Market Size By Product (Self-monitoring blood glucose meters, Consumables), By Application (Type 1 diabetes, Type 2 diabetes, Gestational diabetes), By End Use (Hospitals, Ambulatory surgical centers, Diagnostic centers, Homecare, Other end users). The market forecasts are provided in terms of value (USD).

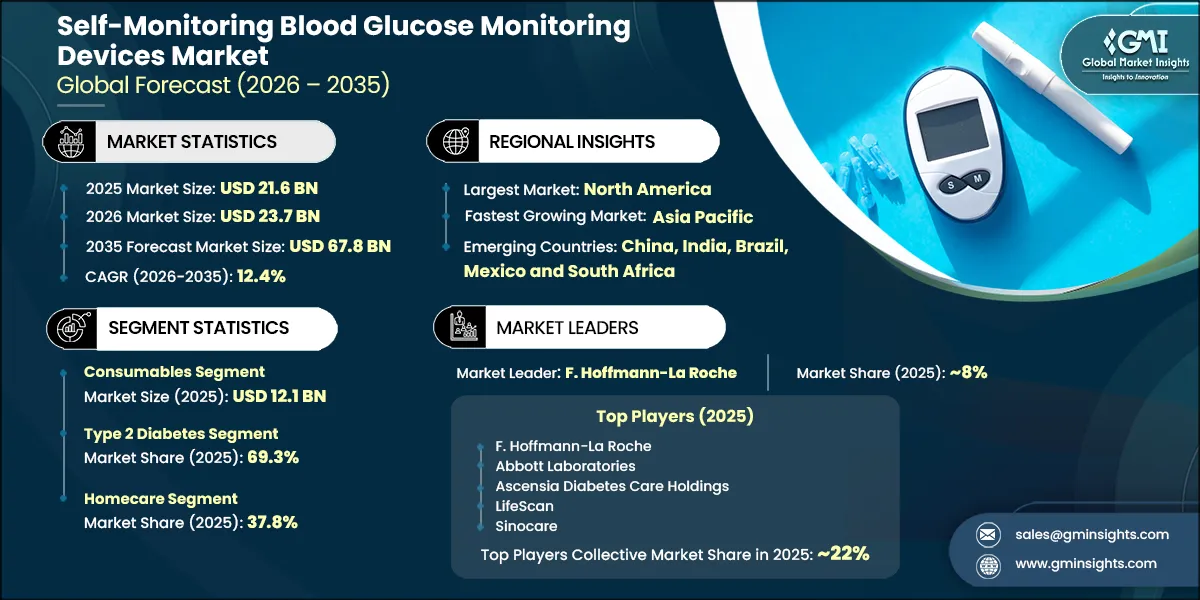

The self-monitoring blood glucose monitoring devices market size was valued at USD 21.6 billion in 2025 and is expected to reach USD 67.8 billion in 2035, growing at a CAGR of 12.4% from 2026 to 2035, according to the latest report published by Global Market Insights Inc.

This steady growth is stimulated by various factors such as rising prevalence of diabetes worldwide, technological advancements of self-monitoring blood glucose monitoring devices in developed countries, and government initiatives for increasing awareness pertaining diabetes among people.

This market is growing due to an increasing prevalence of diabetes mellitus globally. For instance, as per the estimates from the International Diabetes Federation (IDF), 537 million people were living with diabetes worldwide in 2021. The trend is anticipated to increase that number to 643 million in 2030 and then to 783 million in 2045. As the disease is getting prevalent among patients and healthcare providers, the demand for SMBG devices is increasing in order to manage the disease.

In addition, government initiatives to increase awareness about management of diabetes mellitus aids in the early detection and is a reason for the expansion of the market as well. For instance, the U.S. National Diabetes Education Program (NDEP) is one such source wherein the advantages of SMBG devices in self-management have been brought forward. Moreover, in the European Union, screening campaigns target the high-risk groups, such as people over 45 years of age or those having a family history of diabetes, encouraging early diagnosis and thereby creating demand for diabetes-related treatments. Such efforts by the government are helping to increase awareness about this lifestyle disease as well as helping in early detection of the condition. This, in turn, helps in boosting the demand for diabetes care devices as a measure to keep the disease under control.

Self-monitoring blood glucose devices are being used since decades; these operate by pricking a finger with sharp lancet and using the blood on the strip, which is further inserted into the glucometer to measure the blood glucose level of an individual.

Technological advancements in SMBG devices play a critical role in driving market expansion. Innovations in connectivity, accuracy, and usability improve patient adherence and increase consumer preference for advanced monitoring solutions.

Modern SMBG devices support seamless connectivity with smartphone applications through Bluetooth technology and USB interfaces. For example, Omnitest 5 by B. Braun is a smart SMBG device that connects to smartphones via Bluetooth as well as a micro-USB port, enabling effortless data transfer from the device to the mobile application. This allows users to conveniently view glucose readings at a glance and manually log additional health data, such as physical activity, thereby enhancing overall self-monitoring and user engagement.

Additionally, leading market players increasingly focus on cloud-based data integration to enhance usability and remote monitoring. This enables users and healthcare professionals to access glucose data remotely.

For example, Abbott’s FreeStyle Lite allows users to upload glucose readings to the LibreView cloud platform, supporting healthcare providers in tracking patient progress from remote locations. Such features significantly enhance telehealth capabilities and improve patient outcomes.

Furthermore, the accuracy of SMBG devices has improved considerably with the incorporation of advanced algorithms and multi-parameter sensing technologies. Features such as compensation for temperature variations, hematocrit levels, and other physiological factors help minimize measurement errors. For instance, the Accu-Chek Guide system improves disease management accuracy, reducing the risk of misdiagnosis, particularly in unsupervised home-care settings.

SMBG devices have also become more portable and user-friendly due to compact, ergonomic designs and innovative sampling features. For example, the CONTOUR NEXT ONE meter by Ascensia Diabetes Care offers a Second Chance Sampling feature, which allows users to apply additional blood to the same test strip if the initial sample is insufficient. This reduces wasted test strips and lancets, minimizes finger pricks, enhances comfort, and significantly improves overall user experience.

Based on product, the market is segmented into self-monitoring blood glucose meters and consumables. The consumables segment is further bifurcated into testing strips and lancets. This consumables segment was valued at USD 12.1 billion in 2025.

Self-monitoring blood glucose devices require consumable items such as test strips and lancets for daily diabetes management. These items are available over-the-counter, making them easily accessible.

The primary consumable components are test strips, which are single-use devices that capture blood for glucose measurement. Their small size makes them lightweight, portable, and compact. Users can easily carry these with them and test their blood glucose levels anywhere, whether at the office, home, or on vacation.

The accuracy of test strips is crucial for effective diabetes management. A study published in the Journal of Diabetes Science and Technology found that modern test strips, when used with compatible meters, offer an accuracy level of ±15% compared to laboratory testing methods.

Additionally, key players are focusing on improving needle designs for lancets, which are devices used to extract blood samples, making the process safer and less painful.

Thus, the consumables segment, particularly test strips, is the most critical factor of the market's growth.

Based on application, the self-monitoring blood glucose monitoring devices market is segmented into type 1 diabetes, type 2 diabetes, and gestational diabetes. The type 2 diabetes emerged as a dominant segment in the market, accounting for 69.3% of revenue share in 2025.

Type 2 diabetic patients face two major challenges: the pancreas does not produce enough insulin, a hormone that regulates the movement of sugar into cells, and cells do not respond adequately to insulin, resulting in reduced sugar absorption. The increasing prevalence of this condition is a significant factor behind the dominance of this segment.

For example, data from the Centers for Disease Control and Prevention (CDC) indicates that approximately 38 million individuals in the U.S. are diabetic, with 90% - 95% of these cases attributed to type 2 diabetes. While individuals aged 45 and older are more prone to type 2 diabetes, there is a growing number of cases among children, teenagers, and young adults.

Thus, type 2 diabetes is expected to remain a dominant segment and continue driving the market's growth during the forecast period.

Based on end use, the self-monitoring blood glucose monitoring devices market is segmented into hospitals, ambulatory surgical centers, diagnostic centers, homecare, and other end users. Homecare accounted for the largest revenue share of 37.8% in 2025.

Self-monitoring blood glucose (SMBG) devices empower patients to monitor their blood glucose levels at home, reducing the need for clinic visits. This enhances self-management of their condition and is particularly beneficial for elderly patients or those with mobility challenges, as it provides them with greater control over their health.

The use of SMBG devices at home also enables patients to adjust their diets, physical activities, and medication regimens more frequently. For instance, researchers from the NIH reported that patients using SMBG devices daily had a 16% lower HbA1c level compared to those who did not, indicating a lower risk of diabetes-related complications.

Therefore, as these devices can be used without a doctor's supervision and offer significant benefits for elderly patients, the segment is expected to experience substantial growth during the forecast period.

North America Self-monitoring Blood Glucose Monitoring Devices Market

The North America region accounted for 38.1% of the market in 2025. The market in North America is experiencing robust expansion, driven by the region’s advanced healthcare infrastructure and technological advancements.

The U.S. market size reached USD 7.6 billion in 2025, growing from USD 7 billion in 2024.

In the U.S., diabetes carries a significant economic burden. The American Diabetes Association reported that in 2022, the cost of managing diabetes in the U.S. exceeded USD 412.9 billion, a substantial increase from USD 327 billion in 2017.

Additionally, healthcare spending in the U.S. remains exceptionally high, enabling the extensive integration of SMBG devices. These capital investments support the delivery of groundbreaking innovations in advanced SMBG devices, which contribute to economic growth.

Europe Self-monitoring Blood Glucose Monitoring Devices Market

Europe, self-monitoring blood glucose monitoring devices accounted for USD 5.8 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

The rising number of diabetes cases in European countries has increased the demand for glucose monitoring solutions. The necessity for regular blood sugar monitoring among millions of individuals has made SMBG devices essential for effective diabetes management.

Technological advancements have significantly contributed to market growth. Modern SMBG devices now feature smartphone connectivity, cloud-based data tracking, and non-invasive monitoring capabilities. These innovations enhance user convenience, improve patient outcomes, and encourage regular device usage, driving market expansion.

The self-monitoring blood glucose monitoring devices market in the UK is projected to experience steady growth between 2026 and 2035.

The prevalence of diabetes is steadily increasing in the UK. Public Health England estimates that the Diabetes Prevalence Model will reach 4.9 million diabetics in the UK by 2035.

Such high projections, combined with the efforts of the NHS, indicate significant potential for further market expansion in the UK.

Furthermore, the growth of the self-monitoring blood glucose devices market in the UK is expected to be bolstered by the government’s commitment to addressing chronic conditions. Initiatives such as public health campaigns and guidelines promoting healthier lifestyles are contributing to market growth.

Asia Pacific Self-monitoring Blood Glucose Monitoring Devices Market

The Asia Pacific self-monitoring blood glucose monitoring devices is anticipated to grow at the highest CAGR of 13% during the analysis timeframe.

The Asia Pacific market for self-monitoring blood glucose devices is witnessing rapid expansion, driven by the increasing prevalence of diabetes, growing health consciousness among the population, and continuous improvements in healthcare infrastructure.

The development of new hospitals and diagnostic centers across the region is significantly boosting the demand for advanced diabetes care technologies. These infrastructure enhancements are enabling better access to quality care for individuals living with diabetes, thereby accelerating the growth of the SMBG devices market in Asia Pacific.

The China market is anticipated to witness lucrative growth during the forecast period.

The country has one of the fastest-aging populations, which creates a need for frequent health monitoring.

For instance, according to estimates from the World Health Organization in 2019, approximately 254 million people aged 65 and above were residing in the country. This number is projected to rise significantly, with 402 million people expected to be over the age of 60 by 2040.

Individuals in this age group are at a high risk of developing chronic health conditions. This, in turn, drives the demand for medical devices such as self-monitoring blood glucose devices, thereby propelling market growth in the country.

Latin America Self-monitoring Blood Glucose Monitoring Devices Market

The rising prevalence of diabetes and other metabolic disorders in Brazil, driven by rapid urbanization, lifestyle changes, increasing obesity rates, and an expanding aging population, is significantly contributing to the growth of the self-monitoring blood glucose (SMBG) devices market.

The growing burden of type 1 and type 2 diabetes is increasing reliance on regular finger-stick glucose testing, particularly for home-based disease management and the prevention of diabetes-related complications.

Increasing awareness regarding early detection of blood glucose abnormalities and routine diabetes self-management in Brazil, supported by public health initiatives, physician-led education, and community-level screening programs, is encouraging wider adoption of SMBG devices. Greater emphasis on affordable, easy-to-use glucose meters and test strips is strengthening SMBG uptake across hospitals, pharmacies, and home-care settings throughout the country.

Middle East and Africa Self-monitoring Blood Glucose Monitoring Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

The demand for market glucose monitoring devices is increasing, which is mostly caused due to the increasing dietary practices and obesity levels. This is directly related to the surge in cases of diabetes in the country.

For instance, as per the data from the International Diabetes Federation, in 2024 around 5.3 million adults in Saudi Arabia had diabetes.

In addition, adult diabetes is on the rise due to the emerging urban western lifestyles in the cities and is hence increasing the demand for self-monitoring blood glucose devices.

The self-monitoring blood glucose devices market is competitive. The top five companies F. Hoffmann-La Roche, Abbott Laboratories, Ascensia Diabetes Care Holdings, LifeScan, and Sinocare are expected to hold approximately 22% of the market share in 2025. F. Hoffmann-La Roche is a key player in the market, leveraging its extensive product portfolio and early entry into the market. The company has remained focused on accuracy, convenience, and distribution while utilizing advanced research, commercial initiatives, and global partnerships.

For example, the company recently launched a campaign in India on World Diabetes Day to promote self-monitoring of blood glucose (SMBG) and reduce “diabetes distress.” This campaign highlighted the importance of pre-breakfast glucose checks for better diabetes management. Using an omnichannel approach, Roche reached over 15,600 patients through in-clinic sessions and influencer collaborations.

Additionally, Abbott, as a major competitor, has been gaining traction due to its strong focus on the digital health revolution. The company’s cloud-based LibreView technology supports remote monitoring and improved telehealth functionality. These advancements have enabled Abbott to capture a significant share of the tech market. Furthermore, key players are focusing on the connectivity aspect of diabetes care by integrating Bluetooth and micro-USB for data transfer in their products.

Competition within the market has also intensified due to government initiatives aimed at improving diabetes management, along with growing consumer demand for health-focused solutions. This complex environment highlights the ongoing innovation and strategic flexibility required by market players to maintain and strengthen their positions.

Some of the eminent market participants operating in the self-monitoring blood glucose monitoring devices industry include:

Abbott Laboratories

AgaMatrix

All Medicus

Arkray

Ascensia Diabetes Care Holdings

B. Braun Melsungen

Bionime Corporation

DarioHealth

F. Hoffmann-La Roche

LifeScan

Nova Biomedical

Omnis Health

Sanofi

Sinocare

Ypsomed Holding

Ascensia Diabetes Care Holdings

Ascensia Diabetes Care Holdings, one of the key player in the market with a share of 4.1% in 2024. Ascensia Diabetes Care offers novel and precise glucose monitoring devices developed for simplicity while addressing diabetes care management.

LifeScan

LifeScan designs advanced patient-friendly blood glucose monitoring systems that help increase patient confidence and control.

Nova Biomedical

Nova Biomedical specializes in powerful glucose meters that provide immediate and accurate measurements for better diabetes management.

Self-monitoring Blood Glucose Monitoring Devices Industry News:

In November 2024, Ascensia Diabetes Care collaborated with Fitterfly Healthtech to develop a free 21-day Diabetes Management Program offered on Ascensia glucometer devices. It is anticipated that diabetes care will be more effective with this program.

In May 2022, ARKRAY, Inc. collaborated with Rimidi to enable wider data reach through the integration of the GLUCOCARD Shine Connex blood glucose monitoring device with the Rimidi platform, making life easier for both hospitals and patients. This partnership increased the visibility of ARKRAY’s glucose monitoring device and the overall glucose monitoring system allowing ARKRAY to expand into new markets.

The self-monitoring blood glucose monitoring devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2022 - 2035 for the following segments:

Market, By Product

Self-monitoring blood glucose meters

Consumables

Testing strips

Lancets

Market, By Application

Type 1 diabetes

Type 2 diabetes

Gestational diabetes

Market, By End Use

Hospitals

Ambulatory surgical centers

Diagnostic centers

Homecare

Other end users

The above information is provided for the following regions and countries:

3.5.1.3 Mobile applications linked to SMBG systems

3.5.2 Emerging technologies

3.5.2.1 AI enabled glucose pattern analysis and decision support

3.5.2.2 Non invasive and minimally invasive SMBG technologies

3.5.2.3 Advanced test strip chemistries and multi-parameter sensing

3.5.2.4 Integrated digital diabetes management ecosystems

3.6 Pricing analysis, 2025 (Driven by Primary Research)

3.7 Future market trends (Driven by Primary Research)

3.8 Impact of AI and Generative AI on the market (Driven by Primary Research)

3.9 Porter's analysis

3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 Global

4.2.2 North America

4.2.3 Europe

4.2.4 Asia Pacific

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Strategic dashboard

4.7 Key developments

4.7.1 Mergers and acquisitions

4.7.2 Partnerships and collaborations

4.7.3 New product launches

4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

5.1 Key trends

5.2 Self-monitoring blood glucose meters

5.3 Consumables

5.3.1 Testing strips

5.3.2 Lancets

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

6.1 Key trends

6.2 Type 1 diabetes

6.3 Type 2 diabetes

6.4 Gestational diabetes

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

7.1 Key trends

7.2 Hospital

7.3 Ambulatory surgical centers

7.4 Diagnostic centers

7.5 Homecare

7.6 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

8.1 Key trends

8.2 North America

8.2.1 U.S.

8.2.2 Canada

8.3 Europe

8.3.1 Germany

8.3.2 France

8.3.3 UK

8.3.4 Italy

8.3.5 Spain

8.3.6 Netherlands

8.4 Asia Pacific

8.4.1 China

8.4.2 Japan

8.4.3 India

8.4.4 Australia

8.4.5 South Korea

8.5 Latin America

8.5.1 Brazil

8.5.2 Mexico

8.5.3 Argentina

8.6 Middle East and Africa

8.6.1 South Africa

8.6.2 Saudi Arabia

8.6.3 UAE

Chapter 9 Company Profiles

9.1 Abbott Laboratories

9.2 AgaMatrix

9.3 All Medicus

9.4 Arkray

9.5 Ascensia Diabetes Care Holdings

9.6 B. Braun Melsungen

9.7 Bionime Corporation

9.8 DarioHealth

9.9 F. Hoffmann-La Roche

9.10 LifeScan

9.11 Nova Biomedical

9.12 Omnis Health

9.13 Sanofi

9.14 Sinocare

9.15 Ypsomed Holding

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Regional or domestic-only leaders not in the global top tier

Distributors and channel partners who control market access

Emerging disruptors, startups, or adjacent-industry entrants

Niche players focused on a specific application or end-use

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Authors: Monali Tayade, Jignesh Rawal

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at[email protected]

Self-monitoring Blood Glucose Monitoring Devices Market Size

The self-monitoring blood glucose monitoring devices market size was valued at USD 21.6 billion in 2025 and is expected to reach USD 67.8 billion in 2035, growing at a CAGR of 12.4% from 2026 to 2035, according to the latest report published by Global Market Insights Inc.

This steady growth is stimulated by various factors such as rising prevalence of diabetes worldwide, technological advancements of self-monitoring blood glucose monitoring devices in developed countries, and government initiatives for increasing awareness pertaining diabetes among people.

This market is growing due to an increasing prevalence of diabetes mellitus globally. For instance, as per the estimates from the International Diabetes Federation (IDF), 537 million people were living with diabetes worldwide in 2021. The trend is anticipated to increase that number to 643 million in 2030 and then to 783 million in 2045. As the disease is getting prevalent among patients and healthcare providers, the demand for SMBG devices is increasing in order to manage the disease.

In addition, government initiatives to increase awareness about management of diabetes mellitus aids in the early detection and is a reason for the expansion of the market as well. For instance, the U.S. National Diabetes Education Program (NDEP) is one such source wherein the advantages of SMBG devices in self-management have been brought forward. Moreover, in the European Union, screening campaigns target the high-risk groups, such as people over 45 years of age or those having a family history of diabetes, encouraging early diagnosis and thereby creating demand for diabetes-related treatments. Such efforts by the government are helping to increase awareness about this lifestyle disease as well as helping in early detection of the condition. This, in turn, helps in boosting the demand for diabetes care devices as a measure to keep the disease under control.

Self-monitoring blood glucose devices are being used since decades; these operate by pricking a finger with sharp lancet and using the blood on the strip, which is further inserted into the glucometer to measure the blood glucose level of an individual.

Self-monitoring Blood Glucose Monitoring Devices Market Trends

Self-monitoring Blood Glucose Monitoring Devices Market Analysis

Based on product, the market is segmented into self-monitoring blood glucose meters and consumables. The consumables segment is further bifurcated into testing strips and lancets. This consumables segment was valued at USD 12.1 billion in 2025.

Based on application, the self-monitoring blood glucose monitoring devices market is segmented into type 1 diabetes, type 2 diabetes, and gestational diabetes. The type 2 diabetes emerged as a dominant segment in the market, accounting for 69.3% of revenue share in 2025.

Based on end use, the self-monitoring blood glucose monitoring devices market is segmented into hospitals, ambulatory surgical centers, diagnostic centers, homecare, and other end users. Homecare accounted for the largest revenue share of 37.8% in 2025.

North America Self-monitoring Blood Glucose Monitoring Devices Market

The North America region accounted for 38.1% of the market in 2025. The market in North America is experiencing robust expansion, driven by the region’s advanced healthcare infrastructure and technological advancements.

The U.S. market size reached USD 7.6 billion in 2025, growing from USD 7 billion in 2024.

Europe Self-monitoring Blood Glucose Monitoring Devices Market

Europe, self-monitoring blood glucose monitoring devices accounted for USD 5.8 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

The self-monitoring blood glucose monitoring devices market in the UK is projected to experience steady growth between 2026 and 2035.

Asia Pacific Self-monitoring Blood Glucose Monitoring Devices Market

The Asia Pacific self-monitoring blood glucose monitoring devices is anticipated to grow at the highest CAGR of 13% during the analysis timeframe.

The China market is anticipated to witness lucrative growth during the forecast period.

Latin America Self-monitoring Blood Glucose Monitoring Devices Market

Middle East and Africa Self-monitoring Blood Glucose Monitoring Devices Market

The market in Saudi Arabia is expected to experience significant and promising growth from 2026 to 2035.

Self-monitoring Blood Glucose Monitoring Devices Market Share

Self-monitoring Blood Glucose Monitoring Devices Market Companies

Some of the eminent market participants operating in the self-monitoring blood glucose monitoring devices industry include:

Ascensia Diabetes Care Holdings, one of the key player in the market with a share of 4.1% in 2024. Ascensia Diabetes Care offers novel and precise glucose monitoring devices developed for simplicity while addressing diabetes care management.

LifeScan designs advanced patient-friendly blood glucose monitoring systems that help increase patient confidence and control.

Nova Biomedical specializes in powerful glucose meters that provide immediate and accurate measurements for better diabetes management.

Self-monitoring Blood Glucose Monitoring Devices Industry News:

The self-monitoring blood glucose monitoring devices market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2022 - 2035 for the following segments:

Market, By Product

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries: