Authors:

Preeti Wadhwani, Satyam Jaiswal

Download free PDF

Small Cell Network Market Size & Share 2026-2035

Report ID: GMI13216

|

Published Date: April 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Small Cell Network Market

Get a free sample of this report

Get a free sample of this report Small Cell Network Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Small Cell Network Market Size

The global small cell network market was valued at USD 3.1 billion in 2025. The market is expected to grow from USD 3.9 billion in 2026 to USD 64.6 billion in 2035 at a CAGR of 36.6%, according to latest report published by Global Market Insights Inc.

Small Cell Network Market Key Takeaways

Market Leader: Ericsson led with over 19% market share in 2025.

Leading Players: Top 5 players in this market include Ericsson, Huawei, Nokia, Samsung, ZTE, which collectively held a market share of 66% in 2025.

The rapid deployment of 5G networks resulted in an increased number of small cell deployments to meet the demand for high-speed mobile connectivity in urban areas and indoor locations. Mobile carriers are investing in small cells to meet these performance demands. In February 2025, Ericsson made announcement of expanding its 5G small cell portfolio to include more Radio Dot System (RDS) installations throughout Europe to help support the growth of additional densification and capacity for indoor applications.

The explosive growth of mobile data consumption from video streaming, gaming, and cloud services has resulted in additional deployments of small cells to reduce congestion and improve operational efficiency. In January 2026, Verizon expanded its 5G Ultra-Wideband small cell coverage to more markets in the United States due to rapidly-growing data traffic.

As the Internet of Things (IoT) continues to expand across industries such as manufacturing, logistics, and smart cities the demand for small cells that provide reliable and dense connectivity will increase. In March 2025, Huawei implemented its 5G LampSite solution inside a smart factory in China to enable mass IoT connectivity and real-time monitoring.

Ultra-low-latency applications such as autonomous systems, augmented and virtual reality and real-time analytics are deploying small cells alongside edge compute resources. In April 2026, Nokia, launched next-generation AirScale small cell solutions with edge computing capabilities, which allow for ultra-low latency for enterprise applications.

Small Cell Network Market Trends

As the telecom industry shifts from traditional RAN deployments toward Open RAN and cloud-based solutions, operators are moving away from single-vendor dependencies and towards more flexible and cost-effective network deployment strategies. Operators are also adopting disaggregated RAN models to lower their costs and speed up the rollout of small cells (5G) in urban areas and business districts.

AI and machine learning are integral parts of small cell solutions to provide automation for traffic management, self-healing, and predictive maintenance. These technologies will also improve network efficiency, reduce operational expenditures, and enhance the quality of real-time services delivered to end users in densely populated urban areas.

Integration of small cells with edge computing infrastructures provide ultra-low latency processing closer to the end user. This enables real-time applications that require ultra-low latency, such as autonomous systems augmented and virtual reality (AR/VR) and industrial automation, while also reducing backhaul congestion and improving overall performance.

Private 5G networks are deployed at a rapid pace using small cells to provide secure, high-performance connectivity for enterprise businesses. The manufacturing, logistics and smart campus verticals are leading the way in the deployment of private 5G networks where deterministic and reliable connectivity will be required for the continued automation and expansion of the Internet of Things (IoT).

Small Cell Network Market Analysis

Based on component, the small cell network market is divided into solution and services. Solution dominated the market, accounting for 67% in 2025 and are expected to grow at a CAGR of 36% through 2026 to 2035.

Telecom vendors and systems integrators are beginning to offer integrated, end-to-end support for the planning, site acquisition, installation, backhaul integration, and optimization of small cell networks. The growth of this industry has resulted in operators deploying small cells more quickly while mitigating the risk of deployment failures improving the overall speed and performance of their networks for both end users and enterprises.

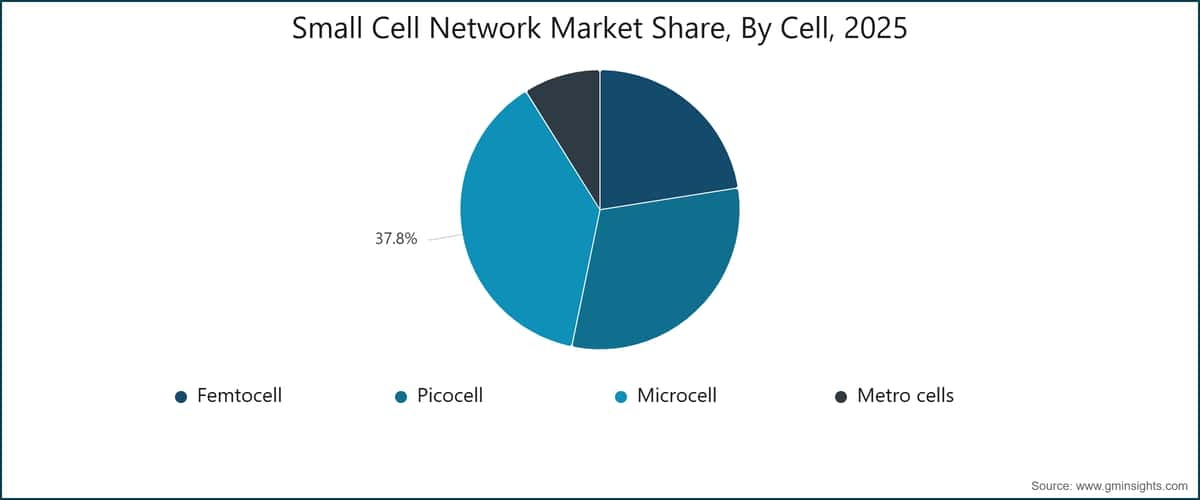

Based on cell, the small cell network market is segmented into femtocell, picocell, microcell and metro cells. Microcell segment dominates the market with 37.8% share in 2025, and the segment is expected to grow at a CAGR of 36.9% from 2026 to 2035.

Based on deployment mode, the small cell network market is segmented into indoor and outdoor. Indoor segments dominate the market with 64% share in 2025, and the segment is expected to grow at a CAGR of 35.8% from 2026 to 2035.

Based on organization size, the small cell network market is segmented into SME and large organization. Large organization segment is expected to dominate the market with a share of 64% in 2025.

U.S. small cell network market reached USD 723.9 million in 2025, growing from USD 571.9 million in 2024.

North America dominated the small cell network market with a market size of USD 877 million in 2025.

Europe small cell network market accounted for a share of 21.2% and generated revenue of USD 651.3 million in 2025.

Germany dominates the small cell network market, showcasing strong growth potential, with a CAGR of 37.6% from 2026 to 2035.

The Asia Pacific small cell network market is anticipated to grow at the highest CAGR of 38.1% from 2026 to 2035 and generated revenue of USD 1.2 billion in 2025.

China small cell network market is estimated to grow with a CAGR of 39.3% from 2026 to 2035.

Latin America small cell network market shows lucrative growth over the forecast period.

Brazil small cell network market is estimated to grow with a CAGR of 34.5% from 2026 to 2035 and reach USD 1.4 billion in 2035.

Middle East and Africa small cell network market accounted for USD 161.2 million in 2025 and is anticipated to show lucrative growth over the forecast period.

UAE market is expected to experience substantial growth in the Middle East and Africa small cell network market, with a CAGR of 26.3% from 2026 to 2035.

Small Cell Network Market Share

Small Cell Network Market Companies

Major players operating in the small cell network industry are:

Airspan Networks

19% market share

Collective market share in 2025 is 66%

Small Cell Network Industry News

The small cell network market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) and shipments (million units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Component

Market, By Cell

Market, By Technology

Market, By Deployment mode

Market, By End Use

Market, By Organization size

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

Chapter 6 Market Estimates & Forecast, By Cell, 2022 - 2035 ($Mn, Mn Units)

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Mn)

Chapter 8 Market Estimates & Forecast, By Deployment mode, 2022 - 2035 ($Mn, Mn Units)

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn)

Chapter 10 Market Estimates & Forecast, By Organization size, 2022 - 2035 ($Mn)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Mn Units)

Chapter 12 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →