Authors:

Monali Tayade, Jignesh Rawal

Download free PDF

Hemodynamic Monitoring Devices Market Size & Share 2026-2035

Report ID: GMI7995

|

Published Date: January 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Hemodynamic Monitoring Devices Market

Get a free sample of this report

Get a free sample of this report Hemodynamic Monitoring Devices Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Hemodynamic Monitoring Devices Market Size

The global hemodynamic monitoring devices market was valued at USD 1.6 billion in 2025 and is projected to grow from USD 1.7 billion in 2026 to USD 3.1 billion by 2035, expanding at a CAGR of 7.2%, according to the latest report published by Global Market Insights Inc. This substantial growth is driven by numerous factors such as rising incidence of chronic diseases across the globe, technological advancements in hemodynamic monitoring devices, increasing preference for telehealth services, and growing number of surgeries.

Hemodynamic Monitoring Devices Market Key Takeaways

Market Leader: Koninklijke Philips N.V. led with over 20% market share in 2025.

Leading Players: Top 5 players in this market include Koninklijke Philips N.V., Baxter International, Abbott Laboratories, Siemens Healthineers, GE HealthCare Technologies Inc., which collectively held a market share of 53% in 2025.

Hemodynamic monitoring devices measure blood pressure and flow within the cardiovascular system in order to evaluate circulation and heart function. They offer real time information on variables like blood pressure, vascular resistance, and cardiac output. These devices are frequently used to direct medication and fluid therapy during high-risk surgeries, critical care units, and operating rooms. Additionally, they are used to treat conditions where accurate cardiovascular monitoring is crucial, such as heart failure, shock, and severe trauma. Koninklijke Philips N.V., Baxter International, Abbott Laboratories, Siemens Healthineers, and GE HealthCare Technologies Inc. are some of the top firms in the hemodynamic monitoring devices market. By introducing cutting-edge non-invasive technologies, incorporating AI-driven analytics, and increasing their presence in emerging markets, leading companies in the market are expanding.

The market grew from USD 1.3 billion in 2022 to USD 1.5 billion in 2024. The rising incidence of chronic diseases worldwide is significantly driving the growth of the market. According to the World Health Organization, noncommunicable diseases (NCDs) caused death of at least 43 million people in 2021, representing 75% of non-pandemic-related deaths globally. Cardiovascular diseases accounted for the largest share with 19 million deaths, followed by cancers (10 million), chronic respiratory diseases (4 million), and diabetes (over 2 million including kidney disease deaths caused by diabetes).

This growing burden of chronic conditions necessitates advanced monitoring solutions to manage hemodynamic parameters effectively, especially in critical care and surgical settings. As these diseases often lead to complications such as heart failure, hypertension, and multi-organ dysfunction, healthcare providers are increasingly adopting hemodynamic monitoring devices to ensure accurate assessment and timely intervention. This adoption is expected to accelerate further with the integration of AI-driven analytics and remote monitoring capabilities, making hemodynamic monitoring an essential component of modern healthcare delivery.

Additionally, the rising volume of surgical procedures is a key factor fueling the growth of the hemodynamic monitoring devices market. These devices are essential for assessing cardiovascular function during complex surgeries, ensuring patient safety and optimizing outcomes. As surgical interventions become more frequent, hospitals and surgical centers are increasingly adopting advanced monitoring systems to manage perioperative risks such as hypotension and cardiac instability.

According to the Agency for Healthcare Research and Quality, U.S. hospital-owned facilities conducted approximately 12.4 million ambulatory surgery encounters in 2022, up from 11.9 million in 2021. This surge in surgical volumes underscores the growing demand for reliable monitoring technologies that can deliver real-time insights into cardiac output, blood pressure, and tissue perfusion. As healthcare systems worldwide expand surgical capacity and prioritize patient safety, the adoption of minimally invasive and advanced hemodynamic monitoring solutions is expected to accelerate, driving market growth over the coming years.

Hemodynamic monitoring devices are a vital part of today's healthcare, providing real-time assessments of cardiovascular parameters including cardiac output, blood pressure, and tissue perfusion. The information recovered from these devices is used to assist clinicians in managing patients who are receiving fluid therapy or undergoing medical treatment during times of surgical or critical care. By using this type of monitoring, clinicians can detect instability in patients' hemodynamic system before severe complications develop, ultimately improving patient outcomes, and providing more individualized treatment plans, making them indispensable in enhancing patient safety and optimizing resource utilization in hospitals and surgical centers.

Hemodynamic Monitoring Devices Market Trends

Hemodynamic Monitoring Devices Market Analysis

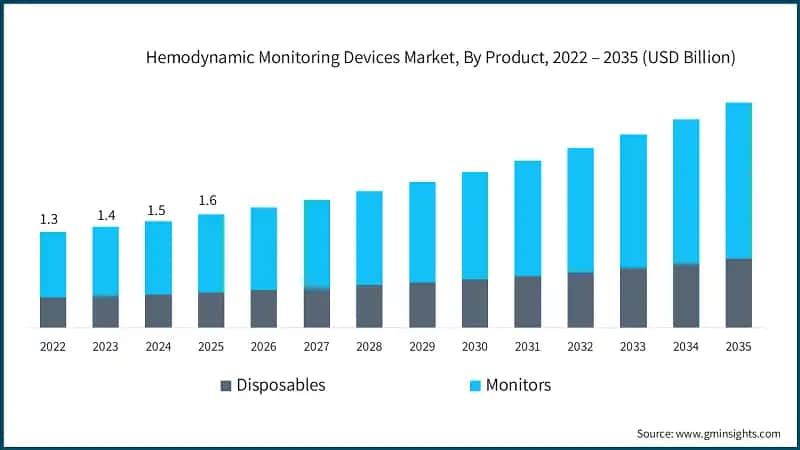

Based on product, the market is bifurcated into disposables and monitors. The monitors segment is dominating the market with the largest revenue of USD 1.1 billion in 2025.

Based on system type, the hemodynamic monitoring devices market is segmented into non-invasive, invasive, and minimally invasive. The non-invasive segment dominated the market with the largest revenue of USD 809.4 million in 2025 and is expected to grow at a CAGR of 7.3% over the forecast period.

Based on end use, the hemodynamic monitoring devices market is segmented into hospitals, ambulatory surgical centers, homecare settings, and other end users. The hospitals segment dominated the market with the largest revenue share of 64.4% in 2025 and is expected to grow at the fastest CAGR over the forecast period.

North America hemodynamic monitoring devices market

North America dominated the market with a market share of 36.4% in 2025.

Europe Hemodynamic Monitoring Devices Market

Europe market accounted for USD 433.9 million in 2025 and is anticipated to show lucrative growth over the forecast period.

Germany hemodynamic monitoring devices market is projected to experience steady growth between 2026 and 2035.

Asia Pacific Hemodynamic Monitoring Devices Market

The Asia Pacific region is projected to be valued at USD 380.7 million in 2025.

Japan hemodynamic monitoring devices market is poised to witness lucrative growth between 2026 - 2035.

Latin America Hemodynamic Monitoring Devices Market

Middle East and Africa Hemodynamic Monitoring Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

Hemodynamic Monitoring Devices Market Share

20% market share

Hemodynamic Monitoring Devices Market Companies

Few of the prominent players operating in the hemodynamic monitoring devices industry include:

Baxter is a major player in the hemodynamic monitoring devices market, notably through its Starling Fluid Management Monitoring System, which utilizes patented bioreactance technology to deliver noninvasive, real-time cardiac output and fluid responsiveness data. This innovation supports individualized fluid therapy across ICU, ED, OR, and rapid response settings, reducing potential complications from invasive lines and aligning with a broader healthcare trend toward non-invasive patient care. Baxter’s strategic focus on non-invasive solutions positions it strongly in a market that increasingly favors safer, patient-friendly monitoring platforms.

Philips holds a significant position in the interventional hemodynamic monitoring market through its Hemo system with IntelliVue X3. Tailored for catheterization labs, this solution integrates advanced hemodynamic measurements into a touchscreen patient monitor, facilitating seamless table side control and real-time data visualization. This approach aligns with Philips’s commitment to workflow optimization and enhanced clinical decision-making in interventional environments, reinforcing its influence in cathlab hemodynamic monitoring.

GE Healthcare’s Mac Lab Hemodynamic Recording System has long been a cornerstone in cath lab monitoring, with nearly 20 years of trusted use. The system excels at integrating imaging, waveform data, and reporting tools within high-volume cath labs, ensuring data synchronization, interoperability, and streamlined clinician workflows. GE’s deep integration with hospital IT systems and its commitment to documentation efficiency underscore its sustained leadership in invasive hemodynamic monitoring platforms.

Hemodynamic Monitoring Devices Market News:

The hemodynamic monitoring devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 - 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Product

Market, By System Type

Market, By End Use

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology and Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

Chapter 6 Market Estimates and Forecast, By System Type, 2022 - 2035 ($ Mn)

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

Chapter 9 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →