Authors:

Avinash Singh, Sunita Singh

Download free PDF

North America Smart Greenhouse Market Size & Share 2026-2035

Report ID: GMI15577

|

Published Date: February 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

North America Smart Greenhouse Market

Get a free sample of this report

Get a free sample of this report North America Smart Greenhouse Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

North America Smart Greenhouse Market Size

The North America smart greenhouse market was estimated at USD 1.24 billion in 2025. The market is expected to grow from USD 1.22 billion in 2026 to USD 3.3 billion in 2035, at a CAGR of 11.5% according to latest report published by Global Market Insights Inc.

North America Smart Greenhouse Market Key Takeaways

Market Leader: Priva led with over 16% market share in 2025.

Leading Players: Top 5 players in this market include Priva, Freight Farms, Argus Control Systems, Fluence Bioengineering, Total Grow Control, which collectively held a market share of 48% in 2025.

The market for smart greenhouses in North America is growing at a rapid pace owing to a number of factors that are currently converging, including an increasing demand for food production, resource scarcity, and a strong need for sustainable models of agriculture. The agricultural sector in North America is undergoing a transformation due to the adoption of technologies that improve climate control, automate processes, and optimize resource utilization, making smart greenhouses a necessity in order to fulfill future food security requirements.

The North American market has experienced rapid growth over the past few years due to an increasing awareness of the environmental impacts associated with traditional farming methods. More stringent regulations on water and pesticide use, as well as a general move towards sustainability, have compelled farmers and agricultural businesses to adopt controlled environment agriculture (CEA). Rapid urbanization in major American and Canadian cities has also increased demand for locally grown produce throughout the year, further justifying the need for smart greenhouses in the commercial and urban farming sectors.

At present, North America accounts for more than 49% of the overall smart greenhouse market share, primarily because of its strong adoption of agricultural technology and its continued investment in Agri-tech innovation. However, with the increasing concerns about food security and resilience, especially in the context of climate volatility, there is a growing need for farmers to adopt climate-independent food systems. Moreover, the urban and peri-urban markets are increasingly turning to smart greenhouses to make their carbon footprint smaller and to ensure a steady supply of high-quality, pesticide-free food. Although there has been progress in this area, the region is still challenged by factors such as high capital costs and a lack of qualified personnel who can handle sophisticated automated systems.

From the technology segmentation perspective, hydroponics-based smart greenhouses currently lead the North American market because of their resource efficiency and high output capacity. The growing interest in soilless agriculture, along with innovations in automated nutrient delivery, water recycling, and precision feeding, has made hydroponic systems particularly appealing to large commercial farmers as well as urban farmers. Their compatibility with sustainability agendas such as water conservation and decreased chemical use further cements their leading position in the North American market. Regulatory pressure in North America is another key factor that is fueling the growth of the market.

Tightening environmental regulations, particularly in arid regions like California and the Southwest, are encouraging farmers to adopt more efficient and scalable models of farming. Water and certain chemical pesticides restrictions are directly leading to increased adoption of smart greenhouse technology. As the need to comply becomes an imperative for most farmers, smart greenhouses are turning out to be one of the most feasible, productive, and compliant agricultural technologies.

The overall scenario is also supporting the North American transition to technology-driven food production. According to the Food and Agriculture Organization of the United Nations, the world will require a 56% increase in food production by 2050, with the same amount of arable land being reduced due to urbanization and climate change. At the same time, research from the World Bank suggests that agriculture accounts for 70% of global freshwater use—furthering the need for water conservation through controlled environment agriculture.

Advances in CEA technology, such as automated climate control, IoT sensing, real-time analytics, and AI-driven decision support tools, are significantly improving productivity, reducing labor intensity, and optimizing overall operational efficiency. Overall, the North American smart greenhouse market is positioned for strong continuous growth as regulatory requirements, sustainability goals, and food security concerns push the region toward advanced, high‑yield, and climate‑independent modes of agriculture.

North America Smart Greenhouse Market Trends

In North America, the demand for smart greenhouse technology has increased substantially because of the efforts of government agencies and agricultural organizations to adopt sustainable, resilient, and technology-based food security solutions. The region is also under similar pressures in the global market, including the reduction of freshwater resources, the reduction of arable land due to urbanization, and the increase in food requirements due to population growth. U.S. and Canadian agricultural organizations are increasingly advocating for sustainable agricultural practices, supporting technologies that are less resource-dependent. Climate-resilient, lower chemical, and water-conserving policies continue to drive the adoption of controlled environment agriculture (CEA) in the region.

North America Smart Greenhouse Market Analysis

Based on the type of segment, the market is further segmented into hydroponic greenhouse and non-hydroponic greenhouse. The hydroponic greenhouse segment was valued at USD 877.6 million in 2025 and is projected to reach USD 2.56 billion by 2035.

The requirement to advance the effectiveness and sustainability of the division of the high-value, soil-friendly crops administration thusly drives the consummation of the non-hydroponic clever systems that can act as a significant transitional step amid the ordinary farming and the non-soil based flora development.

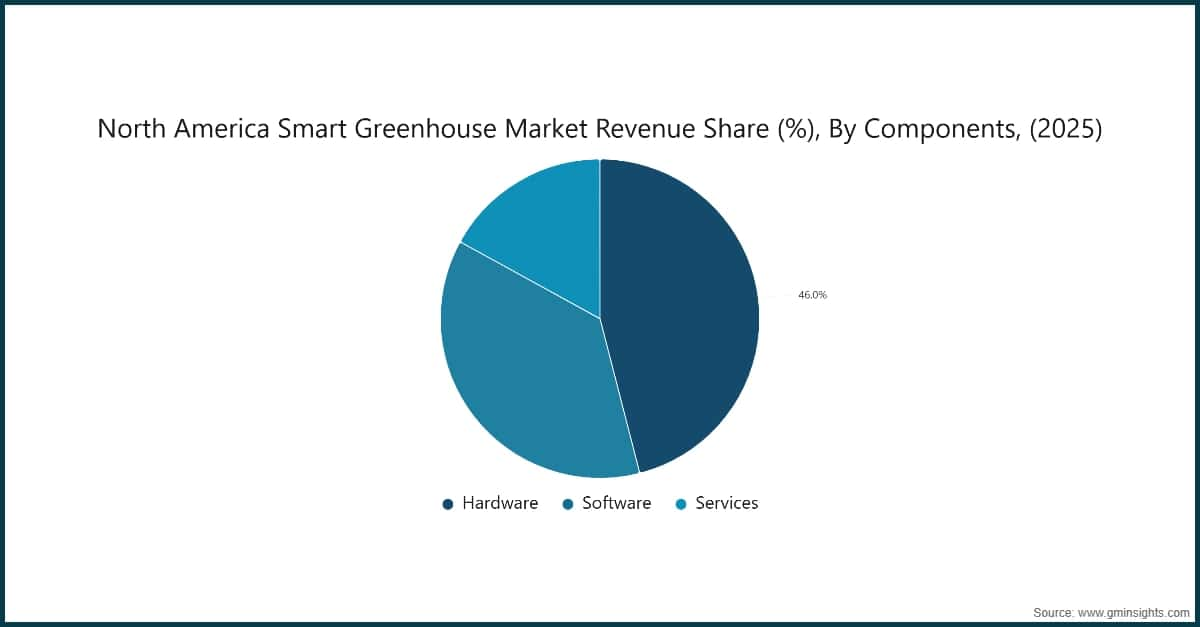

Based on components, the smart greenhouse market is segmented into hardware, software, and services. The hardware segment was valued at USD 519.2 million in 2025 and is anticipated to grow with a CAGR of 5.9% during the forecast period.

Based on technology, the smart greenhouse market is segmented into HVAC systems, LED grow lights, sensors and control systems, irrigation System, pumps and valves, and material handling. The HVAC system dominates the market and shows potential growth in the upcoming future.

The U.S. dominated the North America smart greenhouse market, which was valued at USD 988 million in 2025 and is estimated to grow at a CAGR of 11.6% from 2026 to 2035.

North America Smart Greenhouse Market Share

North America Smart Greenhouse Market Companies

Major players operating in the smart greenhouse industry are:

~16% market share

Collective Market Share in 2024 is ~48%

North America Smart Greenhouse Industry News

The smart greenhouse market research report includes in-depth coverage of the industry, with estimates & forecasts in terms of revenue ($ Bn) from 2026 to 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Type

Market, By Component

Market, By Application

Market, By Technology

Market, By End-user

The above information is provided for the following countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Type, 2022-2035 (USD Million)

Chapter 6 Market Estimates & Forecast, By Components, 2022-2035 (USD Million)

Chapter 7 Market Estimates & Forecast, By Application, 2022-2035 (USD Million)

Chapter 8 Market Estimates & Forecast, By Technology, 2022-2035 (USD Million)

Chapter 9 Market Estimates & Forecast, By End-User, 2022-2035 (USD Million)

Chapter 10 Market Estimates & Forecast, By Country, 2022-2035 (USD Million)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →