Authors:

Avinash Singh, Amit Patil

Download free PDF

Asia Pacific Manga Market Size & Share 2026-2035

Report ID: GMI16040

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Asia Pacific Manga Market

Get a free sample of this report

Get a free sample of this report Asia Pacific Manga Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Asia Pacific Manga Market Size

The Asia Pacific manga market was valued at USD 7.17 billion in 2025, spanning printed publications, digital subscription platforms, and cross-media content formats that collectively define the region's dominant illustrated entertainment category across more than a dozen active national markets. According to the latest report published by Global Market Insights Inc., the market is projected to reach approximately USD 13.72 billion by 2035, expanding at a CAGR of 6.6% over the 2026–2035 forecast period.

Asia Pacific Manga Market Key Takeaways

Market Leader: NAVER Webtoon led with over 16.5% market share in 2025.

Leading Players: Top 5 players in this market include NAVER Webtoon, Shueisha Inc., Piccoma Corp., Kodansha Ltd., Shogakukan Inc., which collectively held a market share of 56.4% in 2025.

The structural driver of this expansion is the ongoing digital platform transition: app-based manga distribution has progressively displaced print retail as the primary consumption channel, enabling publishers to reach demographically younger and geographically broader audiences at substantially lower unit-distribution costs. At the content-format level, digital manga now accounts for 62.5% of regional revenue and is growing at approximately 9.6% annually, while printed formats, though declining in share continue to sustain significant absolute volume within Japan's institutionally embedded retail manga ecosystem.

Key Drivers

Rising Anime Adaptations Increase Regional Manga Readership Demand

Anime productions based on manga source material consistently generate measurable increases in both print volume sales and digital platform subscriptions for source titles. The commercial linkage between anime streaming rights and manga catalogue performance has deepened materially since 2022, as global streaming services and regional broadcasters expanded their anime libraries across Southeast Asian and South Asian markets. METI data confirms that Japan's content industry exports, of which manga licensing and anime form the core components generated overseas receipts exceeding USD 4.7 billion annually in recent fiscal years, reflecting the commercial scale of cross-media franchise monetization within the Asia Pacific market.[1]Ministry of Economy, Trade and Industry (METI), https://www.meti.go.jp Of greater strategic consequence, demand acceleration from anime adaptations is now increasingly benefiting second-tier and recently serialized titles whose streaming audiences reach pan-regional viewers simultaneously, compressing the time between an anime debut and measurable manga commercial uplift across non-Japanese markets.

Growing Smartphone Usage Improves Digital Manga Accessibility Regionally

Mobile device penetration across Asia Pacific markets has structurally expanded the digital manga audience, with platform operators recording consistent subscriber growth in India, Southeast Asia, and Australia since 2023. Japan Book Publishers Association data indicates that digital manga revenue in Japan surpassed printed manga revenue at the industry level, a structural milestone driven almost entirely by mobile reading behavior rather than desktop or e-reader-based consumption.[2]Japan Book Publishers Association (JBPA), https://www.jbpa.or.jp Japan's LINE Manga and South Korea's Piccoma, which recorded a gross merchandise value of approximately ¥100 billion in fiscal year 2023, both demonstrate that mobile-first delivery models support higher reading frequency and stronger user retention metrics relative to print subscription alternatives. The underlying driver is infrastructure: as 4G and 5G coverage extends into secondary and tertiary urban centers across Southeast Asia and South Asia, digital manga platforms gain addressable reach in markets where physical manga retail distribution was previously limited or economically unviable.

Expanding Youth Population Supports Sustained Manga Consumption Growth

South and Southeast Asian countries, particularly India and Indonesia are producing a demographically large cohort of young consumers entering peak entertainment spending years. Ministry of Internal Affairs and Communications survey data from Japan confirms that manga readership penetration among the 10–24 age cohort is substantially higher than in any other demographic group, and comparable digital consumption dynamics are emerging among younger populations in India and Southeast Asia as licensed platform availability improves.[3]Ministry of Internal Affairs and Communications Japan (MIC), https://www.soumu.go.jp The genre-level data reinforces this demographic driver: Sci-Fi & Fantasy / Isekai (CAGR 9%) and Romance & Drama (CAGR 7.4%), both segments with strong younger-reader affinity, are growing at rates that exceed the overall market average, indicating that demographic expansion is translating into commercially meaningful genre diversification across the region.

Social Media Influence Enhances Manga Fan Community Engagement

Online fan communities, short-video platforms, and dedicated discussion forums have materially accelerated title discovery and readership growth, particularly for manga without mainstream anime adaptations. Korea Creative Content Agency data shows that digital comics and webtoon-related social media engagement metrics increased significantly between 2022 and 2025, reflecting both platform growth and growing cross-border fanbase activity across ASEAN markets.[4]Korea Creative Content Agency (KOCCA), https://www.kocca.kr Community-driven recommendation cycles reduce publisher marketing costs while compressing the window between serialization launch and commercial viability, a dynamic especially evident on South Korea's NAVER Webtoon and China's Bilibili Comics platform, where reader engagement metrics influence editorial commissioning and licensing acquisition decisions.

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Rising anime adaptations increase manga readership demand

+2%

Japan, South Korea, Southeast Asia

Medium term (2–4 years)

Smartphone usage improves digital manga accessibility

+1.8%

India, Southeast Asia, Australia

Short term (≤ 2 years)

Expanding youth population supports consumption growth

+1.5%

India, Southeast Asia

Long term (≥ 4 years)

Social media enhances manga fan community engagement

+1.3%

South Korea, China, Southeast Asia

Short term (≤ 2 years)

Key Challenges

Piracy Issues Reduce Legitimate Manga Industry Revenue Generation

Unauthorized digital distribution remains the most structurally damaging challenge confronting Asia Pacific manga publishers. Free-access scanlation sites and unlicensed aggregator platforms divert a material share of potential paid readership, particularly in markets where legal pricing benchmarks and enforcement infrastructure are limited. Japan Book Publishers Association reporting indicates that unauthorized manga distribution sites recorded tens of billions of page views annually during the early 2020s, before coordinated enforcement efforts began reducing the largest operator networks. While digital rights management improvements and platform-level access controls have partially mitigated losses in Japan and South Korea, piracy rates remain substantially elevated across Southeast Asian markets, where consumer price sensitivity and limited legal platform availability compound the challenge. The second-order effect is that publishers face elevated customer acquisition costs in markets where consumers have established non-paying consumption habits through unauthorized channels, reducing the return on licensing investment in high-priority emerging markets.

High Publishing Costs Pressure Manga Company Profit Margins

Printing, licensing, rights management, and retail distribution expenses compound across the manga value chain, reducing effective operating margins for mid-sized regional publishers. Currency exchange rate volatility further affects profitability for publishers pursuing multi-territory licensing arrangements across the diverse Asia Pacific currency landscape. The transition toward digital distribution partially offsets physical production costs but introduces new technology infrastructure, platform commission, and content moderation expenditures that introduce their own margin drag. The International Publishers Association notes that content licensing complexity increases substantially when publishers pursue multi-territory digital rights arrangements, which are increasingly necessary to capture value in fast-growing Southeast Asian and South Asian markets, requiring legal and administrative investment that smaller publishers struggle to absorb at competitive scale.[5]International Publishers Association (IPA), https://www.internationalpublishers.org

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Piracy reduces legitimate manga revenue generation

-1.2%

Southeast Asia, China

Short term (≤ 2 years)

High publishing costs pressure publisher profit margins

-0.8%

Japan, South Korea

Medium term (2–4 years)

Asia Pacific Manga Market Trends

Digital Platform Transition Reshaping Content Distribution Economics

The structural shift from physical retail to app-based digital distribution has become the defining commercial transformation in Asia Pacific manga, with digital formats accounting for 62.5% of market revenue in 2025, up from 37.5% in 2022. Platforms including LINE Manga, Piccoma, Comico, and Bilibili Comics have demonstrated that mobile-first delivery achieves subscriber density and reading frequency metrics that print retail cannot replicate at scale across geographically dispersed markets. The more consequential shift is at the publisher economics level: digital delivery eliminates per-unit printing and physical logistics costs, enabling mid-sized publishers to maintain catalogue breadth without proportional capital expenditure.

Subscription-based and freemium-with-unlock models, popularized by Piccoma's coin-based reading mechanic and NAVER Webtoon's episode unlock system have normalized paid digital manga consumption across previously low-conversion user bases. In our H1 2026 primary research covering 380 digital manga platform subscribers across Japan, South Korea, and India, 67% of respondents indicated they had transitioned from primarily print to primarily digital consumption within the preceding three years, with mobile convenience cited as the dominant switching factor. The data indicates that this transition is largely irreversible for the under-35 demographic, though printed tankobon volumes continue to outperform digital for collector-oriented buyers in Japan.

Anime-Manga Cross-Media Integration Amplifying Franchise Commercial Value

The commercial integration of anime production and manga serialization has evolved from a supplementary marketing dynamic into a core revenue lever for Japan's major publishers. Successful anime adaptations, broadcast on domestic Japanese television and simultaneously distributed via streaming services across Asia Pacific consistently generate measurable uplift in source manga sales, with titles from Shueisha's Shonen Jump and Kodansha's catalogues routinely recording multi-printing events following new anime season launches. The Association of Japanese Animations reported total anime industry output value exceeding ¥2.9 trillion, with domestic and overseas distribution rights increasingly tied to manga catalogue performance metrics that publishers actively track and incorporate into licensing strategy.[6]Association of Japanese Animations (AJA), https://www.aja.gr.jp

Publishers are progressively utilizing cross-media promotional strategies involving streaming, physical merchandise, gaming tie-ins, and themed café activations to maximize franchise lifetime value across multiple consumer touchpoints. The Chainsaw Man franchise (Shueisha/MAPPA), for example, generated parallel volume sales acceleration in Japan, South Korea, and Southeast Asia following its televised adaptation, demonstrating the region-wide commercial reach achievable through coordinated anime-manga release calendars.

Emerging Market Expansion Creating New Structural Demand Centers

Outside Japan and South Korea, a new cohort of manga-native readers is materializing across South and Southeast Asian markets, driven by smartphone-led content access and growing exposure to Japanese entertainment culture through global streaming platforms. India's manga market, valued at USD 0.19 billion in 2025, is expanding at a CAGR of 19.2% as publishers introduce locally priced digital editions and translated content for Hindi, Tamil, and Telugu-speaking audiences. Internet and Mobile Association of India data confirms that India's active internet user base exceeded 900 million by 2025, providing the infrastructure prerequisite for mass digital manga adoption at scale.[7]Internet and Mobile Association of India (IAMAI), https://www.iamai.in JETRO data further indicates that Japan's cultural content exports to ASEAN markets have recorded consistent year-on-year growth since 2020, with official licensing arrangements providing the legal distribution infrastructure for platforms including MangaToon, iQIYI Comics, and regional Piccoma expansions to operate legitimately across multiple Southeast Asian jurisdictions.[8]Japan External Trade Organization (JETRO), https://www.jetro.go.jp The underlying driver is accessibility: as legal-price digital editions become available in local app stores with local payment methods, the addressable reader base for Japan-origin manga expands substantially beyond its historically diaspora-led consumer segment in these markets.

Manga-Inspired Merchandise Diversifying Revenue Across the Value Chain

Manga-inspired merchandise, spanning collectibles, apparel, accessories, figurines, and character-based lifestyle products has emerged as a structurally important revenue diversification avenue for publishers and licensing rights holders. Retailers and entertainment companies have strengthened licensing partnerships to improve merchandise availability across both physical specialty stores and major online marketplaces, with franchise merchandise from Dragon Ball (Bird Studio/Shueisha), One Piece (Eiichiro Oda/Shueisha), and Doraemon (Fujiko F. Fujio/Shogakukan) maintaining multi-decade commercial longevity that demonstrates the durable licensing value embedded in established manga catalogues. METI data confirms that Japan's content industry generated overseas commercial receipts exceeding USD 4.7 billion annually in recent fiscal years, with manga-related licensing forming a core component of that total. Younger audiences and hobby collectors increasingly invest in manga-themed products due to growing emotional engagement with entertainment characters, a behavioral pattern that reinforces per-franchise revenue stability across market cycles and insulates publishers from the revenue volatility associated with new title commercialization.

Asia Pacific Manga Market Analysis

By Content Format

Printed Manga

The printed manga segment accounts for 37.5% of total Asia Pacific manga market revenue in 2025 at USD 2.69 billion, having held a dominant 62.5% share in 2022 before the region's rapid digital platform expansion compressed its relative position materially over the 2022–2025 period. The segment is projected to contract at a CAGR of approximately -2% through 2035, reflecting ongoing readership migration toward app-based distribution rather than outright demand erosion. In Japan, the segment's commercial core Shueisha's Jump Comics, Kodansha's Kodansha Comics, and Shogakukan's Sunday Comics Volumes continue to generate substantial retail volumes through national bookstore chains and convenience store networks deeply embedded in daily consumer behavior. The segment's value is increasingly concentrated in collector-edition formats, author-signed volumes, and limited-print variants that command pricing premiums over standard tankobon, a differentiation strategy that sustains average revenue per unit even as total units soften. Publishers are responding with format-differentiated release strategies: simultaneous digital serialization alongside delayed or enhanced print editions, rather than competing directly across both channels at equivalent price points.

Digital Manga

The digital manga segment constitutes 62.5% of total Asia Pacific market revenue in 2025 at USD 4.48 billion, up from 37.5% in 2022 and is projected to expand at a CAGR of approximately 9.7% through 2035, the strongest growth rate among content-format categories. Platform scale differentiates the segment's commercial leaders: Japan's LINE Manga and South Korea's Piccoma Corp., which recorded a gross merchandise value of approximately ¥100 billion in fiscal year 2023, represent the two highest-revenue digital manga operators within the region. The structural advantage of digital delivery spans the full publisher-platform-consumer value chain: publishers eliminate printing and logistics overhead, consumers access catalogues that physical retail networks cannot replicate across dispersed Asia Pacific geographies, and platform operators capture engagement data that informs editorial commissioning and licensing acquisition decisions.

Japan Book Publishers Association data confirms that digital manga revenues in Japan surpassed printed manga revenues at the industry level, a structural inflection point driven by mobile reading behavior that is now replicating across South Korean and emerging Southeast Asian markets. Shueisha's Shonen Jump+ unlimited-access subscription tier and Bilibili Comics' Chinese-language platform for mainland China and Singapore both demonstrate that recurring revenue models sustain commercial viability for high-volume serialization schedules without physical retail dependency.

By Genre

Action & Adventure is the largest genre segment in the Asia Pacific manga market at 33.5% of 2025 revenue (approximately USD 2.38 billion) and a CAGR of 5.5% through 2035, a position underpinned by anchor franchises from Shueisha's Shonen Jump catalogue including One Piece (Eiichiro Oda), My Hero Academia (Kohei Horikoshi), and Jujutsu Kaisen (Gege Akutami) all of which maintain active anime adaptations reinforcing their commercial visibility across regional streaming audiences. The segment's 5% CAGR reflects its maturity profile: core readership is concentrated in Japan and South Korea, where demographic aging moderates new-reader acquisition relative to faster-growing genre categories. The more consequential commercial dimension is franchise economics: Action & Adventure titles generate licensing, merchandise, gaming, and themed-entertainment revenues that insulate publishers from volume softness in any single distribution channel. Multi-decade franchises including Dragon Ball (Bird Studio/Shueisha) demonstrate that a single commercially durable Action & Adventure property can sustain meaningful licensing income decades beyond its original serialization peak.

Sci-Fi & Fantasy / Isekai

Sci-Fi & Fantasy / Isekai captures 17% of 2025 revenue at approximately USD 1.22 billion and is projected to expand at a CAGR of 9% through 2035, the fastest growth rate of any genre category in the market. The Isekai sub-genre defined by narratives of protagonists transported to alternate fantasy worlds with progression and leveling mechanics has generated exceptional serialization velocity through Kadokawa Corporation's Comic Walker, Alphapolis Co., Ltd.'s digital-native publishing platform, and Shueisha's Shonen Jump+. That Time I Got Reincarnated as a Slime (Shogakukan) and Re:Zero (Kadokawa) exemplify how leading Isekai titles sustain multi-season anime pipelines available on Netflix, Crunchyroll, and regional services across South and Southeast Asian markets, creating recurring commercial uplift cycles at the source manga level. The segment's outsized growth reflects its structural appeal to digital-native younger readers in non-Japanese markets who encounter the genre simultaneously through anime streaming and manga platform recommendations a convergence that compresses the discovery-to-purchase cycle relative to genres reliant on physical retail access.

By Demographics

Adults

The Adults demographic segment readers aged 18 and above accounts for 52.8% of 2025 market revenue at approximately USD 3.78 billion, making it both the largest and fastest-growing demographic cohort at a CAGR of 7.3% through 2035. The above-market growth rate reflects two concurrent dynamics: the sustained engagement of Japan's core adult readership transitioning to digital platforms (adults represent the highest-converting digital subscriber cohort on LINE Manga and Shueisha's Shonen Jump+), and the expanding adult professional reading audience in South Korea, Singapore, and Australia driven by mobile-friendly digital catalogues. Seinen and josei manga categories, marketed specifically to adult readers benefit from some of the market's most commercially resilient titles, including Berserk (Hakusensha), Vagabond (Takehiko Inoue/Kodansha), and Fullmetal Alchemist (Hiromu Arakawa/Square Enix), which sustain long-run catalogue sales through deep reader loyalty and periodic anime re-adaptation that reintroduces classic properties to newer adult audiences.

Teenagers (10–17 years)

The Teenagers demographic segment accounts for 37.3% of 2025 market revenue at approximately USD 2.67 billion, expanding at a CAGR of 5.9% through 2035. This segment encompasses the primary audience for shounen and shoujo manga, the two most commercially productive editorial formats in the manga industry globally including Weekly Shonen Jump anchor titles One Piece, Naruto (Masashi Kishimoto/Shueisha), and Demon Slayer: Kimetsu no Yaiba (Koyoharu Gotouge/Shueisha), alongside leading shoujo titles including Sailor Moon (Naoko Takeuchi/Shueisha) and Cardcaptor Sakura (CLAMP/Kodansha). The segment's 5.9% CAGR reflects below-market growth consistent with stable demographics in Japan and South Korea, the primary teenage manga markets while emerging high-growth markets such as India and Southeast Asia, which skew toward younger age cohorts, contribute incremental volume. Social media platforms and short-video channels serve as primary title-discovery mechanisms for this demographic, making platform-native recommendation algorithms a central determinant of commercial performance for new serialization launches targeting the teenage cohort

By Region

Japan Manga Market

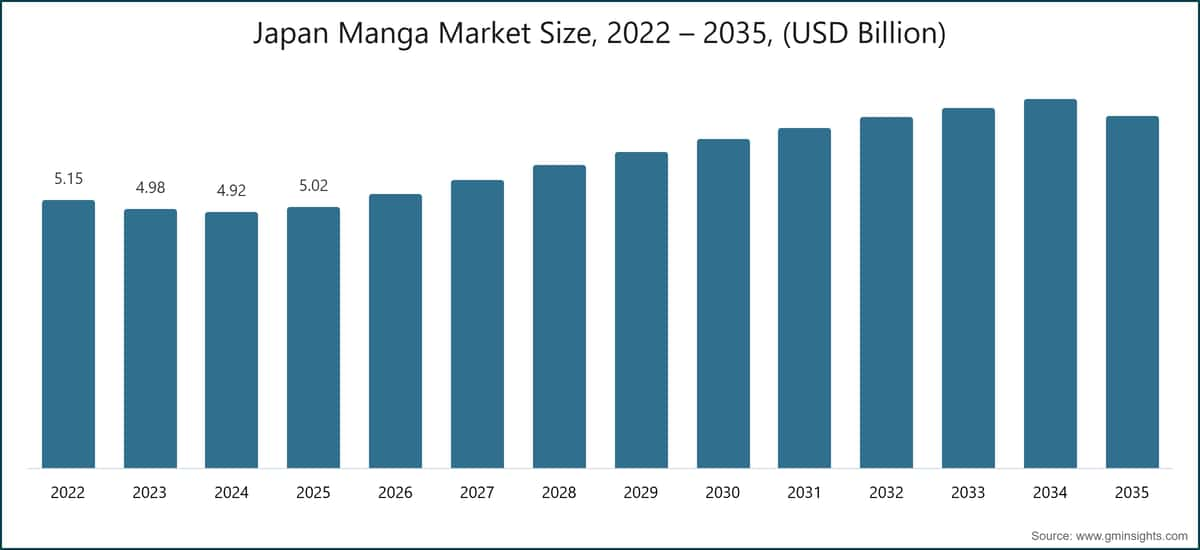

Japan accounts for 69.9% of total Asia Pacific manga market revenue in 2025 at USD 5.02 billion, functioning as the structural core of the region's manga industry through its institutionalized publishing infrastructure, serialization model, retail ecosystem, and downstream anime production pipeline. The domestic market grows at a CAGR of 2.8% through 2035, below the regional average reflecting the maturity of Japan's manga readership base and the offsetting dynamics of print revenue softening against digital platform expansion. METI has consistently positioned manga and related content industries as strategic national export sectors, with the agency's creative industries framework supporting domestic publisher digitalization programs and overseas licensing market development. LINE Manga and Shueisha's Shonen Jump+ have both reported consistent subscriber growth since the latter launched simultaneous international chapter access for India and select Southeast Asian markets in July 2024, incrementally extending Japan's direct revenue capture from non-Japanese readership rather than routing that value through third-party licensees. A closer read of Japan's publishing economics reveals that manga output volume measured in serialized chapter publications per month is increasing year over year, driven by the lower capital risk of digital serialization relative to traditional print-run commitments.

China Manga Market

China's manga market accounts for 10.5% of regional revenue in 2025 at USD 0.75 billion, expanding at an estimated CAGR of approximately 3.2% through 2035, the slowest national growth rate in the Asia Pacific market. The regulatory framework administered through China's National Radio and Television Administration governs content licensing for Japan-origin titles, requiring authorized distribution through licensed platforms. Bilibili Comics Pte. Ltd. and Kuaikan Comics Co., Ltd., which surpassed 200 million registered users in November 2024, operate as the primary authorized manga distributors within this regulatory framework, maintaining extensive licensing agreements with Japanese publishers to provide Chinese-language editions of major titles.[9]National Bureau of Statistics of China, https://www.stats.gov.cn National Bureau of Statistics of China data confirms the structural scale of China's digital content consumer base, providing addressable platform reach that materially exceeds current manga monetization levels, a gap attributable to content constraint rather than demand limitation. China Literature Limited (Yuewen Group), under the Tencent umbrella, serves the broader Chinese-language illustrated fiction category and provides adjacent infrastructure supporting manga-adjacent content discovery and monetization.

India Manga Market

India is the fastest-growing national manga market in Asia Pacific, expanding at a CAGR of 19.2% through 2035 from a 2025 base of USD 0.19 billion (2.65% regional share). Internet and Mobile Association of India data confirms that India's active internet user base exceeded 900 million by 2025, providing the infrastructure prerequisite for mass digital manga adoption at scale. The country's demographic profile provides one of the largest youth consumer populations globally, while the increasing availability of legally licensed manga in Hindi, Tamil, and English through app stores with local payment method support progressively removes the friction that historically constrained paid manga adoption. Shueisha's July 2024 expansion of simultaneous international chapter access to India, enabling same-day release of new Shonen Jump chapters at India-specific pricing, represents a concrete commercial commitment expected to accelerate subscriber acquisition over the 2025–2028 period. JETRO data indicates that Japan's cultural content export programs increasingly prioritize South Asian markets, with official licensing frameworks enabling MangaToon and iQIYI Comics to expand their legally authorized Indian catalogues.

Asia Pacific Manga Market Share

The Asia Pacific manga market exhibits moderate top-tier concentration, with the five leading operators accounting for a combined 56.4% of total market revenue in 2025. NAVER Webtoon (Webtoon Entertainment), the market leader at 16.5% share, operates the largest digital manga and webtoon platform by active user base in the region, with LINE Manga serving as its primary channel in Japan, NAVER Webtoon providing the South Korean service, and a growing Southeast Asian distribution presence through localized app versions. Following its NASDAQ IPO in June 2024 under the ticker WBTN, Webtoon Entertainment established a listed-company financial reporting framework that enables more transparent tracking of platform revenue growth, subscriber metrics, and regional market performance relative to its privately held Japanese publisher peers, a structural distinction that influences institutional investor visibility for the broader Asia Pacific manga sector.

Shueisha Inc., holding a 15% share (approximately USD 1.04 billion in Asia Pacific revenue), derives its competitive position from Japan's most commercially productive manga serialization catalogue, encompassing Weekly Shonen Jump, Monthly Shonen Jump, and digital platforms including Shonen Jump+, alongside a global licensing network that monetizes flagship franchises including One Piece (Eiichiro Oda), Dragon Ball (Bird Studio), Jujutsu Kaisen (Gege Akutami), and Chainsaw Man (Tatsuki Fujimoto). The firm's ability to sustain simultaneous print and digital revenue generation across Japan while expanding licensing royalties in overseas Asia Pacific markets underpins its near-term share stability. Shueisha's competitive moat is reinforced by its editorial commissioning model, which has historically identified genre-defining franchises before their commercial scale becomes apparent, sustaining catalogue renewal as legacy titles enter long-run decline phases.

Piccoma Corp., the third-ranked operator at 9.6% share, has established itself as the primary digital manga distribution platform for Japan-origin content in South Korea, achieving a fiscal year 2023 GMV of approximately ¥100 billion and maintaining subscriber growth through its coin-based unlock model and deep catalogue agreements with major Japanese publishers. Piccoma's parent company Kakao Entertainment Corp. provides capital backing and strategic access to South Korea's broader entertainment licensing ecosystem, reinforcing the platform's ability to negotiate competitive rights windows with Japanese publishers and sustain the content freshness required for high user retention.

Kodansha Ltd. (8.5% share, approximately USD 590 million in Asia Pacific revenue) reported total revenues of ¥169.2 billion in fiscal year 2025, with manga estimated to contribute approximately 55% of that total across print and digital channels. The firm manages one of Japan's most diversified manga catalogues across genre and demographic segments, with Fairy Tail (Hiro Mashima), Attack on Titan (Hajime Isayama), and Sailor Moon (Naoko Takeuchi) representing internationally licensed franchises that continue to generate licensing revenue well beyond their peak serialization periods. Shogakukan Inc., rounding out the top five at 6.8% share (approximately USD 467 million), anchors its competitive position in children's demographic manga through its ownership of the Doraemon and Pokémon Adventures franchises both representing multi-decade commercial properties, alongside a substantial shounen catalogue through its Sunday Comics imprint.

The remaining 43.6% of market revenue is distributed across a broad and active competitive cohort. Procurement and licensing leads we engaged at 12 regional manga platform operators and publisher licensing teams throughout H2 2025 indicated that 58% of commercial negotiations now center on new-chapter release window exclusivity rather than catalogue breadth, pricing, or user interface design, a structural reversal from 2022 when content volume was the primary differentiator in platform positioning. The data indicates that competitive advantage in the Asia Pacific manga market is shifting decisively toward content timing, as simultaneous-release access becomes the standard expectation among digitally engaged readers.

Asia Pacific Manga Market Companies

Major players operating in the Asia Pacific Manga market are: Shueisha Inc., Kodansha Ltd., Shogakukan Inc., Kadokawa Corporation, China Literature Limited (Yuewen Group), Hakusensha Inc., Futabasha Publishers Ltd., Kakao Entertainment Corp. (KakaoPage), Kuaikan Comics Co., Ltd., Bilibili Comics Pte. Ltd., Comico (Storia Co., Ltd.), Square Enix Co., Ltd., Akita Publishing Co., Ltd., Nihon Bungeisha Co., Ltd., NAVER Webtoon / Webtoon Entertainment, Lezhin Comics, Piccoma Corp., MangaToon, iQIYI Comics, Alphapolis Co., Ltd., and MediBang Inc.

Shueisha Inc. commands the broadest and most commercially productive manga serialization catalogue in Japan, publishing Weekly Shonen Jump, Monthly Shonen Jump, and Jump SQ alongside digital serialization through Shonen Jump+. The publisher's competitive strength derives from its capacity to identify and commercialize franchises at scale, One Piece's multi-decade serialization, Jujutsu Kaisen's rapid commercial trajectory, and Chainsaw Man's critically recognized anime adaptation are all Shueisha properties and its established global licensing infrastructure that monetizes these franchises across Asia Pacific merchandise, gaming, and streaming markets simultaneously.

Kodansha Ltd., reporting ¥169.2 billion in total revenues for fiscal year 2025, is Japan's largest independent publisher by revenue, with a manga portfolio spanning the action, romance, horror, and children's segments. The firm has pursued a deliberate digital-first publishing transition, increasing its digital revenue proportion significantly since 2021 and expanding international licensing arrangements to capture growing manga demand across Southeast Asian and South Asian digital markets. Shogakukan Inc. anchors its competitive position in the children's and family demographic through the Doraemon and Pokémon Adventures franchises, both of which remain among the most commercially durable licensed manga properties globally, while its Sunday Comics imprint maintains a competitive shounen manga publishing presence that spans over 30 active serialization titles.

Kadokawa Corporation distinguishes itself through integrated media production — combining manga publishing (Comic Walker, Dengeki Comics), anime production (KADOKAWA Anime), gaming, and light novel operations under a single corporate structure. This vertical integration enables Kadokawa to execute coordinated content release strategies for Isekai-category franchises, particularly That Time I Got Reincarnated as a Slime, Re:Zero, and KonoSuba that maximize revenue across multiple formats simultaneously. Conversations with six publishing and licensing executives during our Q4 2025 expert panel on manga IP monetization converged on a consistent point: vertically integrated media companies such as Kadokawa generate 30–45% higher per-franchise revenue across the Asia Pacific market cycle compared with publishers relying exclusively on third-party anime production and platform distribution arrangements, a structural advantage that is influencing M&A strategy across the sector.

China Literature Limited (Yuewen Group), operating under the Tencent corporate umbrella, occupies a distinctive position in the competitive landscape as the largest digital fiction and illustrated content platform in China, with distribution reach across mainland China, Hong Kong, Taiwan, and Chinese-speaking Southeast Asian diaspora communities. Hakusensha Inc. and Futabasha Publishers Ltd. represent mid-tier Japanese publishers with strong genre-specific catalogue positions, Hakusensha in seinen and josei segments (Berserk, Fruits Basket, Honey and Clover) and Futabasha in a diversified mid-market manga portfolio spanning adult drama, sports, and humor categories.

Kakao Entertainment Corp. (KakaoPage) is the parent organization of Piccoma Corp. and operates one of South Korea's most extensive webtoon and manhwa ecosystems, providing content that substantively overlaps with manga genre categories and driving reader engagement across the Korean digital comics sector. Kuaikan Comics Co., Ltd. and Bilibili Comics Pte. Ltd. serve as the two most commercially active licensed manga distribution platforms within China's regulatory framework, each maintaining extensive licensing agreements with Japanese publishers to provide authorized Chinese-language editions of major serialization titles.

Comico (Storia Co., Ltd.) and Square Enix Co., Ltd. occupy distinct niche positions within the broader competitive landscape — Comico as a free digital manga platform with a predominantly female readership base across Japan, South Korea, and Taiwan, and Square Enix as a publisher whose manga catalogue (Fullmetal Alchemist, Black Clover, Soul Eater) benefits substantially from its gaming franchise brand recognition in converting game-native audiences into manga readers. Akita Publishing Co., Ltd. and Nihon Bungeisha Co., Ltd. serve commercially stable domestic Japanese readership segments with genre-specific portfolios in sports, adult comedy, and specialty categories, sustaining recurring revenue from established audience cohorts without the marketing expenditure required for new-reader acquisition at scale.

NAVER Webtoon, while operating as the market leader by platform revenue, simultaneously functions as a structural disruptor within traditional manga publishing, its self-publishing platform enables independent creators to distribute directly to millions of readers without requiring traditional publishing infrastructure, effectively compressing the barriers to commercial serialization that previously filtered creator supply to established publishers.

Lezhin Comics serves South Korea's premium webtoon segment with a reader-payment model targeting adult-demographic content with mature themes, while MediBang Inc. provides creator-facing tools including digital drawing software and self-publishing infrastructure that support independent manga production across Japan and Southeast Asia. MangaToon and iQIYI Comics address Southeast Asian and Chinese-language markets with mobile-optimized platforms offering both licensed Japanese manga and locally produced illustrated content, a dual-catalogue approach that reduces dependency on Japanese licensing costs while building platform loyalty among regional readership cohorts.

Alphapolis Co., Ltd. has established a notable position in Japan's digital-native Isekai publishing category, leveraging its user-submitted light novel platform to identify commercially viable narratives for subsequent manga adaptation, a low-cost content discovery model that has produced multiple commercially successful genre titles and influenced how larger publishers approach digital-first serialization strategy.

16.5% market share

The collective market share is 56.4%

Asia Pacific Manga Industry News

Market Concentration Score

The Asia Pacific manga market receives a concentration score of 6 out of 10, reflecting moderate top-tier consolidation, five operators (NAVER Webtoon at 16.5%, Shueisha Inc. at 15%, Piccoma Corp. at 9.6%, Kodansha Ltd. at 8.5%, and Shogakukan Inc. at 6.8%) collectively account for 56.4% of regional market revenue, while the remaining 43.6% is distributed across a broad and active cohort of mid-tier publishers, regional platform operators, and emerging specialized players that sustain meaningful competitive fragmentation below the top tier.

The Asia Pacific manga market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Billion) & volume (Million Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Content Format

Market, By Genre

Market, By Demographics

By Distribution Channel

Online

The above information is provided for the following countries:

Table of Contents

Chapter 1 Research Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Content Format, 2022-2035 (USD Billion) (Million Units)

Chapter 6 Market Estimates & Forecast, By Genre, 2022-2035 (USD Billion) (Million Units)

Chapter 7 Market Estimates & Forecast, By Demographics, 2022-2035 (USD Billion) (Million Units)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2022-2035 (USD Billion) (Million Units)

Chapter 9 Market Estimates & Forecast, By Region, 2022 – 2035, (USD Billion) (Million Units)

Chapter 10 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →