Summary

Table of Content

U.S. Tooth Filling Materials Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

U.S. Tooth Filling Materials Market Size

The U.S. tooth filling materials market size was valued at USD 749.3 million in 2024. The market is expected to reach from USD 789.4 million in 2025 to USD 1.3 billion in 2034, growing at a CAGR of 5.5% during the forecast period, according to the latest report published by Global Market Insights Inc. Rising incidence of dental ailments, growing demand for cosmetic dentistry, technological advancements, an aging population, and increasing awareness of oral health are driving market growth.

U.S. Tooth Filling Materials Market Key Takeaways

Market Size & Growth

- 2024 Market Size: USD 749.3 Million

- 2025 Market Size: USD 789.4 Million

- 2034 Forecast Market Size: USD 1.3 Billion

- CAGR (2025–2034): 5.5%

Regional Dominance

- Largest Market: South Atlantic

- Fastest Growing Region: North East

Key Market Drivers

- Increasing prevalence of dental caries.

- Growing awareness regarding dental care and hygiene.

- Rising demand for dental aesthetics.

Challenges

- Toxicity associated with silver amalgams.

- High cost of advanced dental materials and procedures.

Opportunity

- Technological innovation in bioactive and nanocomposite materials.

- Rising adoption of digital dentistry and CAD/CAM technology.

Key Players

- Market Leader: Ivoclar led with over 14% market share in 2024.

- Leading Players: Top 5 players in this market include Lvoclar, Dentsply Sirona, 3M, Kuraray, Envista, which collectively held a market share of 40% in 2024.

Get Market Insights & Growth Opportunities

The U.S. market offers advanced dental restoration products that enhance clinical efficiency, patient comfort, and aesthetic outcomes. Materials such as composite resins, glass ionomers, amalgams, and ceramics are widely used by dentists for cavity restoration and cosmetic procedures. Leading market players include 3M Company, Dentsply Sirona, Envista Holdings Corporation, GC America Inc., and Ivoclar Vivadent. These companies remain competitive by continuously innovating biomaterials, maintaining extensive distribution networks across the U.S., establishing strategic partnerships with dental institutions and professionals, and investing heavily in R&D to address evolving patient needs and regulatory standards.

The market has increased from USD 600.9 million in 2021 and reached USD 703.3 million in 2023. The growth of the U.S. tooth filling materials market is primarily driven by the rising prevalence of dental disorders such as cavities, tooth decay, and dental caries, which continue to affect a large portion of the population. Increased consumption of sugary foods and beverages, along with poor oral hygiene practices, has amplified the need for restorative dental procedures. Additionally, the growing geriatric population, more prone to tooth wear, enamel loss, and root caries, further fuels the demand for durable and aesthetic filling materials.

Technological advancements have also been a major catalyst for market expansion. The introduction of nanocomposites, bioactive glass ionomers, and hybrid composite adhesives has significantly improved the durability, adhesion, and aesthetic appeal of dental restorations. Moreover, the increasing adoption of computer-aided design and manufacturing (CAD/CAM) technology in dental practices has enhanced precision in filling procedures, reducing dental chair time and improving patient satisfaction.

Tooth filling materials are restorative substances used to repair and restore teeth damaged by decay, fractures, or wear. These materials such as composite resins, amalgams, glass ionomers, and ceramics restore tooth function, integrity, and aesthetics, preventing further decay and maintaining oral health by sealing cavities and protecting tooth structure.

To get key market trends

U.S. Tooth Filling Materials Market Trends

The increasing incidence of dental caries is one of the principal drivers of the U.S. market for tooth-filling materials. Dental caries, or tooth decay, is a widespread condition that occurs among large segments of the population, including children, adults, and the elderly.

- Habits like excessive intake of sweets and colas, low oral hygiene strategies, and changes in lifestyle have been major contributors to the rising rate of cavities. The resultant increased disease burden has led to a greater demand for restorative dental treatments, which subsequently drives the demand for high-tech tooth-filling materials.

- Technological developments have also enhanced this need. The creation of high-performance composite resins, bioactive glass ionomers, and nanocomposite materials has enhanced the durability, aesthetics, and biocompatibility of fillings. Advances in digital dentistry, such as computer-aided design and manufacturing (CAD/CAM) systems, enable accurate customization of restorations, minimizing treatment time while improving patient satisfaction. Progress in adhesive technologies and minimally invasive procedures guarantees improved long-term results, raising patient acceptance and preference for restorative treatment.

- From a macroeconomic perspective, rising disposable incomes and increased healthcare spending in the U.S. enable a larger patient base to access advanced dental treatments. Government and private insurance reimbursement policies also reduce out-of-pocket costs for restorative procedures, promoting adoption. On the microeconomic level, dental clinics and laboratories are investing in modern equipment and materials to meet patient expectations, strengthen brand reputation, and maintain competitive advantage.

- Overall, the increasing prevalence of dental caries, coupled with technological innovation and favorable economic factors, continues to drive significant growth in the U.S. market. This trend underscores the importance of product development, R&D investment, and adoption of advanced restorative solutions to address the growing clinical demand and improve oral health outcomes across the population.

U.S. Tooth Filling Materials Market Analysis

")

Learn more about the key segments shaping this market

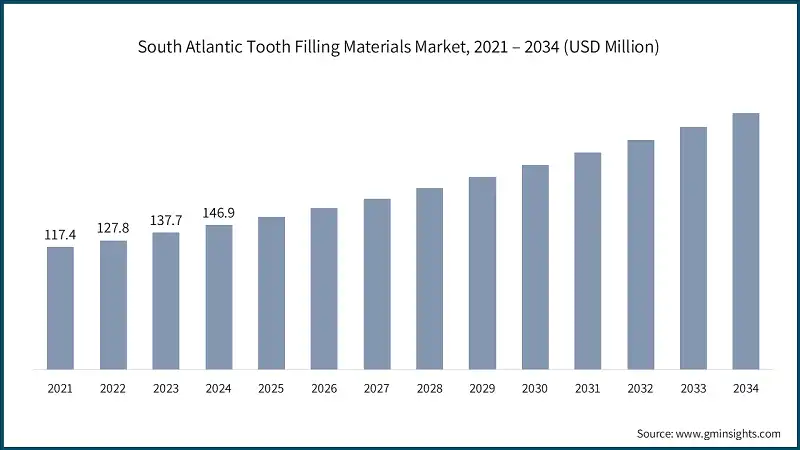

The U.S. market was valued at USD 600.9 million in 2021. The market size reached USD 703.3 million in 2023, from USD 653.4 million in 2022.

Based on the device type, the U.S. market is segmented into composite resin, silver amalgam, glass ionomer, gold fillings, and other products. The composite resin segment has asserted its dominance in the market by securing a significant market share of 34.7% in 2024, driven by the high aesthetic appeal, tooth-colored appearance, strong adhesion, minimally invasive procedures, and growing demand for cosmetic dentistry. The segment is expected to exceed USD 459.1 million by 2034, growing at a CAGR of 5.9% during the forecast period.

On the other hand, the silver amalgam segment is expected to grow with a CAGR of 5.6%. The growth of this segment can be attributed to the durability, cost-effectiveness, long-term performance, widespread historical usage, and ease of application support that continue to demand silver amalgam fillings.

- The composite resin segment dominates the U.S. tooth-filling materials market due to its superior aesthetic appeal and natural tooth-colored appearance, making it the preferred choice in cosmetic dentistry.

- Advances in technology have enhanced the bonding strength, durability, and wear resistance of these materials to enable minimally invasive approaches with greater preservation of natural tooth structure. Moreover, advances in nanocomposites and better adhesive systems maximize the life and performance of restorations.

- Rising awareness about oral health and preventive dentistry has further fueled adoption, as dental professionals can provide effective and visually appealing treatments.

- The silver amalgam segment held a revenue of USD 241.9 million in 2024, with projections indicating a steady expansion at 5.6% CAGR from 2025 to 2034. The silver amalgam segment continues to hold a significant share in the market due to its durability, cost-effectiveness, and long-term performance. Amalgam fillings are highly resistant to wear and fracture, making them suitable for restoring posterior teeth subjected to heavy chewing forces. Their ease of application and ability to set quickly make them popular among dental practitioners for efficient restorative procedures.

- Despite growing cosmetic trends, the segment benefits from widespread historical usage and patient familiarity, which ensures continued demand in both public and private dental practices. Technological refinements in alloy composition have improved biocompatibility and reduced mercury concerns, further supporting adoption.

- The glass ionomer segment held a revenue of USD 164.8 million in 2024, with projections indicating a steady expansion at 5.4% CAGR from 2025 to 2034. The glass ionomer segment is driven by its unique combination of fluoride release, chemical bonding, and biocompatibility, making it highly suitable for preventive and restorative dentistry. Its ability to release fluoride helps reduce secondary caries, offering long-term oral health benefits, particularly for children and elderly patients.

- Technological advancements, including resin-modified glass ionomers and improved adhesion properties have enhanced strength, durability, and aesthetic appeal, making them competitive with traditional composites.

Learn more about the key segments shaping this market

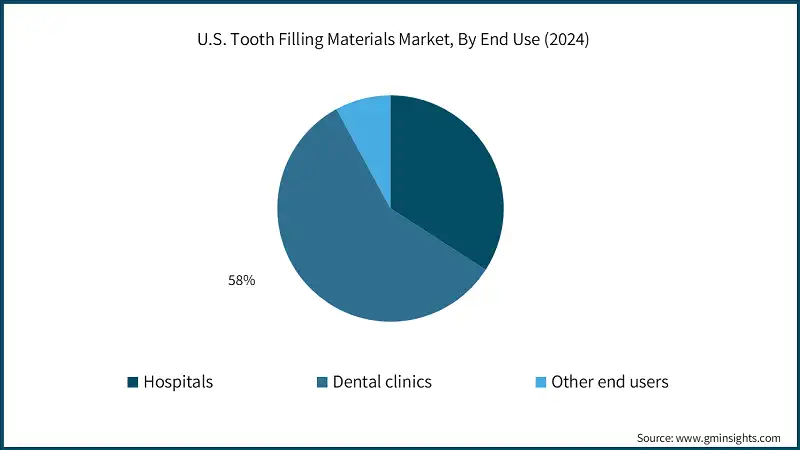

Based on end use, the U.S. tooth filling materials market is classified into hospitals, dental clinics, and other end users. The dental clinics segment dominated the market with a revenue share of 58% in 2024 and is expected to reach USD 758.2 million within the forecast period.

- The two largest segments account for over 92.1% of the total market value. The segment of hospitals has a significant share with the provision of extensive dental care services and sophisticated infrastructure to carry out restorative procedures.

- Referral of complicated dental treatment cases to hospitals provides steady demand for quality filling materials. The availability of dental specialists and coordination with the rest of the medical services enable effective treatment of comorbid patients and facilitate high volumes of procedures.

- Technology, like CAD/CAM systems and computerized imaging, is increasingly used within hospitals to increase accuracy, patient outcomes, and workflow effectiveness. Hospitals also deal with high-risk geriatric and pediatric patients who are helped by biocompatible and preventive restoration materials such as glass ionomers.

- The dental clinics segment held a revenue of USD 434.3 million in 2024, with projections indicating a steady expansion at 5.7% CAGR from 2025 to 2034. The dental clinics segment in the U.S. market is driven by increasing patient visits for routine dental care, cosmetic treatments, and preventive dentistry.

- Clinics offer personalized and convenient care, allowing dental professionals to build strong patient relationships and encourage regular cavity restoration procedures. Rising awareness of oral hygiene and aesthetic dentistry has led patients to seek composite and tooth-colored fillings, further boosting the demand.

- Technological integration, including digital dentistry, laser treatments, and adhesive materials, enhances procedural efficiency and patient satisfaction in clinic settings. The growing number of private and specialty dental clinics, along with urbanization and increased disposable incomes, facilitates greater accessibility to advanced restorative treatments.

Looking for region specific data?

South Atlantic Tooth Filling Materials Market

South Atlantic dominated the U.S. market with the highest market share of 19.6% in 2024.

- The South Atlantic zone is the leader in the U.S. market because of a combination of high population density, expanding dental service availability, and growing awareness about oral health. Florida, Georgia, and North Carolina have established healthcare infrastructure in terms of sophisticated hospitals, specialist dental clinics, and institutions, making access to restorative and cosmetic dental treatments easy.

- In the zone, the increasing geriatric population with susceptibility to tooth decay and cavities highly increases demand for long-lasting and cosmetic filling materials. Technological uptake, such as digital dentistry, CAD/CAM systems, and new composite and glass ionomer products, improves efficiency of treatment and patient satisfaction in both urban and suburban areas.

- Additionally, favorable economic factors such as rising disposable incomes, higher insurance penetration, and government-supported dental programs encourage patients to seek high-quality restorative treatments.

Northeast Tooth Filling Materials Market

Northeast market accounted for USD 119 million in 2024 and is anticipated to show lucrative growth over the forecast period.

- The Northeast tooth filling materials market is driven by a combination of demographic, economic, and technological factors. The zone has a high concentration of urban populations with greater awareness of oral health and increasing demand for cosmetic dentistry, which boosts the adoption of aesthetic restorative materials like composite resins and ceramics.

- Rising prevalence of dental caries, particularly among children and the elderly, further fuels the need for preventive and restorative treatments. Advanced healthcare infrastructure, including well-equipped hospitals, specialized dental clinics, and academic dental institutions, facilitates the use of innovative materials and techniques, supporting market growth.

- Technological advancements, such as CAD/CAM systems, digital imaging, and bioactive filling materials, are widely adopted in the zone, improving procedural efficiency and patient outcomes.

- Additionally, higher disposable incomes, robust insurance coverage, and favorable reimbursement policies enable greater access to advanced dental restorations, making the Northeast a lucrative and steadily expanding market for tooth-filling materials.

East North Central Tooth Filling Materials Market

The East North Central market is anticipated to grow at a high CAGR of 5.9% during the analysis timeframe.

- The East North Central zone is experiencing high growth in the tooth filling material market due to increased incidence of dental caries and improved awareness of oral health among the population. Urbanization and increased disposable incomes have improved access to sophisticated dental care, while the demand for cosmetic and aesthetic dentistry is driving the use of tooth-colored composite resins.

- Technological innovations, including CAD/CAM systems, digital impressions, and bioactive restorative materials, have enhanced treatment accuracy, productivity, and patient satisfaction, prompting dental practitioners to embrace contemporary filling options.

- Additionally, a robust presence of leading dental clinics, hospitals, and dental laboratories in metropolitan areas facilitates widespread availability of advanced materials. Favorable reimbursement policies and insurance coverage in the zone further enhance patient affordability for restorative procedures.

U.S. Tooth Filling Materials Market Share

The U.S. market is highly competitive, with leading dental material manufacturers emphasizing product innovation, advanced biomaterials, and strategic collaborations to strengthen their market presence. The rising prevalence of dental caries, growing demand for cosmetic and minimally invasive dentistry, and increasing awareness of oral health are driving companies to invest in R&D, digital dentistry integration, and advanced restorative solutions to enhance treatment outcomes and patient satisfaction. Additionally, the shift toward value-based dental care and broader insurance coverage are encouraging manufacturers to develop cost-effective, patient-centric materials and expand their reach across dental clinics, hospitals, and specialty practices.

Key players include Ivoclar, Dentsply Sirona, 3M, Kuraray, and Envista, collectively accounting for approximately 40% of the U.S. market. These companies maintain leadership through extensive product portfolios, strong U.S. distribution networks, and continuous advancements in composite resins, glass ionomers, and other tooth filling materials. Their dominance is reinforced by strategic partnerships with dental professionals, hospitals, and academic institutions to enhance accessibility and adoption.

Smaller and niche players are also gaining traction by focusing on innovative, biocompatible, and aesthetic materials tailored to pediatric, geriatric, and high-risk patient populations. Competitive differentiation is increasingly defined by the ability to provide durable, visually appealing, and technologically advanced restorations. As the market evolves, competition is expected to intensify, with both established leaders and emerging firms pursuing product innovation, digital dentistry solutions, and strategic alliances to capture greater market share.

U.S. Tooth Filling Materials Market Companies

A few of the prominent players operating in the Tooth Filling Materials industry include:

- 3M

- BISCO

- COLTENE

- DenMat

- Dentsply Sirona

- detax

- Envista

- GC International

- Ivoclar

- KETTENBACH DENTAL

- KULZER

- Kuraray

- PENTRON

- SDI

- SHOFU

- Tokuyama

- VOCO

- Ivoclar

Ivoclar emphasizes advanced composite technologies to deliver aesthetic, efficient restorations. Their strategy focuses on simplifying workflows for clinicians through bulk-fill solutions and promoting minimally invasive, patient-friendly procedures.

Dentsply Sirona integrates restorative materials with digital dentistry platforms like CEREC. Their strategy centers on innovation in hybrid composites, enhancing chairside efficiency, and offering durable, aesthetic solutions that streamline treatment and improve patient outcomes.

3M leverages its expertise in nanotechnology to develop high-performance composites. Their strategy focuses on delivering strong, aesthetic restorations with simplified application techniques, supporting clinicians with reliable, science-backed materials for consistent clinical success.

U.S. Tooth Filling Materials Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 749.3 Million |

| Market Size in 2025 | USD 789.4 Million |

| Forecast Period 2025 – 2034 CAGR | 5.5% |

| Market Size in 2034 | USD 1.3 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Increasing prevalence of dental caries | Growing incidence of cavities and tooth decay drives higher demand for restorative materials, expanding dental treatment procedures and market growth nationwide. |

| Growing awareness regarding dental care and hygiene | Enhanced patient knowledge encourages regular dental visits, early interventions, and preventive care, boosting demand for tooth filling materials. |

| Rising demand for dental aesthetics | Preference for natural-looking, tooth-colored restorations increases adoption of cosmetic filling materials, driving innovation and boosting overall market revenue. |

| Pitfalls & Challenges | Impact |

| Toxicity associated with silver amalgams | Concerns about mercury content limit patient acceptance and usage of amalgam fillings, negatively affecting demand for traditional restorative materials. |

| High cost of advanced dental materials and procedures | Elevated pricing restricts affordability for some patients, slowing adoption of premium composite and ceramic restorations, impacting overall market growth. |

| Opportunities: | Impact |

| Technological innovation in bioactive and nanocomposite materials | Development of longer-lasting, tooth-repairing materials will enhance treatment outcomes, attract new patients, and significantly expand market potential. |

| Rising adoption of digital dentistry and CAD/CAM technology | Integration of precise, customized restorations improves efficiency and aesthetics, creating a high-growth avenue for filling materials aligned with modern dental practices. |

| Market Leaders (2024) | |

| Market Leaders |

Around 14% |

| Top Players |

Collective market share in 2024 is Around 40% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | South Atlantic |

| Fastest growing market | North East |

| Future outlook |

|

What are the growth opportunities in this market?

Tooth Filling Materials Industry News:

- In March 2025, Ivoclar Group launched Tetric Plus, a new simplified composite material. It is specially designed to set new standards in universal composites. This development is expected to further help the company in improving and consolidating its industry presence.

- In August 2024, COLTENE Holding AG launched the tooth whitening product BRILLIANT Lumina. This product launch may enhance their product offerings and improve their presence in the dental preservation and aesthetics segment.

- In June 2024, Kuraray Noritake Dental launched the CLEARFIL MAJESTY ES Flow Universal, a high-viscosity flowable composite. The product offers exceptional aesthetics and superior physical properties. This product launch enabled the company to improve its product offering and sales prospects in the industry.

The U.S. tooth filling materials market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Million from 2021 – 2034 for the following segments:

Market, By Product

- Composite resin

- Silver amalgam

- Glass ionomer

- Gold fillings

- Other products

Market, By End Use

- Hospitals

- Dental clinics

- Other end users

The above information is provided for the following zones and states:

- East North Central

- Illinois

- Indiana

- Michigan

- Ohio

- Wisconsin

- West South Central

- Arkansas

- Louisiana

- Oklahoma

- Texas

- South Atlantic

- Delaware

- Florida

- Georgia

- Maryland

- North Carolina

- South Carolina

- Virginia

- West Virginia

- Washington, D.C.

- Northeast

- Connecticut

- Maine

- Massachusetts

- New Hampshire

- Rhode Island

- Vermont

- New Jersey

- New York

- Pennsylvania

- East South Central

- Alabama

- Kentucky

- Mississippi

- Tennessee

- West North Central

- Iowa

- Kansas

- Minnesota

- Missouri

- Nebraska

- North Dakota

- South Dakota

- Pacific Central

- Alaska

- California

- Hawaii

- Oregon

- Washington

- Mountain States

- Arizona

- Colorado

- Utah

- Nevada

- New Mexico

- Idaho

- Montana

Frequently Asked Question(FAQ) :

How big is the U.S. tooth filling materials market?

The U.S. tooth filling materials industry was valued at approximately USD 703.3 million in 2023 and is expected to grow at a 5.5% CAGR from 2024 to 2032, driven by the increasing prevalence of dental caries and rising demand for dental aesthetics.

Why is the use of composite resins rising?

The composite resin segment recorded revenues of around USD 242.6 million in 2023 and is gaining popularity due to its ability to closely match the color of natural teeth, making it a preferred choice for aesthetic dental solutions.

What is the size of the South Atlantic tooth filling materials market?

The South Atlantic tooth filling materials market accounted for USD 137.7 million in 2023 and is anticipated to grow at a 5.6% CAGR between 2024 and 2032, driven by population density and increasing dental care awareness.

Who are some of the prominent players in the U.S. tooth filling materials market?

Key players in the industry include 3M, Coltene Whaledent, Den-Mat, Dentspy Sirona, Envista, GC America, Ivoclar Vivadent, Kulzer, and Kuraray Noritake Dental.

What is the market size of the U.S. tooth filling materials market in 2024?

The market size was USD 749.3 million in 2024, driven by the rising incidence of dental caries, growing awareness of oral hygiene, and increasing adoption of advanced restorative materials in cosmetic dentistry.

What is the projected market value of the U.S. tooth filling materials industry by 2034?

The market is expected to reach USD 1.3 billion by 2034, growing at a CAGR of 5.5%, fueled by technological advancements in biomaterials, expansion of digital dentistry, and rising patient preference for minimally invasive and aesthetic dental treatments.

What is the estimated market size of the U.S. tooth filling materials market in 2025?

The market is projected to reach USD 789.4 million in 2025, supported by increased adoption of nanocomposites, bioactive glass ionomers, and CAD/CAM-enabled restorations improving treatment precision and outcomes.

Which product segment led the U.S. tooth filling materials market in 2024?

The composite resin segment dominated the market with a 34.7% share in 2024, valued at USD 260 million, owing to its superior aesthetics, strong adhesion, and preference for tooth-colored restorations in cosmetic dentistry.

Which end-use segment generated the highest revenue in 2024?

The dental clinics segment held the largest share of 58% in 2024, generating USD 434.3 million, driven by increasing patient visits for preventive and aesthetic treatments and the integration of digital dental technologies.

Which region leads the U.S. tooth filling materials industry?

The South Atlantic region led the market with a 19.6% share in 2024, supported by high population density, advanced dental infrastructure, and strong adoption of aesthetic and preventive dental treatments.

Who are the key players in the U.S. tooth filling materials market?

Key players include Ivoclar, Dentsply Sirona, 3M, Kuraray, Envista, COLTENE, GC International, Kulzer, Tokuyama, and VOCO, collectively accounting for around 40% of the market share through product innovation and strong U.S. distribution networks.

U.S. Tooth Filling Materials Market Scope

Related Reports