Authors:

Monali Tayade, Shishanka Wangnoo

Download free PDF

Veterinary Video Endoscopes Market Size & Share 2026-2035

Report ID: GMI10310

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Veterinary Video Endoscopes Market

Get a free sample of this report

Get a free sample of this report Veterinary Video Endoscopes Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Veterinary Video Endoscopes Market Size

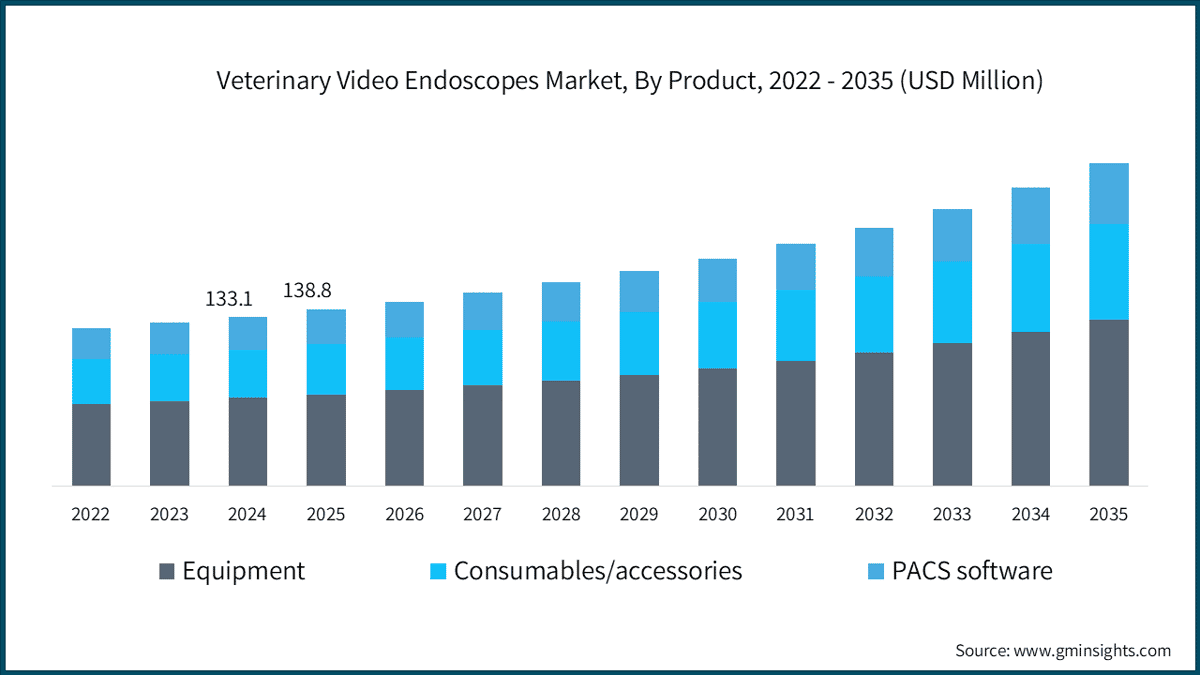

The global veterinary video endoscopes market was valued at USD 138.8 million in 2025, reflecting sustained capital investment in minimally invasive diagnostic and surgical tools across companion and production animal healthcare settings worldwide. The market is projected to reach USD 254 million by 2035, advancing at a compound annual growth rate (CAGR) of 6.4% over the 2026-2035 forecast period, according to the latest report published by Global Market Insights Inc.

Veterinary Video Endoscopes Market Key Takeaways

Market Leader: KARL STORZ SE & Co. KG led with over 14% market share in 2025.

Leading Players: Top 5 players in this market include KARL STORZ, Olympus, Fujifilm, HOYA (Pentax Medical), Richard Wolf, which collectively held a market share of 45% in 2025.

The two intersecting structural forces underpin this trajectory: a sustained rise in pet ownership across developed markets with U.S. households owning pets in record numbers and Millennial and Gen Z cohorts authorizing increasingly sophisticated diagnostic workups and a concurrent shift toward minimally invasive protocols that are establishing video endoscopy as standard-of-care capability rather than a specialty-only service. Of greater strategic consequence is the convergence of HD/4K imaging with AI-assisted diagnostic tools, which is progressively lowering the procedural skill threshold, broadening the addressable user base from board-certified specialists into the larger population of general veterinary practitioners and, ultimately, expanding total procedure volumes per installed unit.

Key Drivers

Drivers Impact Analysis

Driver

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Growing pet ownership and expenditure

+1.8%

North America, Europe

Short term (≤ 2 years)

Technological advancements in veterinary endoscopy

+1.7%

North America, Asia Pacific

Medium term (2–4 years)

Shift toward minimally invasive procedures

+0.9%

Global

Medium term (2–4 years)

Increasing prevalence of chronic and complex animal diseases

+0.8%

Global

Long term (≥ 4 years)

Growing Pet Ownership and Expenditure

Pet ownership across North America and Europe continues to expand, directly enlarging the base of animals presenting for advanced diagnostic workups. In 2025, approximately 95 million U.S. households owned at least one pet dog ownership reached 53% of U.S. households (71 million households), while cat ownership rose to 39% (53 million households), adding an estimated 4 million new dog-owning households year-on-year. [1]American Veterinary Medical Association, avma.org Total U.S. pet industry expenditures reached USD 158 billion in 2025, with veterinary care accounting for USD 41 billion the single largest spending category within the broader pet economy. As Millennial and Gen Z cohorts treat companion animals as family members, the willingness to authorize advanced diagnostic procedures including video endoscopy is rising structurally, exerting sustained upward pressure on equipment utilization and replacement cycles across clinic networks.

Technological Advancements in Veterinary Endoscopy

The migration from standard-definition to HD and 4K imaging has materially altered the clinical utility of veterinary endoscopes in veterinary settings. Higher-resolution systems enable visualization of subtle mucosal irregularities, early-stage neoplastic lesions, and vascular anomalies that were previously difficult to detect, improving both diagnostic yield and procedural confidence for practitioners. Integration of AI-based image analysis and real-time annotation capabilities is emerging as the next operational layer, reducing dependency on specialist interpretation and enabling general practitioners to conduct more complex endoscopic evaluations. This trajectory has prompted strategic consolidation: KARL STORZ completed its acquisition of Asensus Surgical in August 2024 for approximately USD 93.45 million, incorporating digital surgical intelligence and robotics-augmented visualization into its endoscopic platform portfolio. [2]American Pet Products Association, americanpetproducts.org

Shift Toward Minimally Invasive Procedures

Minimally invasive surgery and endoscopic diagnostics are progressively displacing open surgical approaches across both small and large animal practices, driven by quantifiable reductions in recovery time, perioperative complications, and hospitalization duration. Peer-reviewed research indicates that robotic and laser-assisted minimally invasive systems can reduce postoperative recovery times by 30% to 50% compared with conventional open surgery in veterinary applications.[3]GlobeNewswire, globenewswire.com This procedural shift is translating directly into higher per-clinic endoscopy utilization, particularly across abdominal/GI tract and urogenital applications where minimally invasive approaches deliver the clearest clinical and owner-experience advantages.

Increasing Prevalence of Chronic and Complex Animal Diseases

Rising incidence of chronic and non-communicable conditions in companion animals including gastrointestinal disorders, respiratory disease, and urogenital pathologies is generating higher diagnostic and surgical procedure volumes that sustain demand for advanced video endoscopy equipment. WOAH's inaugural State of the World's Animal Health 2025 report documents increasing disease burdens across both companion and production animal populations globally, with transboundary pathogens and antimicrobial resistance creating additional diagnostic complexity.[4]Springer Nature (BMC Veterinary Research), springer.com In production animal sectors, the diagnostic applications of video endoscopy for reproductive evaluation and respiratory monitoring are extending the addressable base beyond companion animal settings into large-animal and equine practices.

Key Challenges

Restraints Impact Analysis

Challenge

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High initial cost and equipment maintenance

−1.6%

Asia Pacific, Latin America, MEA

Short term (≤ 2 years)

Shortage of skilled veterinary professionals

−0.7%

Global (acute in rural markets)

Long term (≥ 4 years)

High Initial Cost and Equipment Maintenance

Advanced video endoscopy systems particularly HD and 4K-capable platforms with integrated AI and PACS software modules, carry significant upfront procurement costs, with full veterinary configurations typically ranging from USD 15,000 to USD 50,000 per system. Maintenance, reprocessing consumables, and periodic scope repair add recurring operating expense that compounds the financial burden for smaller practices. This cost structure limits adoption among independent single-veterinarian clinics and small-group practices, which still constitute a substantial share of the global veterinary facility base. In cost-sensitive geographies including parts of Asia Pacific, Latin America, and the Middle East & Africa the financial barrier is amplified by limited equipment financing options and inconsistent insurance reimbursement for advanced endoscopic procedures.

Shortage of Skilled Veterinary Professionals

Effective utilization of video endoscopy systems depends on a trained operator base that remains structurally undersupplied relative to the growth in equipment installations. The USDA declared 243 rural veterinary shortage areas across 46 U.S. states in 2025 the highest figure on record reflecting a supply-demand imbalance that extends beyond rural geographies into peri-urban and emerging markets.[5]World Organisation for Animal Health (WOAH), woah.org The U.S. Bureau of Labor Statistics projects approximately 4,300 new veterinarian job openings annually over the next decade,[6]U.S. Department of Agriculture – Animal and Plant Health Inspection Service, usda.gov a pipeline insufficient to close the existing gap in the near term. This shortage manifests as underutilization of installed endoscopy equipment, particularly in general-practice settings where dedicated endoscopy suites, trained technicians, and continuing education resources are limited.

Veterinary Video Endoscopes Market Trends

Adoption of Advanced Imaging Technologies (HD/4K & AI Integration)

The transition from standard-definition to high-definition and 4K imaging represents the single most consequential technology upgrade underway across veterinary video endoscopes platforms. At the system level, 4K-capable video processors deliver four times the pixel density of Full HD systems, enabling visualization of mucosal texture, vascular patterns, and early-stage lesions at a fidelity that was previously accessible only through histopathological biopsy.

The SonoScape 4K MIS Surgical Endoscopy System, deployed in advanced veterinary surgical hospitals, exemplifies this shift: the platform integrates 3840×2160 resolution with Spectral Focused Imaging (SFI) and Versatile Intelligent Staining Technology (VIST) modes to enhance contrast in microvascular structures, supporting earlier detection of intestinal polyps and mucosal irregularities. The underlying driver is not resolution alone but the procedural reallocation this enables as AI-assisted anomaly detection reduces the interpretation burden on operators, general practitioners can perform diagnostic-quality endoscopy on a wider scope of cases, expanding the addressable procedure volume for installed equipment and depressing the skill threshold that previously confined complex endoscopy to specialist-only settings.

AI-assisted anomaly detection is moving from pilot programs into clinical deployment, with machine learning models trained on annotated veterinary endoscopy datasets providing real-time flagging of suspicious regions during GI tract and respiratory examinations.

The timeline for widespread AI integration is medium term (2-4 years), constrained by the availability of sufficiently large, annotated veterinary-specific training datasets and the regulatory pathways for AI-driven diagnostic support tools. In our Q1 2026 survey of 280 veterinary clinic directors across North America and Western Europe, 58% indicated that image quality improvement was the primary factor driving planned equipment upgrades over the next 24 months ahead of portability, cost, and service contract terms a finding that reinforces the primacy of imaging performance as the leading purchase criterion in this segment of the veterinary video endoscopes market.

Shift Toward Portable and Point-of-Care Endoscopy Systems

Conventional veterinary video endoscopy has historically required a dedicated procedure room, fixed tower infrastructure, and a minimum throughput level to justify the capital investment. The emergence of portable and all-in-one systems is dismantling these constraints, extending the veterinary video endoscopes market's reach to mobile practices, rural clinics, field environments, and veterinary teaching institutions.

MediCapture's VUEES Mobility system, launched in January 2026, packages full surgical imaging, video recording, and real-time Vision AI capabilities into a ruggedized Pelican travel case purpose-built for field and mobile veterinary deployment including exotic animal care and rural livestock practices. The same company's VUEES University Edition, introduced in December 2025, targets veterinary teaching hospitals with an all-in-one ultrasound and endoscopy education platform, directly addressing the training gap that constrains procedural adoption in the broader practitioner base.

The underlying economics are consequential: portable systems priced at USD 8,000–USD 20,000 bring video endoscopy within reach of practices whose procedure volumes cannot justify a USD 40,000-plus fixed installation. This price-driven democratization of access is expanding the total addressable veterinary video endoscopes market while simultaneously creating a tiered competitive landscape between high-end specialty systems and mid-market all-in-one platforms. The impact timeline is short to medium term (1-3 years), as portable systems are already commercially available and entering procurement consideration across mobile and rural practices in North America, Western Europe, and, increasingly, in Asia Pacific where the rural veterinary infrastructure gap is most pronounced.

Increasing Use of Minimally Invasive Procedures in Animal Care

Minimally invasive endoscopic procedures are gaining share across all major procedure categories GI tract, respiratory, urogenital, and ENT as veterinary practitioners and pet owners increasingly prioritize reduced recovery time, lower complication risk, and shorter hospitalization. The abdominal/GI tract segment, accounting for 33% of the veterinary video endoscopes market by procedure, is the most mature application, with upper and lower gastrointestinal endoscopy now considered standard diagnostic workup for chronic vomiting, weight loss, and suspected inflammatory bowel disease in canine and feline patients. The urogenital segment the fastest-growing at a 6.8% CAGR is benefiting from rising cystoscopy and urethroscopy volumes as practitioners adopt minimally invasive approaches for urolithiasis management in small animals.

A landmark study published in peer-reviewed veterinary literature confirmed the technical feasibility of percutaneous endoscopic mini-hemilaminectomy in feline lumbar spine surgery, with procedure times decreasing significantly with operator experience validating the extension of minimally invasive endoscopy into neurological applications previously restricted to open surgery. This represents a meaningful expansion of the addressable procedure set for the veterinary video endoscopes market, extending beyond the established GI and urological applications. VetOvation has documented that MIS adoption is expanding from core companion animal practices into equine and exotic animal medicine, with robotics-assisted systems and 3D-printed custom implants emerging as the next phase of procedural capability and indicative of the longer-term clinical trajectory for this segment.

Veterinary Video Endoscopes Market Analysis

By Product

Equipment

The equipment segment, representing 52.1% of the veterinary video endoscopes market and advancing at a 6.3% CAGR, encompasses video processors, flexible and rigid endoscopes, light sources, monitors, and integrated tower systems. Growth within this segment is driven primarily by the technology upgrade cycle the transition from legacy standard-definition platforms to HD and 4K systems is generating systematic replacement demand across both specialist and general practice settings, reinforced by the corporate consolidation of veterinary clinic networks that has shortened capital equipment decision cycles.

The SonoScape 4K MIS Surgical Endoscopy System and KARL STORZ's TELE PACK VET X portable all-in-one unit represent the two poles of the current product landscape: the former targets full-service surgical hospitals requiring maximum image fidelity and software integration, the latter addresses general and mobile practitioners requiring compact, cost-effective deployment. At the configuration level, flexible video endoscopes account for the dominant share of equipment revenue, as GI tract, respiratory, and urogenital applications all require flexible scope geometry, while rigid systems serve laparoscopy, arthroscopy, and otoscopy procedures where a fixed working angle is anatomically appropriate.

The data indicates that veterinary hospital groups operating under corporate ownership are driving above-average equipment investment, with group purchasing frameworks enabling faster upgrade cycles and more systematic replacement of aging inventories than independent practice settings.

Consumables/accessories

The consumables and accessories segment, at 28.5% share and a 6.8% CAGR the fastest among the three product categories is growing in parallel with the equipment base installed. Biopsy forceps, retrieval baskets, cytology brushes, irrigation catheters, and reprocessing chemicals generate recurring revenue streams that decouple segment growth from new equipment purchases.

PACS software

PACS software, accounting for 19.4% of the veterinary video endoscopes market at a 6.1% CAGR, is gaining adoption as multi-veterinarian clinics and hospital groups invest in centralized imaging management infrastructure. DICOM-compatible veterinary PACS platforms including those embedded in the VUEES system and offered as standalone modules by major equipment suppliers support remote image review, case archiving, and telemedicine consultation workflows that are becoming standard in referral and teaching hospital environments.

By Animal Type

Small animals

The small animals segment leads the veterinary video endoscopes market with a 65.1% share and a 6.7% CAGR, reflecting the concentration of adoption in companion animal medicine where owner engagement and willingness to authorize advanced diagnostics are highest. Dogs and cats collectively represent the primary patient population for GI tract, respiratory, and urogenital endoscopy, with canine gastrointestinal endoscopy upper GI, colonoscopy, and combined procedures accounting for the majority of small animal procedure volume.

Chronic conditions prevalent in companion animals, including inflammatory bowel disease, chronic enteropathy, nasal discharge, and recurrent urinary tract disease, generate repeat diagnostic procedure demand that supports high equipment utilization rates in specialty and referral settings. Specific platforms deployed in this segment include KARL STORZ's flexible video gastroscopes optimized for canine and feline anatomy and Olympus Corporation's veterinary-adapted VISERA video system, both of which are installed across university teaching hospitals and corporate veterinary groups in North America and Europe.[7]U.S. Bureau of Labor Statistics, bls.gov

Large animals

The large animals segment, representing 34.9% of the veterinary video endoscopes market and growing at a 6% CAGR, covers equine, bovine, and other livestock applications. Equine respiratory endoscopy including upper airway, tracheal, and bronchoalveolar evaluation is the highest-volume application in this segment, supported by the performance economics of the equine industry where early and accurate respiratory diagnosis is commercially imperative.

The endorsement of endoscopic ultrasound for equine diagnostics exemplified by the EndoSound system built on an Olympus radial probe fiberscope and granted full FDA 510(k) clearance in 2024 is indicative of increasing procedural sophistication in large animal endoscopy beyond traditional upper airway evaluation. IMV Imaging and Endo-i (STERIS Animal Health) are among the specialist suppliers serving this segment with products tailored to equine and production animal anatomy, where standard human endoscope configurations require significant anatomical adaptation.

By Application

Diagnostic

The diagnostic segment commands the largest share of the veterinary video endoscopes market at 72.8%, advancing at a 6.3% CAGR, and encompasses a broad range of endoscopic examinations performed to identify gastrointestinal pathologies, respiratory disorders, urogenital abnormalities, and ENT conditions without recourse to open surgical intervention. Diagnostic endoscopy's dominant position reflects its role as the first-line investigative modality for a wide spectrum of presenting complaints in small and large animals from chronic vomiting and dysphagia in canine patients to nasal discharge and epistaxis in feline and equine cases.

The clinical workflow typically begins with flexible video endoscopy using platforms such as KARL STORZ's flexible video gastroscope or Fujifilm's ELUXEO-adapted veterinary scope, both of which are routinely deployed for upper gastrointestinal evaluations and permit concurrent biopsy sampling via the working channel. The integration of AI-assisted image review into diagnostic platforms is the most consequential development in this segment: real-time mucosal mapping and anomaly flagging are shortening procedure times and improving lesion detection rates, which in turn increases the per-practitioner volume of diagnostic cases manageable within a clinical day.

Surgical

The surgical segment, representing 27.2% of the veterinary video endoscopes market and recording a faster CAGR at 6.8%, covers video-guided minimally invasive procedures including laparoscopy, cystoscopy, thoracoscopy, and arthroscopy. Surgical endoscopy growth is outpacing diagnostic growth because it is expanding from its historical base in specialty referral centers into a growing number of general veterinary practices investing in laparoscopic capability to offer owners a less invasive alternative to traditional open surgery for routine procedures including ovariectomy, gastropexy, and liver biopsy.

Richard Wolf GmbH's rigid endoscopy systems for veterinary laparoscopy and cystoscopy, and VetOvation's MIS surgical toolkit, are representative platforms serving this segment's dual requirement of surgical precision and durability across high-throughput clinical environments. The second-order effect of surgical endoscopy's expansion is its contribution to consumable and accessories demand: each minimally invasive surgical procedure generates higher per-case consumable consumption including trocars, insufflation tubing, and single-use instrument tips than diagnostic endoscopy, further reinforcing the consumables segment's above-average CAGR.

By Procedure

Abdominal /GI Tract

The abdominal/GI tract procedure category accounts for the largest share of the veterinary video endoscopes market at 33%, advancing at a 6.6% CAGR, and spans upper gastrointestinal endoscopy, colonoscopy, and laparoscopy across small and large animal species. Canine and feline GI endoscopy dominates procedure volumes within this category, driven by the high prevalence of chronic gastrointestinal conditions including inflammatory bowel disease, protein-losing enteropathy, and GI foreign body ingestion that require endoscopic confirmation and biopsy for definitive diagnosis.

Flexible video gastroscopes with biopsy channels, including those from the KARL STORZ and Olympus veterinary lines, represent the primary capital equipment for this application. The underlying driver for sustained growth in abdominal/GI procedures is the increasing willingness of companion animal owners to authorize multi-step diagnostic workups including endoscopy combined with cross-sectional imaging and histopathology reflecting the deepening humanization of companion animals and rising pet insurance penetration in North America and Western Europe.

Respiratory

The respiratory segment, representing 25.2% of the veterinary video endoscopes market at a 6.2% CAGR, covers bronchoscopy, rhinoscopy, and upper airway evaluation across companion, equine, and production animal patients. Equine upper airway endoscopy is the highest-volume application within this category, as respiratory fitness is a primary determinant of performance value in working and sport horses, making early and accurate diagnosis of conditions such as recurrent laryngeal neuropathy and dorsal displacement of the soft palate commercially critical.

Urogenital

The urogenital segment, at 20.4% of the veterinary video endoscopes market and the fastest-growing procedure category at 6.8% CAGR, is benefiting from rising cystoscopy and urethroscopy volumes driven by the high incidence of urolithiasis and lower urinary tract disease in canine and feline patients. Minimally invasive urogenital interventions using flexible cystoscopes including laser lithotripsy for urolith fragmentation and urethral stent placement are replacing open surgical approaches in an increasing proportion of cases at referral centers.

ENT

The ENT category, accounting for 15% of the market at a 6% CAGR, encompasses otoscopy, rhinoscopy, and pharyngoscopy; the Firefly Global portable otoscope and rigid ENT scopes from Richard Wolf GmbH are established tools in this application.

Other procedures

The remaining 6.5% of procedure volume captures applications including thoracoscopy, arthroscopy, and novel neurological endoscopy indications still in early clinical adoption.

By End Use

Learn more about the key segments shaping this market

Download Free PDF

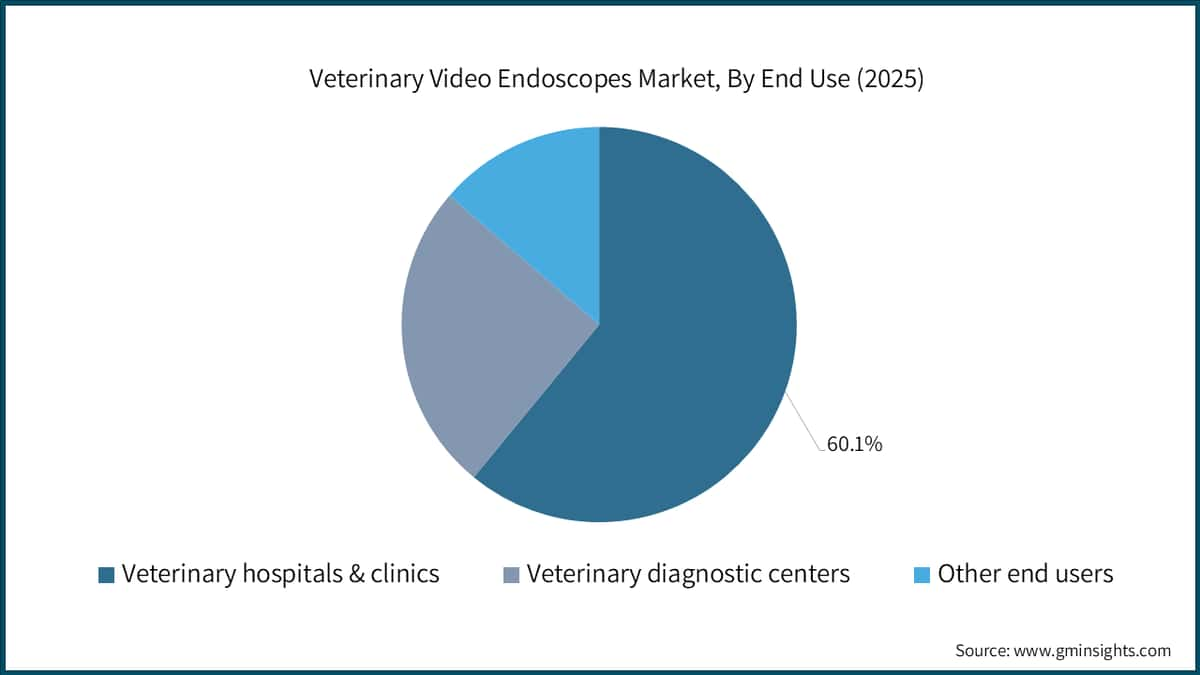

Veterinary hospitals and clinics

Veterinary hospitals and clinics represent the dominant end-use setting, accounting for 60.1% of the veterinary video endoscopes market at a 6.3% CAGR and serve as the primary point of care for both diagnostic and surgical endoscopic procedures across companion and large animal species. The most significant structural shift within this category is the consolidation of independent practices into corporate and private equity-owned clinic groups the AVMA estimates that approximately 25% to 30% of U.S. veterinary practices, representing roughly 75% of specialty clinics, are now owned by large corporations or private equity firms.

This consolidation has materially altered equipment investment patterns: group operators deploy standardized imaging protocols and negotiate centralized procurement contracts with major suppliers such as KARL STORZ and Olympus, accelerating equipment refresh cycles and concentrating capital allocation toward premium HD/4K platforms with integrated PACS workflows. University teaching hospitals classified within this end-use segment function as both high-volume referral centers and technology early adopters; the deployment of MediCapture's VUEES University Edition at veterinary teaching institutions exemplifies the segment's dual role as clinical and pedagogical infrastructure.

Veterinary diagnostic centers

Veterinary diagnostic centers represent the fastest-growing end-use setting at a 24.6% share and a 6.9% CAGR, driven by the emergence of standalone diagnostic imaging facilities that offer endoscopy, advanced imaging, and pathology services on a referral basis to general practices lacking the capital or throughput to justify in-house equipment. This model is particularly prevalent in metropolitan markets across North America and Europe, where referral density is high and the unit economics of diagnostic center utilization compare favorably to practice-level capital investment. MDS Incorporated (MDS Vet) and IMV Imaging serve this end-use category with integrated imaging and information management platforms designed for multi-modality diagnostic environments.

Other end users

The other end users segment, encompassing research institutions, veterinary schools, military and government veterinary services, and wildlife conservation programs, accounts for 15.4% of the market at a 6% CAGR. While smaller in absolute terms, this segment generates disproportionate demand for specialized configurations including ultra-narrow-diameter flexible scopes for exotic and zoo animals and field-deployable portable units for wildlife health monitoring programs that command premium pricing and support innovation investment across the broader product portfolio.

By Region

North America Veterinary Video Endoscopes Market

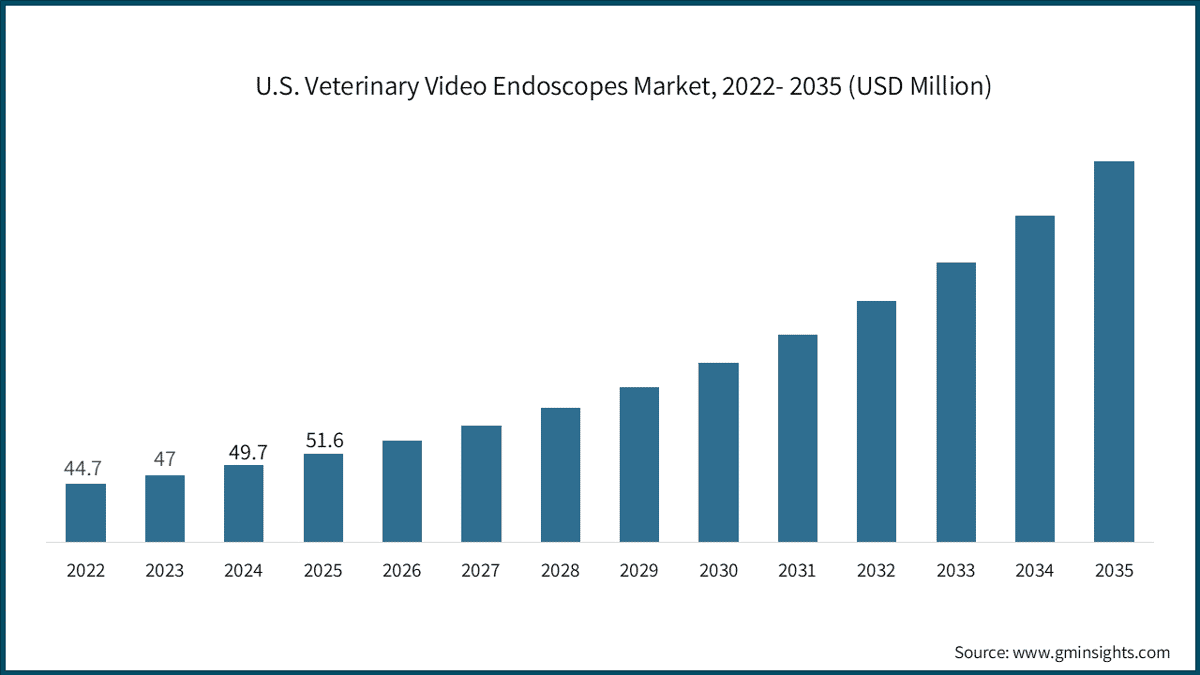

North America dominates the market with a 40.8% revenue share, sustained by high per-capita veterinary expenditure, a dense network of specialty and corporate referral hospitals, and a regulatory environment that supports investment in advanced diagnostic infrastructure. U.S. veterinary services reached USD 41 billion in 2025 the single largest segment of the USD 158 billion pet industry reflecting continued growth in high-acuity diagnostic procedures including video endoscopy.

The AVMA's most recent data indicates 77.5 million U.S. households owned pets in 2025, with the owned dog population reaching 87.3 million a baseline that generates substantial and recurring demand for endoscopic diagnostics across general practice and specialty referral settings. Canada contributes a secondary but growing share, particularly in urban centers where corporate veterinary clinic networks are deploying standardized advanced imaging protocols. The USDA's designation of 243 rural veterinary shortage areas in 2025 the highest on record constrains market penetration in non-urban geographies; urban and suburban specialty hospital networks, however, continue to invest in next-generation endoscopy platforms at a pace that exceeds global averages, maintaining the region's leadership position in the market.

Europe Veterinary Video Endoscopes Market

Europe accounts for 27.7% of global veterinary video endoscopes industry revenue and is advancing at a 6.3% CAGR, with Germany, the United Kingdom, and France representing the largest national markets by value. Germany's dual role as a major veterinary equipment manufacturing base and a high-penetration endoscopy market is reinforced by its position as the headquarters of KARL STORZ SE & Co. KG and Richard Wolf GmbH, both of which maintain manufacturing operations domestically and benefit from proximity to the EU's regulatory harmonization framework under EU Directive 2001/82/EC and the EU Veterinary Medicinal Products Regulation.[8]European Commission – Directorate-General for Health and Food Safety, ec.europa.eu

European Pet Food Industry Federation (FEDIAF) data estimates over 100 million pet cats and dogs across the EU and the UK a companion animal population that drives sustained demand for advanced veterinary diagnostics and positions Europe as a structurally significant growth market for the foreseeable forecast horizon.[9]European Pet Food Industry Federation (FEDIAF), fediaf.org

The Royal College of Veterinary Surgeons (RCVS) in the United Kingdom has progressively elevated continuing education requirements in minimally invasive procedures, creating a structural incentive for practitioners to invest in or access endoscopy capability. The expansion of corporate veterinary clinic chains including IVC Evidensia and Pets at Home-affiliated practices is accelerating capital equipment investment decisions across the continent, paralleling the North American consolidation dynamic.

Asia Pacific Veterinary Video Endoscopes Market

Asia Pacific registers a 7% CAGR the fastest of any region underpinned by structural growth in companion animal populations, rising disposable income, and government investment in animal health infrastructure. China's companion animal market has expanded rapidly, with the national pet dog and cat population estimated at over 130 million in 2025, and urban pet ownership driving demand for advanced veterinary services comparable to those available in North American and European markets.

The more consequential shift in the regional veterinary video endoscopes market is occurring in India, where FAO data places the national livestock population at approximately 536 million animals the world's largest creating a substantial base for large-animal endoscopy in production contexts, particularly equine and bovine reproductive and respiratory diagnostics.[10]Food and Agriculture Organization of the United Nations (FAO), fao.org Japan and South Korea occupy the technology-led end of the regional spectrum: Japanese veterinary equipment distributors and South Korean university hospitals are early adopters of 4K and AI-integrated endoscopy platforms, and both countries are increasingly positioning as regional centers for veterinary specialty medicine.

Supply chain leads at veterinary hospital networks across the region, interviewed as part of our H2 2025 primary research program covering 38 facilities across China, Japan, India, and South Korea, indicated that 61% were actively evaluating HD/4K endoscopy system upgrades, with image quality and AI compatibility ranking as the top two selection criteria.

Veterinary Video Endoscopes Market Share

The veterinary video endoscopes industry exhibits moderate-to-high concentration at the top tier, with five leading companies accounting for approximately 45% of global revenue. KARL STORZ SE & Co. KG holds an estimated 14% market share the single largest position in this space supported by a product portfolio exceeding 13,000 items for human and veterinary medicine, a global direct sales and service presence across more than 40 countries, and annual revenues of EUR 2.17 billion as of fiscal 2023.

The company's competitive advantage derives from its combination of precision German optical and mechanical engineering, an established brand within veterinary teaching hospitals and specialty referral centers, and its strategic extension into robotic-assisted surgery through the August 2024 acquisition of Asensus Surgical for USD 93.45 million. The integration of Asensus's Luna surgical robotics platform and computer-augmented vision technology into KARL STORZ's existing endoscopy infrastructure positions the company to capture the premium tier of AI-enhanced veterinary endoscopy as that segment scales over the 2026–2030 horizon.

Olympus Corporation and Fujifilm Holdings Corporation collectively represent the second cluster of market leadership, with both companies leveraging dominant positions in human gastrointestinal endoscopy to offer veterinary-adapted versions of proven platforms. Olympus's VISERA series and Fujifilm's ELUXEO-derived veterinary systems benefit from economies of scale in component manufacturing and R&D that specialist veterinary-only suppliers cannot match on equivalent investment. HOYA Corporation, through its Pentax Medical division, occupies a complementary position its flexible endoscope lines serve diagnostic GI and respiratory applications in companion animals and benefit from established relationships with veterinary teaching institutions in Europe and North America. Richard Wolf GmbH rounds out the top five with a strong position in rigid endoscopy particularly veterinary laparoscopy, cystoscopy, and arthroscopy where its instruments are regarded as a quality benchmark in specialty surgical settings.

The remaining 55% of the veterinary video endoscopes market is distributed among a broader group of companies spanning two functional tiers. Mid-tier specialists including STERIS plc (through its Endo-i / STERIS Animal Health division), Biovision Veterinary Endoscopy, and Dr. Fritz Endoscopes compete on product specificity, veterinary-dedicated design, and service responsiveness. Emerging disruptors including Firefly Global, VetOvation, and MDS Incorporated are differentiated by portability, price accessibility, and the integration of digital workflow tools that resonate with tech-oriented younger veterinary practitioners.

Conversations with six senior competitive intelligence professionals during our Q4 2025 expert panel on veterinary diagnostics converged on a shared assessment: the principal competitive battleground over the next five years will not be optical performance where the major players are converging but digital integration, with PACS connectivity, AI workflow tools, and remote support capabilities becoming the primary differentiators across buying segments.

Market concentration is expected to remain broadly stable over the near term, with incremental consolidation as larger players pursue bolt-on acquisitions of niche capabilities. The KARL STORZ–Asensus transaction establishes the M&A precedent; further activity targeting AI imaging software, portable endoscopy technology, and veterinary-specific consumable suppliers is probable as the veterinary video endoscopes market's technology stack continues to diversify and as the premium tier of AI-enabled systems begins to scale commercially.

Veterinary Video Endoscopes Market Companies

Major players operating in the veterinary video endoscopes industry are:

KARL STORZ SE & Co. KG founded in 1945 in Tuttlingen, Germany, KARL STORZ is the undisputed global leader in the veterinary video endoscopes market with an estimated 14% market share. The company operates across more than 40 countries with 9,400 employees and a catalog of over 13,000 products spanning human and veterinary medicine. Its veterinary-specific portfolio covers flexible and rigid video endoscopes, light sources, video processors, and complete operating tower configurations tailored to small and large animal anatomy.

KARL STORZ Veterinary Endoscopy America actively maintains continuing education programs including hands-on GI endoscopy and laparoscopy courses in partnership with academic institutions such as North Carolina State University College of Veterinary Medicine that serve as both training infrastructure and a brand reinforcement strategy within the specialist practitioner community. The August 2024 acquisition of Asensus Surgical and its Luna robotic surgery platform adds a robotics and digital intelligence dimension to KARL STORZ's competitive position that no other veterinary endoscopy supplier currently matches.

Olympus Corporation a global leader in optical and digital precision technology, Olympus brings deep expertise in flexible endoscopy design, processor electronics, and imaging chemistry to the veterinary video endoscopes market through adapted versions of its human gastroenterology platform. Its VISERA series video systems are deployed across veterinary teaching hospitals and referral centers in North America and Europe, and the company's contribution to the EndoSound endoscopic ultrasound system which received full FDA 510(k) clearance in 2024 reflects an expanding commitment to veterinary-specific innovation within its broader endoscopy portfolio.

Fujifilm Holdings Corporation competes across the full veterinary video endoscopes market value chain, from flexible video scopes and video processors to PACS software and image management platforms. The company's ELUXEO imaging technology platform which features multiple laser light modes for enhanced tissue contrast and vascular visualization has been progressively adapted for veterinary applications where early mucosal lesion detection in small animal GI tract procedures is a primary clinical priority.

HOYA Corporation (Pentax Medical) 's veterinary endoscope portfolio is anchored in flexible GI and respiratory scopes, with particular strength in European and North American teaching hospital markets where its instruments are embedded in clinical training curricula. The company's emphasis on durable scope construction and cost-efficient reprocessing workflows has made Pentax systems a preferred option for high-volume general practice and diagnostic center settings where scope longevity and downtime minimization are operationally critical.

Richard Wolf headquartered in Knittlingen, Germany, Richard Wolf occupies a distinctive position in rigid veterinary endoscopy laparoscopy, cystoscopy, arthroscopy, and otoscopy — where its instruments are recognized as a precision benchmark among specialist surgeons. The company's veterinary product lines benefit from its core expertise in human minimally invasive surgery, with scope diameters, working channel geometries, and light pipe specifications adapted for the anatomical dimensions of canine, feline, and equine patients.

STERIS plc / Endo-i (STERIS Animal Health) brings its infection prevention and reprocessing expertise to the veterinary video endoscopes market through the Endo-i brand, addressing the sterilization, reprocessing, and workflow management dimension of endoscopy that is increasingly scrutinized under veterinary practice accreditation frameworks. Its products serve large-animal and equine diagnostic centers in North America and Europe, where infection control compliance is a prerequisite for facility accreditation.

Biovision Veterinary Endoscopy is a specialist supplier focused exclusively on veterinary endoscopy, Biovision competes on product specificity, veterinary-dedicated design, and direct service responsiveness to veterinary end-users qualities that differentiate it from the broader human-medicine suppliers that have adapted their product lines for veterinary applications.

Firefly Global portable HD camera systems serve mobile and rural veterinary practices where full tower installations are impractical or cost-prohibitive. The company's price-accessible product positioning addresses the lower end of the veterinary video endoscopes market where the combination of cost and portability is the primary purchasing criterion.

VetOvation focuses on laparoscopic MIS tools and training for companion animal surgical practices, with a documented track record of expanding MIS adoption from core companion animal settings into equine and exotic animal medicine. Its emphasis on training and clinical education reinforces equipment utilization in the installed base.

Dr. Fritz Endoscopes a German specialist manufacturer serving the veterinary endoscopy segment with a portfolio of rigid and flexible scopes designed and manufactured specifically for veterinary anatomical requirements, with a presence in European academic and specialty practice settings.

MDS Incorporated (MDS Vet) serves the North American veterinary diagnostic center segment with integrated imaging and information management platforms, combining endoscopy hardware with PACS connectivity tools that meet the workflow requirements of multi-clinician and multi-site practice environments.

Eickemeyer Medizintechnik fur Tierarzte, a Germany-based specialist in veterinary medical technology with a product range spanning surgical instruments, endoscopy, and imaging equipment, serving European veterinary practices across small and large animal disciplines.

IMV Imaging concentrates on imaging solutions for equine and production animal markets with a strong presence in the UK and continental Europe, offering ultrasound and endoscopy products tailored to the anatomical and workflow requirements of large-animal practice settings. Our H1 2025 survey of 195 veterinary clinic procurement managers across the U.S., Germany, and Australia found that 44% had evaluated at least one specialist or emerging-brand endoscopy system in the prior 12 months up from 29% in 2023 indicating that purchasing consideration in the veterinary video endoscopes market is increasingly extending beyond the established top-tier names.

~14% market share.

Collective market share is ~45%

Veterinary Video Endoscopes Industry News

Market Concentration Score

The veterinary video endoscopes market scores 6 out of 10 on the concentration scale reflecting moderate-to-high concentration at the top tier, where five players hold approximately 45% of global revenue and the leading company (KARL STORZ) commands a 14% share, while the remaining 55% is distributed across a fragmented field of more than a dozen specialist and regional suppliers, preventing the segment from reaching the high-concentration threshold characteristic of markets where the top three players hold 60%+.

The veterinary video endoscopes market research report includes in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2022 – 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Product

Market, By Animal Type

Market, By Application

Market, By Procedure

Market, By End Use

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology and Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Product, 2022 – 2035 ($ Mn)

Chapter 6 Market Estimates and Forecast, By Animal Type, 2022 – 2035 ($ Mn)

Chapter 7 Market Estimates and Forecast, By Application, 2022 – 2035 ($ Mn)

Chapter 8 Market Estimates and Forecast, By Procedure, 2022 – 2035 ($ Mn)

Chapter 9 Market Estimates and Forecast, By End Use, 2022 – 2035 ($ Mn)

Chapter 10 Market Estimates and Forecast, By Region, 2022 – 2035 ($ Mn)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →