Rock Breaker Market Size & Share 2026-2035

Market Size – By Type (Hydraulic, Pneumatic, Others), By Product (Premium, Non-premium), By Equipment Size (Light Duty (Up to 500 Kg), Medium Duty (501–1200 Kg), Heavy Duty (Above 1200 Kg)), By Application (Quarrying, Demolition, Tunneling, Scaling, Others), By End Use (Construction, Mining, Government, Private), Growth Forecast.

Report ID: GMI11930

|

Published Date: April 2026

|

Report Format: PDF

Download Free PDF

Authors: Preeti Wadhwani, Aishvarya Ambekar

Rock Breaker Market Size

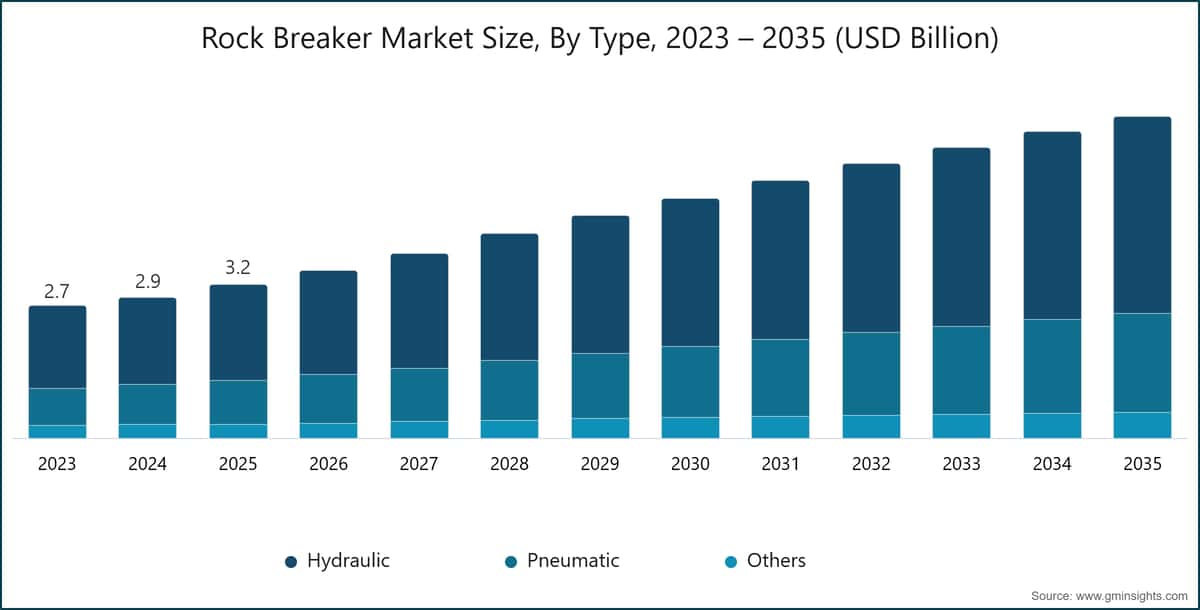

The global rock breaker market was estimated at USD 3.2 billion in 2025. The market is expected to grow from USD 3.5 billion in 2026 to USD 6.7 billion in 2035, at a CAGR of 7.5%, according to latest report published by Global Market Insights Inc.

Rock Breaker Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

The rock breaker market volume was estimated at 80,200 units in 2025. The market is projected to grow from 86,800 units in 2026 to 1,31,754 units by 2035, registering strong double-digit growth over the forecast period.

The rapid expansion of mining, quarrying, and infrastructure development activities is significantly transforming the rock breaker market. Traditionally used for basic demolition and secondary rock breaking, rock breakers are now becoming essential for high-efficiency material fragmentation across modern construction and mining operations. With increasing project scale and complexity, these machines play a critical role in improving productivity, reducing manual intervention, and ensuring operational safety, thereby directly influencing project timelines, cost efficiency, and worker protection.

Rising demand for faster and more precise excavation in urban construction and large-scale mining projects is further strengthening the importance of advanced rock breaking solutions. Applications such as road construction, tunneling, trenching, and demolition are driving the adoption of high-performance hydraulic breakers equipped with enhanced impact energy and durability. At the same time, manufacturers are focusing on lightweight yet robust materials and improved design structures to enhance equipment efficiency while minimizing wear and maintenance requirements.

For instance, in February 2025, Sandvik announced the launch of a new generation of intelligent hydraulic breakers equipped with real-time monitoring capabilities and automated performance adjustment, aimed at improving productivity and reducing downtime in mining and construction operations.

The increasing focus on infrastructure development, particularly in emerging economies, along with the expansion of mining activities, is accelerating the demand for technologically advanced rock breakers. Governments are investing heavily in transportation networks, smart cities, and energy projects, which require efficient rock excavation and material handling solutions. As a result, construction and mining companies are shifting toward high-capacity and versatile rock breakers capable of operating across diverse environments and material conditions.

Innovation in design and technology is reshaping the competitive landscape of the market. Advanced features such as noise and vibration reduction systems, energy recovery mechanisms, and automated lubrication systems are gaining widespread adoption. In addition, manufacturers are integrating telematics and IoT-enabled monitoring systems that provide real-time data on equipment performance, usage patterns, and maintenance needs, helping operators optimize productivity and reduce operational costs.

Electrification and sustainability trends are also influencing rock breaker development. While hydraulic breakers continue to dominate, there is growing interest in electrically powered and hybrid-compatible systems, especially for urban construction projects where emissions and noise regulations are stringent. Manufacturers are increasingly focusing on energy-efficient designs and environmentally friendly manufacturing processes to align with global sustainability goals.

Application-specific customization is becoming a key trend across different end-use sectors. In mining, rock breakers are designed to handle high-impact and continuous operations in harsh environments, often integrated with stationary boom systems for primary breaking. In construction and demolition, compact and versatile breakers are preferred for precision work in confined urban spaces. Additionally, the growing use of rock breakers in recycling applications, such as concrete and asphalt processing, is expanding their market scope.

North America and Europe represent mature and high-value markets for rock breakers, driven by established construction industries, stringent safety regulations, and the adoption of advanced equipment technologies. The presence of major OEMs and increasing renovation and infrastructure upgrade projects further support demand for high-performance and low-noise rock breaking solutions.

Asia-Pacific is the fastest-growing rock breaker market due to rapid urbanization, large-scale infrastructure investments, and expanding mining activities. China dominates the regional market with extensive construction and mining operations, while India, Japan, and South Korea are witnessing rising demand driven by government infrastructure initiatives and industrial growth. Increasing adoption of cost-effective, durable, and high-efficiency rock breakers is supporting strong market expansion across the region.

Rock Breaker Market Trends

The rock breaker market is increasingly adopting smart and connected technologies to enhance operational efficiency and reduce downtime. Modern breakers are equipped with IoT sensors and telematics systems that monitor parameters such as impact frequency, temperature, and wear levels in real time. This data enables predictive maintenance, preventing unexpected failures and extending equipment lifespan. Integration with fleet management systems also allows operators to optimize utilization and improve productivity, especially in large-scale mining and infrastructure projects where continuous performance is essential.

Hydraulic rock breakers dominate the market due to their superior power, efficiency, and adaptability across various applications. Manufacturers are focusing on improving energy transfer mechanisms to maximize impact force while minimizing energy loss. Enhanced designs also reduce vibration and noise, improving operator comfort and equipment longevity. These advancements result in faster material breaking, lower fuel consumption, and reduced operational costs. Their ability to handle diverse materials and harsh environments makes them a preferred choice in construction, demolition, and mining industries.

For example, in January 2025, Sandvik AB launched an advanced digital rock breaker system integrated with IoT-enabled sensors and telematics, allowing real-time monitoring of performance metrics such as impact energy and component wear, enabling predictive maintenance and reducing unplanned downtime in mining operations.

Increasing urbanization and stringent environmental regulations are driving the demand for quieter and less disruptive rock breaking solutions. Manufacturers are developing advanced enclosure designs, shock absorption systems, and optimized impact technologies to reduce noise and vibration levels. This is particularly important for construction activities in densely populated areas where regulatory compliance is critical. Lower vibration also reduces operator fatigue and minimizes structural damage to surrounding areas, making these solutions more sustainable and suitable for sensitive infrastructure projects.

Automation is becoming a key trend in the rock breaker market, especially in mining and large-scale construction operations. Modern systems are being equipped with remote-control and semi-autonomous capabilities, allowing operators to control equipment from a safe distance. This reduces exposure to hazardous environments such as unstable rock formations and underground sites. Automation also improves precision and consistency in operations, leading to higher productivity. Additionally, it helps address labor shortages and enhances overall safety and efficiency in demanding working conditions.

The rapid growth of infrastructure and mining activities in emerging economies is significantly boosting demand for rock breakers. Governments are investing heavily in transportation networks, energy projects, and urban development, all of which require efficient rock excavation. Simultaneously, increasing demand for minerals and raw materials is driving mining operations. Countries in Asia-Pacific, Latin America, and the Middle East are witnessing strong adoption of cost-effective and durable equipment, supporting market expansion and creating new growth opportunities for manufacturers and suppliers.

Rock Breaker Market Analysis

Learn more about the key segments shaping this market

Download Free PDF

Based on type, the market is divided into hydraulic, pneumatic, and others. The Hydraulic segment dominated the market, accounting for around 62.3% in 2025 and is expected to grow at a CAGR of more than 7.3% through 2035.

Based on product, the market is categorized into premium, and non-premium. The premium segment dominates the market accounting for around 64.1% share in 2025, and the segment is expected to grow at a CAGR of over 8% from 2026-2035.

Based on equipment size, the global rock breaker market is divided into light duty (up to 500 kg), medium duty (501-1200 kg), and heavy duty (above 1200 kg). The medium duty (501-1200 Kg) segment held the major market share in 2025.

Based on application, the market is divided into quarrying, demolition, tunneling, scaling, and others. The radiators segment dominated the rock breaker market.

China dominated the rock breaker market in Asia Pacific with around 64.2% share and generated USD 817.5 million in revenue in 2025.

The rock breaker market in Germany is expected to experience significant and promising growth from 2026 to 2035.

The rock breaker market in U.S. is expected to experience significant and promising growth from 2026-2035.

The rock breaker market in Brazil is expected to experience significant and promising growth from 2026 to 2035.

The rock breaker market in UAE is expected to experience significant and promising growth from 2026-2035.

Rock Breaker Market Share

Rock Breaker Market Companies

Major players operating in the rock breaker industry are:

8.8% market share

Collective Market Share in 2025 is 39.2%

Rock Breaker Industry News

The rock breaker market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($Bn), and shipment (Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Type

Market, By Product

Market, By Equipment Size

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries: