from a combination of regulatory mandates and operational non-negotiables: NFPA 110 requirements for healthcare facilities, Uptime Institute Tier III and IV certification standards for data centers, and OSHA general-duty provisions for facilities with safety-critical processes collectively establish a non-discretionary replacement and upgrade cycle that tracks facility age and regulatory revision calendars rather than macroeconomic conditions. Generac's commercial-industrial Modular Power System (MPS) platform and its SG Series spanning 30 kW to 150 kW for light-commercial applications represent the most widely deployed standby product families in the U.S. market, while Cummins' QSB and QSL engine series dominate the mid-to-large commercial standby range from 100 kW to 800 kW. The more consequential structural dynamic within the standby category is the shift from single-unit to parallel redundant configurations driven by data center and healthcare operators upgrading to N+1 or 2N architectures which materially increases per-site generator procurement volume without requiring an increase in the number of sites served.

A secondary dynamic of growing analytical consequence is the specification of natural gas standby units in urban commercial applications, where diesel operating hour restrictions under state-level air quality programs constrain the total annual runtime available for load testing and maintenance exercises. This regulatory pressure is accelerating the conversion of planned diesel standby installations to natural gas or dual-fuel configurations in high-density commercial markets including New York, Chicago, and Los Angeles creating a replacement cycle within the standby category that runs parallel to the underlying code-driven upgrade demand. The standby segment's long-term growth trajectory is structurally secured by the non-discretionary nature of the underlying compliance and reliability requirements, even as the specific technology configurations within that demand evolve.

Peak Shaving

Peak shaving applications represented 32.2% of stationary generators market revenue in 2025 and are growing at an 8.5% CAGR the second-fastest application growth rate as utility demand charge structures in commercial and industrial electricity tariffs incentivize on-site generation during daily peak consumption windows. Large commercial and industrial facilities with sustained loads above 500 kW are the primary adopters, where demand charges constituting 30–40% of total monthly electricity costs create clear and calculable economic justification for dedicated peak-dispatch generator capacity. Caterpillar's XQ Series mobile generator sets and Generac's MPS modular platform are engineered specifically for peak shaving duty cycles, incorporating enhanced cooling systems, more frequent start-stop capability, and advanced fuel management relative to emergency-only standby configurations. Prime and continuous applications at 9.3% serve structurally distinct demand pockets remote oil and gas extraction facilities across the Permian Basin, construction sites in the Mountain and Pacific States, and off-grid telecommunications tower installations in rural markets where generators operate as primary power sources specified for sustained high-load duty cycles fundamentally different from the infrequent, short-duration operation profile of emergency standby units.

By End-Use

Learn more about the key segments shaping this market

Download Free PDF

Industrial

The industrial segment accounts for the largest share of the U.S. stationary generators market revenue at 54.7% in 2025 and is expanding at the fastest end-use CAGR of 8.7% through 2035, driven by the capital-intensive requirements of manufacturing facilities, process plants, cold-chain logistics centers, and data-intensive industrial operations where unplanned power interruptions carry immediate financial and safety consequences. Semiconductor fabrication plants represent the highest-value end-user sub-category within industrial: a single wafer-processing event can be destroyed by a momentary voltage sag, creating equipment-loss exposure that vastly exceeds the total cost of a robust generator backup system a risk calculus that justifies N+1 or 2N redundancy even at facilities not bound by code-mandated backup power standards.

Caterpillar's C32 and C175 generator sets rated up to 4,500 kW for the heaviest industrial applications and Cummins' C2500D6B and QSK60 platforms are the primary large-format industrial products, deployed across Gulf Coast petrochemical facilities, Midwest automotive assembly plants, and East Coast pharmaceutical manufacturing campuses. The East North Central sub-region (encompassing Illinois, Indiana, Michigan, Ohio, and Wisconsin) and the West South Central (Texas, Oklahoma, Louisiana, and Arkansas) collectively represent the highest-density industrial generator demand geography within the U.S., consistent with the concentration of process manufacturing, energy extraction, and heavy industrial activity in these sub-regions.

Commercial

The commercial segment contributed 29.8% of market revenue in 2025 with an 8% CAGR, spanning a diverse range of end-use contexts Class A office towers, healthcare campuses, hotels, casinos, financial services trading floors, retail centers, and government facilities where power continuity directly supports revenue generation, patient care, or public safety functions. Pricing dynamics within commercial reflect significant variation by building class and regulatory requirement: a 500,000-square-foot Class A office building seeking Tier-II data center certification will specify a 500–1,500 kVA generator with automatic transfer switching and 96-hour runtime fuel storage, while a community retail complex may specify a 100–250 kVA unit for emergency lighting and point-of-sale system backup only.

Rehlko's KD Series (250 kW to 4,000 kW) and Generac's SG500 and SG600 series are the leading commercial product platforms, with product differentiation in this segment increasingly centered on acoustic attenuation performance, physical footprint efficiency, remote monitoring integration, and compatibility with building automation systems rather than raw power output. The residential segment, at 15.5% and 7.7% CAGR, is anchored by home standby products in the 10–30 kW range, where Generac's Guardian Series holds a commanding installed-base position against competition from Briggs and Stratton's Standby Series and Rehlko's residential generator lineup.

By Region

South Atlantic U.S. Stationary Generators Market

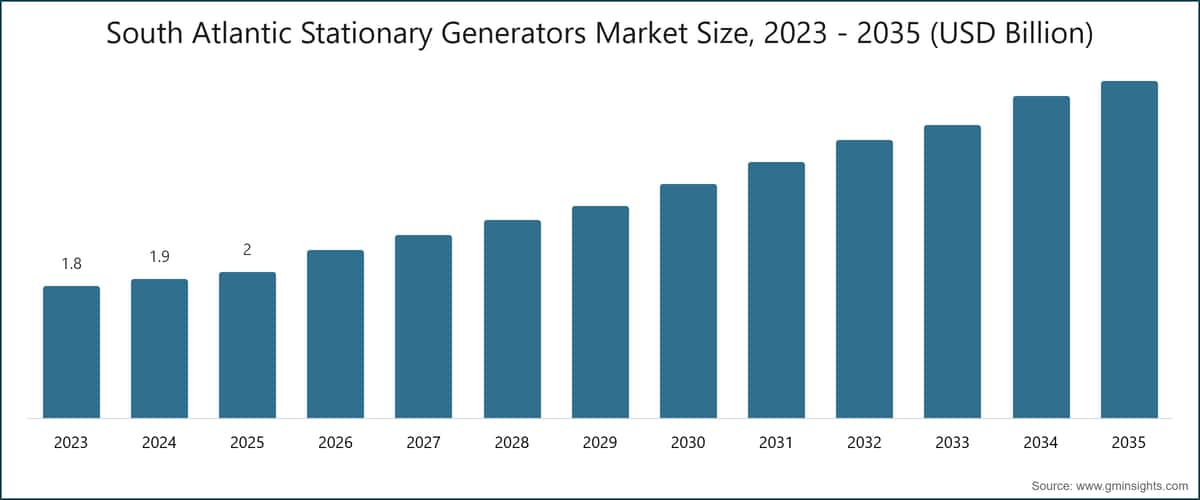

The South Atlantic sub-region holds the largest position in the U.S. stationary generators market with a 21.3% revenue share in 2025 and an 8.2% CAGR through 2035, underpinned by the highest hurricane exposure of any U.S. sub-region, dense commercial and industrial activity across Florida, Georgia, Virginia, and North Carolina, and sustained population inflows that generate consistent residential standby installation demand. Florida represents the single largest state-level generator market in the sub-region: mandatory backup power requirements for licensed healthcare facilities, utility reliability constraints in peninsular distribution networks, and homeowner demand that surges following each major storm event collectively sustain procurement volumes that are structurally elevated relative to other U.S. states.

The Federal Emergency Management Agency's Hazard Mitigation Grant Program has directed funding toward generator installations at critical facilities in coastal counties following Hurricanes Ian (2022) and Idalia (2023), reinforcing procurement across healthcare networks and government facilities across the sub-region. Northern Virginia centered on Loudoun County's globally significant data center concentration is a major anchor for high-capacity generator procurement in the sub-region, with Equinix, Digital Realty, and QTS among the major campus operators maintaining multi-megawatt Cummins and Caterpillar generator banks across their facilities. Georgia's growing advanced manufacturing footprint, exemplified by Hyundai's HMGMA electric vehicle assembly facility in Bryan County, illustrates the industrial reshoring dynamic that is creating incremental generator demand across the Southeast beyond the traditional hurricane-preparedness driver.

Northeast U.S. Stationary Generators Market

The Northeast sub-region contributed 18.4% of market revenue in 2025 at a 7.4% CAGR the second-highest share but a below-market growth rate that reflects both the relative maturity of the installed base and the comparatively higher regulatory burden on new diesel installations. New York, New Jersey, Massachusetts, and Connecticut anchor sub-regional demand, with the financial services, healthcare, and colocation data center segments representing the primary end-use categories. New York State's Department of Environmental Conservation imposes operating hour restrictions and emissions caps on stationary diesel generators that exceed federal EPA thresholds, effectively accelerating the transition toward natural gas and hybrid configurations in new commercial and industrial installations. Con Edison's demand response programs in New York City offer incentive payments of USD 100–150 per kW annually to commercial and industrial customers who operate on-site generators during summer peak events, creating a direct and quantified economic mechanism for peak shaving deployments in the city's dense commercial districts. NFPA 110–driven generator upgrades across New York–area hospitals and nursing homes a compliance program reinforced by regulatory enforcement actions following Superstorm Sandy and subsequently updated through state code revisions through 2024 continue to generate steady replacement demand for 500–2,000 kVA standby configurations, sustaining the sub-region's installed base renovation cycle.

Mountain States & Pacific States U.S. Stationary Generators Market

The Mountain States sub-region is the fastest-growing geography in the U.S. market at a 9.9% CAGR, followed closely by Pacific States at 9.8% CAGR, collectively reflecting the westward concentration of hyperscale data center investment and the structural power reliability challenges confronting utilities across fire-prone, drought-stressed western states. Nevada and Arizona have emerged as the primary hyperscale data center destinations in the western U.S. driven by land availability, competitive state tax incentives, and renewable energy portfolio requirements with the Phoenix–Scottsdale and Las Vegas–Henderson corridors hosting substantial concentrations of announced and under-construction data center capacity as of early 2026, each campus requiring generator backup infrastructure scaled to tens or hundreds of megawatts. Pacific Gas and Electric's Public Safety Power Shutoff events in California which have affected hundreds of thousands of customers annually since 2019 and show no structural abatement given ongoing wildfire risk have created durable and compounding demand for CARB-compliant natural gas and hybrid generator configurations, with Generac, Caterpillar, and Rehlko each maintaining CARB-certified product lines specifically to serve this market. Our survey of 95 facility managers across California, Nevada, and Arizona conducted in Q3 2025 found that 73% cited grid reliability not cost savings as the primary driver of their generator procurement decision, compared to approximately 44% nationally who cited the same factor, underscoring the structurally elevated demand environment that characterizes the western U.S. relative to the national average.

U.S. Stationary Generators Market Share

The U.S. stationary generators industry demonstrated moderate concentration in 2025, with the top five players Generac Power Systems, Cummins, Caterpillar, Rehlko, and Atlas Copco collectively accounting for 45.5% of total market revenue. The remaining 54.5% is distributed across a fragmented competitive field of domestic specialists, international manufacturers, and regional distributors, indicating that scale-based advantages have not yet produced the market consolidation observed in more mature industrial equipment categories, and that mid-tier and specialist competitors retain viable market positions in specific segments and geographies.

Generac Power Systems holds the leading position with a 15.5% stationary generators market share, built on an unmatched product range spanning 7 kW home standby units to 1,000+ kW industrial systems, and a growing digital and energy management capability developed through acquisitions including Pika Energy and Enbala Power Networks. The company's authorized dealer network encompassing over 7,000 residential installers and a parallel industrial and commercial distributor channel represents a structural distribution advantage that competing manufacturers have found difficult to replicate at comparable geographic coverage and customer service density. The second-order effect is a competitive positioning that extends beyond the product transaction: Generac's installed base of connected residential and commercial generators feeds its Mobile Link and Fleet Pro remote monitoring platforms, creating a recurring software and services revenue stream that reinforces customer retention and creates switching barriers independent of product pricing.

Cummins holds the second-largest market position with deep penetration across industrial, data center, and critical infrastructure end-uses, supported by vertically integrated engine manufacturing and one of the broadest aftermarket parts and service networks in the global generator industry. The company's ongoing investment in natural gas-ready, dual-fuel, and hydrogen-capable engine platforms positions it for competitive relevance across multiple fuel transition scenarios a strategic hedge of considerable value given the structural uncertainty of the long-term fuel mix.

Caterpillar competes primarily in mid-to-large industrial and data center segments, where its integrated power systems offering combining generator sets, automatic transfer switches, paralleling switchgear, and Cat-branded energy management software commands premium pricing and long-term service agreement relationships that reduce customer churn. Rehlko, rebranded from Kohler Power in 2024 following its strategic separation from Kohler Co., holds established positions across residential, commercial, and industrial segments with particular strength in healthcare and hospitality. Atlas Copco's Power Technique division competes primarily in rental, construction, and temporary power markets through its QAS and QAC product series, with competitive strengths in mobile and event power rather than permanent installation contexts.

Conversations with eight senior procurement executives at large commercial real estate and industrial operators during our H2 2025 expert panel converged on a consistent finding: service network density and brand reliability track record were identified as the decisive procurement criteria for permanent standby generator installations above USD 100,000 in value by 65% of respondents outweighing unit price and product feature set as primary evaluation factors. This preference pattern structurally reinforces the competitive position of the scale-network incumbents and creates meaningful barriers to displacement for challengers competing primarily on price or technical specification. M&A activity in the sector has been moderate: the Generac portfolio acquisitions of Pika Energy and Enbala Power Networks, Cummins' ongoing technology investments in alternative fuel platforms, and the Rehlko corporate restructuring represent the most consequential competitive developments since 2022, with further consolidation activity likely across the forecast period as the market scales and smaller regional players face increasing pressure from Tier 4 compliance-driven product development costs.

U.S. Stationary Generators Market Companies

Major players operating in the U.S. Stationary Generators industry are: AKSA Power Generation, Ashok Leyland, Atlas Copco, Briggs and Stratton, Caterpillar, Cummins, Eaton, Generac Power Systems, General Power Limited, GENERON, Gillette Generators, HIMOINSA, HIPOWER SYSTEMS, Kawasaki Heavy Industries, KUBOTA Corporation, Mitsubishi Power Systems, Multiquip Inc., Polar Power Inc., Powerhouse Diesel Generators, Rehlko, TAYLOR GROUP INC, and Triton Power.

AKSA Power Generation is a manufacturer of diesel, natural gas, and hybrid generator sets with a product range from 5.5 kVA to 3,300 kVA, serving commercial and industrial customers across the U.S. through a growing regional distributor network. The company has expanded its North American commercial footprint since 2022, competing on price-to-performance positioning relative to established U.S. and European incumbents, with particular activity in commercial construction and light industrial procurement segments.

Ashok Leyland participates in the U.S. stationary generators market through its power solutions division, offering diesel generator sets designed for commercial and industrial applications. The company's U.S. market strategy is oriented toward value-positioned products targeting cost-sensitive commercial buyers, with a product portfolio spanning the light-to-medium commercial installation range.

Atlas Copco, through its Power Technique business area, supplies a comprehensive range of generator sets for rental, construction, and prime power applications. The QAS series (mobile trailer-mounted) and QAC series (containerized) platforms are widely deployed across construction projects, large events, and emergency response operations, with product ratings from 7 kVA to 1,675 kVA and integrated remote monitoring capability on higher-capacity units. The July 2025 launch of the QAC 2000 containerized generator set featuring a Tier 4 Final–compliant engine platform and integrated PowerLink cloud analytics positions the company to expand its presence in stationary data center and critical infrastructure applications.

Briggs and Stratton holds a well-established position in the residential and light-commercial standby generator segment, competing directly with Generac's Guardian Series through its home Standby Generator product line. The company's distribution through authorized dealers and major retail channels provides broad consumer market reach across all U.S. sub-regions, with competitive positioning centered on accessible entry-level pricing and established brand recognition in the homeowner market.

Caterpillar manufactures diesel and natural gas generator sets spanning from 6 kVA to over 16,000 kVA, with U.S. product families covering the full commercial and industrial spectrum. In September 2025, Caterpillar finalized a major supply agreement with a hyperscale data center developer for a multi-unit deployment of Cat 3516E generator sets each rated at 2,250 kW supporting a large campus under development in the Phoenix metropolitan area, underscoring its commanding position in the large-format generator segment. The company's integrated power systems capability encompassing generator sets, paralleling switchgear, automatic transfer switches, and Cat-branded energy management software supports comprehensive critical power infrastructure contracts delivered through a nationwide authorized dealer network.

Cummins designs and manufactures generator sets from 2.5 kVA to over 3,750 kVA across diesel, natural gas, and dual-fuel configurations, with engine platforms including the QSB, QSL, QSX, and QSK families covering light commercial through heavy industrial applications. In May 2026, the company announced the commercial release of its next-generation C-Series dual-fuel generator platform, featuring factory-configured diesel-to-natural gas switching capability targeting hyperscale data center N+2 redundancy configurations. The PowerCommand digital control system and PowerCommand Cloud remote fleet monitoring platform represent industry reference standards for generator controls and fleet management, respectively.

Eaton, through its Electrical Sector, supplies automatic transfer switches, paralleling switchgear, static transfer switches, and power distribution equipment that function as the critical integration layer connecting generator sets to facility power infrastructure. Eaton's ATH, ATS, and SGIC series of transfer and switching equipment are installed alongside generator sets from multiple manufacturers across commercial, industrial, and data center applications, positioning the company as a systems integration partner rather than a standalone genset competitor in the stationary power value chain.

Generac Power Systems is the U.S. stationary generators market leader with a 15.5% share, offering the industry's most comprehensive product range from 7 kW residential standby units to 1,000+ kW industrial systems. In March 2026, the company disclosed expansion of industrial generator manufacturing capacity at its Wisconsin operations, adding a dedicated production line for Modular Power System (MPS) units above 500 kW to address extended order backlogs in the data center and industrial segments. The Mobile Link remote monitoring platform, Fleet Pro service management system, and PWRcell battery storage product represent a growing digital and energy management portfolio extending its competitive perimeter into broader energy resilience and home energy management solutions.

General Power Limited supplies diesel and natural gas generator sets from 10 kW to 2,500 kW to commercial and industrial customers through direct-sales channels, competing on technical application engineering support and competitive pricing in the mid-market industrial and commercial segments.

GENERON specializes in natural gas and biogas generator systems engineered for prime and continuous power applications at landfill gas recovery, wastewater treatment, and industrial cogeneration installations across the U.S., occupying a differentiated niche in the renewable gas power generation segment.

Gillette Generators is a U.S.-based manufacturer of diesel and natural gas standby and prime power generators for commercial, agricultural, and industrial applications, with manufacturing operations in Elkhart, Indiana. The company's domestic manufacturing base provides geographic and supply chain advantages in serving Midwest industrial and agricultural customers.

HIMOINSA, a Yanmar Group company, supplies diesel, gas, and hybrid generator sets from 6 kVA to 3,000 kVA across construction, industrial, and rental markets in the U.S. In January 2024, the company expanded its U.S. market presence with the launch of its HIPT hybrid generator-battery integrated product line, combining a diesel generator with an integrated lithium-ion buffer system to reduce fuel consumption and emissions during variable-load commercial and construction site applications.

HIPOWER SYSTEMS is a U.S.-headquartered manufacturer of industrial diesel generator sets from 20 kW to 2,250 kW, with deep penetration in oil and gas, mining, utilities, and industrial sectors. In April 2025, the company completed a significant expansion of its Boca Raton, Florida manufacturing facility, increasing production capacity for Tier 4 Final–compliant generator sets in the 500–2,250 kW range to serve accelerating demand from data center and industrial customers.

Kawasaki Heavy Industries participates in the U.S. stationary generators market through its gas turbine generator and large industrial generator platforms, with applications concentrated in utility-scale power generation, petrochemical, and marine sectors requiring outputs that exceed the range of conventional reciprocating engine generator sets.

KUBOTA Corporation offers diesel generator sets in the 3 kVA to 35 kVA light-industrial and commercial range, leveraging its established U.S. agricultural and construction equipment distribution network to serve commercial, agricultural, and small industrial end-users with value-positioned compact products.

Mitsubishi Power Systems supplies large gas turbine generator sets and heavy industrial diesel systems for utility-scale and critical infrastructure applications, with U.S. installations concentrated in power generation facilities, petrochemical complexes, and large industrial backup power infrastructure where gas turbine configurations are specified for high-output, high-availability applications.

Multiquip Inc. manufactures and distributes diesel and gasoline generator sets from 6 kW to 500 kW for the construction, rental, and light industrial markets, with a broad U.S. distribution footprint serving contractor, rental fleet, and small commercial end-users requiring portable and semi-permanent power solutions.

Polar Power Inc. specializes in DC generator systems for telecommunications tower backup power applications, with products engineered for the specific duty cycle, fuel flexibility, and remote monitoring requirements of off-grid and weak-grid telecom infrastructure across rural and suburban U.S. markets.

Powerhouse Diesel Generators supplies diesel generator sets for commercial and industrial applications, with distribution concentrated in the South and Southeast U.S. sub-regions, serving construction, light industrial, and commercial standby markets through a regional dealer and direct-sales channel.

Rehlko (formerly Kohler Power, rebranded in 2024 following its strategic separation from Kohler Co.) offers generator sets from 2 kW residential units to 4,000 kW industrial systems across diesel, natural gas, and propane configurations. In January 2026, Rehlko completed its full operational transition as an independent company, consolidating its commercial and industrial generator, transfer switch, and power management portfolios under the Rehlko brand across all U.S. sales channels. The company's April 2024 KD Series product refresh incorporating Tier 4 Final–compliant engine updates and an integrated digital control architecture compatible with building automation and energy management systems reinforces its competitive strength in healthcare, hospitality, and commercial real estate end-uses.

TAYLOR GROUP INC manufactures diesel generator sets and integrated power systems for military, government, and heavy industrial procurement, with U.S.-based manufacturing capabilities that support domestic content requirements and defense acquisition program standards.

Triton Power manufactures industrial diesel generator sets from 20 kW to 2,500 kW for commercial, industrial, rental, and prime power markets. The company is expanding its presence in data center and critical infrastructure applications, with Tier 4 Final compliance and paralleling switchgear compatibility as standard features on its industrial product line.

Market Share of 15.5%

Collective Market Share of 45.5%

U.S. Stationary Generators Industry News

May 2026: Cummins announced the commercial release of its next-generation C-Series dual-fuel generator platform, featuring factory-configured diesel-to-natural gas switching capability targeting hyperscale data center N+2 redundancy configurations.

Mar 2026: Generac Power Systems disclosed expansion of industrial generator manufacturing capacity at its Wisconsin operations, adding a dedicated production line for Modular Power System (MPS) units above 500 kW to address extended order backlogs in the data center and industrial segments.

Jan 2026: Rehlko completed its full operational transition as an independent company following separation from Kohler Co., consolidating its commercial and industrial generator, transfer switch, and power management portfolios under the Rehlko brand across all U.S. sales channels.

Nov 2025: The U.S. Environmental Protection Agency published finalized amendments to the National Emission Standards for Hazardous Air Pollutants (NESHAP) for stationary reciprocating internal combustion engines (RICE), tightening formaldehyde and carbon monoxide emission limits applicable to engines above 500 kW with an effective date of January 2027.

Sep 2025: Caterpillar finalized a major supply agreement with a hyperscale data center developer for a multi-unit deployment of Cat 3516E generator sets each rated at 2,250 kW supporting a large campus under development in the Phoenix metropolitan area.

Jul 2025: Atlas Copco Power Technique launched the QAC 2000 containerized generator set for stationary data center and critical infrastructure applications, incorporating a Tier 4 Final–compliant engine platform and integrated PowerLink remote monitoring with cloud-based fleet analytics.

Apr 2025: HIPOWER SYSTEMS completed a significant expansion of its Boca Raton, Florida manufacturing facility, increasing production capacity for Tier 4 Final–compliant generator sets in the 500–2,250 kW range to serve accelerating demand from data center and industrial customers.

Feb 2025: Generac Power Systems integrated advanced predictive analytics capabilities into its Fleet Pro commercial generator management platform, enabling condition-based maintenance alerts and failure-mode prediction for managed generator fleets across commercial and industrial end-uses.

Oct 2024: The U.S. Department of Energy published updated federal data center operational guidelines under the Federal Sustainability Plan, specifying minimum backup power system efficiency and runtime requirements for federally funded and federally occupied data center facilities.

Jul 2024: Cummins entered a multi-year supply agreement with a Tier-1 colocation data center operator for natural gas generator sets supporting a portfolio of campus expansions concentrated in the Mountain States and Pacific States sub-regions.

Apr 2024: Rehlko announced the KD Series product refresh across its full 250 kW to 4,000 kW commercial and industrial generator range, incorporating Tier 4 Final–compliant engine updates and an integrated digital control architecture compatible with building automation and energy management systems.

Jan 2024: HIMOINSA expanded its U.S. market presence with the launch of its HIPT hybrid generator-battery integrated product line, combining a diesel generator with an integrated lithium-ion buffer system to reduce fuel consumption and emissions during variable-load commercial and construction site applications.

Market Concentration Score

The U.S. stationary generators market scores 5 out of 10 on the concentration scale, reflecting moderate fragmentation: the top five players collectively held 45.5% of revenue in 2025 with Generac Power Systems alone at 15.5% while the remaining 54.5% is distributed across 17 additional manufacturers spanning domestic specialists, international entrants, and regional distributors, indicating that scale incumbents hold structural distribution and service advantages but have not yet achieved the consolidation levels that would define a high-concentration market.

The U.S. stationary generators market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) & volume (‘000 Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Power Rating

≤ 50 kVA

> 50 kVA - 125 kVA

> 125 kVA - 200 kVA

> 200 kVA - 330 kVA

> 330 kVA - 750 kVA

> 750 kVA

Market, By Fuel

Diesel

Gas

Hybrid

Market, By End Use

Residential

Commercial

Telecom

Healthcare

Data centers

Educational institutions

Government centers

Hospitality

Retail sales

Real estate

Commercial complex

Infrastructure

Others

Industrial

Oil & gas

Manufacturing

Construction

Electric utilities

Mining

Transportation & logistics

IT

Military

Others

Market, By Application

Standby

Peak shaving

Prime/continuous

The above information has been provided for the following regions:

East North Central

West South Central

South Atlantic

North East

East South Central

West North Central

Pacific States

Mountain States

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2026

Chapter 5 Market Size and Forecast, By Power Rating, 2022 - 2035 (USD Million & '000 Units)

Chapter 6 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million & '000 Units)

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & '000 Units)

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million & '000 Units)

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & '000 Units)

Chapter 10 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →