Market Size, By Platform Type (iOS, Android, Other Platform Type), By Revenue Model (Free Apps, Subscription-Based), By Application (Depression and Anxiety Management, Meditation Management, Stress Management, Wellness Management, Other Applications), and By End Use (Home Care Settings, Mental Hospitals, Other End Users). The market forecasts are provided in terms of revenue (USD Million).

Report ID: GMI9407

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Mental Health Apps Market Size

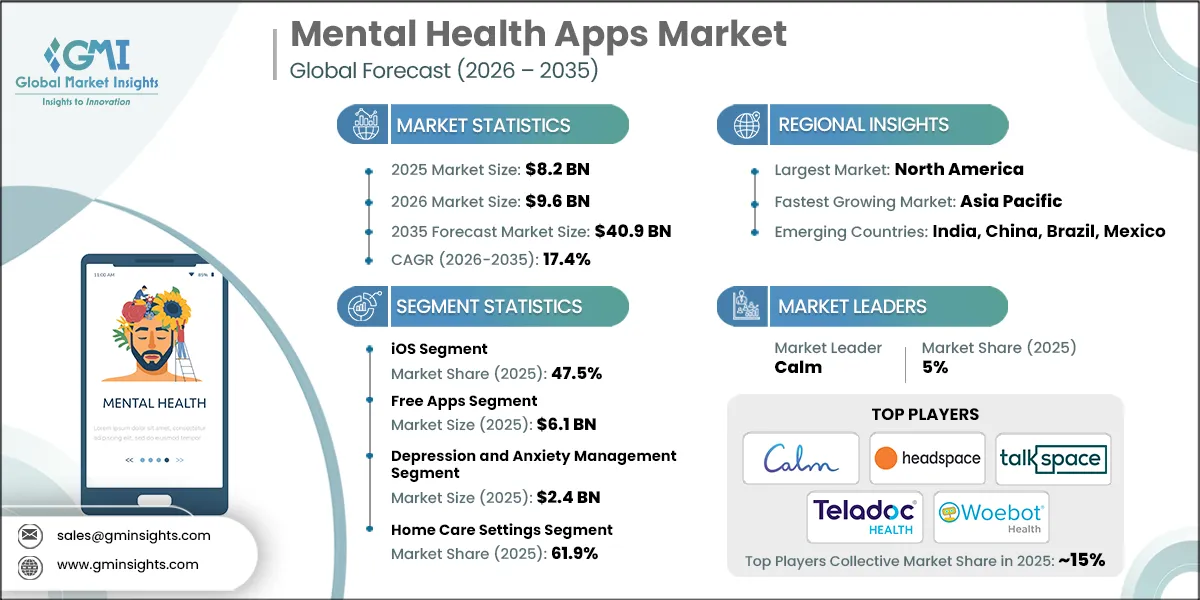

The global mental health apps market was estimated at USD 8.2 billion in 2025. The market is expected to grow from USD 9.6 billion in 2026 to USD 40.9 billion in 2035, at a CAGR of 17.4% during the forecast period, according to the latest report published by Global Market Insights Inc.

The market is driven by numerous factors, such as rising prevalence of mental health disorders and growing adoption of virtual therapy for mental health coupled with increasing awareness regarding mental health, among other factors.

Integration of AI, chatbots, and digital therapeutics, a growing focus on preventive and self-care solutions, and employer-sponsored mental wellness programs are expected to fuel the industry's growth. Calm, Headspace Inc., Talkspace, Teladoc Health, Inc., and Woebot are among the leading players operating in the market. These players mainly focus on the availability of apps on different major platforms, service innovation, geographic expansion, integration of AI in programs, and collaboration with healthcare providers and corporate businesses, among other factors.

The rising prevalence of mental health disorders is a key factor propelling the industry's growth. Governments across the world are taking potential steps to limit the target population to mental health disorders. For instance, the World Health Organization (WHO) has set up a Mental Health Action Plan 2013–2030 that focuses on providing appropriate intervention for people suffering with various mental disorders, including depression. In addition, the favorable government policies and payer support for these solutions are anticipated to contribute to the overall market growth.

Further, mental health apps provide users with tools and resources to proactively manage their mental health, prevent the onset of mental health conditions, and maintain overall well-being, thereby propelling industry growth. Additionally, many organizations are implementing corporate wellness programs to support the mental health and well-being of their employees. Mental health apps are being integrated into these programs as a cost-effective and scalable way to provide employees with access to mental health resources, stress management tools, and support services.

Mental health apps are software applications designed to provide support, resources, and tools for managing mental health and well-being. These apps can offer a wide range of features and functionalities aimed at helping users cope with stress, anxiety, depression, and other mental health conditions. Mental health apps can be accessed via smartphones, tablets, computers, wearable devices, and other digital platforms.

Mental Health Apps Market Trends

Demand for remote and on‑demand mental health support, cost-effectiveness compared to traditional therapy, and a growing focus on preventive and self-care solutions are among the key trends shaping the market growth positively.

There has been a notable increase in the prevalence of mental health disorders globally. Conditions such as depression, anxiety, stress-related disorders, PTSD, and others are affecting a growing portion of the population. For instance, according to the data reported by the National Alliance on Mental Illness, 57.8 million people, or around 22.8% of U.S. adults, experienced mental health illness in 2021. 5.5% of them were categorized under serious mental illness in the country.

Additionally, with the increasing emphasis on self-care and self-management of health, many individuals prefer to take an active role in managing their mental health. Mental health apps empower users to track their symptoms, learn coping strategies, practice mindfulness, and access therapeutic interventions independently, aligning with this trend towards self-directed healthcare.

Further, modern lifestyles are characterized by various stress factors, including work pressures, social media, financial worries, and lifestyle changes. These stress factors contribute to the development or exacerbation of mental health conditions. Thus, to deal with such situations, young people with high stress levels are opting for mental health solutions.

Mental Health Apps Market Analysis

Based on platform type, the mental health apps market is categorized into iOS, Android, and other platform type. The iOS segment accounted for a majority share of 47.5% in 2025. Increased smartphone and internet penetration is anticipated to fuel the segment's growth. The segment is expected to reach USD 18.2 billion by 2035, growing at a CAGR of 16.7% during the forecast period.

The majority of mental health apps are offered within the iOS ecosystem due to their higher engagement level and therefore higher interest in spending money and time on mental health applications.

iOS applications have the ability to foster a community of app users through consistency with privacy regulations, a seamless integration with wearable technology, and a highly developed user experience that allows iOS users to subscribe to mental health applications on a monthly basis.

Additionally, developers launch premium wellness or clinically focused apps on iOS due to iOS's reliability with respect to hardware characteristics and performance capability. By providing key features such as secure storage of health data, tracking of biometrics, and integration with an ecosystem of wearable devices like smartwatches, developers have created an ecosystem that keeps users of mental health apps engaged.

The Android segment is anticipated to record the higher growth, with a CAGR of 18.5%, to reach over USD 20.2 billion by 2035. The Android platform offers developers a high degree of customization and flexibility, allowing them to create innovative and feature-rich mental health apps tailored to specific user needs. Developers can leverage Android's open-source nature to implement unique features and functionalities that cater to diverse user preferences.

Further, Android devices seamlessly integrate with various Google services, such as Google Play Store, Google Fit, and Google Assistant. Mental health apps can leverage these integrations to enhance user experiences, access health-related data, and provide personalized recommendations and insights.

Furthermore, Android's popularity extends beyond developed countries to emerging markets and regions with limited access to mental health resources. As a result, mental health apps on the Android platform have the potential to reach users worldwide, including those in underserved communities.

Based on revenue model, the mental health apps market is categorized into free apps and subscription-based. The free apps segment generated the highest revenue of USD 6.1 billion in 2025.

Free mental health apps are accessible to a wide range of users, including those who may not have the financial means to pay for premium apps or traditional therapy services. This accessibility ensures that individuals from diverse socioeconomic backgrounds can access support and resources for managing their mental health.

Free mental health apps eliminate financial barriers to accessing mental health support, making them an attractive option for users who are unable or unwilling to pay for premium apps or therapy sessions. This affordability encourages greater adoption and usage of mental health apps among a broader demographic.

Additionally, free mental health apps play a crucial role in promoting mental health awareness and destigmatizing mental illness by providing accessible resources and support to individuals in need. These apps raise awareness about the importance of mental well-being and encourage help-seeking behavior

The subscription-based segment is anticipated to record the highest growth, with a CAGR of 17.8%. Subscription-based mental health applications have a recurring revenue model through monthly and annual plans, which offer premium resources (advanced content, customized programs, therapy access) and data-driven insights.

In addition, this model allows the company to continuously improve the features of its services, validate them clinically, and engage users for an extended period of time. As a result of the subscription model, users are able to implement structured interventions and track their progress while having access to premium resources that are customized for their needs.

Further, the subscription model is preferable as costs are predictable, and the deployment of subscription models is scalable, due to which the subscription model is appealing to both employers and insurance companies.

Based on application, the mental health apps market is categorized into depression and anxiety management, meditation management, stress management, wellness management, and other applications. The depression and anxiety management segment generated the highest revenue of USD 2.4 billion in 2025.

Depression and anxiety are among the most common mental health disorders worldwide, affecting millions of people of all ages, genders, and backgrounds. The high prevalence of these conditions has led to a growing demand for accessible and effective solutions to manage symptoms and improve overall well-being.

Additionally, depression and anxiety management apps offer users convenient access to evidence-based tools and interventions at their fingertips, anytime and anywhere. These apps empower users to engage with mental health resources from the comfort of their homes, during moments of distress, or while on the go, facilitating the integration of self-care practices into their daily routines.

Moreover, these apps empower users to proactively manage their mental well-being, equipping them with self-management skills to address symptoms and triggers effectively. They typically offer a range of resources, including psychoeducation, cognitive-behavioral therapy (CBT) techniques, mindfulness exercises, and stress reduction strategies, enabling users to take independent action towards better mental health.

The meditation management segment was valued at USD 2 billion in 2025. Meditation management applications emphasize the use of mindfulness techniques, controlled breathing exercises, relaxing methods, and soothing techniques.

These apps appeal to both clinical and non-clinical users seeking mental clarity, emotional balance, and stress reduction. Many structured meditation programmes help users maintain consistent meditation practices, while shorter sessions are useful for people with busy schedules.

Further, people commonly use meditation software to support their self-care routines, improve workplace wellness, and promote lifestyle enhancement.

The stress management segment is expected to record significant growth, with a CAGR of 17.1% over the forecast period. Stress management apps help users identify stress triggers and develop healthier responses through relaxation techniques, habit tracking, and behavioral insights.

Furthermore, the number of users of these applications is very high among both working adults and students who experience performance-related stress/anxiety. Features such as guided breathing exercises, resilience training, and time management tools are some methods available for helping users alleviate daily stress and anxiety. In addition, corporate wellness initiatives often include stress management programs due to their effectiveness at increasing employee productivity and overall health.

Based on end use, the mental health apps market is categorized into home care settings, mental hospitals, and other end-users. The home care settings segment accounted for the leading market share of 61.9% in 2025.

Mental health apps present a cost-effective solution for home care settings, empowering caregivers to offer additional support and resources to individuals without necessitating in-person visits or costly interventions. This approach not only reduces healthcare expenses but also enhances the efficiency of home care programs.

Mental health apps facilitate remote monitoring of individuals' mental well-being by caregivers, enabling them to track progress, identify emerging symptoms, and deliver timely interventions from a distance. This proactive monitoring aids in detecting changes in mental health status early, thereby averting potential crises or hospitalizations.

Moreover, the rising demand for mental health apps in home care settings stems from the necessity for convenient, cost-effective, and tailored solutions that cater to individuals' mental health needs while ensuring comfort and autonomy within their homes.

The mental hospitals segment was valued at USD 2.5 billion in 2025. Digital tools are used by clinicians to monitor patient activity, provide therapeutic assistance, and facilitate ongoing patient support after discharge from inpatient treatment facilities.

Furthermore, mental health apps can enable mental health professionals to conduct remote monitoring of their patients' symptomology and can assist in supporting adherence to treatment plans. Clinicians can benefit from enhanced outcome tracking due to integration into their clinical workflows and access to hybrid care models.

North America Mental Health Apps Market

The North America market accounted for a majority share of 57.6% in 2025 and is anticipated to show notable growth over the forecast period.

The U.S. market was valued at USD 4.4 billion in 2025 from USD 3.8 billion in 2024.

North America has a relatively high prevalence of mental health conditions such as depression, anxiety, and substance abuse disorders. The growing recognition and awareness of mental health issues have led to an increased demand for accessible and effective solutions to address these conditions.

Additionally, there is a growing acceptance of digital health solutions, including mental health apps, among both healthcare providers and consumers in the region. As perspective towards digital health continue to evolve, more individuals are willing to use technology-based tools to manage their mental health and well-being.

Europe Mental Health Apps Market

Europe accounted for a significant share of the market and was valued at USD 2.3 billion in 2025.

The market for mental health apps in Europe continues to grow due to high public awareness, innovative healthcare systems, and rising popularity of digital healthcare solutions.

Increased prevalence of stress-related disorders and an aging population, along with growing concerns about mental well-being at work, are contributing to the growth of this segment across the region.

Additionally, governments and healthcare providers are pushing for better access to early intervention and digital self-care programs, especially where access to therapists is limited.

Further, employers are introducing mental health applications as part of their employee benefit packages, which is increasing the number of businesses adopting these programs.

Asia Pacific Mental Health Apps Market

The Asia Pacific market accounted for a substantial share of the market and was valued at USD 639.8 million in 2025.

In the Asia Pacific region, there is a growing demand for mental health applications due to various factors, including increased urbanization, a large regional population, and increased smartphone penetration.

Additionally, due to stress from work, school, and lifestyle changes, there has been an increased awareness of mental health needs among young people. The low price of smartphones and access to mobile internet are contributing to increased accessibility to these apps across developed and developing countries of the region.

Both employers and governments are investing in initiatives that encourage the implementation of digital wellness programs. Users are attracted to mental health-related mobile applications due to their availability in multiple languages, localized content, and free versions.

Further, the growing adoption of these applications can also be attributed to the growing acceptance of self-care and options for digital-first health behaviors.

Latin America Mental Health Apps Market

The Latin American market is anticipated to exhibit remarkable growth during the analysis period.

In Latin America, awareness of mental wellness is rising, and consequently, mental health app use has increased as well. Factors such as economic instability, high levels of societal stress, and increasing rates of anxiety have driven more people to seek mental health support.

This has created a strong demand for easily accessible and affordable mental health solutions. The limited availability of mental health professionals in many areas makes digital solutions particularly attractive.

In addition to increased smartphone use and mobile-first engagement, app adoption has also surged among younger users due to the availability of free or low-cost apps that may help reduce barriers to access.

Employers are beginning to use mental health tools as part of their employee wellness strategy to address issues such as employee burnout and improve employee productivity.

Middle East and Africa Mental Health Apps Market

The Middle East and Africa market is expected to experience substantial growth over the analysis timeframe.

The market within the MEA region is at an early stage; however, it is growing steadily due to rising awareness of mental health issues as well as the improvement of digital infrastructures across the region.

Additionally, urbanization, youth population growth, and workplace stress are raising demand for discreet and convenient mental health solutions. Apps are particularly valuable in regions where stigma or limited clinical access restricts traditional care.

Furthermore, both public and private organizations are beginning to recognize and prioritize supporting mental health as part of larger well-being initiatives. The most common types of apps, both in terms of use and build-out, are educational and self-care apps.

Mental Health Apps Market Share

The competitive environment in the mental health application industry is fragmented in nature. There are several global players, niche specialty companies, and small start-up companies offering their services. Intense competition exists based on the relatively low barriers to entry, rapid changes in technology, and increasing levels of demand from consumers, employers, and the healthcare industry. The major players in mental health apps compete based on their brand recognition, the quality of their content, user experience with the product, and by creating broader service offerings such as meditation, therapy, mindfulness coaching, and AI assistant-type support. The key differentiators in this space are subscription-based services and enterprise contracts, both of which create predictable revenue & the ability to develop long-term relationships.

Additionally, competing through technology is an essential part of the competitive landscape, where businesses employ artificial intelligence, personalization algorithms, and data analysis to generate better results and higher levels of retention. Increasingly, companies will form partnerships with employers, insurers, healthcare providers (including hospitals), and wellness platforms to grow their user base and support their credibility.

Further, competition exists between self-guided wellness apps that provide access to therapists and platforms allowing them to provide clinical-grade telehealth services. Key competitive factors are data privacy, clinical validity, and compliance with regulations. Lastly, differentiation can be sustained by establishing user trust, the depth of user engagement, integration within a larger continuum of care, and the balancing of scalability with individualized mental health support.

Mental Health Apps Market Companies

A few of the prominent players operating in the mental health apps industry include:

Calm focuses on premium subscriptions, content-led partnerships, celebrity-led mindfulness programs, and expansion into sleep, stress, and workplace mental wellness solutions for consumers and enterprises.

Woebot focuses on AI-driven conversational therapy, scalable automated mental health support, clinical validation, and partnerships with healthcare systems to deliver always-available, cost-effective interventions.

Headspace emphasizes evidence-based mindfulness, healthcare and employer partnerships, integrated mental health services, and hybrid models combining self-guided content with professional coaching and clinical support.

Mental Health Apps Industry News

In March 2026, Give Me Five, an Australian psychological wellness startup, announced its foray into the Indian market with an initial investment of USD 3.4 million (AUD 5 million) and the launch of its GM5 app. This Give Me Five, a mental health platform, is focused on detecting early signs of conditions such as anxiety, depression, and stress, helping individuals address them before they escalate.

In August 2023, Swiss Re Reinsurance Solutions and Wysa launched the first insurance-specific mental health app, Wysa Assure, an AI-based mental health support app. The app is designed to measure an individual's risk score and meet the needs of insurers and their customers. This development enabled the company to develop similar products to cater to a wide range of patient populations, thereby improving their industry reputation in the coming years.

In October 2022, Calm launched its clinical mental health offering, Calm Health. It is a subscription-based app focused on providing condition-specific programs specially designed to 'bridge the gap between mental and physical healthcare.' This product launch has improved the company’s product portfolio and sales, generating prospects.

The global mental health apps market research report includes an in-depth coverage of the industry with estimates and forecasts in terms of revenue in (USD Million) from 2022 - 2035 for the following segments:

Market, By Platform Type

iOS

Android

Other platform type

Market, By Revenue Model

Free apps

Subscription-based

Market, By Application

Depression and anxiety management

Meditation management

Stress management

Wellness management

Other applications

Market, By End Use

Home care settings

Mental hospitals

Other end users

The above information is provided for the following regions and countries:

North America

U.S.

Canada

Europe

Germany

UK

France

Spain

Italy

Netherlands

Asia Pacific

China

Japan

India

Australia

South Korea

Latin America

Brazil

Mexico

Argentina

MEA

South Africa

Saudi Arabia

UAE

Authors: Monali Tayade, Shishanka Wangnoo

Mental Health Apps Market Scope

Mental Health Apps Market Size

Mental Health Apps Market Trends

Mental Health Apps Market Analysis

Mental Health Apps Market Share

Report Content

Chapter 1 Research Methodology

1.1 Research approach

1.2 Quality commitments

1.2.1 GMI AI policy & data integrity commitment

1.2.1.1 Source consistency protocol

1.3 Research trail & confidence scoring

1.3.1 Research trail components

1.3.2 Scoring components

1.4 Data collection

1.4.1 Partial list of primary sources

1.5 Data mining sources

1.5.1 Paid sources

1.5.1.1 Sources, by region

1.6 Base estimates and calculations

1.6.1 Base year calculation

1.7 Forecast model

1.7.1 Quantified market impact analysis

1.7.1.1 Mathematical impact of growth parameters on forecast

1.8 Research transparency addendum

1.8.1 Source attribution framework

1.8.2 Quality assurance metrics

1.8.3 Our commitment to trust

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional trends

2.2.2 Platform type trends

2.2.3 Revenue model trends

2.2.4 Application trends

2.2.5 End use trends

2.3 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing adoption of virtual therapy for mental health

3.2.1.2 Increasing awareness regarding mental health

3.2.1.3 Rise in target population suffering from mental conditions

3.2.2 Industry pitfalls and challenges

3.2.2.1 Data privacy and connectivity issues

3.2.3 Opportunities

3.2.3.1 Integration with wearable and biometric data

3.2.3.2 Corporate wellness and B2B mental health platforms

3.3 Growth potential analysis

3.4 Regulatory landscape (Driven by Primary Research)

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Future market trends (Driven by Primary Research)

3.7 Pricing analysis, 2025 (Driven by Primary Research)

3.8 Impact of AI & generative AI on the market (Driven by Primary Research)

3.8.1 AI-driven disruption of existing business models

3.8.2 GenAI use cases & adoption roadmap by segment

3.9 Reimbursement scenario

3.10 Start-up scenario

3.11 Gap analysis

3.12 Porter's analysis

3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company matrix analysis

4.3 Company market share analysis (Driven by Primary Research)

4.3.1 Global

4.3.2 North America

4.3.3 Europe

4.3.4 Asia Pacific

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Platform Type, 2022 - 2035 ($ Mn)

5.1 Key trends

5.2 iOS

5.3 Android

5.4 Other platform type

Chapter 6 Market Estimates and Forecast, By Revenue Model, 2022 - 2035 ($ Mn)

6.1 Key trends

6.2 Free apps

6.3 Subscription-based

Chapter 7 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

7.1 Key trends

7.2 Depression and anxiety management

7.3 Meditation management

7.4 Stress management

7.5 Wellness management

7.6 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

8.1 Key trends

8.2 Home care settings

8.3 Mental hospitals

8.4 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 France

9.3.4 Spain

9.3.5 Italy

9.3.6 Netherlands

9.4 Asia Pacific

9.4.1 China

9.4.2 Japan

9.4.3 India

9.4.4 Australia

9.4.5 South Korea

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.6 MEA

9.6.1 South Africa

9.6.2 Saudi Arabia

9.6.3 UAE

Chapter 10 Company Profiles

10.1 7 cups of Tea

10.2 BetterSleep

10.3 Calm

10.4 Dario Mind

10.5 Fabulous

10.6 Headspace Inc.

10.7 Mindscape

10.8 MoodMission Pty Ltd.

10.9 rhope

10.10 Spring Health

10.11 Talkspace

10.12 Teladoc Health, Inc.

10.13 Woebot

10.14 Wysa

10.15 Youper, Inc.

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Regional or domestic-only leaders not in the global top tier

Distributors and channel partners who control market access

Emerging disruptors, startups, or adjacent-industry entrants

Niche players focused on a specific application or end-use

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Authors: Monali Tayade, Shishanka Wangnoo

For inquiries regarding discounts, bulk purchases, or customization requests, please contact us at[email protected]

Explore our licensing options:

Starting at: $2,450

Premium Report Details

Base Year: 2025

Companies Profiled: 15

Tables and Figures: 150

Countries covered: 19

Pages: 140

Download Free PDF

Premium Report Details

Base Year: 2025

Companies Profiled: 15

Tables and Figures: 150

Countries covered: 19

Pages: 140

Download Free PDF

Share Content

Add Citations

Monali Tayade. 2026, April. Mental Health Apps Market - By Platform Type, By Revenue Model, By Application, By End Use - Global Forecast, 2026 - 2035 (Report ID: GMI9407). Global Market Insights Inc. Retrieved June 20, 2026, from https://www.gminsights.com/toc/details/mental-health-apps-market

Mental Health Apps Market

Get a free sample of this report

Get a free sample of this report Mental Health Apps Market

Is your requirement urgent? Please give us your business email for a speedy delivery!

Mental Health Apps Market Size

The global mental health apps market was estimated at USD 8.2 billion in 2025. The market is expected to grow from USD 9.6 billion in 2026 to USD 40.9 billion in 2035, at a CAGR of 17.4% during the forecast period, according to the latest report published by Global Market Insights Inc.

The market is driven by numerous factors, such as rising prevalence of mental health disorders and growing adoption of virtual therapy for mental health coupled with increasing awareness regarding mental health, among other factors.

Integration of AI, chatbots, and digital therapeutics, a growing focus on preventive and self-care solutions, and employer-sponsored mental wellness programs are expected to fuel the industry's growth. Calm, Headspace Inc., Talkspace, Teladoc Health, Inc., and Woebot are among the leading players operating in the market. These players mainly focus on the availability of apps on different major platforms, service innovation, geographic expansion, integration of AI in programs, and collaboration with healthcare providers and corporate businesses, among other factors.

The rising prevalence of mental health disorders is a key factor propelling the industry's growth. Governments across the world are taking potential steps to limit the target population to mental health disorders. For instance, the World Health Organization (WHO) has set up a Mental Health Action Plan 2013–2030 that focuses on providing appropriate intervention for people suffering with various mental disorders, including depression. In addition, the favorable government policies and payer support for these solutions are anticipated to contribute to the overall market growth.

Further, mental health apps provide users with tools and resources to proactively manage their mental health, prevent the onset of mental health conditions, and maintain overall well-being, thereby propelling industry growth. Additionally, many organizations are implementing corporate wellness programs to support the mental health and well-being of their employees. Mental health apps are being integrated into these programs as a cost-effective and scalable way to provide employees with access to mental health resources, stress management tools, and support services.

Mental health apps are software applications designed to provide support, resources, and tools for managing mental health and well-being. These apps can offer a wide range of features and functionalities aimed at helping users cope with stress, anxiety, depression, and other mental health conditions. Mental health apps can be accessed via smartphones, tablets, computers, wearable devices, and other digital platforms.

Mental Health Apps Market Trends

Demand for remote and on‑demand mental health support, cost-effectiveness compared to traditional therapy, and a growing focus on preventive and self-care solutions are among the key trends shaping the market growth positively.

Mental Health Apps Market Analysis

Based on platform type, the mental health apps market is categorized into iOS, Android, and other platform type. The iOS segment accounted for a majority share of 47.5% in 2025. Increased smartphone and internet penetration is anticipated to fuel the segment's growth. The segment is expected to reach USD 18.2 billion by 2035, growing at a CAGR of 16.7% during the forecast period.

Based on revenue model, the mental health apps market is categorized into free apps and subscription-based. The free apps segment generated the highest revenue of USD 6.1 billion in 2025.

Based on application, the mental health apps market is categorized into depression and anxiety management, meditation management, stress management, wellness management, and other applications. The depression and anxiety management segment generated the highest revenue of USD 2.4 billion in 2025.

Based on end use, the mental health apps market is categorized into home care settings, mental hospitals, and other end-users. The home care settings segment accounted for the leading market share of 61.9% in 2025.

North America Mental Health Apps Market

The North America market accounted for a majority share of 57.6% in 2025 and is anticipated to show notable growth over the forecast period.

Europe Mental Health Apps Market

Europe accounted for a significant share of the market and was valued at USD 2.3 billion in 2025.

Asia Pacific Mental Health Apps Market

The Asia Pacific market accounted for a substantial share of the market and was valued at USD 639.8 million in 2025.

Latin America Mental Health Apps Market

The Latin American market is anticipated to exhibit remarkable growth during the analysis period.

Middle East and Africa Mental Health Apps Market

The Middle East and Africa market is expected to experience substantial growth over the analysis timeframe.

Mental Health Apps Market Share

The competitive environment in the mental health application industry is fragmented in nature. There are several global players, niche specialty companies, and small start-up companies offering their services. Intense competition exists based on the relatively low barriers to entry, rapid changes in technology, and increasing levels of demand from consumers, employers, and the healthcare industry. The major players in mental health apps compete based on their brand recognition, the quality of their content, user experience with the product, and by creating broader service offerings such as meditation, therapy, mindfulness coaching, and AI assistant-type support. The key differentiators in this space are subscription-based services and enterprise contracts, both of which create predictable revenue & the ability to develop long-term relationships.

Additionally, competing through technology is an essential part of the competitive landscape, where businesses employ artificial intelligence, personalization algorithms, and data analysis to generate better results and higher levels of retention. Increasingly, companies will form partnerships with employers, insurers, healthcare providers (including hospitals), and wellness platforms to grow their user base and support their credibility.

Further, competition exists between self-guided wellness apps that provide access to therapists and platforms allowing them to provide clinical-grade telehealth services. Key competitive factors are data privacy, clinical validity, and compliance with regulations. Lastly, differentiation can be sustained by establishing user trust, the depth of user engagement, integration within a larger continuum of care, and the balancing of scalability with individualized mental health support.

Mental Health Apps Market Companies

A few of the prominent players operating in the mental health apps industry include:

Calm focuses on premium subscriptions, content-led partnerships, celebrity-led mindfulness programs, and expansion into sleep, stress, and workplace mental wellness solutions for consumers and enterprises.

Woebot focuses on AI-driven conversational therapy, scalable automated mental health support, clinical validation, and partnerships with healthcare systems to deliver always-available, cost-effective interventions.

Headspace emphasizes evidence-based mindfulness, healthcare and employer partnerships, integrated mental health services, and hybrid models combining self-guided content with professional coaching and clinical support.

Mental Health Apps Industry News

The global mental health apps market research report includes an in-depth coverage of the industry with estimates and forecasts in terms of revenue in (USD Million) from 2022 - 2035 for the following segments:

Market, By Platform Type

Market, By Revenue Model

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries: