Authors:

Ankit Gupta, Vinayak Shukla

Download free PDF

Stationary Hydrogen Energy Storage Market Size & Share 2026-2035

Report ID: GMI11050

|

Published Date: May 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Stationary Hydrogen Energy Storage Market

Get a free sample of this report

Get a free sample of this report Stationary Hydrogen Energy Storage Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Stationary Hydrogen Energy Storage Market Size

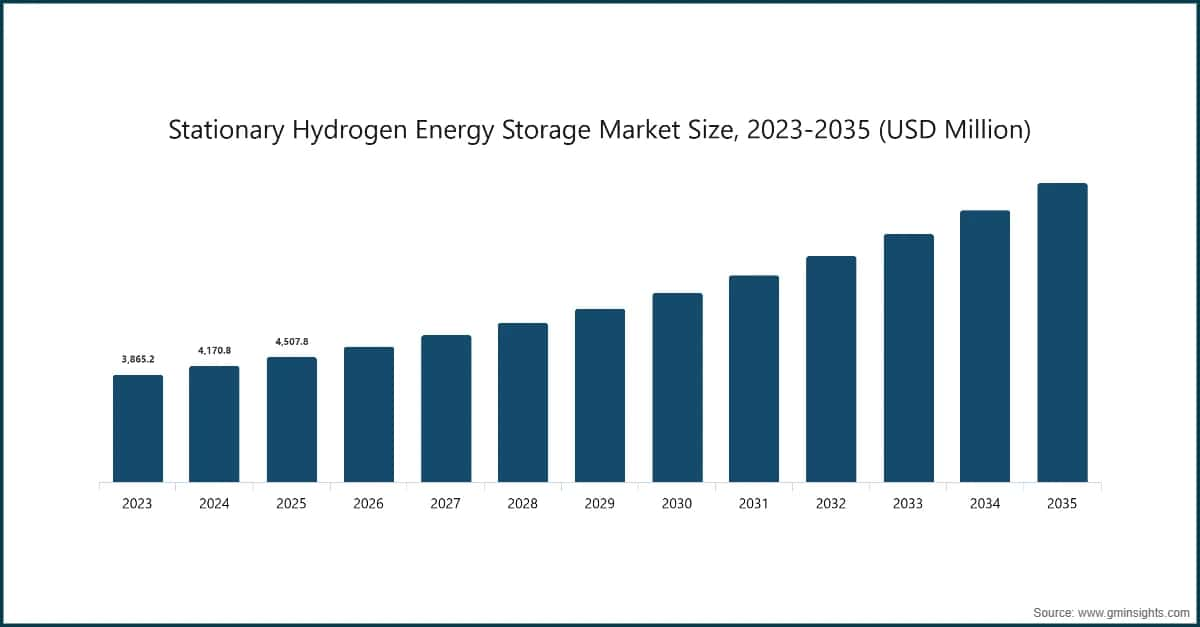

According to a recent study by Global Market Insights Inc., the stationary hydrogen energy storage market was estimated at USD 4.5 billion in 2025. The market is expected to grow from USD 4.9 billion in 2026 to USD 10.8 billion by 2035, at a CAGR of 10.2%.

Stationary Hydrogen Energy Storage Market Key Takeaways

Market Leader: Air Liquide led with over 12.5% market share in 2025.

Leading Players: Top 5 players in this market include Air Liquide, ENGIE, Cockerill Jingli, Air Products and Chemicals, Linde, which collectively held a market share of 36% in 2025.

The innovations in technology for storing, be it solid-state or liquid hydrogen, are being developed to enhance efficacy and decrease costs. Such advancements are favorable for the cost-effectiveness and performance of Hydrogen storage solutions. The shift towards decarbonization and usage of renewable sources of energy creates a need for efficient hydrogen storage systems. Hydrogen is regarded as an important factor in the integration of fluctuating renewable energy sources in order to achieve grid stability.

Considerable investment is being put into hydrogen infrastructure, be it production, storage or distribution. This is motivated by both public and private sectors’ funding which aims at increasing storage capacity for Hydrogen while reducing the investment needed for its infrastructure. In order to promote hydrogen energy, governments and regulatory agencies are coming up with policies and incentives. These include subsidies, tax exemptions, and provision for the basic acceptance of strategic aid to the development and use of hydrogen storage technologies.

The accelerating penetration of renewable energy sources such as wind and solar is a primary driver for stationary hydrogen energy storage. As renewable generation is intermittent and often mismatched with demand profiles, hydrogen offers a long-duration and seasonal energy storage solution that batteries alone cannot economically deliver. Excess renewable electricity can be converted into green hydrogen via electrolysis and stored for later use, supporting grid balancing, peak shaving, and backup power. This capability is increasingly critical as grids transition toward higher renewable shares, driving utilities and grid operators to adopt hydrogen-based storage systems to enhance reliability, flexibility, and overall system resilience.

Stationary Hydrogen Energy Storage Market Trends

Strategic partnerships are increasingly being formed between business leaders, technology providers, and research institutes, and these partnerships are promoting creativity and speeding the implementation of hydrogen storage systems. There is an increased interest in storing energy in hydrogen form primarily from the perspective of GHG emission reduction and flexible energy storage. Its contribution towards achieving net-zero emission targets is well accepted. The market is growing across the world, with notable increase in Europe, North America, and Asia Pacific. This growth is fueled by local efforts and spending towards hydrogen technology.

Government policies, decarbonization targets, and hydrogen-specific strategies are also significantly accelerating market growth. Many countries have introduced national hydrogen roadmaps, funding mechanisms, and incentives aimed at reducing emissions across power, industrial, and energy sectors. Stationary hydrogen energy storage aligns well with net-zero commitments by enabling low-carbon power generation, grid-scale energy storage, and sector coupling. Regulatory support for green hydrogen production, carbon pricing mechanisms, and subsidies for electrolyzers and fuel cells improve project economics. These supportive policy environments are encouraging utilities, independent power producers, and industrial players to invest in stationary hydrogen storage infrastructure.

Advancements in hydrogen production, storage, and conversion technologies are further driving stationary hydrogen energy storage market expansion. Improvements in electrolyzer efficiency, declining capital costs, and progress in solid-state, compressed, and liquid hydrogen storage systems are making stationary hydrogen solutions more commercially viable. In parallel, fuel cell and hydrogen turbine technologies are becoming more efficient and durable for stationary power applications. Digitalization, automation, and advanced monitoring systems are also improving operational safety and performance. These technological developments reduce system costs, increase scalability, and enhance confidence among end users considering hydrogen for long-duration and backup energy storage.

Growing demand from industrial, commercial, and utility-scale applications is another critical growth driver. Energy-intensive industries are adopting stationary hydrogen storage to ensure uninterrupted power supply and to integrate onsite renewable generation. Data centers, hospitals, ports, and remote facilities increasingly value hydrogen storage for its long-duration backup and low-emission profile compared to diesel generators. Utilities are also deploying hydrogen energy storage to defer grid upgrades, manage congestion, and support microgrids. Together, expanding application areas, grid modernization needs, and the push for energy security are strengthening long-term demand for stationary hydrogen energy storage solutions.

Stationary Hydrogen Energy Storage Market Analysis

Learn more about the key segments shaping this market

Download Free PDF

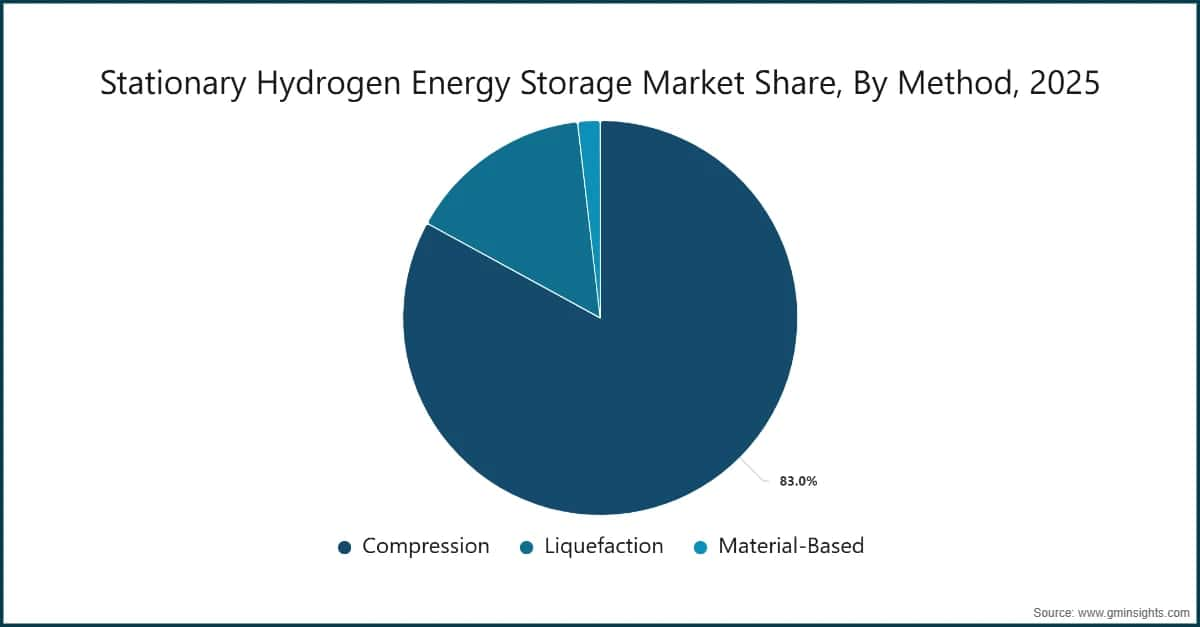

The market is classified by method into compression, liquefaction, and material-based. The compression market is expected to be valued at over USD 8.7 billion by 2035. While hydrogen has become a more popular energy carrier, the need for efficient, scalable storage solutions has risen. Hydrogen compression technology is essential to make various applications more feasible. With improved efficiency, reduced energy consumption, and increased safety, the compression segment is anticipated to rise due to technological changes in the compression systems. Innovation in engineering and materials is aiding in the production of more advanced, cost effective, and reliable compression solutions.

Compressed hydrogen storage is gaining traction due to its technological maturity, operational simplicity, and relatively lower system complexity compared to alternative methods. For stationary energy storage applications, compression-based systems are well suited for grid balancing, renewable energy integration, and backup power due to their fast response times and modular design. The availability of established standards, proven safety protocols, and widespread industry experience supports easier permitting and deployment. Additionally, declining costs of high-pressure storage tanks and advances in compression efficiency are improving project economics. Utilities and industrial users favor compressed hydrogen for short- to medium-duration storage where reliability and scalability are critical drivers.

Hydrogen liquefaction is driven by its ability to offer significantly higher energy density, making it attractive for large-scale, long-duration stationary storage applications. As renewable penetration increases, liquefied hydrogen enables centralized storage of large energy volumes to support seasonal balancing and grid stability. Growth is further supported by infrastructure synergies with emerging hydrogen supply chains, including production hubs and export terminals. Technological advancements in cryogenic systems, insulation materials, and energy recovery mechanisms are gradually improving efficiency and reducing boil-off losses. These developments are encouraging utilities and energy developers to adopt liquefaction for high-capacity storage where space constraints and long-term storage needs dominate.

Material-based hydrogen storage, including metal hydrides and advanced sorbent materials, is driven by its superior safety profile and lower operating pressures. For stationary energy storage, these systems are particularly attractive in urban, commercial, and sensitive industrial environments where safety, stability, and compact design are priorities. Ongoing research and development in novel materials is improving hydrogen absorption capacity, charge–discharge cycling, and operating temperature ranges. As material costs decline and system efficiencies improve, material-based storage is increasingly viewed as a viable option for decentralized and behind-the-meter applications. This method benefits from strong interest in long-duration, low-risk hydrogen storage solutions.

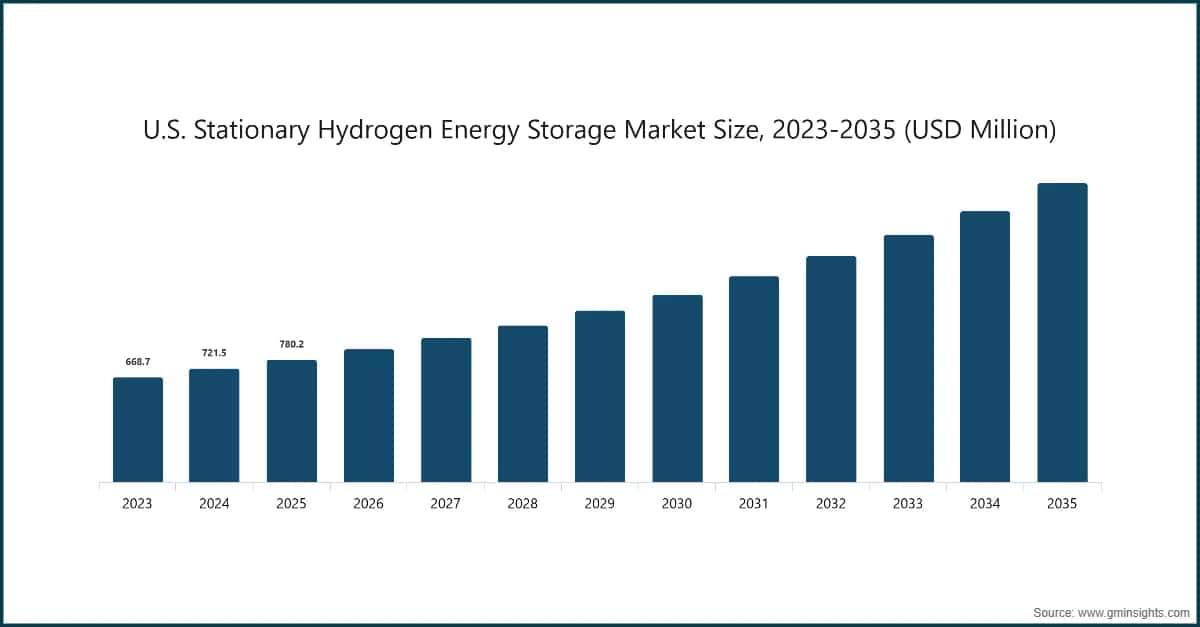

The U.S. dominated the stationary hydrogen energy storage market in North America with around 77% share in 2025 and generated USD 780.2 million in revenue. The U.S. market is driven by aggressive decarbonization goals, grid modernization efforts, and rising renewable energy penetration. Federal initiatives promoting clean hydrogen, coupled with incentives for electrolyzer deployment and long-duration energy storage, are encouraging large-scale projects. Utilities are increasingly adopting hydrogen storage to enhance grid resilience, manage renewable curtailment, and replace fossil-based peaker plants. Strong investment in hydrogen hubs, defense microgrids, and critical infrastructure backup further supports adoption. In addition, the presence of advanced technology providers, strong R&D ecosystems, and supportive state-level clean energy mandates strengthens the U.S. market’s growth momentum.

The Asia Pacific market is expected to have a market value greater than USD 4.5 billion by 2035. Currently, the Asia Pacific region is undergoing swift technological improvements in hydrogen storage including the development of advanced high-pressure compression techniques, liquefaction, and solid-state storage. The goal of these developments is to enhance the efficiency, safety, and cost-effectiveness of hydrogen storage solutions. Member countries in the Asia-Pacific region are adopting friendly policies and incentives to encourage the use of hydrogen technologies. These policies include subsidies, tax breaks, and other policies aimed at developing hydrogen economies and infrastructure storage solutions.

Europe’s growth is primarily driven by stringent climate targets, cross-border energy integration needs, and strong policy backing for green hydrogen. The region’s high renewable energy share necessitates seasonal and long-duration storage solutions, positioning hydrogen as a strategic option. European Union hydrogen strategies, funding programs, and carbon reduction regulations actively support stationary hydrogen energy storage deployment. Grid operators are leveraging hydrogen storage to stabilize power networks and support renewable-heavy systems. Additionally, Europe’s focus on energy security, particularly reducing dependency on imported fossil fuels, is accelerating investments in domestic hydrogen-based storage infrastructure across utility-scale and industrial applications.

Countries with abundant solar and wind resources are adopting stationary hydrogen storage to utilize excess renewable generation and support grid expansion. Emerging economies benefit from hydrogen storage for remote, off-grid, and weak-grid applications where long-duration storage is essential. In the Middle East, diversification away from hydrocarbons and development of clean hydrogen value chains support market growth. Overall, increasing investments in clean energy infrastructure and export-oriented hydrogen projects drive regional adoption.

12.5% Market Share

Collective Market Share of 36%

Stationary Hydrogen Energy Storage Market Share

Air Liquide has emerged as a major force in the stationary hydrogen energy storage business owing to its strong production potential, persistent investment in new technology, and agreements with leading hydrogen manufacturers. The focus of Air Liquide’s transformation has resulted in innovative hydrogen energy storage technologies that are supporting the increased requirement for clean and efficient energy technologies.

Stationary Hydrogen Energy Storage Market Companies

Stationary Hydrogen Energy Storage Industry News:

The stationary hydrogen energy storage market research report includes an in-depth coverage of the industry with estimates & forecast in terms of revenue in USD Million from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Method (USD Million)

The above information has been provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2026

Chapter 5 Market Size and Forecast, By Method, 2022 - 2035 (USD Million)

Chapter 6 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

Chapter 7 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →