Authors:

Ankit Gupta, Shubham Chaudhary

Download free PDF

CHP Equipment Market Size & Share 2026-2035

Report ID: GMI16273

|

Published Date: July 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Download Free PDF

CHP Equipment Market

Get a free sample of this report

Get a free sample of this report CHP Equipment Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

CHP Equipment Market Size

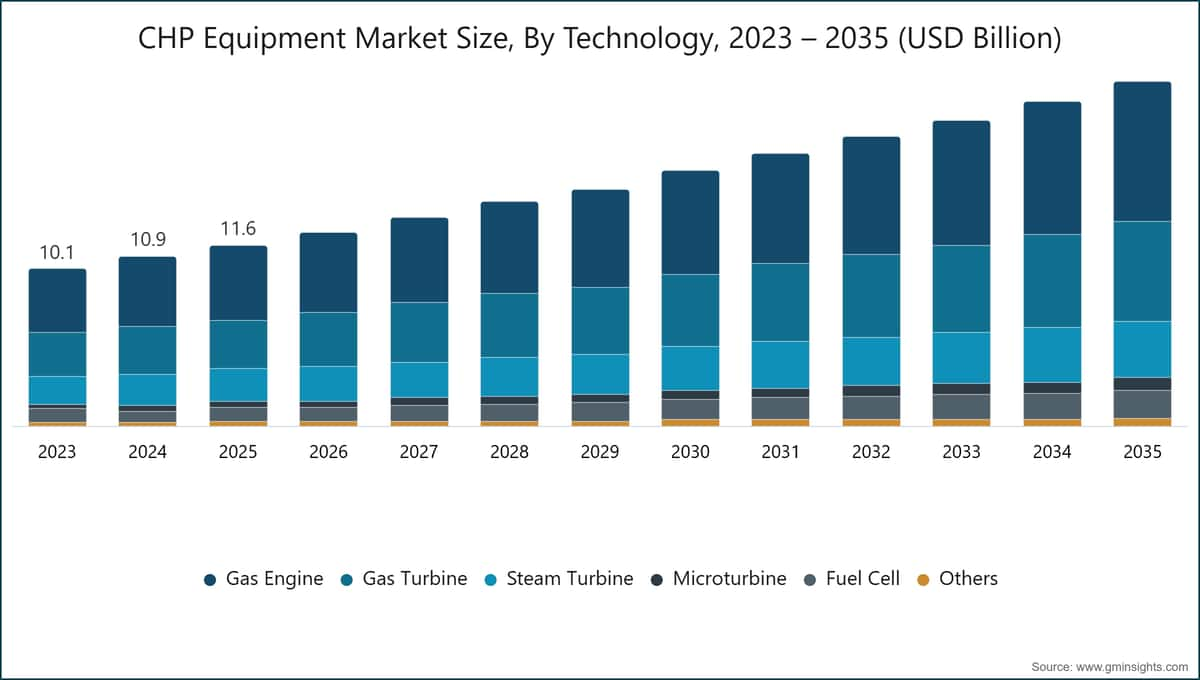

The global combined heat and power equipment market was valued at USD 11.6 billion in 2025, underpinned by widespread industrial adoption of on-site cogeneration systems that simultaneously produce electricity and recoverable thermal energy consistently delivering 75–80% fuel-to-useful-energy conversion versus approximately 36% for conventional grid generation.[1]International Energy Agency, iea.org The market is projected to reach USD 22.1 billion by 2035, advancing at a compound annual growth rate (CAGR) of 6.5% over the 2026–2035 forecast period, as energy cost pressures, decarbonization mandates, and grid resilience priorities accelerate capital allocation toward integrated on-site power and heat systems. These projections are according to the latest report published by Global Market Insights Inc.

CHP Equipment Market Key Takeaways

Market Leader: Caterpillar led with over 10.5% market share in 2025.

Leading Players: Top 5 players in this market include GE Vernova, Caterpillar, Siemens Energy, Bloom Energy, Mitsubishi Heavy Industries, which collectively held a market share of 40.5% in 2025.

The structural growth narrative is defined by a transition from single-fuel gas engine configurations to multi-fuel, digitally managed, and hydrogen-compatible platforms a shift reshaping product roadmaps across OEMs and creating differentiated demand profiles across technology, capacity, fuel, application, and installation segments. At the competitive level, the CHP equipment market bifurcates between incumbent gas engine and gas turbine manufacturers expanding their fuel-flexibility envelope and emerging fuel cell-first competitors targeting high-value, low-emissions niches across data center, industrial, and district energy applications.

Key Drivers

Drivers Impact Analysis

Driver

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Rising Demand for Energy Efficiency and Cost Savings

+1.9%

Global

Short term (≤ 2 years)

Growing Focus on Decarbonization and Emissions Reduction

+1.6%

Europe, North America

Medium term (2–4 years)

Expansion of Distributed Energy Generation

+1.5%

North America, Asia Pacific

Short term (≤ 2 years)

Increasing Industrial and Commercial Energy Demand

+1.2%

Asia Pacific, MEA

Long term (≥ 4 years)

Rising Demand for Energy Efficiency and Cost Savings

CHP systems convert up to 80% of fuel input into useful energy combined heat and electricity compared with approximately 36% conversion efficiency for conventional centralized power generation. This differential translates directly into measurable operational cost savings for energy-intensive industries including chemicals, food processing, paper manufacturing, and pharmaceutical production. The economics of on-site cogeneration are particularly compelling when grid electricity tariffs are elevated and natural gas prices are stable conditions that characterized much of Europe and North America through the 2022–2025 period. Declining system costs in packaged CHP configurations below 500 kW have broadened the addressable market to include commercial buildings, hospitality complexes, hospitals, and multifamily residential developments. On a unit-economics basis, operators in high-tariff jurisdictions can achieve payback periods of four to seven years on mid-scale gas engine CHP installations, making the capex case increasingly defensible across a wider buyer segment.

Growing Focus on Decarbonization and Emissions Reduction

Decarbonization policy is the most consequential structural accelerant for CHP adoption across European and North American markets. The revised EU Energy Efficiency Directive (Directive 2023/1791) requires member states to conduct cost-benefit analyses for all new or substantially refurbished thermal installations exceeding 20 MW total thermal input, establishing a regulatory floor that effectively embeds CHP consideration into every major industrial energy capital expenditure decision above that threshold.[2]European Commission – Energy, energy.ec.europa.eu The directive sets a legally binding EU-wide target of reducing final energy consumption by 11.7% by 2030 versus projected levels, with high-efficiency cogeneration defined as achieving at least 10% primary energy savings compared with separate heat and electricity production. In the United States, the EPA's CHP Partnership Program formally recognizes CHP as a clean energy strategy, and the DOE's Better Buildings initiative provides technical assistance and deployment resources to support CHP adoption at industrial and commercial facilities.[3]US Environmental Protection Agency, epa.gov The emissions reduction case is quantifiable: high-efficiency cogeneration can achieve up to 90% total energy conversion at state-of-the-art configurations, reducing CO₂ output per unit of useful energy by 20–30% compared with separate generation.

Expansion of Distributed Energy Generation

The structural shift toward distributed energy architectures driven by grid resilience concerns, data center power demand growth, and microgrid deployment across industrial and commercial campuses is expanding the CHP equipment addressable market well beyond its traditional heavy-industrial base. CHP units are increasingly configured as anchor generation assets within microgrid designs, providing firm baseload output with co-located thermal offtake. The US DOE estimates total technical CHP potential at over 240 GW across industrial and commercial sites in the United States alone, versus approximately 82 GW of currently installed capacity at more than 4,700 operational sites a ratio that signals a substantial long-term deployment runway. Distributed CHP is also gaining traction in data center power strategies, where fuel cell CHP systems offer high-density on-site generation Bloom Energy's 100 MW per-acre power density benchmark combined with waste heat recovery for cooling and conditioning loads.

Increasing Industrial and Commercial Energy Demand

Industrial output expansion in Asia Pacific and the Middle East is directly driving demand for on-site energy infrastructure at industrial parks, processing facilities, and special economic zones. Manufacturing growth in China, India, and Gulf Cooperation Council economies is creating deployment opportunities for CHP systems in the 1–50 MW capacity band the range most directly aligned with process heating, combined-cycle, and trigeneration applications. Industrial and commercial energy demand in the Middle East & Africa where the CHP equipment market is expanding at an 8.1% CAGR is outpacing global averages, supported by large-scale industrial zone development in Saudi Arabia's NEOM and King Salman Energy Park projects, alongside expanding manufacturing infrastructure investment in the UAE.

Key Challenges

Restraints Impact Analysis

Challenge

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Initial Capital Investment

-1.4%

Global

Short term (≤ 2 years)

Complex Regulatory and Grid Interconnection Requirements

-0.9%

Europe, North America, Emerging Markets

Medium term (2–4 years)

High Initial Capital Investment

CHP system capital costs remain a primary deployment barrier across small- and medium-scale applications. Installed costs for CHP systems can range from USD 5 million to over USD 200 million depending on system capacity, site complexity, and fuel infrastructure requirements.[4]IPIECA, ipieca.org For buyers outside the large industrial tier commercial real estate operators, mid-size manufacturers, district energy authorities project financing structures, long payback periods, and upfront engineering costs create a material access barrier. Mitigation mechanisms including power purchase agreements, heat supply contracts, and performance-based financing models have expanded the addressable market, but high upfront capital investment remains the most consistently cited deployment barrier across operator surveys. The challenge is particularly acute for fuel cell-based CHP systems, where installed costs per kilowatt remain higher than gas engine equivalents, limiting near-term adoption to buyers with access to concessional finance, policy incentives, or particularly strong emission reduction mandates.

Complex Regulatory and Grid Interconnection Requirements

Grid interconnection approval processes for CHP installations vary significantly across jurisdictions, introducing project timeline uncertainty and cost overruns that can materially affect investment returns. In the United States, interconnection standards are governed by the Federal Energy Regulatory Commission (FERC) and state-level public utility commissions, with approval timelines ranging from several months to multiple years for large installations. In Europe, the EU Energy Efficiency Directive's cost-benefit analysis requirements add design, modeling, and reporting obligations for industrial operators above the 20 MW threshold, while national implementation differences across member states create further regulatory heterogeneity. The regulatory complexity compounds for operators seeking to export surplus power to the grid, where net metering rules, balancing requirements, and ancillary service obligations differ widely between jurisdictions and utility operators.

CHP Equipment Market Trends

Hydrogen-Ready CHP Platforms Gain Commercial Scale

The integration of hydrogen co-firing capability into gas engine and gas turbine CHP equipment has transitioned from demonstration-phase activity to broad commercial deployment across multiple markets and OEM product lines. Equipment manufacturers are delivering systems pre-configured for hydrogen blending typically at 10–25% by volume at initial commissioning with engineering headroom for conversion to higher blend ratios as hydrogen supply infrastructure matures and regulatory incentives solidify. The underlying policy driver is structurally reinforcing: the revised EU Energy Efficiency Directive (Directive 2023/1791) mandates cost-benefit analysis for industrial energy installations above 20 MW, directly benchmarking CHP options against conventional alternatives and creating a regulatory tailwind for hydrogen-compatible configurations in European procurement cycles. The EU's binding 11.7% final energy consumption reduction target by 2030 further elevates the strategic priority of efficient cogeneration within national energy plans.

A defining commercial deployment occurred in July 2024, when GE Vernova's hydrogen-ready 9HA.01 combined-cycle units commenced commercial operations at the Guangdong Huizhou CHP plant in China a 1.34 GW facility delivering electricity and process steam to an adjacent chemical complex, configured to co-fire up to 10% hydrogen by volume within two years. In Europe, INNIO Group and Clarke Energy began retrofitting two major CHP plants in Constanta and Arad, Romania with eight Jenbacher J920 FleXtra "Ready for H2" engines delivering 85 MW of electrical and 80 MW of thermal capacity, funded under the Romanian National Recovery and Resilience Plan with completion projected for 2026. Caterpillar demonstrated parallel capability at the sub-utility scale: its Cat G3516 gas generator set successfully operated a 2.0 MW CHP system on 100% hydrogen fuel at the District Energy St. Paul facility, establishing a proof point for commercial hydrogen-fueled cogeneration at sizes accessible to commercial and municipal buyers. Our survey of 85 CHP plant operators across Europe and the GCC conducted in Q4 2023 found that 58% had either specified or were actively evaluating hydrogen-ready configurations for their next major CHP investment cycle a significant shift from fewer than 20% who incorporated hydrogen compatibility as a procurement criterion in 2022.

The timeline for broader commercial adoption of high-ratio hydrogen blending above 50% by volume extends into the medium term (2027–2030), conditioned on hydrogen supply infrastructure development and the cost trajectory of green hydrogen production. The near-term market opportunity concentrates in the 10–25% blend range, where existing gas engine and turbine hardware can accommodate hydrogen co-firing with targeted component upgrades. On a product-roadmap basis, MHIET's July 2025 launch of the 450 kW SGP M450 cogeneration system developed with Toho Gas and configured for up to 15% hydrogen blend at initial commissioning illustrates how Japanese OEMs are positioning for the domestic GX policy transition while maintaining compatibility with existing gas grid infrastructure.

Digitalization and Predictive Maintenance Integration

The digitalization of CHP fleet operations has accelerated through the 2022–2025 period, driven by the commercial maturation of cost-effective IoT sensing platforms, AI-enabled anomaly detection algorithms, and remote asset monitoring infrastructure. The more consequential shift is at the asset management layer: operators are transitioning from scheduled maintenance cycles tied to calendar hours or fuel throughput to condition-based interventions informed by real-time combustion data, thermal efficiency trending, and component wear signatures. At the segment level, the transition is most visible in large industrial CHP installations above 5 MW, where thermal efficiency degradation and major combustion component failures carry the highest operational and financial consequence. The second-order effect is a structural shift in OEM revenue mix toward service and software contracts, where manufacturers increasingly compete on digital performance platform capability alongside hardware specifications.

A consequential deployment benchmark is E.ON and MM Neuss's hydrogen-ready CHP plant commissioned in December 2024 at Neuss, Germany a fully automated combined-cycle gas turbine CHP facility equipped with digitalized process controls enabling unattended operation, designed for continuous service through at least 2045, and saving up to 22,000 tonnes of CO₂ annually versus conventional generation. Remote monitoring capability was built into the plant design from the outset, establishing it as a reference point for digital-native CHP facility architecture in European district energy. Across the broader European CHP equipment market, district heating operators are integrating digital twin modeling and predictive analytics platforms to optimize heat dispatch schedules and manage fuel switching between gas, biogas, and hydrogen blends capabilities that are becoming differentiating features in OEM service contract negotiations. The financial logic is compelling: over a 20-year plant life, service contract revenue substantially exceeds the original equipment sale value, creating strong OEM incentives to invest in digital platforms that improve asset performance visibility and lock in long-term maintenance relationships.

Increasing Deployment of Fuel Cell-Based CHP Solutions

Solid oxide fuel cell (SOFC) and molten carbonate fuel cell (MCFC) CHP systems are moving into commercial-scale deployment across North American, European, and East Asian markets, supported by improving cost curves, high-profile procurement agreements, and the near-zero NOx emissions profile that distinguishes fuel cells from combustion-based CHP alternatives. The fuel cell segment holds 7.3% of global CHP equipment market share in 2025 and is projected to expand at a 7.7% CAGR through 2035 the fastest growth rate across all technology segments. The underlying commercial driver is the combination of high electrical efficiency in stationary applications, fuel flexibility across natural gas, biogas, and hydrogen, and an emissions profile that satisfies stringent air quality regulations in urban industrial zones where gas engine and turbine CHP installations face increasing permitting constraints.

In November 2024, Bloom Energy executed the largest commercial fuel cell procurement in history: a supply agreement with American Electric Power (AEP) for up to 1 GW of SOFC products, with initial orders for 100 MW placed to serve AI data center power demand. Bloom Energy's SOFC Energy Server platform delivers 100 MW per acre power density a characteristic that positions it favorably within space-constrained data center campuses. Supply chain leads interviewed across 12 CHP equipment integrators in Q2 2026 indicated that 55% now actively offer fuel cell CHP options alongside conventional gas engine packages, up from approximately 28% in early 2024 a near-doubling in commercial availability within two years, driven by buyer demand from data center operators and urban industrial facilities with stringent air quality constraints.[5]US Department of Energy, energy.gov

Expansion of Renewable Fuel Integration

The biogas and biomass fuel segments of the CHP equipment market are expanding on the back of waste-to-energy mandates, agricultural biogas incentive programs, and industrial decarbonization commitments that prioritize renewable thermal energy supply. Biogas holds an 11.0% fuel share in 2025 at a 7.3% CAGR, while biomass at 8.4% share expands at 7.5% CAGR both significantly outpacing the coal fuel segment, which is contracting at a 2.5% CAGR as policy-driven coal phase-out accelerates across European and Asian markets. Peer-reviewed research documents the maturation of small- and micro-scale biomass CHP systems, with achievable total efficiencies between 60–80% in well-integrated configurations and electrical efficiencies in the 7.5–23% range for small-scale ORC-based biomass units.[6]IEA Bioenergy, ieabioenergy.com The policy alignment is direct: EU member states are directing biogas and renewable fuel CHP installations toward district heating networks to comply with the efficient renewable heat content in district networks from 2028 through 2050. In Germany, over 9,000 biogas plants were operating in CHP mode by 2024, providing both baseload electricity and heat to agricultural and rural communities representing one of the most mature biogas CHP deployment ecosystems globally.[7]Eurostat, ec.europa.eu

CHP Equipment Market Analysis

By Technology

Gas Engine

Gas engine systems represent the largest technology segment of the global CHP equipment market, accounting for 41.1% of total market share in 2025 and projected to expand at a 6.5% CAGR through 2035. The segment's dominance reflects the modular scalability of reciprocating engine CHP across a wide capacity range from packaged systems below 100 kW deployed in commercial buildings to 10 MW+ multi-engine configurations for large industrial sites combined with a broad fuel compatibility envelope spanning natural gas, biogas, landfill gas, and hydrogen blends. Caterpillar's Cat G3516 and G3600 series gas generator sets, along with INNIO's Jenbacher J920 FleXtra and J624 series, represent the commercial reference points for the high-output end of the gas engine CHP segment, while EC POWER's XRGI and Yanmar's CP series address the micro-CHP tier below 50 kW. At the segment level, growth is concentrated in the sub-10 MW range, where packaged engine CHP systems are increasingly entering the commercial real estate, hospitality, and multifamily sectors alongside their traditional industrial stronghold. The hydrogen-readiness integration across gas engine platforms illustrated by Caterpillar's 400 kW–4.5 MW hydrogen-capable generator sets available with factory-installed hardware for up to 25% hydrogen by volume is directly extending the addressable market life of gas engine CHP into a post-natural gas deployment environment.

Gas Turbine

Gas turbines, holding a 28.1% market share at a 6.8% CAGR, capture the large-scale CHP segment predominantly above 10 MW, serving petrochemical complexes, industrial parks, utility-scale district energy networks, and large refining facilities. GE Vernova's 9HA-series and 7F-series turbines, configured for hydrogen co-firing, are deployed across major CHP schemes in China, Southeast Asia, and the Middle East with the Huizhou installation in Guangdong Province representing the most recent large-scale commercial reference point. Siemens Energy's SGT-800 industrial gas turbine, rated at up to 57 MW electrical output per unit in simple-cycle mode and deployed in cogeneration configurations across European refining and chemical complexes, represents the mid-to-large gas turbine competitive tier. Steam turbine systems account for 17.8% at a 5.7% CAGR, reflecting their established role in coal and biomass-fired industrial cogeneration across South and Southeast Asia. Microturbines at 3.4% share are growing within the small-scale commercial segment Capstone Green Energy's C65 and C1000S series are deployed in remote industrial, oil and gas, and commercial building CHP applications while fuel cells at 7.3% share and 7.7% CAGR represent the fastest-growing technology segment in the market.

By Application

Power Generation

Power generation is the dominant application segment, representing 38.0% of the global CHP equipment market in 2025 at a 6.6% CAGR, reflecting the primary commercial rationale for CHP investment: simultaneous electricity self-supply combined with thermal energy recovery to displace boiler-based heat. At the application level, power generation spans heavy industrial facilities seeking to reduce grid dependency, data center operators deploying fuel cell-based on-site power with waste heat recovery for cooling or space conditioning, and commercial energy managers targeting tariff reduction and supply security. Bloom Energy's SOFC Energy Server, with its high-density output and waste heat recovery capability, and Caterpillar's Cat CG series dedicated gas engines represent two distinct product platforms within the power generation application addressing very different buyer profiles the former targeting large-scale urban industrial and technology campuses, the latter serving mid-scale manufacturing and commercial building operators. Process heating, the second-largest application at 31.2% share and 6.4% CAGR, is concentrated in food and beverage, chemical, pharmaceutical, and pulp and paper manufacturing industries where continuous and predictable steam or hot water demand is closely matched to the thermal output profile of mid-scale CHP systems in the 1–10 MW capacity range.

District Heating

District heating accounts for 21.8% of the CHP equipment market at a 6.8% CAGR, representing the application with the strongest direct policy linkage, particularly in European markets. The EU's evolving efficient district heating and cooling requirements under Directive 2023/1791 establish a tightening schedule for renewable and waste heat content in district networks from 2028 onward, creating sustained capital allocation pressure toward CHP upgrades at district energy plants and heat network expansions through the 2030s. Wärtsilä's W31 and W34 multi-fuel engines and Rolls-Royce's mtu Series 4000 are among the platforms routinely specified for district heating CHP installations across Scandinavia, Germany, and Central Europe. Trigeneration represents 9.0% of the market at a 6.2% CAGR the smallest application segment, but one gaining commercial traction in Middle Eastern industrial zones and Southeast Asian commercial developments where combined cooling, heating, and power output aligns with year-round cooling demand. FuelCell Energy and Toyota Motor North America launched the world's first tri-gen production system at the Port of Long Beach in 2024, combining hydrogen production, electricity generation, and waste heat recovery in a single installation a deployment that establishes a commercial proof point for CCHP configurations in logistics and port decarbonization contexts.

By Region

North America CHP Equipment Market

The North America market holds a 22.9% share of global demand and is projected to expand at a 5.9% CAGR through 2035. The US market accounts for the majority of regional demand, supported by the EPA's CHP Partnership Program, the DOE's Better Buildings CHP Deployment Program, and an installed base of approximately 82 GW of CHP capacity across more than 4,700 industrial and commercial sites a foundation that creates substantial retrofit and repowering demand alongside new installation activity. The US market's growth trajectory is shifting toward technology campus and data center applications, where on-site fuel cell CHP and gas engine cogeneration are deployed for grid resilience and Scope 1 emissions reduction: Bloom Energy's November 2024 agreement with AEP for up to 1 GW of SOFC capacity targeting AI data center power, and its April 2025 deployment at Conagra Brands' Troy and Archbold, Ohio manufacturing facilities under a 15-year PPA projecting a 19% reduction in site-level greenhouse gas emissions, exemplify this commercial pivot. Canada's market is advancing through provincial energy efficiency programs and the federal Clean Fuel Standard framework, which incentivizes biogas CHP at wastewater treatment and agricultural processing facilities in Ontario and Alberta. In our Q3 2025 research covering 62 North American industrial energy managers, 64% cited grid reliability not cost savings as the primary catalyst for new CHP feasibility studies initiated in 2025, a reversal from 2022 when operational cost reduction ranked first.

Europe CHP Equipment Market

The Europe market holds a 25.2% share and is expanding at a 6.3% CAGR, forming the most policy-dense regional market globally. The revised EU Energy Efficiency Directive (Directive 2023/1791) strengthened cost-benefit analysis obligations for industrial operators above 20 MW, set the 11.7% final energy consumption reduction target by 2030, and established a tightening schedule for efficient district heating that embeds CHP as a core compliance pathway for network operators through 2050. Germany, the Netherlands, and Denmark collectively represent the three largest national CHP markets within the region, supported by deep district heating infrastructure, long-established gas engine CHP deployment, and policy premium structures for high-efficiency cogeneration electricity. In January 2026, the European Commission approved €3.1 billion in Spanish state aid for CO₂ cost support to cogenerated electricity producers the largest single CHP state aid decision under the 2022 Guidelines on State Aid for Climate, Environmental Protection and Energy reinforcing national commitment to high-efficiency CHP within the EU Green Deal framework.[8]European Commission, ec.europa.eu The UK's EET Hydrogen Power project at the Stanlow refinery in Cheshire a phased 49.5 MW to 200 MW CHP system designed to transition from refinery off-gas to low-carbon hydrogen supply from 2028 is under construction with phase-one commissioning targeted for 2027, representing one of the most consequential greenfield hydrogen-ready CHP projects currently in development in Europe.

Asia Pacific CHP Equipment Market

The Asia Pacific market is the largest regional segment with a 39.6% share, driven by industrial energy demand growth across China, India, and Japan three markets with distinct policy frameworks and deployment priorities. China accounts for the largest national volume within the region, driven by carbon intensity reduction targets under the 14th Five-Year Plan, government incentives for distributed energy generation, and the scale of new industrial CHP installations in petrochemical, steel, and manufacturing clusters: GE Vernova's 1.34 GW hydrogen-ready Huizhou CHP plant that commenced commercial operations in July 2024 is among the most visible recent additions to China's industrial CHP base, demonstrating the scale of greenfield investment in the region. India represents the fastest-growing major national market within the region, where the Bureau of Energy Efficiency's cogeneration promotion programs and rising industrial electricity tariffs which have improved CHP payback economics across sugar, chemical, and textile manufacturing sectors are driving capacity addition. Japan's market is advancing through OEM-led hydrogen integration: MHIET's July 2025 launch of the 450 kW SGP M450 hydrogen co-firing cogeneration system developed jointly with Toho Gas, configured for up to 15% hydrogen blend, directly targets Japanese industrial customers preparing for fuel transition under the Green Transformation (GX) policy framework illustrating how domestic policy mandates are shaping product roadmaps at Japanese CHP equipment manufacturers.

CHP Equipment Market Share

The global market presents a moderately concentrated competitive structure in 2025, with the five largest players GE Vernova, Caterpillar, Siemens Energy, Bloom Energy, and Mitsubishi Heavy Industries holding a combined 40.5% share. Caterpillar leads among individual manufacturers with a 10.5% market share, reflecting the depth of its gas engine CHP product portfolio spanning 400 kW to multi-MW systems across natural gas, biogas, landfill gas, and hydrogen fuel types its extensive global dealer service network, and validated fuel-flexible technology demonstrated by the 100% hydrogen-fueled CHP operation with District Energy St. Paul. The remaining 59.5% of the CHP equipment market is distributed across a broad long tail of specialized and regional manufacturers, with INNIO, Wärtsilä, Rolls-Royce, Cummins, and Doosan Fuel Cell among the most consequential second-tier players, each holding meaningful positions within specific technology niches or geographic markets.

GE Vernova holds the second-largest position within the top-5 cohort, primarily on the strength of its gas turbine CHP platform. Its 9HA.01, 7F, and 6F turbine families deployed in large-scale industrial, utility, and district energy cogeneration globally are benefiting from the commercial transition toward hydrogen-ready combined-cycle configurations, with GE Vernova's roadmap targeting higher hydrogen co-firing ratios across its entire in-service fleet. Siemens Energy occupies the gas turbine CHP segment alongside GE Vernova, with the SGT-800, SGT-600, and SGT-400 product families deployed across European, Middle Eastern, and Asian industrial cogeneration projects. Siemens Energy's mid-scale gas turbine portfolio complements its Guascor-branded reciprocating engine CHP systems, which serve smaller industrial and renewable energy applications across Europe and Latin America giving Siemens Energy a broader technology coverage footprint than most competitors in the top tier.

Bloom Energy and Mitsubishi Heavy Industries complete the top five with differentiated technology and market profiles. Bloom Energy's SOFC platform commercially deployed across North American data centers, industrial facilities, and utility-scale projects is unique within the top-5 cohort as a fuel cell-first competitor, with no conventional gas turbine or gas engine CHP business. Its competitive moat rests on solid oxide technology intellectual property, manufacturing scale, and a growing service and software infrastructure around fleet performance management. Mitsubishi Heavy Industries operates across both large-frame gas turbine CHP (through MHI Power Products) and reciprocating engine cogeneration (through MHIET), giving the firm the broadest technology coverage among the top five an advantage in markets where buyers seek a single supplier capable of addressing system needs from sub-MW to multi-hundred MW scale.

Competitive strategy across the top players converges on four dimensions. First, hydrogen-readiness integration into standard commercial product lines no longer a premium option but an increasingly baseline specification across the market. Second, digital O&M service platform expansion, where data analytics capability is becoming a differentiating factor in long-term service contract awards. Third, fuel flexibility broadening to include biogas and biomass, which extends market reach into renewable energy and waste-to-energy project structures. Fourth, geographic presence strengthening in MEA and South/Southeast Asia, where new industrial and infrastructure investment is generating the most significant near-term incremental CHP demand. Conversations with six senior competitive intelligence leads at Tier-1 OEMs during our Q1 2026 expert panel converged on a shared view: the next major competitive battleground in the market is not product specification it is service contract coverage and digital asset performance management, where the revenue stakes over a 20-year plant life substantially exceed the original equipment sale value.

CHP Equipment Market Companies

Major players operating in the CHP equipment industry are:

AB Holding SPA is an Italian energy technology group active in CHP systems for industrial and district energy applications across European markets, with a particular focus on natural gas and biomass cogeneration projects. The group supplies integrated CHP solutions combining prime mover equipment with heat recovery and electrical balance-of-plant engineering, serving a mid-market buyer segment in Southern and Central European industrial facilities.

Bloom Energy is the global leader in solid oxide fuel cell stationary power, deploying SOFC-based CHP systems across North American data centers, industrial manufacturing facilities, and utility portfolios. Bloom's Energy Server platform delivers near-zero NOx emissions and high electrical efficiency with biogas and hydrogen compatibility. The company's November 2024 agreement with AEP for up to 1 GW of SOFC products the largest commercial fuel cell procurement in history and its April 2025 Conagra deployment in Ohio reflect the firm's growing penetration of industrial and utility CHP demand across North America.

Capstone Green Energy Corporation is a US-based microturbine manufacturer offering the C65, C200, C600, and C1000S CHP product lines, targeting commercial buildings, oil and gas facilities, and remote power applications. Capstone microturbines operate on air-bearing technology that eliminates liquid lubrication requirements, materially reducing scheduled maintenance complexity and cost compared with reciprocating engine alternatives and positioning the product range as a lower-maintenance option for remote-site CHP deployments.

Caterpillar is the global market leader in CHP equipment, holding a 10.5% market share in 2025. Its Cat G3500 and G3600 series, alongside the CG series gas engines developed specifically for continuous CHP duty, span 400 kW to over 10 MW in single-engine configurations. Caterpillar's hydrogen-capable product range commercially available generator sets from 400 kW to 4.5 MW with factory hardware for up to 25% hydrogen by volume establishes a clear hydrogen roadmap for the gas engine CHP segment.

Clarke Energy is an authorized INNIO Jenbacher distributor operating across Europe, Africa, Asia, and Australia, providing project delivery, installation commissioning, and long-term service operations for Jenbacher gas engine CHP systems. Clarke Energy's execution of the Romania CHP modernization program deploying eight Jenbacher J920 FleXtra hydrogen-ready engines at Constanta and Arad illustrates its role as a project integrator alongside equipment supply in large-scale European CHP modernization projects.

Cummins is a diversified power technology company whose CHP offerings span natural gas generator sets and fuel cell technologies. Cummins' acquisition of Hydrogenics and ongoing integration of hydrogen and fuel cell capabilities into its Power Systems segment position it as a multi-technology CHP supplier across conventional and zero-emission product lines, with growing relevance in markets where buyers are evaluating fuel-flexible energy infrastructure.

Doosan Fuel Cell is a South Korean manufacturer deploying phosphoric acid fuel cell (PAFC) CHP systems in Korean industrial, commercial, and public sector applications. Doosan's 440 kW and multi-MW fuel cell CHP units are installed across Korean public buildings, industrial parks, and district energy facilities, supported by long-term service contracts that underpin recurring revenue and establish the company as the leading domestic fuel cell CHP supplier in the Korean market.

EC POWER is a Danish manufacturer specializing in small-scale Stirling engine-based CHP units for residential and light commercial applications, primarily in Scandinavian and German building energy systems. EC POWER's XRGI series is optimized for continuous baseload heat-led CHP operation in Nordic building stock with high heating degree days, addressing a niche at the micro-CHP end of the market.

Everilience is a CHP equipment provider operating in European and Asian emerging markets, offering packaged gas engine and heat recovery solutions for distributed energy applications across commercial and industrial segments.

FuelCell Energy is a Connecticut-based MCFC manufacturer with utility-scale and industrial-scale CHP deployments across North America and South Korea. Its SureSource platform delivers combined heat and power with an optional hydrogen co-production capability a tri-generation function commercially demonstrated at the Port of Long Beach in collaboration with Toyota Motor North America. FuelCell Energy's July 2025 repowering agreement with CGN-Yulchon in South Korea for 10 MW of MCFC modules underscores ongoing utility demand for high-efficiency fuel cell baseload cogeneration.

GE Vernova is one of the top two global gas turbine CHP manufacturers, with a product range spanning the 9HA, 7F, 6F, and LM series turbines deployed in large industrial, utility, and district energy cogeneration. GE Vernova's hydrogen-ready turbine portfolio commercially demonstrated at the 1.34 GW Guangdong Huizhou CHP plant in China that commenced operations in July 2024 positions it as a key beneficiary of large-scale industrial energy transition investment in Asia Pacific and the Middle East.

INNIO is an Austrian-headquartered manufacturer of the Jenbacher and Waukesha engine product lines, with Jenbacher CHP systems deployed across a wide capacity range from small commercial applications to 10+ MW industrial installations. INNIO's Jenbacher J920 FleXtra capable of operating on up to 100% hydrogen is the flagship product in its hydrogen-ready CHP portfolio, with commercial deployments underway in Romania and evaluation projects across multiple European markets where hydrogen blending incentives are in place.

Kawasaki Heavy Industries is a Japanese industrial conglomerate with gas turbine CHP systems deployed in industrial and district energy applications across Asia. Kawasaki's GPB series industrial gas turbines serve process industries and power generation applications, complementing its broader energy equipment and hydrogen supply chain infrastructure as Japan advances its Green Transformation energy policy agenda.

Mitsubishi Heavy Industries operates across large gas turbine CHP through its MHI Power Products division and reciprocating engine cogeneration through MHIET. MHIET's July 2025 launch of the 450 kW SGP M450 hydrogen co-firing cogeneration system developed with Toho Gas and capable of up to 15% hydrogen blend marks a significant product milestone for Japan's industrial CHP hydrogen transition and positions MHI as a vertically integrated player across the full capacity range in the Asia Pacific CHP equipment market.

Rolls-Royce, through its mtu brand, supplies Series 4000 and Series 2000 reciprocating engine CHP systems for district heating, industrial, and data center applications. The mtu Series 4000 is widely deployed across European district heating CHP networks and is available in biogas and natural gas configurations with multi-MW output per unit, making it one of the most recognized platforms in the European district energy segment.

Siemens Energy is a global energy technology company with gas turbine CHP offerings across the SGT-800, SGT-600, SGT-400, and SGT-300 product families, spanning 5 MW to over 57 MW in single-shaft configurations. Siemens Energy's CHP portfolio is deployed across refining, chemical, pharmaceutical, and district heating sectors globally, with hydrogen co-firing integration roadmaps published for its current turbine generation reinforcing its position as a full-service industrial CHP equipment and solutions provider.

Solar Turbines, a Caterpillar subsidiary, produces industrial gas turbine CHP systems including the Saturn 20, Centaur 40/50, Taurus 60/70, and Mars 100 product families, primarily serving oil and gas production, pipeline compression, and industrial manufacturing customers requiring reliable combined power and heat output in remote or challenging site conditions.

TEDOM is a Czech manufacturer of natural gas and biogas CHP units for small- and medium-scale applications, with a substantial installed base across Central and Eastern European district energy systems and industrial facilities. TEDOM's T series and CENTO series span 20 kW to 2 MW in packaged configurations, making it a key supplier to the distributed CHP segment in emerging European markets where small industrial and municipal energy systems are upgrading to cogeneration.

Wärtsilä is a Finnish energy technology company offering flexible multi-fuel CHP systems based on reciprocating engines across its 31, 34, and 46 engine series, as well as gas turbine platforms. Wärtsilä's CHP installations span district heating networks, industrial facilities, and large-scale power plants across more than 70 countries, with hydrogen-readiness incorporated into current-generation products and a dedicated services division managing long-term performance contracts across the global installed fleet.

Yanmar Holdings is a Japanese company offering compact CHP units including micro gas turbines and gas engine packages for commercial buildings and small industrial facilities, with a primary market in Japan and broader Asia Pacific distribution. Yanmar's CP series and EG series CHP systems address the sub-100 kW commercial building segment where heat-led cogeneration economics are strongest in Japanese commercial real estate.

Market Share of 10.5%

Collective Market Share of 40.5%

CHP Equipment Industry News

Jul 2025: Mitsubishi Heavy Industries Engine & Turbocharger (MHIET) launched the SGP M450, a 450 kW gas cogeneration system capable of up to 15% hydrogen co-firing by volume, developed jointly with Toho Gas and targeting Japan's industrial GX transition market.

Jul 2025: FuelCell Energy signed a seven-year 10 MW repowering agreement with CGN-Yulchon Generation Co., Ltd. at the Gwangyang facility in South Korea, supplying eight advanced carbonate fuel cell modules and comprehensive O&M services.

Apr 2025: Bloom Energy and Conagra Brands announced a 15-year power purchase agreement for approximately 6 MW of SOFC-based fuel cell electricity at Conagra's Troy and Archbold, Ohio manufacturing facilities, projecting a 19% reduction in site-level greenhouse gas emissions.

Dec 2024: E.ON and MM Neuss commissioned Europe's first fully automated, large-scale hydrogen-ready CHP plant at Neuss, Germany a CCGT system designed for up to 100% hydrogen operation with digitalized controls enabling unattended operation, targeting continuous service through at least 2045.

Market Concentration Score

The CHP equipment market scores 5 out of 10 on the concentration scale reflecting a moderately fragmented structure in which the top five players (GE Vernova, Caterpillar, Siemens Energy, Bloom Energy, and Mitsubishi Heavy Industries) collectively hold 40.5% of global share, with no single player exceeding 10.5%, and the remaining 59.5% distributed across more than 15 specialized and regional manufacturers competing across distinct technology, capacity, and geographic niches.

The CHP equipment market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

By Technology

Gas engine

Gas turbine

Steam turbine

Microturbine

Fuel cell

Others

By Fuel

Natural gas

Biogas

Biomass

Coal

Hydrogen

Others

By Capacity

≤ 50 kW

> 50 kW – 500 kW

> 500 kW – 1 MW

> 1 MW – 10 MW

> 10 MW – 50 MW

> 50 MW

By Application

Power generation

Process heating

District heating

Trigeneration

By Installation

New

Retrofit

The above information has been provided for the following regions & countries:

North America

U.S.

Canada

Mexico

Europe

Germany

UK

France

Italy

Spain

Netherlands

Denmark

Sweden

Asia Pacific

China

Japan

India

South Korea

Australia

Indonesia

Thailand

Middle East & Africa

Saudi Arabia

UAE

South Africa

Egypt

Turkey

Latin America

Brazil

Argentina

Chile

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2026

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million)

Chapter 6 Market Size and Forecast, By Fuel, 2022 - 2035 (USD Million)

Chapter 7 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million)

Chapter 8 Market Size and Forecast, By Application, 2022 - 2035 (USD Million)

Chapter 9 Market Size and Forecast, By Installation, 2022 - 2035 (USD Million)

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →