Summary

Table of Content

Smart Vehicle Architecture Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Smart Vehicle Architecture Market Size

The market is projected to witness strong growth in the coming years, driven by the rapid electrification of vehicles, rising integration of advanced driver-assistance systems (ADAS), growing demand for software-defined vehicles (SDVs), and increasing connectivity requirements. Automakers and technology providers are accelerating investments in centralized and zonal electrical/electronic (E/E) architectures to support high-performance computing, over-the-air (OTA) updates, and seamless integration of autonomous and connected vehicle functions. The expansion of electric vehicle (EV) platforms, intelligent cockpit systems, and next-generation telematics infrastructure is further boosting demand for scalable and modular vehicle architecture solutions.

Smart Vehicle Architecture Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 88.7 Billion

- 2026 Market Size: USD 94.7 Billion

- 2035 Forecast Market Size: USD 227.6 Billion

- CAGR (2026–2035): 10.2%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: North America

Key Market Drivers

- Rapid Electrification of Vehicles.

- Rise of Software-Defined Vehicles.

- Growing ADAS & Autonomous Integration.

- Demand for Reduced Vehicle Complexity & Weight.

Challenges

- High Development & Integration Costs.

- Cybersecurity & Data Privacy Risks.

Opportunity

- Expansion of Centralized & Zonal Architectures.

- Integration of AI & Edge Computing.

Key Players

- Market Leader: Robert Bosch led with over 16% market share in 2025.

- Leading Players: Top 5 players in this market include Aptiv, Robert Bosch, Continental, Valeo, ZF Friedrichshafen, which collectively held a market share of 49% in 2025.

Get Market Insights & Growth Opportunities

Increasing pressure on OEMs and mobility providers to reduce vehicle complexity, optimize wiring harness weight, enhance cybersecurity, and enable faster feature deployment is driving the shift from traditional distributed architectures to domain and zonal-based architectures. Modern smart vehicle architectures enable centralized computing platforms, high-speed automotive Ethernet networks, real-time data processing, and cloud connectivity, improving system efficiency, reducing latency, and enabling continuous software upgrades throughout the vehicle lifecycle.

Technological advancements such as high-performance vehicle compute units (HPCs), automotive Ethernet (10BASE-T1S/1000BASE-T1), AI-integrated edge processors, service-oriented architecture (SOA), and middleware-based abstraction layers are transforming conventional E/E systems. For instance, in 2025, several leading OEMs accelerated the deployment of zonal architecture platforms integrating centralized compute modules to support Level 2+ and Level 3 automated driving capabilities while reducing hardware redundancy and overall system costs.

Major industry participants including Robert Bosch, Continental AG, ZF Friedrichshafen AG, Denso Corporation, and Aptiv PLC are actively strengthening their portfolios through investments in centralized vehicle controllers, zonal control units, high-speed communication gateways, cybersecurity solutions, and integrated software platforms. These companies are focusing on scalable architectures designed to support electric passenger vehicles, commercial EVs, autonomous vehicles, and next-generation mobility platforms.

The smart vehicle architecture ecosystem continues to evolve as electrification, autonomy, connectivity, and digitalization reshape automotive system design priorities. Industry participants are increasingly emphasizing modular, software-centric, and service-enabled architectures that allow faster feature rollout, enhanced vehicle intelligence, reduced wiring complexity, and lower total cost of ownership. These developments are redefining the automotive landscape, enabling improved system integration, enhanced cybersecurity, optimized energy management, and long-term value creation across passenger, commercial, and mobility service segments worldwide.

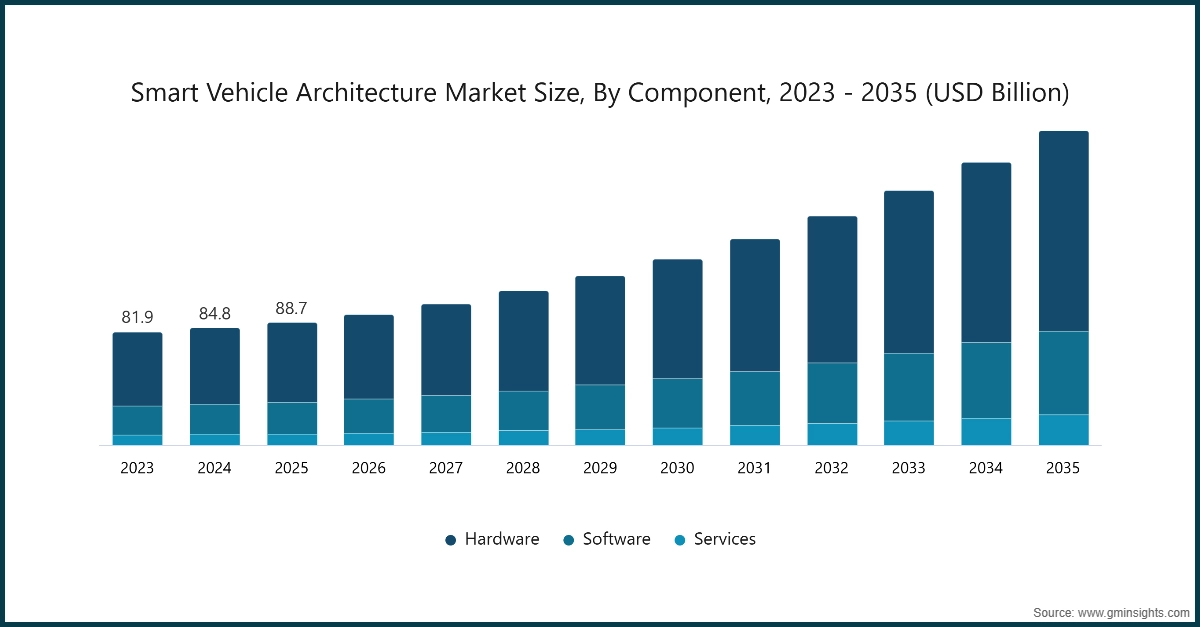

The global smart vehicle architecture market was valued at USD 88.7 billion in 2025. The market is expected to grow from USD 94.7 billion in 2026 to USD 227.6 billion in 2035, at a CAGR of 10.2%, according to latest report published by Global Market Insights Inc.

To get key market trends

Smart Vehicle Architecture Market Trends

The demand for advanced smart vehicle architecture solutions is steadily increasing, driven by growing collaboration among automotive OEMs, Tier-1 suppliers, semiconductor providers, and regulatory authorities. These partnerships aim to enhance vehicle efficiency, improve system integration, optimize data and power distribution, ensure cybersecurity, and comply with increasingly stringent safety and environmental standards across electric, hybrid, and autonomous vehicles. Stakeholders are working together to develop integrated, modular, and software-defined vehicle (SDV) architectures incorporating centralized computing platforms, zonal control units, AI-enabled vehicle management systems, high-speed automotive Ethernet networks, and real-time diagnostics for ADAS, infotainment, and powertrain subsystems.

For instance, in 2025, leading smart vehicle architecture providers strengthened strategic collaborations with global OEMs to deploy centralized compute modules, zonal control units, AI-assisted autonomous driving controllers, and high-bandwidth communication gateways for next-generation EVs and hybrid vehicles. These initiatives improved system efficiency, reduced wiring complexity, optimized energy and data flow, enhanced cybersecurity, and enabled continuous software upgrades across passenger vehicles, commercial EVs, and autonomous mobility platforms worldwide.

Regional customization of smart vehicle architectures has emerged as a key trend. Major suppliers are developing region-specific network calibrations, domain controller configurations, and software integration frameworks tailored for Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa. These solutions address local regulatory standards, connectivity requirements, vehicle platform variations, and autonomous system capabilities across premium, mid-range, and economy EV segments.

The rise of specialized software and electronics providers, along with integrated mobility solution developers, is reshaping the competitive landscape. Companies focusing on centralized and zonal computing, modular domain controllers, AI-enabled sensor fusion, and secure communication gateways are enabling scalable and cost-effective adoption of advanced vehicle architectures. These innovations empower both established OEMs and emerging EV and autonomous vehicle manufacturers to enhance vehicle performance, improve energy efficiency, optimize system integration, and accelerate deployment of next-generation mobility solutions.

The development of standardized, interoperable, and modular smart vehicle architecture platforms is transforming the market. Leading players are deploying systems that integrate seamlessly with vehicle computing, ADAS, infotainment, powertrain, and cloud-connected monitoring frameworks. These platforms support real-time data processing, predictive maintenance, multi-domain compatibility, and global safety and cybersecurity compliance, enabling OEMs to deliver safe, high-performance, energy-efficient, and future-ready vehicles for global automotive markets.

Smart Vehicle Architecture Market Analysis

Learn more about the key segments shaping this market

Based on components, the market is divided into hardware, software and services. The hardware segment dominated the market, accounting for around 65% share in 2025 and is expected to grow at a CAGR of over 10% from 2026 to 2035.

- The hardware segment dominates the smart vehicle architecture market, primarily due to its critical role in actively managing vehicle electronics, data flow, and domain integration to ensure optimal performance, safety, and scalability. With the growing adoption of centralized and zonal architectures in modern electric, hybrid, and autonomous vehicles, active components including high-performance computing units (HPCs), domain controllers, and AI-enabled vehicle management modules have become essential for real-time data processing, low-latency communication, and seamless integration of ADAS, infotainment, and powertrain systems across passenger vehicles, commercial EVs, and autonomous mobility platforms globally.

- Other components, including software and services, play complementary roles within smart vehicle architecture solutions. Software modules provide operating frameworks, middleware, cybersecurity management, and AI-driven analytics for predictive vehicle behavior, feature updates, and cross-domain coordination. Service offerings include system integration, OTA updates, diagnostics, and lifecycle support, enabling continuous optimization and adaptability of vehicle architectures. Although these segments contribute to overall market adoption, their revenue share is smaller than that of active hardware systems in high-performance and software-defined vehicle applications.

")

Learn more about the key segments shaping this market

Based on vehicles, the market is divided into passenger vehicles and commercial vehicles. The passenger vehicles segment dominates the market, accounting for around 76% share in 2025, and the segment is expected to grow at a CAGR of over 9.7% from 2026 to 2035.

- The passenger vehicles segment dominates the smart vehicle architecture market due to the high global production and adoption of electric, hybrid, and autonomous cars, SUVs, and compact EVs. Rising consumer demand for advanced connectivity, enhanced vehicle intelligence, software-defined features, and seamless integration of ADAS, infotainment, and powertrain systems has accelerated the deployment of centralized and zonal vehicle architectures, high-performance computing platforms, and AI-enabled management modules. OEM standardization of scalable, modular, and software-centric architectures across economy, mid-size, and premium passenger EVs further reinforces this segment’s market leadership across Europe, North America, and Asia Pacific.

- The commercial vehicles segment is also witnessing steady adoption of smart vehicle architecture solutions, particularly in electric buses, delivery vans, and light- and medium-duty trucks. Fleet operators increasingly prioritize system reliability, energy efficiency, reduced downtime, and enhanced connectivity to optimize operational performance and fleet management. However, the comparatively lower production volume of commercial EVs relative to passenger EVs limits the overall market share of this segment. As a result, the passenger vehicles segment continues to maintain its dominant position in the global smart vehicle architecture market.

Based on technology layer, the market is divided into ADAS, infotainment & connectivity, over-the-air (OTA) updates, cybersecurity solutions, and ai & machine learning. The ADAS segment dominated the market and was valued at USD 32 billion in 2025.

- The ADAS segment dominates the smart vehicle architecture market due to its critical role in enabling advanced driver-assistance functions, autonomous driving features, and real-time safety systems across passenger vehicles, SUVs, and commercial EVs. ADAS technologies, including adaptive cruise control, lane-keeping assist, automated emergency breaking, and sensor fusion modules, provide real-time decision-making, enhance vehicle safety, and improve overall driving experience. OEMs increasingly integrate ADAS platforms with centralized computing units, high-speed automotive Ethernet networks, and AI-enabled processing modules to ensure optimized system performance, low-latency response, and compliance with global safety standards, making this segment the primary contributor to overall market revenue.

- Other technology layers, including infotainment & connectivity, over-the-air (OTA) updates, cybersecurity solutions, and AI & machine learning, support the overall smart vehicle architecture by enabling enhanced user experience, secure data exchange, remote updates, and predictive vehicle intelligence. Although these segments contribute to market adoption across electric, hybrid, and autonomous vehicle platforms, their revenue share is smaller compared to ADAS due to the latter’s essential role in core vehicle safety, automation, and regulatory compliance.

Based on architecture, the market is divided into zonal architecture, centralized architecture, modular platforms and distributed architecture. The zonal architecture segment dominated the market and was valued at USD 42 billion in 2025.

- The zonal architecture segment dominates the smart vehicle architecture market due to its widespread adoption across electric, hybrid, and autonomous vehicles. Zonal architecture offers efficient distribution of vehicle electronics, reduced wiring complexity, simplified integration of multiple domains (such as ADAS, infotainment, and powertrain), and improved scalability for software-defined vehicles. Their ability to support high-speed automotive Ethernet networks, centralized computing units, and AI-enabled control modules make them the preferred choice for modern EV and autonomous vehicle platforms.

- Other architecture segments, including centralized architecture, modular platforms, and distributed architecture, continue to serve specific vehicle designs and applications. Centralized architectures are mainly implemented in high-performance or premium vehicles requiring a single powerful computing platform. Modular platforms offer flexibility for multi-vehicle variants but may not optimize wiring and domain integration as efficiently as zonal architectures. Distributed architectures are still relevant in legacy vehicle platforms with conventional ECU setups.

Based on propulsion, the market is divided into ICE and Electric Vehicles. The ICE segment dominated the market and was valued at USD 75 billion in 2025.

- The internal combustion engine (ICE) vehicles segment dominates the smart vehicle architecture market due to its widespread global presence across passenger cars, SUVs, and commercial vehicles, along with the complexity of integrating traditional powertrain, safety, and infotainment systems. ICE vehicles rely on extensive electronic control units (ECUs), engine management systems, and auxiliary modules to optimize performance, fuel efficiency, and emissions compliance, making robust vehicle architectures essential for seamless system integration and operational reliability.

- The electric vehicle (EV) segment continues to contribute to smart vehicle architecture adoption, particularly in regions accelerating the transition to electrification. EVs, including hybrid and fully electric platforms, require high-performance computing, centralized or zonal control units, and AI-enabled software integration for battery management, ADAS, and connectivity. While EVs are driving growing demand for next-generation architectures, the ICE segment currently maintains a dominant position due to its higher production volume and established global infrastructure.

Based on end use, the market is divided into automotive OEMs, Tier 1 & Tier 2 Suppliers, autonomous vehicle developers, fleet management companies and mobility service providers. The automotive OEMs segment dominated the market and was valued at USD 29 billion in 2025.

- The automotive OEMs segment dominates the smart vehicle architecture market due to its central role in designing, developing, and deploying advanced vehicle systems across passenger cars, SUVs, commercial vehicles, and electric platforms. OEMs are responsible for integrating centralized and zonal architectures, high-performance computing units, ADAS modules, infotainment systems, and connectivity platforms to optimize vehicle performance, safety, and user experience. Their large-scale production capabilities, global R&D investments, and standardization of software-defined vehicle platforms make this segment the primary contributor to overall market revenue.

- Other end-use segments, including Tier 1 & Tier 2 suppliers, autonomous vehicle developers, fleet management companies, and mobility service providers, continue to drive adoption by providing specialized components, integration services, and technology solutions. While these stakeholders support the deployment and scalability of smart vehicle architectures, their market share is smaller compared to automotive OEMs due to the OEMs’ direct control over vehicle design, production volume, and system-level integration.

Looking for region specific data?

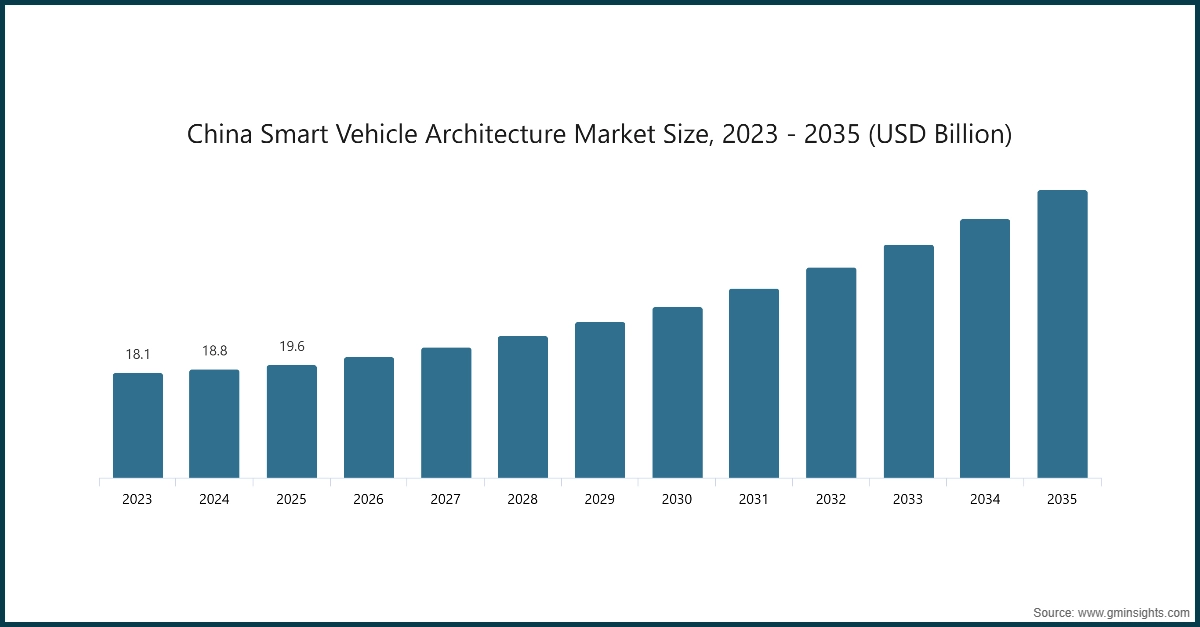

In 2025, China dominated the Asia Pacific smart vehicle architecture market with around 55% market share and generated approximately USD 19.6 billion in revenue.

- China market dominates the Asia-Pacific market due to strong electric vehicle production, rapid electrification initiatives, and the presence of leading automotive OEMs, semiconductor suppliers, and vehicle technology developers across the region. High EV penetration, expanding production of software-defined and connected vehicles, and supportive government policies significantly contribute to robust demand for advanced smart vehicle architecture solutions, including centralized and zonal computing platforms, domain controllers, high-speed automotive Ethernet networks, ADAS modules, and AI-enabled vehicle management systems across passenger EVs, commercial EVs, and autonomous mobility platforms.

- Within the region, China leads the Asia-Pacific smart vehicle architecture market, supported by its large-scale EV manufacturing ecosystem, vertically integrated automotive electronics supply chain, and strong network of Tier-1 architecture and software solution providers. Major automotive innovation hubs such as Shanghai, Beijing, Shenzhen, and Guangzhou are witnessing widespread deployment of advanced vehicle architectures, including centralized compute units, zonal control modules, AI-assisted autonomous driving platforms, and over-the-air (OTA) update frameworks.

- Other Asia-Pacific markets, including India, Japan, and South Korea, are emerging as high-growth regions driven by rising EV adoption, expansion of domestic automotive electronics manufacturing, and investment in next-generation vehicle architectures. India emphasizes cost-effective and scalable architectures for mass-market EVs and commercial fleets, Japan focuses on precision-engineered, software-defined vehicle platforms with enhanced integration of ADAS and infotainment systems, while South Korea prioritizes modular, high-performance, and AI-enabled architectures designed for premium EV segments and global export markets.

US holds share of 71% in North America smart vehicle architecture market in 2025 and it will grow tremendously between 2026 and 2035.

- North America holds a significant position in the market, supported by a well-established electric and autonomous vehicle ecosystem, advanced OEM operations, growing EV production capacity, and robust regulatory frameworks for vehicle safety, cybersecurity, and energy efficiency. The region benefits from large-scale EV and connected vehicle manufacturing, increasing adoption of software-defined and AI-enabled vehicle platforms, and investments in high-performance computing, domain controllers, and zonal architecture solutions, positioning it as a key market for technologically advanced smart vehicle architectures.

- Within the region, the United States dominates the North American smart vehicle architecture market, driven by rapid electrification initiatives, strong presence of leading OEMs and Tier-1 suppliers, and continuous advancements in vehicle electronics and AI-enabled integration. Widespread deployment of centralized compute platforms, zonal control units, ADAS modules, high-speed automotive Ethernet networks, and over-the-air (OTA) software update frameworks across passenger EVs, commercial EVs, and autonomous mobility platforms fuels market growth. Major automotive and EV hubs such as Detroit, Austin, California’s EV corridor, and Tennessee serve as key centers for innovation, software-defined vehicle development, and next-generation architecture integration.

- Leading smart vehicle architecture providers operating in the U.S., including Aptiv PLC, Robert Bosch, Continental AG, Valeo, and ZF Friedrichshafen AG, continue to expand their portfolios of centralized and zonal computing platforms, high-performance domain controllers, AI-assisted ADAS modules, cybersecurity solutions, and OTA-enabled software frameworks. Ongoing investments in modular architectures, high-speed communication networks, predictive vehicle intelligence, and enhanced system integration further consolidate the U.S.’s dominant position in the North American market.

Germany holds share of 21% in Europe smart vehicle architecture market in 2025 and it will grow tremendously between 2026 and 2035.

- Europe holds a major share of the market, supported by a highly developed electric and autonomous vehicle ecosystem, strong regulatory enforcement, and the presence of globally recognized automotive OEMs and Tier-1 suppliers. Stringent EU CO₂ emission targets, vehicle safety regulations, and sustainability mandates have accelerated EV production and advanced vehicle electronics integration across passenger and commercial vehicles. Manufacturers across the region prioritize energy-efficient architectures, seamless software integration, modular and zonal E/E systems, and over-the-air (OTA) update capabilities. Well-established R&D infrastructure, standardized manufacturing regulations, and growing investments in connected and autonomous vehicle platforms reinforce Europe’s position as a key regional market.

- Germany dominates the European smart vehicle architecture market, driven by its strong automotive industry, concentration of premium OEMs, advanced engineering expertise, and strict regulatory compliance culture. German manufacturers and suppliers lead in the deployment of centralized and zonal computing platforms, high-performance domain controllers, AI-assisted ADAS modules, high-speed automotive Ethernet networks, and cybersecurity-enabled software frameworks. Continuous investments in modular architecture, scalable software-defined vehicle platforms, predictive vehicle intelligence, and integrated connectivity solutions strengthen system performance, improve energy efficiency, and optimize vehicle functionality.

- Other major European countries, including the United Kingdom, France, and the Netherlands, contribute significantly to regional market expansion. The UK emphasizes modular vehicle platform integration and connected mobility solutions, France focuses on emission compliance and integration of advanced ADAS and infotainment systems, while the Netherlands prioritizes sustainable mobility initiatives and high-speed connected vehicle infrastructure. Despite expanding adoption across these countries, Germany maintains its leading role in scale, technological innovation, high-precision engineering, and comprehensive deployment of advanced smart vehicle architecture solutions across Europe.

Smart vehicle architecture market in Brazil will experience significant growth between 2026 and 2035.

- Latin America holds a smaller but steadily growing share of the market, driven by increasing production of passenger EVs, electric SUVs, and hybrid vehicles, rising adoption of connected and software-defined vehicle platforms, and gradual deployment of standardized centralized and zonal architectures. OEMs, Tier-1 suppliers, and mobility service providers across the region are implementing modular, AI-enabled vehicle computing systems, high-speed automotive Ethernet networks, domain controllers, and over-the-air (OTA) update frameworks to ensure optimized system integration, enhanced safety, and compliance with regional regulatory standards.

- Brazil dominates the Latin American smart vehicle architecture market, supported by its large automotive and EV manufacturing industry, growing domestic electronics and semiconductor production, and increasing deployment of advanced vehicle architecture solutions. Major automotive and industrial hubs such as São Paulo, Rio de Janeiro, and Belo Horizonte host extensive OEM operations and supplier networks, where manufacturers deploy centralized and zonal computing platforms, ADAS modules, AI-enabled vehicle management systems, and cybersecurity-integrated software frameworks. Leading smart vehicle architecture providers, including Aptiv PLC, Robert Bosch GmbH, Continental AG, Valeo, and ZF Friedrichshafen AG, actively offer integrated hardware, software, and service solutions, maintaining Brazil’s dominant position in the regional market.

- Mexico represents the second largest and rapidly growing market in Latin America, driven by rising EV adoption, expansion of domestic supplier networks, and increasing integration of centralized computing and zonal architecture solutions in passenger cars, SUVs, and light commercial electric vehicles. Key industrial centers such as Mexico City, Monterrey, and Guadalajara are witnessing higher deployment of high-performance domain controllers, AI-assisted ADAS modules, OTA-enabled software platforms, and connected vehicle management systems, contributing to the overall modernization of Latin America’s smart vehicle architecture ecosystem, while Brazil continues to lead the regional market.

Smart vehicle architecture market in UAE will experience significant growth between 2026 and 2035.

- Middle East & Africa (MEA) holds a smaller but gradually expanding share of the market, driven by growing production and adoption of passenger EVs, electric SUVs, and hybrid vehicles, increasing integration of centralized and zonal computing platforms, and rising investment in modular, AI-enabled vehicle management systems. OEMs, fleet operators, and mobility service providers across the region are increasingly implementing standardized system integration, software update protocols, and predictive diagnostics to ensure optimized vehicle performance, enhanced connectivity, and regulatory compliance.

- The UAE dominates the MEA smart vehicle architecture market, supported by its rapidly developing EV and connected vehicle sector, strong OEM and Tier-1 supplier networks, and early adoption of predictive, modular, and high-performance vehicle architecture solutions. Major automotive and industrial hubs such as Dubai, Abu Dhabi, and Sharjah host extensive OEM operations and supplier facilities, where vehicle architecture programs include centralized computing units, zonal domain controllers, AI-enabled ADAS modules, high-speed automotive Ethernet networks, and over-the-air (OTA) software update frameworks.

- Other MEA countries, including Saudi Arabia, South Africa, and Egypt, are emerging as high-growth markets, driven by increasing EV adoption, expansion of domestic supplier networks, and deployment of advanced centralized and zonal architectures across passenger vehicles, SUVs, and hybrid platforms. Saudi Arabia emphasizes fleet and commercial EV applications, South Africa focuses on passenger and light commercial EVs, while Egypt prioritizes modular, high-performance, and AI-assisted vehicle architectures. Despite growth in these markets, the UAE continues to maintain its leading role in MEA due to technological innovation, large-scale system integration capabilities, and strong government and enterprise support.

Smart Vehicle Architecture Market Share

The top 7 companies in the market are Bosch, Valeo, ZF Friedrichshafen, Aptiv, Continental AG, Infineon Technologies and Qualcomm. These companies hold around 55% of the market share in 2025.

- Robert Bosch is a leading provider of smart vehicle architecture solutions, offering centralized and zonal computing platforms, high-performance domain controllers, ADAS modules, high-speed automotive Ethernet networks, and AI-enabled vehicle management systems for passenger EVs, commercial EVs, and autonomous mobility platforms. Bosch leverages advanced electronics integration, modular architecture designs, and global OEM collaborations to deliver high-performance, reliable, and scalable vehicle architecture solutions.

- Valeo delivers advanced smart vehicle architecture solutions, including modular domain controllers, sensor fusion hubs, centralized compute units, and AI-assisted ADAS and infotainment platforms. Valeo emphasizes energy-efficient system integration, lightweight architectures, and interoperability across multiple vehicle domains to optimize performance, connectivity, and safety. Its global R&D footprint and multi-OEM collaborations reinforce its strong presence in the smart vehicle architecture market.

- ZF Friedrichshafen AG provides high-performance vehicle architecture platforms, including centralized and zonal computing systems, autonomous driving controllers, secure vehicle networking solutions, and software-defined domain integration for passenger cars, commercial EVs, and autonomous vehicles. ZF leverages expertise in intelligent mobility systems, powertrain integration, and modular software architectures to deliver optimized vehicle performance, low-latency communication, and scalable deployment, strengthening its market share.

- Aptiv PLC offers comprehensive smart vehicle architecture solutions, including centralized compute units, zonal gateways, high-speed Ethernet networks, software-defined vehicle platforms, and AI-enabled vehicle management systems. Aptiv’s focus on advanced driver-assistance systems (ADAS), autonomous driving integration, and cybersecurity frameworks ensure seamless data processing, feature scalability, and system reliability across global OEM platforms, consolidating its competitive position in the market.

- Continental AG provides integrated vehicle architecture solutions, including high-performance computing platforms, domain controllers, body and motion control modules, AI-enabled ADAS integration, and over-the-air (OTA) software frameworks. Continental leverages electronics integration expertise, scalable modular designs, and global OEM collaborations to enhance system efficiency, connectivity, and safety, strengthening its market presence.

- Infineon Technologies specializes in semiconductor-based smart vehicle architecture solutions, including automotive-grade microcontrollers, power electronics, sensor interfaces, and AI-assisted control modules for centralized and zonal architectures. Infineon leverages expertise in high-performance computing, energy-efficient electronics, and secure vehicle integration to support optimized system performance across passenger EVs, commercial vehicles, and autonomous platforms, enhancing its market competitiveness.

- Qualcomm Technologies delivers advanced smart vehicle computing solutions, including automotive SoCs, AI-enabled ADAS platforms, centralized compute modules, and secure connectivity solutions for software-defined and autonomous vehicles. Qualcomm leverages expertise in high-performance processors, AI acceleration, and cloud-connected vehicle architectures to enable real-time data processing, OTA updates, and scalable deployment, reinforcing its strategic position in the market.

Smart Vehicle Architecture Market Companies

Major players operating in the smart vehicle architecture industry include:

- Aptiv PLC

- Continental AG

- Delphi Technologies

- Harman International

- Infineon Technologies

- Mahle

- Qualcomm Technologies

- Robert Bosch

- Valeo

- ZF Friedrichshafen AG

- The smart vehicle architecture market is highly competitive, with leading solution providers such as Robert Bosch, Continental AG, Denso, Valeo, Infineon Technologies, MAHLE, Hanon Systems, Dana, BorgWarner, and Hitachi Astemo occupying key segments across centralized and zonal computing platforms, high-performance domain controllers, ADAS modules, high-speed vehicle networks, AI-enabled vehicle management systems, and over-the-air (OTA) software frameworks.

- Robert Bosch, Continental AG, Denso, Valeo, Infineon Technologies, MAHLE, and Hanon Systems lead the market with comprehensive smart vehicle architecture solutions, integrating modular computing platforms, sensor fusion modules, AI-assisted ADAS, cybersecurity frameworks, and OTA-enabled software systems. These companies focus on enhancing vehicle safety, system efficiency, real-time connectivity, and scalable integration while maintaining strong OEM collaborations, global engineering capabilities, and service networks.

- Dana, BorgWarner, and Hitachi Astemo specialize in advanced, technology-driven vehicle architecture solutions, emphasizing modular system designs, high-performance computing platforms, predictive AI-based vehicle intelligence, and software-defined vehicle integration. Their products enable optimized data processing, enhanced connectivity, low-latency communication, and seamless integration across passenger EVs, commercial electric vehicles, and autonomous mobility platforms worldwide.

Smart Vehicle Architecture Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 88.7 Billion |

| Market Size in 2026 | USD 94.7 Billion |

| Forecast Period 2026-2035 CAGR | 10.2% |

| Market Size in 2035 | USD 227.6 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Rapid Electrification of Vehicles | The global shift toward electric vehicles (EVs) requires advanced E/E architecture capable of managing high-voltage systems, battery management, power electronics, and energy optimization through centralized platforms. |

| Rise of Software-Defined Vehicles | Automakers are transitioning to software-centric platforms that enable over-the-air (OTA) updates, feature-on-demand services, and continuous performance enhancements driving demand for centralized and zonal architectures. |

| Growing ADAS & Autonomous Integration | Increasing deployment of Level 2+ and Level 3 automation features requires high-performance computing (HPC), real-time sensor fusion, and low-latency communication networks, supported by next-gen vehicle architectures. |

| Demand for Reduced Vehicle Complexity & Weight | Zonal and centralized architectures significantly reduce wiring harness length, lower vehicle weight, and improve manufacturing efficiency supporting cost optimization and energy efficiency goals. |

| Pitfalls & Challenges | Impact |

| High Development & Integration Costs | Transitioning from distributed to centralized/zonal architecture demands substantial R&D investments, new semiconductor platforms, software integration frameworks, and redesign of legacy systems. |

| Cybersecurity & Data Privacy Risks | As vehicles become more connected and software-driven, vulnerabilities increase. Ensuring end-to-end cybersecurity protection across vehicle networks, cloud interfaces, and OTA systems remain a critical challenge. |

| Opportunities: | Impact |

| Expansion of Centralized & Zonal Architectures | The growing adoption of high-performance compute units and automotive Ethernet creates opportunities for scalable, modular architecture platforms across EVs, commercial vehicles, and autonomous fleets. |

| Integration of AI & Edge Computing | AI-enabled edge processors and real-time analytics offer opportunities to optimize energy management, predictive maintenance, autonomous driving functions, and in-vehicle personalization unlocking new revenue streams through software services. |

| Market Leaders (2025) | |

| Market Leader |

16% market share |

| Top Players |

Collective market share in 2025 is 49% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest growing market | North America |

| Emerging countries | Brazil, Mexico, UAE |

| Future outlook |

|

What are the growth opportunities in this market?

Smart Vehicle Architecture Industry News

- In March 2025, Robert Bosch launched an advanced smart vehicle architecture platform featuring centralized and zonal computing units, high-performance domain controllers, ADAS modules, and AI-enabled vehicle management systems. The initiative aims to enhance system integration, real-time connectivity, cybersecurity, and global deployment across passenger EVs, electric SUVs, and commercial electric vehicles.

- In February 2025, Denso expanded its smart vehicle architecture portfolio, introducing modular domain controllers, sensor-integrated ADAS modules, high-speed automotive Ethernet platforms, and OTA-enabled software frameworks. The rollout focuses on improving vehicle safety, system efficiency, and adoption across OEMs and fleet operators worldwide.

- In January 2025, BorgWarner upgraded its vehicle architecture offerings with centralized compute platforms, hybrid-compatible zonal controllers, and AI-assisted management systems for passenger and commercial electric vehicles. The initiative targets large-scale OEM integration, optimized system performance, and enhanced operational reliability.

- In December 2024, Valeo introduced an advanced smart vehicle architecture platform combining high-performance centralized computing, domain controllers, predictive AI-based ADAS integration, and over-the-air (OTA) software frameworks. The deployment aims to improve system safety, reduce latency, and support passenger EV, electric SUV, and commercial vehicle platforms globally.

- In October 2024, MAHLE, Hanon Systems, and Dana launched integrated vehicle architecture solutions for passenger EVs, electric SUVs, and light commercial vehicles, combining modular computing units, AI-enabled ADAS platforms, zonal controllers, and OTA update capabilities. The initiative emphasizes optimized system performance, enhanced connectivity, operational reliability, and seamless OEM integration across global markets.

The smart vehicle architecture market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Bn) from 2022 to 2035, for the following segments:

Market, By Component

- Hardware

- Centralized computing units

- Adas modules

- Vehicle communication interfaces

- Power distribution units (PDUS)

- Smart sensors & actuators

- Software

- Embedded vehicle software

- Cloud-based vehicle software

- Cybersecurity solutions

- Over-the-air (OTA) update systems

- Vehicle operating systems

- Services

- Vehicle diagnostics & maintenance services

- Connected vehicle data services

- Software-as-a-service (SAAS) for automotive

- Remote monitoring & fleet management services

- Integration & customization services

Market, By Vehicle

- Passenger vehicles

- Hatchbacks

- Sedans

- SUV

- Commercial vehicles

- Light commercial vehicles (LCV)

- Medium commercial vehicles (MCV)

- Heavy commercial vehicles (HCV)

Market, By Architecture

- Centralized Architectures

- Domain Controllers

- Central Computing Platforms

- Zonal Architectures

- Zone Controllers

- Gateway Modules

- Modular Platforms

- Scalable Hardware Platforms

- Software-Defined Modules

- Distributed Architectures

- Traditional ECU Networks

- Point-to-Point Communication Systems

Market, By Technology Layer

- ADAS

- Infotainment & Connectivity

- Over-the-Air (OTA) Updates

- Cybersecurity Solutions

- AI & Machine Learning

Market, By Propulsion

- ICE

- Gasoline

- Diesel

- Hybrid

- EV (Electric Vehicles)

- BEV (Battery Electric Vehicle)

- PHEV (Plug-in Hybrid Electric Vehicle)

- FCEV (Fuel Cell Electric Vehicle) ADAS

Market, By End-Use

- Automotive OEMs

- Tier 1 & Tier 2 Suppliers

- Autonomous vehicle developers

- Fleet management companies

- Mobility service providers

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Belgium

- Netherlands

- Sweden

- Asia Pacific

- China

- India

- Japan

- Australia

- Singapore

- South Korea

- Vietnam

- Indonesia

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

What is the market size of the smart vehicle architecture in 2025?

The market size was valued at USD 88.7 billion in 2025, at a CAGR of 10.2% till 2035. The market is driven by the rapid electrification of vehicles, increasing adoption of advanced driver-assistance systems (ADAS), and growing demand for software-defined vehicles (SDVs).

What is the projected value of the smart vehicle architecture market by 2035?

The market is poised to reach USD 227.6 billion by 2035, supported by advancements in centralized and zonal electrical/electronic (E/E) architectures, high-performance computing, and next-generation telematics infrastructure.

What is the expected size of the smart vehicle architecture industry in 2026?

The market size is projected to grow to USD 94.7 billion in 2026.

How much revenue did the hardware segment generate in 2025?

The hardware segment accounted for approximately 65% of the market share in 2025 and is projected to grow at a CAGR of over 10% up to 2035.

What was the valuation of the ADAS segment in 2025?

The ADAS segment was valued at USD 32 billion in 2025, led by its critical role in enabling advanced driver-assistance functions, autonomous driving features, and real-time safety systems.

What is the growth outlook for the passenger vehicles segment from 2026 to 2035?

The passenger vehicles segment is set to expand at a CAGR of over 9.7% through 2035.

Which region leads the smart vehicle architecture sector?

China led the Asia Pacific market in 2025, accounting for approximately 55% of the regional market share and generating around USD 19.6 billion in revenue.

What are the upcoming trends in the smart vehicle architecture market?

Key trends include centralized and zonal computing platforms, AI-enabled vehicle management systems, high-speed automotive Ethernet networks, real-time diagnostics, and region-specific vehicle architecture customization.

Who are the key players in the smart vehicle architecture industry?

Major players include Aptiv PLC, Continental AG, Delphi Technologies, Harman International, Infineon Technologies, Mahle, Qualcomm Technologies, Robert Bosch, Valeo, and ZF Friedrichshafen AG.

Smart Vehicle Architecture Market Scope

Related Reports