Summary

Table of Content

Religious and Spiritual Products Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Religious and Spiritual Products Market Size

According to a recent study by Global Market Insights Inc., the global religious and spiritual products market was estimated at USD 5.5 billion in 2024 and projected to grow at a CAGR of 11.4% from 2025 to 2034.

Religious and Spiritual Products Market Key Takeaways

Market Size & Growth

- 2024 Market Size: USD 5.5 billion

- 2034 Forecast Market Size: USD 15.7 billion

- CAGR (2025–2034): 11.4%

Key Market Drivers

- Cultural embeddedness and ritual continuity.

- Rise of faith-based enterprises and ethical consumerism.

- Digital Evangelism and e-commerce expansion.

Challenges

- Commercialization backlash and moral sensitivities.

- Workplace and organizational tensions.

Opportunity

- Integration of spiritual wellness into healthcare and aging services.

- Rise of experiential and community-based spiritual consumption.

Key Players

- Market Leader: Bolsius International BV led with over 1.8% market share in 2024.

- Leading Players: Top 5 players in this market include Bolsius International BV, Mysore Deep Perfumery House, Delsbo Candle AB, Shubhkart, Sounds True Inc., which collectively held a market share of 6% in 2024.

Get Market Insights & Growth Opportunities

- The market has grown 49% since 2019, driven by the emergence of faith-based enterprises, businesses that explicitly align with religious values has significantly expanded the market. These organizations often integrate spiritual values into their branding, operations, and product offerings. For example, Chick-fil-A in the U.S. and Patanjali in India have leveraged religious identity to build trust and loyalty among consumers. This alignment with ethical and spiritual values appeals to a growing segment of consumers seeking authenticity and purpose in their purchases.

- Moreover, the rise of ethical consumerism where buyers prefer products that align with their moral or spiritual beliefs has created a fertile ground for religious product innovation. From eco-friendly incense to cruelty-free candles used in rituals, the market is evolving to meet both spiritual and sustainability expectations. This dual alignment enhances brand equity and drives premium pricing opportunities.

- The convergence of spirituality and healthcare presents a compelling opportunity for manufacturers and service providers of religious and spiritual products. Institutions such as Duke University’s Center for Spirituality, Theology and Health have documented how spiritual practices such as prayer, meditation, and ritual engagement, positively influence mental health, resilience, and recovery. This opens a pathway for spiritual products to be positioned not merely as religious artifacts but as therapeutic tools within wellness ecosystems. For example, products like guided meditation kits, spiritual journals, and ritual candles can be marketed as adjuncts to mental health programs, elder care services, and rehabilitation centers. The aging population, particularly in developed economies, is increasingly seeking meaning and purpose in later life stages.

- The religious and spiritual products market is increasingly shaped by the intersection of belief systems and economic structures, where tangible sacred items are not only expressions of faith but also commercial commodities. This dual nature allows producers to design products that serve both devotional and lifestyle purposes, thereby expanding their consumer base beyond traditional religious adherents.

- As spiritual consumption becomes more personalized and diversified, businesses must align product design with symbolic meaning and cultural relevance to maintain authenticity and market appeal. As per the data reported by Serkan Güne (2022) in the U.S. alone, religious institutions generated approximately USD 378 billion annually from direct religious services, with the broader economic impact including goods and services produced by religious groups estimated at USD 1.2 trillion. This scale positions the American belief industry among the top twenty global economies, illustrating the vast commercial potential of religious products when integrated with structured market strategies and consumer-centric design.

Religious and spiritual products are deeply embedded in the cultural and ritualistic fabric of societies, especially in countries with high religiosity. In India, for instance, over 79.8% of the population identifies as Hindu, and daily rituals such as pooja (worship) require specific items like incense sticks, diyas, and idols. This cultural continuity ensures a consistent baseline demand for spiritual products, regardless of economic cycles. The U.S. also reflects this trend, where 65% of adults identify with a religious tradition, and faith-based consumerism is growing through Christian bookstores and online devotional platforms.

This embeddedness is not merely habitual, it is identity-driven. Products like prayer beads, holy water, or religious icons serve as tangible extensions of belief systems. Their consumption is often non-discretionary, especially during festivals, life events (births, marriages, deaths), or spiritual milestones. This makes the market resilient and less susceptible to volatility compared to other lifestyle segments.

To get key market trends

Religious and Spiritual Products Market Trends

- The market is witnessing a rapid infusion of technology, particularly through mobile applications, AI-driven personalization, and e-commerce platforms. Companies are offering customized pooja kits, astrology-based product recommendations, and virtual ritual experiences tailored to individual belief systems. For example, platforms like Sounds True Inc. have capitalized on digital content delivery, offering meditation courses and spiritual guidance through subscription models, thereby expanding access and engagement across geographies.

- Faith-based enterprises are evolving beyond traditional religious institutions into structured, profit-oriented businesses that align spiritual values with consumer expectations. Brands like Patanjali in India and Chick-fil-A in the U.S. exemplify how religious identity can be embedded into product positioning, supply chain ethics, and customer loyalty strategies. This trend is enabling religious product companies to diversify into adjacent sectors such as wellness, food, and education, thereby enhancing revenue streams and market resilience.

- Modern consumers are increasingly seeking immersive spiritual experiences rather than passive product ownership. This has led to the rise of community-based rituals, spiritual retreats, and hybrid offerings that combine products with guided practices. For instance, Shubhkart’s bundling of pooja kits with vastu consultations reflects a broader shift toward holistic spiritual ecosystems. This trend is particularly strong among younger demographics who value authenticity, emotional resonance, and shared spiritual engagement.

Religious and Spiritual Products Market Analysis

")

Learn more about the key segments shaping this market

The market by product type is segmented into artifacts and accessories, ceremonial items, digital products, textbooks, and others. In 2024, the artifacts and accessories segment dominated the market and generated a revenue of USD 1.9 billion and is expected to grow at CAGR of around 10.1% during the forecast period 2025 to 2034.

- Artifacts such as idols, prayer beads, and sacred symbols hold enduring cultural significance, making them essential components of daily worship and spiritual identity across diverse traditions.

- These products are frequently purchased by individuals for personal use, home altars, and gifting, resulting in consistent demand and high turnover across both urban and rural markets.

- Artifacts and accessories offer wide scope for customization, artistic expression, and regional adaptation, enabling manufacturers to cater to varied consumer preferences and belief systems.

- The category allows for both artisanal and mass production models, facilitating participation from small-scale producers to global enterprises, thereby expanding supply-side capacity.

- Many accessories, such as spiritual jewelry or decor items, transcend religious boundaries and appeal to wellness, fashion, and cultural consumers, broadening market reach beyond traditional faith-based buyers.

Learn more about the key segments shaping this market

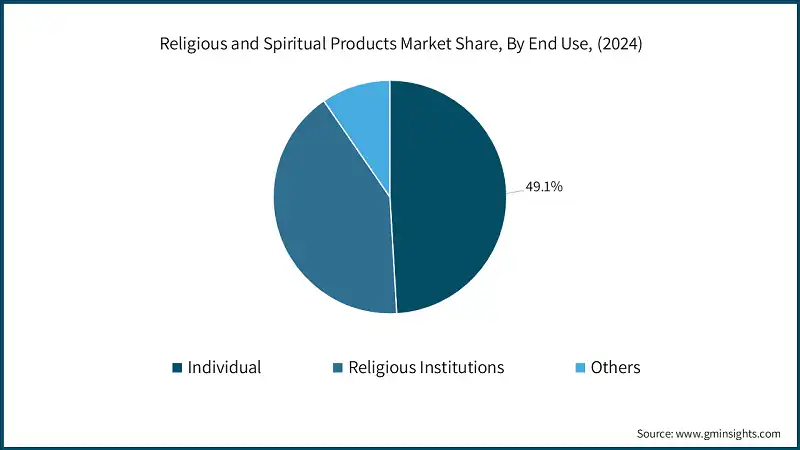

The religious and spiritual products market by end user is segmented into individual, religious institutions, and others. The individual segment was the leading segment in this market in 2024 with a revenue of USD 2.7 billion and has a market share of around 49.1%.

- Individuals engage in frequent, personalized consumption of spiritual products for daily rituals, meditation, and home worship, driving consistent demand across regions and demographics.

- The rise of spiritual self-care and mindfulness practices has expanded product relevance beyond traditional religious use, attracting younger and wellness-oriented consumers.

- E-commerce platforms and mobile apps have made spiritual products more accessible to individuals, enabling direct purchases without institutional intermediaries.

- Product categories such as accessories, incense, and digital content are designed for individual use, offering convenience, customization, and emotional resonance.

- Cultural traditions and life events, such as festivals, births, and personal milestones, often prompt individual purchases, reinforcing the segment’s dominance in both volume and value.

Looking for region specific data?

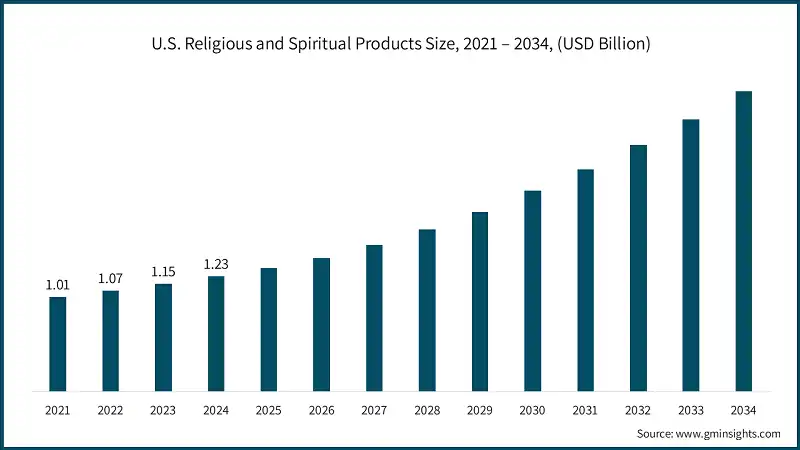

- The U.S. religious and spiritual products market was valued at around USD 1.23 billion in 2024 and is anticipated to register a CAGR of 10.4% between 2025 and 2034.

- The U.S. demonstrates strong demand in the market due to its deeply rooted religious infrastructure and widespread individual engagement in spiritual practices. According to the U.S. Bureau of Labor Statistics, over 56,000 clergy members are employed across various sectors, including religious organizations, hospitals, and schools, with religious organizations alone accounting for 26,850 clergy positions. This institutional presence reflects a robust ecosystem that supports the consumption of ceremonial items, religious texts, and spiritual accessories. Additionally, the U.S. Commission on International Religious Freedom (USCIRF) emphasizes that religious freedom remains a national priority, reinforcing the cultural and policy environment that sustains demand for faith-based products.

- From a consumer behavior perspective, the U.S. market is also driven by the integration of spirituality into wellness and mental health practices. A study by the National Center for Complementary and Integrative Health reports that approximately 14.3% of U.S. adults engage in meditation, a practice often supported by spiritual products such as incense, prayer beads, and guided audio tools. This trend is further amplified by the rise of e-commerce and digital platforms that offer personalized spiritual experiences, making products more accessible to individual consumers. The convergence of institutional support, consumer interest, and digital innovation positions the U.S. as a mature and expanding market for religious and spiritual products.

- Europe: Europe witnessed promising demand in the religious and spiritual products market with a share of around 22.2% in 2024 and is expected to grow at a robust CAGR of 10.6% during the forecast period.

o Europe is demonstrating strong demand in the market due to its deeply embedded cultural and educational frameworks that support religious expression. According to the European Union’s Charter of Fundamental Rights, member states are required to respect the right of parents to educate their children in accordance with their religious and philosophical convictions. This legal foundation has led to the integration of religious education in public schools across countries like Germany, Austria, and Belgium, where optional religious subjects are part of the formal curriculum. Such institutional support sustains a steady demand for religious texts, ceremonial items, and educational materials, reinforcing the market’s relevance across generations.

o Additionally, Europe’s robust e-commerce infrastructure is amplifying access to spiritual products, particularly among individual consumers. The International Trade Administration reports that Europe is the third-largest retail e-commerce market globally, with revenues reaching USD 631.9 billion and projected to grow to USD 902.3 billion by 2027. Countries like Germany, France, and the Netherlands show high weekly online shopping rates, with Germany leading at 45%. This digital penetration enables consumers to purchase spiritual accessories, ritual items, and digital content with ease, driving consumption beyond traditional religious institutions. The convergence of cultural tradition and digital accessibility positions Europe as a mature and expanding market for religious and spiritual products.

- Asia Pacific: In 2024, the religious and spiritual products market revenue for the Asia Pacific was around USD 2 billion and is expected to reach USD 6.3 billion by 2034.

o The Asia-Pacific (APAC) region is demonstrating the strongest demand in the market due to its vast population, cultural diversity, and rapid digital adoption. According to the International Trade Administration, the APAC region is projected to reach an e-commerce market value of over USD 28.9 trillion by 2026, with countries like China, Indonesia, and Vietnam leading in cross-border digital commerce. This digital infrastructure enabling widespread access to spiritual products, from incense and pooja kits to digital meditation tools, especially among younger, tech-savvy consumers. Additionally, Southeast Asia’s internet economy alone is expected to grow from USD 194 billion to over USD 330 billion by 2025, further reinforcing the region’s capacity to consume spiritual goods at scale.

o Culturally, the region is home to some of the world’s most spiritually active populations, including the largest Muslim-majority country (Indonesia), deeply rooted Buddhist and Hindu traditions (India, Thailand, Vietnam), and a growing Christian base in countries like the Philippines. The U.S. Commission on International Religious Freedom notes that ASEAN countries uphold religious freedom as a constitutional right, which supports the open practice and commercialization of spiritual traditions. This legal and cultural environment, combined with a regional GDP of approximately USD 3.9 trillion and a population of 678 million across ASEAN nations, creates a fertile ground for sustained and diversified demand in the market.

Religious and Spiritual Products Market Share

- The top 5 companies in the market, such as Bolsius International BV, Mysore Deep Perfumery House, Delsbo Candle AB, Shubhkart, Sounds True Inc., hold a market share of 5-7%.

- Bolsius has built its competitive resilience through a combination of heritage branding, sustainability leadership, and global distribution. As a certified B Corp, the company aligns its operations with the UN Sustainable Development Goals and the Paris Agreement, focusing on emission reduction and ethical sourcing. Its “Reduce, Care & Engage” impact strategy not only enhances brand equity but also appeals to environmentally conscious consumers. With operations in over 50 countries and a strong emphasis on innovation and transparency, Bolsius continues to differentiate itself in a saturated candle market.

- MDPH has scaled its business by leveraging deep market penetration, competitive pricing, and a vast distribution network that spans 7.5 lakh retail outlets and 43 countries. The company manufactures 35 million incense sticks daily and has diversified into pooja essentials, home fragrances, and personal care. Its strategy includes aggressive brand building through celebrity endorsements, innovation-driven product launches, and AI-enabled operational upgrades. MDPH’s ability to combine traditional product categories with modern business practices allows it to withstand competition and pursue ambitious growth targets.

- Delsbo Candle maintains its market position through a focused niche strategy centered on sustainability and private-label production. As the first manufacturer of Swan-labelled candles globally, the company adheres to strict environmental standards, avoiding products like tealights that conflict with its eco-policy. Its ISO 9001-certified operations and flexible production model allow it to serve large institutional clients while maintaining artisanal quality. By aligning its brand with environmental values and offering customization, Delsbo effectively competes in both B2B and premium consumer segments.

Religious and Spiritual Products Market Companies

Shubhkart has carved a unique space by offering bundled spiritual solutions, combining pooja kits with vastu products, astrology services, and personalized consultations. Its direct-to-consumer model enables efficient distribution and customer engagement, while its product range caters to both traditional and modern spiritual needs. The company’s strategy focuses on creating a holistic spiritual ecosystem, which not only drives repeat purchases but also builds long-term consumer trust. This integrated approach helps Shubhkart differentiate itself in a fragmented market.

Sounds True thrives on content-driven differentiation, offering digital spiritual products such as meditation courses, audio programs, and online retreats. Its partnerships with globally recognized spiritual teachers and authors provide exclusive content that is difficult for competitors to replicate. The company has embraced subscription-based models and personalized digital experiences, which have seen significant growth in user engagement. By positioning itself at the intersection of spirituality and wellness, Sounds True continues to expand its influence in both consumer and institutional segments.

Major players operating in the religious and spiritual products industry are:

- Bolsius International BV

- Brown Living

- Delsbo Candle AB

- Divine Hindu

- Indo Divine Spiritual Solutions Pvt. Ltd.

- Mysore Deep Perfumery House

- Namoh Indiya

- Powerfulhand.com

- Prajjwal International

- Pujahome

- Rgyan Shop

- Rudra India

- Shubhkart

- Sounds True Inc.

- Stuller, Inc.

Religious and Spiritual Products Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 5.5 billion |

| Forecast Period 2025 - 2034 CAGR | 11.4% |

| Market Size in 2034 | USD 15.7 billion |

| Key Market Trends | |

| Drivers | Impact |

| Cultural embeddedness and ritual continuity | Sustains consistent global demand for religious products by anchoring them in daily rituals, festivals, and life events across diverse cultures. |

| Rise of faith-based enterprises and ethical consumerism | Expands market reach by aligning product offerings with spiritual values and ethical consumption trends, especially among younger and value-driven consumers. |

| Digital Evangelism and e-commerce expansion | Accelerates global accessibility and personalization of spiritual products through online platforms, reaching diaspora and tech-savvy audiences at scale. |

| Pitfalls & Challenges | Impact |

| Commercialization backlash and moral sensitivities | Undermines consumer trust and brand credibility when sacred products are perceived as commodified or culturally insensitive. |

| Workplace and organizational tensions | Limits scalability and inclusivity as faith-driven enterprises risk internal bias and external reputational challenges in diverse markets. |

| Opportunities: | Impact |

| Integration of spiritual wellness into healthcare and aging services | Unlocks new revenue streams and cross-sector partnerships by embedding spiritual products into therapeutic, elder care, and mental wellness ecosystems. |

| Rise of experiential and community-based spiritual consumption | Drives product innovation and brand loyalty through immersive, socially engaging spiritual experiences that blend tradition with modern lifestyle preferences. |

| Market Leaders (2024) | |

| Market Leaders |

1.8% market share |

| Top Players |

Collective market share in 2024 is 6% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Middle East and Africa |

| Emerging Country | India, Brazil, Indonesia, South Africa, Vietnam |

| Future Outlook |

|

What are the growth opportunities in this market?

Religious and Spiritual Products Industry News

- In July 2025, spiritual tech platform Rgyan launched Bodhi, India’s first AI-powered devotional companion designed to offer personalized spiritual guidance. This innovation marks a significant leap in integrating artificial intelligence with devotional practices, enabling users to access tailored content, rituals, and spiritual insights through a conversational interface. The launch reflects a broader trend of digitizing spirituality to meet the evolving needs of tech-savvy consumers.

- In July 2025, Astroyogi, a leading spiritual retail and astrology platform, announced its strategic focus on AI-driven personalization and expanded spiritual commerce, targeting a revenue milestone of USD 29 million. The company is leveraging data analytics and machine learning to enhance user engagement and product relevance, positioning itself as a frontrunner in the convergence of spirituality and digital retail. This move underscores the growing demand for customized spiritual experiences in India’s online marketplace.

- In January 2025, Utsav, a spiritual and devotion platform, secured USD 8 million in a funding round to scale its operations and expand its product offerings. The capital infusion will support technology upgrades, content diversification, and market outreach, enabling Utsav to strengthen its position in the competitive spiritual tech landscape. This investment signals investor confidence in the monetization potential of devotional platforms in India’s digital economy.

- In October 2025, Brown Living, a sustainable goods marketplace, announced its ambition to tap into the USD 50 billion sustainable products market with new capital backing. While not exclusively religious, the platform’s focus on eco-conscious spiritual items such as biodegradable incense and ethically sourced ritual accessories aligns with the rising demand for ethical consumerism in the spiritual segment. This development highlights the intersection of sustainability and spirituality as a future growth driver.

The religious and spiritual products market research report includes in-depth coverage of the industry, with estimates & forecasts in terms of revenue (USD Billion) and volume (Million Units) from 2021 to 2034, for the following segments:

Market, By Product Type, 2021 -2034

- Artifacts and accessories

- Ceremonial items

- Digital products

- Textbooks

- Others

Market, By End User, 2021 -2034

- Individual

- Religious institutions

- Others

Market, By Distribution Channel, 2021 -2034

- Online

- Company website

- E-commerce website

- Offline

- Religious bookstores

- Gift shops

- Specialty stores

- Others

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- Germany

- U.K.

- France

- Italy

- Spain

- Netherlands

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- UAE

- Saudi Arabia

- South Africa

Frequently Asked Question(FAQ) :

What is the market size of the religious and spiritual products in 2024?

The market size was USD 5.5 billion in 2024, with a CAGR of 11.4% expected from 2025 to 2034, driven by cultural embeddedness, ritual continuity, and the rise of faith-based enterprises.

What is the projected value of the religious and spiritual products market by 2034?

The market is expected to reach USD 15.7 billion by 2034, fueled by digital evangelism, e-commerce expansion, and integration of spiritual wellness into healthcare and aging services.

How much revenue did the artifacts and accessories segment generate in 2024?

The artifacts and accessories segment generated USD 1.9 billion in 2024, dominating the market due to their cultural significance and broad consumer appeal.

What was the valuation of the individual end-user segment in 2024?

The individual segment held a 49.1% market share and generated USD 2.7 billion in 2024, driven by personalized spiritual consumption and e-commerce accessibility.

What is the growth outlook for the Asia Pacific religious and spiritual products market?

Asia Pacific revenue was USD 2 billion in 2024 and is expected to reach USD 6.3 billion by 2034, supported by cultural diversity, digital adoption, and high religiosity.

Which region leads the religious and spiritual products industry?

Asia Pacific is the largest market, with strong demand from countries such as India, Indonesia, and China, driven by deep-rooted spiritual traditions and rapid e-commerce growth.

Who are the key players in the religious and spiritual products market?

Key players include Bolsius International BV, Mysore Deep Perfumery House, Delsbo Candle AB, Shubhkart, Sounds True Inc., Brown Living, Divine Hindu, Indo Divine Spiritual Solutions, Namoh Indiya, Powerfulhand.com, Prajjwal International, Pujahome, Rgyan Shop, Rudra India, and Stuller, Inc.

Religious and Spiritual Products Market Scope

Related Reports