Market Size By Product (Holter Monitors, Smartwatches, Patch, Defibrillators, Pulse Oximeters, Other Products), By Application (Coronary Artery Disease (CAD), Cardiomyopathies, Post-myocardial Infarction, Congenital Heart Diseases, Post-surgical Cardiac Care, Other Applications), By End Use (Hospitals, Specialty Centers, Home Care Settings, Other), Growth Forecast. The market forecasts are provided in terms of value (USD Million).

Report ID: GMI4711

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Wearable Cardiac Devices Market Size

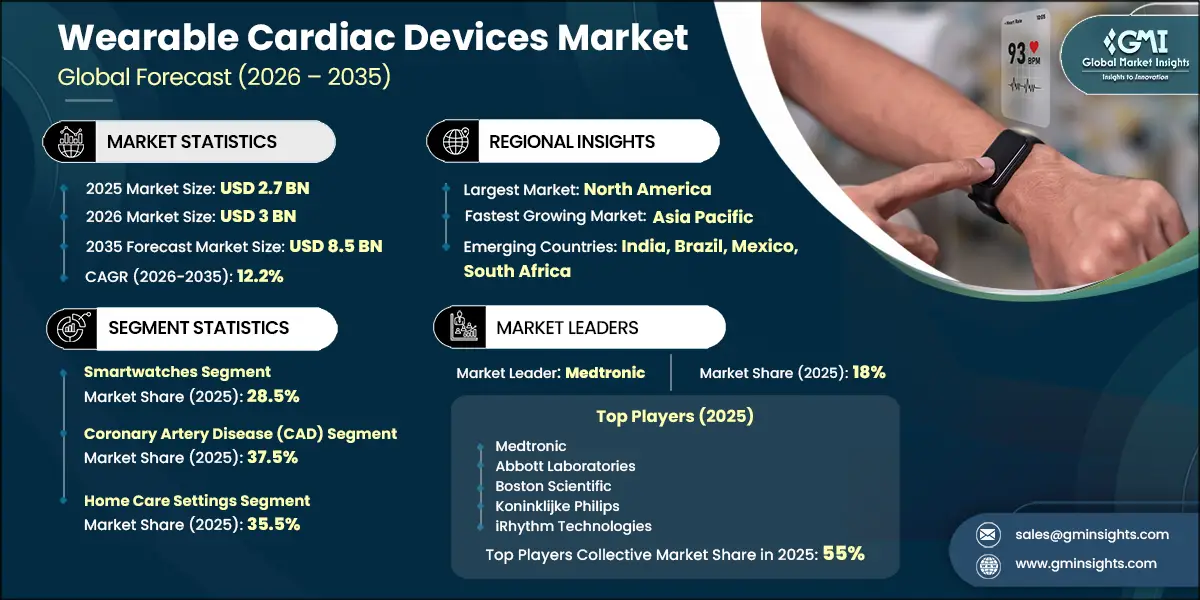

The global wearable cardiac devices market was valued at USD 2.7 billion in 2025 and is projected to grow from USD 3 billion in 2026 to USD 8.5 billion by 2035, expanding at a CAGR of 12.2%, according to the latest report published by Global Market Insights Inc.

This fairly considerable growth is driven by numerous factors such as increasing number of patients suffering from cardiovascular diseases, rapid technological advancements in wearable cardiac devices, growing preference of minimally invasive devices, and rising health consciousness and preventive care.

Wearable cardiac devices are advanced medical technologies designed to continuously monitor, diagnose, and manage cardiovascular conditions outside of traditional clinical settings. These devices incorporate technologies such as electrocardiography (ECG), biosensors, wireless connectivity, and digital signal processing to track heart rate, heart rhythm, and other vital cardiac parameters in real time. Wearable cardiac devices enable clinicians to detect conditions such as arrhythmias, atrial fibrillation, ischemic events, and heart failure at earlier stages. By facilitating continuous monitoring and timely intervention, these devices support personalized care, improve clinical outcomes, reduce hospital admissions, and enhance overall patient quality of life.

The market grew from USD 2 billion in 2022 to USD 2.4 billion in 2024. The rising global prevalence of cardiovascular diseases (CVDs) is a key factor driving growth in the wearable cardiac devices market. Cardiovascular conditions remain a leading cause of mortality and long‑term disability worldwide, accounting for a significant proportion of total global deaths. In 2021 alone, CVDs were responsible for approximately 20.5 million fatalities, representing nearly one‑third of all deaths globally. This substantial disease burden underscores the growing need for advanced cardiac monitoring solutions. Wearable cardiac devices enable continuous, real‑time monitoring and early detection of cardiac abnormalities, supporting timely clinical intervention and effective disease management. As a result, these technologies play a critical role in improving patient outcomes, reducing healthcare costs, and addressing the overall global burden of cardiovascular diseases.

Additionally, the growing preference for minimally invasive devices is a key driver of the wearable cardiac devices market, as patients and clinicians increasingly favor solutions that reduce procedural risk, discomfort, and recovery time. Wearable cardiac devices offer continuous, non-invasive heart monitoring without the need for surgical implantation, making them particularly attractive for long-term arrhythmia detection, post-operative monitoring, and chronic cardiac care. Their ease of use, improved patient compliance, and ability to deliver real-time clinical insights align well with the shift toward patient-centric and home-based healthcare, thereby accelerating adoption across both hospital and remote care settings.

Wearable cardiac devices are non-invasive or minimally invasive medical devices designed to continuously monitor, record, and analyze heart activity in real time. They are worn on the body, such as watches, patches, or vests, to detect cardiac abnormalities like arrhythmias. These devices support early diagnosis, remote patient monitoring, and improved management of cardiovascular conditions.

Wearable Cardiac Devices Market Trends

Rapid technological advancements in wearable cardiac devices have emerged as a major growth driver of the wearable cardiac devices industry, enabling continuous, accurate, and real‑time monitoring of cardiovascular parameters while significantly improving patient comfort and safety.

Advanced sensor technologies, including electrocardiography (ECG), photoplethysmography (PPG), temperature, and motion sensors, now enable long‑term, high‑fidelity cardiac rhythm monitoring outside hospital settings. Devices such as iRhythm’s Zio Patch, a lightweight adhesive ECG monitor worn for up to 14 days, have demonstrated superior arrhythmia detection compared to traditional Holter monitors due to extended wear duration and AI‑assisted data analysis.

AI‑powered analytics and machine learning algorithms are enhancing diagnostic accuracy by automatically detecting atrial fibrillation, bradycardia, tachycardia, and other rhythm abnormalities from large volumes of continuous data. Medical‑grade wearables such as BioIntelliSense’s BioSticker integrate FDA‑cleared sensors with advanced analytics to monitor heart rate trends, respiratory rate, and activity levels, enabling early clinical intervention and efficient remote patient management.

Connectivity and digital health integration further enhance the value of wearable cardiac devices by enabling seamless data transmission to clinicians, electronic health records (EHRs), and remote patient monitoring platforms. Integration with mobile applications, cloud‑based dashboards, and tele‑cardiology services supports continuous care delivery for conditions such as atrial fibrillation and heart failure while reducing hospital visits and readmissions.

Collectively, these technological advancements are improving clinical outcomes, enabling early disease detection, and expanding the use of wearable cardiac devices across hospitals, cardiology clinics, ambulatory centers, and home‑care settings. The convergence of advanced sensors, AI‑driven analytics, and smart connectivity is driving strong global adoption and sustained growth of the market.

Wearable Cardiac Devices Market Analysis

Based on product, the wearable cardiac devices market is segmented into holter monitors, smartwatches, patch, defibrillators, pulse oximeters, and other products. The smartwatches segment dominated the market, accounting for 28.5% of the total revenue share in 2025.

Smartwatches feature user‑friendly and intuitive designs, enabling individuals to monitor cardiac health independently without the need for continuous clinical supervision, thereby improving accessibility across a broad consumer base.

These devices are increasingly integrated with advanced sensors and AI‑driven analytics, allowing real‑time cardiac monitoring for both users and healthcare professionals, which supports timely and data‑driven clinical decision‑making.

Furthermore, sophisticated algorithms enable early detection of abnormal heart rhythms, such as atrial fibrillation, helping to reduce the risk of severe cardiovascular events. By tracking multiple vital parameters including heart rate, ECG, blood oxygen saturation, and physical activity smartwatches provide a comprehensive assessment of cardiovascular health.

For instance, the CardiacSense smartwatch offers continuous heart rate monitoring and atrial fibrillation detection. The company has also announced plans to introduce additional features, including continuous monitoring of respiratory rate, oxygen saturation, core body temperature, and absolute blood pressure.

Consequently, the combination of advanced functionalities, compact form factors, and ongoing innovation by key market players is significantly contributing to the sustained growth of the smartwatch segment within the market.

Based on application, the wearable cardiac devices market is segmented into coronary artery disease (CAD), cardiomyopathies, post‑myocardial infarction, congenital heart diseases, post‑surgical cardiac care, and other applications. The coronary artery disease (CAD) segment held a 37.5% market share in 2025 and is expected to experience robust growth, reaching USD 3.3 billion by 2035.

Coronary artery disease represents the most common cardiovascular condition globally, accounting for a substantial portion of cardiac‑related morbidity and mortality. In the United States, CAD led to 371,506 deaths in 2022, underscoring the significant clinical and economic burden associated with the disease.

The rising prevalence of lifestyle‑related risk factors, including obesity, physical inactivity, unhealthy dietary patterns, and tobacco use, is a key contributor to the increasing incidence of CAD. As these risk factors continue to intensify, demand for continuous cardiac monitoring solutions is rising, thereby driving increased adoption of wearable cardiac devices.

According to estimates from the World Health Organization (WHO), 1 in 8 people worldwide were obese in 2022. Furthermore, adult obesity has increased more than twofold since 1990, while adolescent obesity has increased fourfold, significantly elevating long‑term cardiovascular risk.

Consequently, the growing prevalence of unhealthy lifestyle behaviors remains a major factor supporting the dominance of the CAD segment. This segment is expected to maintain its leading position over the forecast period, driven by sustained disease prevalence and the expanding role of wearable cardiac monitoring technologies.

Based on end use, the wearable cardiac devices market is segmented into hospitals, specialty centers, home care settings, and other end users. The home care settings segment accounted for a 35.5% market share in 2025, reflecting strong adoption across non‑clinical environments.

In home care settings, patients can utilize wearable cardiac devices without the need for frequent visits to healthcare facilities, enabling continuous cardiac monitoring within a comfortable and familiar home environment. This improves patient convenience, adherence, and long‑term disease management.

Wearable cardiac devices are also designed to comply with regulatory requirements for point‑of‑care (POC) applications, making them suitable for home‑based monitoring while maintaining clinical reliability and safety standards.

For example, the World Health Organization’s ASSURED criteria, which emphasize affordability, sensitivity, specificity, user friendliness, rapid and robust performance, equipment free operation, and deliverability to end users, provide a standardized framework that guides manufacturers in developing wearable cardiac devices suitable for decentralized and home based care settings.

Consequently, the ease of use, enhanced patient comfort, and adherence to established regulatory guidelines are key factors driving revenue growth of the home care settings segment within the market.

North America Wearable Cardiac Devices Market

North America dominated the global market with a market share of 40.4% in 2025.

North America represents a significant share of the wearable cardiac devices industry, primarily driven by the high prevalence of cardiovascular diseases in the U.S. According to the Centers for Disease Control and Prevention (CDC), cardiovascular diseases remain the leading cause of death across most ethnic groups in the country, with 702,880 cardiac‑related deaths reported in 2022. This substantial disease burden has increased the demand for continuous cardiac monitoring solutions, thereby supporting market growth in the region.

In addition, the U.S. benefits from a highly advanced healthcare system supported by well‑established medical infrastructure and strong adoption of digital health technologies. The availability of sophisticated healthcare facilities, favorable reimbursement frameworks, and growing patient awareness has promoted the widespread use of wearable cardiac devices for early diagnosis, remote monitoring, and long‑term disease management, further strengthening the market in North America.

Europe Wearable Cardiac Devices Market

Europe market accounted for USD 591.7 million in 2025 and is anticipated to show lucrative growth over the forecast period.

Europe represents a substantial market for wearable cardiac devices, largely driven by the high burden of cardiac disorders across the region. Cardiovascular diseases remain the leading cause of mortality in the European Union. According to Eurostat, diseases of the circulatory system accounted for approximately 1.68 million deaths in the EU in 2022, representing about 32.7% of all deaths. Similarly, the World Health Organization (WHO) reports that cardiovascular diseases cause nearly half of all deaths in the WHO European Region, with an estimated 10,000 deaths per day, underscoring the scale of the public health challenge posed by cardiac disorders.

This factor collectively position Europe as a key growth region for the market, with rising demand for remote and preventive cardiac monitoring solutions.

The UK wearable cardiac devices market is projected to experience steady growth between 2026 and 2035.

The UK has a well-established regulatory environment, with bodies such as the Medicines and Healthcare Products Regulatory Agency (MHRA) ensuring the safety and effectiveness of medical devices. Thus, companies can launch wearable cardiac devices to market with confidence, which in turn fosters innovation and product adoption.

Moreover, the cardiac diseases in the country are on the rise. According to British Heart Foundation, there are more than 7.6 million people living with a heart disease in the UK.

Thus, the aforementioned factors are expected to fuel the market growth in the country.

Asia Pacific Wearable Cardiac Devices Market

The Asia Pacific region is projected to be valued at USD 674.3 million in 2025.

The Asia Pacific region bears a significant and growing burden of cardiovascular diseases, making it a key market for wearable cardiac devices. According to government‑backed statistics from the World Health Organization, cardiovascular diseases are the leading cause of mortality across the region. The WHO South‑East Asia Region alone reported approximately 4.3 million cardiovascular‑related deaths in 2021, accounting for around 32% of all deaths, while the broader Asia‑Pacific region experiences over 10 million cardiovascular deaths annually. Rapid urbanization, aging populations, changing lifestyles, and a rising prevalence of hypertension and diabetes are major contributors to the increasing incidence of cardiac disorders across countries such as China, India, Japan, and Southeast Asian nations.

In response to this high disease burden, governments and regional health authorities are strengthening cardiovascular prevention, screening, and management initiatives. Public health programs led by organizations such as WHO, national ministries of health, and regional alliances emphasize early diagnosis and continuous monitoring to reduce premature mortality. These efforts, combined with expanding healthcare coverage, increasing digital health adoption, and policy support for remote and home‑based care, are accelerating the demand for wearable cardiac devices across the Asia Pacific region, positioning it as a high‑growth market for continuous cardiac monitoring solutions.

Japan wearable cardiac devices market is poised to witness lucrative growth between 2026 - 2035.

Japan has one of the world’s oldest populations, along with a high prevalence of cardiovascular diseases. For instance, according to Statista, in 2022, people over 65 years of age accounted for 29.3% of total Japanese population and this number is expected to rise to 38% by 2070, owing to low birth rate. Moreover, as per the data from National Center for Biotechnology Information, in recent years, the crude mortality rate of heart disease in Japan has been observed to rise year by year with the aging population.

Furthermore, Japan’s healthcare system creates increased awareness of heart disease prevention and promotes early detection, the wearable cardiac devices, are becoming quite popular among consumers seeking to actively monitor their cardiovascular health.

Latin America Wearable Cardiac Devices Market

The Brazil wearable cardiac devices industry is expected to grow steadily during the forecast period.

Brazil represents a growing market for wearable cardiac devices, driven primarily by the high burden of cardiovascular diseases across the country. According to official data compiled from the Brazilian Ministry of Health and national mortality systems, cardiovascular conditions account for approximately one in every three deaths nationwide. In 2022, nearly 400,000 deaths in Brazil were attributed to cardiovascular diseases, with ischemic heart disease and stroke together accounting for about 76% of these fatalities. Additionally, government‑backed analyses indicate that in 2019, ischemic heart disease and cerebrovascular diseases alone were responsible for around 21.4% of all deaths in the country, highlighting the widespread prevalence of cardiac disorders and the pressing need for effective monitoring solutions.

In response to this significant disease burden, demand for wearable cardiac devices is increasing as healthcare providers and patients seek early diagnosis, continuous monitoring, and improved disease management. The expansion of Brazil’s public healthcare system, growing adoption of digital health technologies, and rising awareness of preventive cardiac care are supporting market growth.

Middle East and Africa Wearable Cardiac Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

Saudi Arabia represents a steadily expanding market for wearable cardiac devices, supported by the country’s high prevalence of cardiovascular diseases and strong government focus on healthcare modernization. Cardiovascular diseases are among the leading causes of mortality, accounting for a substantial share of non‑communicable disease–related deaths.

Government‑backed and WHO‑supported analyses indicate that non‑communicable diseases contribute to about 35% of all deaths in Saudi Arabia, with cardiovascular diseases being the largest contributor within this group, primarily driven by ischemic heart disease and stroke.

Strong government investment in healthcare infrastructure, national screening programs, and rising awareness of cardiovascular health is expected to accelerate the adoption of wearable cardiac devices, positioning Saudi Arabia as a key growth market in the Middle East.

Wearable Cardiac Devices Market Share

Medtronic, Abbott Laboratories, Boston Scientific, Koninklijke Philips, and iRhythm Technologies are the leading players in the global wearable cardiac devices industry, collectively holding approximately 55% of the total market share.

These players define the competitive landscape across medical‑grade wearable cardiac monitoring solutions, addressing a wide range of indications such as arrhythmia detection, atrial fibrillation screening, remote ECG monitoring, heart rate variability assessment, and long‑term ambulatory cardiac diagnostics through extensive portfolios of ECG patches, Holter monitors, mobile cardiac telemetry systems, and connected wearable platforms.

Medtronic and Abbott Laboratories maintain leading positions through robust, clinically validated wearable and implant‑adjacent cardiac monitoring technologies with strong global adoption. Medtronic leads through its comprehensive cardiac diagnostics ecosystem, combining wearable monitors with cloud‑based data analytics and physician workflows to support continuous, real‑world cardiac assessment.

Philips, Boston Scientific, and iRhythm Technologies reinforce the competitive environment through specialization in ambulatory cardiac monitoring and digital cardiology. Philips leverages its strong expertise in connected care and remote patient monitoring to deliver scalable wearable cardiac solutions used across hospitals and home‑care environments.

Collectively, these companies are shaping the evolution of the market toward continuous monitoring, earlier diagnosis, reduced hospital dependency, and personalized cardiovascular care.

Strategic investments in AI‑driven arrhythmia detection, cloud‑based analytics, miniaturized sensor technologies, and workflow‑optimized remote monitoring platforms are expanding clinical utility and accelerating global adoption of wearable cardiac devices across hospitals, cardiology clinics, ambulatory diagnostic centers, and home‑based care environments.

Wearable Cardiac Devices Market Companies

Few of the prominent players operating in the wearable cardiac devices industry include:

Abbott Laboratories

Boston Scientific

Cardiac Insight

CardiacSense

Cardiac Rhythm

iRhythm Technologies

Integra LifeSciences

Koninklijke Philips

Medtronic

Proteus Digital Health

Qardio

ZOLL Medical Corporation

Welch Allyn

VitalConnect

Zimmer Biomet

Medtronic

Medtronic is a global leader in the wearable cardiac devices market, offering a broad portfolio that spans mobile cardiac telemetry, and connected wearable solutions integrated with remote patient monitoring platforms. Its offerings emphasize long-term rhythm monitoring, early arrhythmia detection, and seamless clinician workflow integration, supporting both hospital-based and home-care settings. Medtronic’s strong presence across North America and Europe, combined with continuous investments in digital health, AI-enabled diagnostics, and wearable form factors, positions the company as a key driver in the shift from episodic cardiac assessment toward continuous, data-driven cardiac care.

Abbott Laboratories

Abbott Laboratories holds a strong position in the wearable cardiac devices industry through its advanced cardiac monitoring portfolio focused on connected, long-term rhythm surveillance. The company emphasizes Bluetooth-enabled, miniaturized cardiac monitoring technologies that support continuous data transmission and remote clinical decision-making, particularly for arrhythmia and atrial fibrillation detection. Abbott’s strategy centers on improving diagnostic accuracy, extending monitoring duration, and reducing clinical data burden, which aligns well with the growing demand for outpatient and remote cardiac care across developed and emerging healthcare systems.

Boston Scientific

Boston Scientific is a prominent player in the market, offering a comprehensive range of ambulatory and wearable ECG monitoring solutions designed for continuous and near real-time cardiac diagnostics. Its wearable portfolio focuses on patient-friendly, lightweight designs combined with robust remote data transmission and analytics to support timely arrhythmia detection and clinical intervention. Through its expanding cardiac diagnostics segment and emphasis on integrated digital ecosystems, Boston Scientific supports the broader industry transition toward wearable, home-based cardiac monitoring and value-based cardiac care models.

Wearable Cardiac Devices Industry News

In January 2023, CardiacSense Ltd. received FDA clearance for its CSF-3 watch that measures ECG, heart rate, and SpO2. This enhanced the company's position in the market for wearable cardiac devices.

In September 2023, iRhythm Technologies, Inc. launched its next-generation Zio monitor in the U.S. It is a prescription-only ECG monitor, which is an integral part of the Zio LTCM service. This launch improved patient and healthcare professional experiences, thereby promoting market growth.

In January 2021, Philips acquired BioTelemetry and its wearable remote heart monitors, enhancing its portfolio in remote patient monitoring devices, which is expected to reach USD 41.3 billion in 2032. This acquisition enabled the company to provide monitoring solutions for heart health and strengthened its position in the digital health sector.

In January 2021, Boston Scientific announced an agreement to acquire Preventice Solutions, Inc., a privately held firm offering products such as portable cardiac health solutions, including Holter monitors to mobile cardiac telemetry. This acquisition established the company in a strong position in the ambulatory electrocardiography space.

The wearable cardiac devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 - 2035 for the following segments:

Market, By Product

Holter monitors

Smartwatches

Patch

Defibrillators

Pulse oximeters

Other products

Market, By Application

Coronary artery disease (CAD)

Cardiomyopathies

Post-myocardial infarction

Congenital heart diseases

Post-surgical cardiac care

Other applications

Market, By End Use

Hospitals

Specialty centers

Home care settings

Other end users

The above information is provided for the following regions and countries:

North America

U.S.

Canada

Europe

Germany

UK

France

Italy

Spain

Netherlands

Asia Pacific

China

India

Japan

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

Middle East and Africa

Saudi Arabia

South Africa

UAE

Authors: Monali Tayade, Jignesh Rawal

Wearable Cardiac Devices Market Scope

Wearable Cardiac Devices Market Size

Wearable Cardiac Devices Market Trends

Wearable Cardiac Devices Market Analysis

Wearable Cardiac Devices Market Share

Report Content

Chapter 1 Research Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.2.1.1 Source consistency protocol

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.5.1.1 Sources, by region

1.6 Base estimates and calculations

1.6.1 Base year calculation for any one approach

1.7 Forecast model

1.7.1 Quantified market impact analysis

1.7.1.1 Mathematical impact of growth parameters on forecast

1.8 Research transparency addendum

1.8.1 Source attribution framework

1.8.2 Quality assurance metrics

1.8.3 Our commitment to trust

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Product trends

2.2.2 Application trends

2.2.3 End use trends

2.2.4 Regional trends

2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing number of patients suffering from cardiovascular diseases

3.2.1.2 Rapid technological advancements in wearable cardiac devices

3.2.1.3 Growing preference of minimally invasive devices

3.2.1.4 Rising health consciousness and preventive care

3.2.2 Industry pitfalls and challenges

3.2.2.1 Data privacy issues

3.2.2.2 Stringent regulatory policies

3.2.3 Market opportunities

3.2.3.1 Rapid expansion of home-use wearable cardiac devices

3.2.3.2 Integration with AI and advanced analytics

3.3 Growth potential analysis

3.4 Regulatory landscape (Driven by primary research)

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.5 Technology landscape

3.5.1 Current technological trends

3.5.1.1 Continuous ECG and patch based wearable cardiac monitoring devices

3.5.2.1 Non invasive optical and multimodal biosensing cardiac diagnostics

3.5.2.2 Smart, connected, and personalized wearable cardiac devices

3.6 Future market trends (Driven by primary research)

3.7 Impact of AI and Generative AI on the market (Driven by primary research)

3.8 Pricing analysis, 2025

3.9 Porter’s analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers and acquisitions

4.6.2 Partnerships and collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 – 2035 ($ Mn)

5.1 Key trends

5.2 Holter monitors

5.3 Smartwatches

5.4 Patch

5.5 Defibrillators

5.6 Pulse oximeters

5.7 Other products

Chapter 6 Market Estimates and Forecast, By Application, 2022 – 2035 ($ Mn)

6.1 Key trends

6.2 Coronary artery disease (CAD)

6.3 Cardiomyopathies

6.4 Post-myocardial infarction

6.5 Congenital heart diseases

6.6 Post-surgical cardiac care

6.7 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2022 – 2035 ($ Mn)

7.1 Key trends

7.2 Hospitals

7.3 Specialty centers

7.4 Home care settings

7.5 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 – 2035 ($ Mn)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 UK

8.3.3 UK

8.3.4 Spain

8.3.5 Italy

8.3.6 Netherlands

8.4 Asia Pacific

8.4.1 China

8.4.2 Japan

8.4.3 India

8.4.4 Australia

8.4.5 South Korea

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.6 Middle East and Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 UAE

Chapter 9 Company Profiles

9.1 Abbott Laboratories

9.2 Boston Scientific

9.3 Cardiac Insight

9.4 CardiacSense

9.5 Cardiac Rhythm

9.6 iRhythm Technologies

9.7 Integra LifeSciences

9.8 Koninklijke Philips

9.9 Medtronic

9.10 Proteus Digital Health

9.11 Qardio

9.12 ZOLL Medical Corporation

9.13 Welch Allyn

9.14 VitalConnect

9.15 Zimmer Biomet

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Regional or domestic-only leaders not in the global top tier

Distributors and channel partners who control market access

Emerging disruptors, startups, or adjacent-industry entrants

Niche players focused on a specific application or end-use

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Authors: Monali Tayade, Jignesh Rawal

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at[email protected]

Explore our licensing options:

Starting at: $2,450

Premium Report Details

Base Year: 2025

Companies Profiled: 15

Tables and Figures: 167

Countries covered: 19

Pages: 130

Download Free PDF

Premium Report Details

Base Year: 2025

Companies Profiled: 15

Tables and Figures: 167

Countries covered: 19

Pages: 130

Download Free PDF

Share Content

Add Citations

Monali Tayade. 2026, April. Wearable Cardiac Devices Market- By Product, By Application, By End Use - Global Forecast, 2026 - 2035 (Report ID: GMI4711). Global Market Insights Inc. Retrieved August 5, 2026, from https://www.gminsights.com/toc/details/wearable-cardiac-devices-market

Wearable Cardiac Devices Market

Get a free sample of this report

Get a free sample of this report Wearable Cardiac Devices Market

Is your requirement urgent? Please give us your business email for a speedy delivery!

Wearable Cardiac Devices Market Size

The global wearable cardiac devices market was valued at USD 2.7 billion in 2025 and is projected to grow from USD 3 billion in 2026 to USD 8.5 billion by 2035, expanding at a CAGR of 12.2%, according to the latest report published by Global Market Insights Inc.

This fairly considerable growth is driven by numerous factors such as increasing number of patients suffering from cardiovascular diseases, rapid technological advancements in wearable cardiac devices, growing preference of minimally invasive devices, and rising health consciousness and preventive care.

Wearable cardiac devices are advanced medical technologies designed to continuously monitor, diagnose, and manage cardiovascular conditions outside of traditional clinical settings. These devices incorporate technologies such as electrocardiography (ECG), biosensors, wireless connectivity, and digital signal processing to track heart rate, heart rhythm, and other vital cardiac parameters in real time. Wearable cardiac devices enable clinicians to detect conditions such as arrhythmias, atrial fibrillation, ischemic events, and heart failure at earlier stages. By facilitating continuous monitoring and timely intervention, these devices support personalized care, improve clinical outcomes, reduce hospital admissions, and enhance overall patient quality of life.

The market grew from USD 2 billion in 2022 to USD 2.4 billion in 2024. The rising global prevalence of cardiovascular diseases (CVDs) is a key factor driving growth in the wearable cardiac devices market. Cardiovascular conditions remain a leading cause of mortality and long‑term disability worldwide, accounting for a significant proportion of total global deaths. In 2021 alone, CVDs were responsible for approximately 20.5 million fatalities, representing nearly one‑third of all deaths globally. This substantial disease burden underscores the growing need for advanced cardiac monitoring solutions. Wearable cardiac devices enable continuous, real‑time monitoring and early detection of cardiac abnormalities, supporting timely clinical intervention and effective disease management. As a result, these technologies play a critical role in improving patient outcomes, reducing healthcare costs, and addressing the overall global burden of cardiovascular diseases.

Additionally, the growing preference for minimally invasive devices is a key driver of the wearable cardiac devices market, as patients and clinicians increasingly favor solutions that reduce procedural risk, discomfort, and recovery time. Wearable cardiac devices offer continuous, non-invasive heart monitoring without the need for surgical implantation, making them particularly attractive for long-term arrhythmia detection, post-operative monitoring, and chronic cardiac care. Their ease of use, improved patient compliance, and ability to deliver real-time clinical insights align well with the shift toward patient-centric and home-based healthcare, thereby accelerating adoption across both hospital and remote care settings.

Wearable cardiac devices are non-invasive or minimally invasive medical devices designed to continuously monitor, record, and analyze heart activity in real time. They are worn on the body, such as watches, patches, or vests, to detect cardiac abnormalities like arrhythmias. These devices support early diagnosis, remote patient monitoring, and improved management of cardiovascular conditions.

Wearable Cardiac Devices Market Trends

Wearable Cardiac Devices Market Analysis

Based on product, the wearable cardiac devices market is segmented into holter monitors, smartwatches, patch, defibrillators, pulse oximeters, and other products. The smartwatches segment dominated the market, accounting for 28.5% of the total revenue share in 2025.

Based on application, the wearable cardiac devices market is segmented into coronary artery disease (CAD), cardiomyopathies, post‑myocardial infarction, congenital heart diseases, post‑surgical cardiac care, and other applications. The coronary artery disease (CAD) segment held a 37.5% market share in 2025 and is expected to experience robust growth, reaching USD 3.3 billion by 2035.

Based on end use, the wearable cardiac devices market is segmented into hospitals, specialty centers, home care settings, and other end users. The home care settings segment accounted for a 35.5% market share in 2025, reflecting strong adoption across non‑clinical environments.

North America Wearable Cardiac Devices Market

North America dominated the global market with a market share of 40.4% in 2025.

Europe Wearable Cardiac Devices Market

Europe market accounted for USD 591.7 million in 2025 and is anticipated to show lucrative growth over the forecast period.

The UK wearable cardiac devices market is projected to experience steady growth between 2026 and 2035.

Asia Pacific Wearable Cardiac Devices Market

The Asia Pacific region is projected to be valued at USD 674.3 million in 2025.

Japan wearable cardiac devices market is poised to witness lucrative growth between 2026 - 2035.

Latin America Wearable Cardiac Devices Market

The Brazil wearable cardiac devices industry is expected to grow steadily during the forecast period.

Middle East and Africa Wearable Cardiac Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

Wearable Cardiac Devices Market Share

Wearable Cardiac Devices Market Companies

Few of the prominent players operating in the wearable cardiac devices industry include:

Medtronic is a global leader in the wearable cardiac devices market, offering a broad portfolio that spans mobile cardiac telemetry, and connected wearable solutions integrated with remote patient monitoring platforms. Its offerings emphasize long-term rhythm monitoring, early arrhythmia detection, and seamless clinician workflow integration, supporting both hospital-based and home-care settings. Medtronic’s strong presence across North America and Europe, combined with continuous investments in digital health, AI-enabled diagnostics, and wearable form factors, positions the company as a key driver in the shift from episodic cardiac assessment toward continuous, data-driven cardiac care.

Abbott Laboratories holds a strong position in the wearable cardiac devices industry through its advanced cardiac monitoring portfolio focused on connected, long-term rhythm surveillance. The company emphasizes Bluetooth-enabled, miniaturized cardiac monitoring technologies that support continuous data transmission and remote clinical decision-making, particularly for arrhythmia and atrial fibrillation detection. Abbott’s strategy centers on improving diagnostic accuracy, extending monitoring duration, and reducing clinical data burden, which aligns well with the growing demand for outpatient and remote cardiac care across developed and emerging healthcare systems.

Boston Scientific is a prominent player in the market, offering a comprehensive range of ambulatory and wearable ECG monitoring solutions designed for continuous and near real-time cardiac diagnostics. Its wearable portfolio focuses on patient-friendly, lightweight designs combined with robust remote data transmission and analytics to support timely arrhythmia detection and clinical intervention. Through its expanding cardiac diagnostics segment and emphasis on integrated digital ecosystems, Boston Scientific supports the broader industry transition toward wearable, home-based cardiac monitoring and value-based cardiac care models.

Wearable Cardiac Devices Industry News

The wearable cardiac devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million and from 2022 - 2035 for the following segments:

Market, By Product

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries: