Summary

Table of Content

Personal 3D Printers Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Personal 3D Printers Market Size

The global personal 3D printer market was valued at USD 5.99 billion in 2024 with a volume of 13,300 thousand units and is projected to reach USD 6.17 billion by 2025 and USD 10.47 billion with a volume of 20,146 thousand units by 2034 growing at a value CAGR of 6% during the forecast period 2025–2034, according to Global Market Insights Inc.

To get key market trends

- The increasing affordability of desktop 3D printer models represents a significant driving force for the personal 3D printer market. Over the past few years, declining costs due to technological advancements and competitive production made good-quality printers affordable to more consumers like hobbyists, educators, and small businesses. Reductions in price removed a significant adoption barrier, enabling more individuals to experiment with 3D printing at relatively low capital investment. Besides, economical models today are also fitted with features such as improved resolution, multi-material capability, and easy-to-use interfaces that allow users to generate high-quality results.

- The growing popularity of DIY and maker culture are driving personal 3D printer adoption. Enthusiast, educational, and small business communities are finding 3D printing increasingly used to prototype, customize, and produce unique items. Schools, maker spaces, and online forums have widened visibility and technical knowledge, promoting experimentation and innovation on an individual scale. Such cultural change rewards creativity, autonomy, and learning through experience, and therefore single-user 3D printers are best suited to hobbyists, students, and professionals.

- By printing technology type, the fused deposition modelling (FDM) accounted for the largest share 42.87% in 2024. The growth is driven by its low cost, ease of use, wide material compatibility, and strong presence in the hobbyist and educational segments.

- The consumer goods in the end user segment are the fastest growing segment with an estimated CAGR of 6.7%, due to rising demand for customized products, rapid prototyping, and home-based fabrication of lifestyle and utility items.

Personal 3D Printers Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 5.99 Billion |

| Market Size in 2025 | USD 6.17 Billion |

| Forecast Period 2025 - 2034 CAGR | 6% |

| Market Size in 2034 | USD 10.47 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Affordability of desktop models | Contributes 30% growth as low-cost printers make personal 3D printing accessible to students, hobbyists, and first-time users globally. |

| Expanding DIY & maker culture | Drives 20% growth as rising interest in personalized projects like cosplay, model-making, and functional parts strengthens grassroots adoption. |

| Educational integration | Adds 15% growth by embedding 3D printing in STEM curricula, leading to recurring institutional demand and long-term user familiarity from an early age. |

| User-friendly software & ecosystems | Drives 10% growth through intuitive software, pre-configured slicers, and guided setups that lower the entry barrier for beginners and increase usability. |

| Growth of customization trends | Enables 10% growth as consumers increasingly value the ability to design and print one-off items tailored to their specific needs and preferences. |

| Pitfalls & Challenges | Impact |

| Limited Material Versatility | Restrains growth, as inability to print with advanced materials (e.g., ABS, carbon fibre composites) limits crossover into prosumer and functional parts markets. |

| Maintenance & Reliability Issues | Causes user churn, particularly among first-time buyers discouraged by manual calibration, part failures, or clogging, affecting overall market stickiness. |

| Opportunities: | Impact |

| Growth in Micro-Entrepreneurship | Drives growth, as individuals monetize 3D printing via online stores (e.g., Etsy), boosting filament sales, printer upgrades, and design software adoption. |

| Integration with AI & IoT | Contributes to growth, with smart printers offering auto-calibration, remote access, and error detection, attracting professionals and tech-savvy users. |

| Entry into Home Healthcare & Assistive Devices | Adds growth, by enabling affordable, custom printing of orthotic tools, ergonomic handles, and home medical models. |

| Localized Sustainability & Recycling | Unlocks growth, driven by interest in filament recyclers, biodegradable materials, and low-waste home manufacturing, appealing to eco-conscious users. |

| Market Leaders (2024) | |

| Market Leaders |

Top 2 companies hold 33% market share in 2024 |

| Top Players |

Collective market share in 2024 is 59.9% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | North America |

| Fastest Growing Market | Asia Pacific |

| Emerging Countries | India, Brazil, Vietnam |

| Future outlook |

|

What are the growth opportunities in this market?

Personal 3D Printer Market Trends

- The market has witnessed diversification in printable materials, including advanced polymers, composites, and biodegradable filaments. Coupled with improved software and slicing technologies, these developments enable higher accuracy, durability, and customization in printed objects. Innovations in hybrid and multi-material printing further enhance the versatility of personal 3D printers, supporting complex prototypes and specialized applications.

- Manufacturers have been adopting subscription-based services, bundled support packages, and online marketplaces for designs and materials. These models foster continuous engagement with users, creating recurring revenue streams and facilitating seamless access to updates, maintenance, and technical guidance. Such approaches strengthen customer loyalty while lowering entry barriers for new users in personal and professional segments.

- Personal 3D printing has increasingly integrated with cloud-based platforms, IoT connectivity, and CAD software ecosystems. This integration enables remote monitoring, collaborative design, and real-time updates, enhancing operational efficiency. By bridging hardware with digital tools, manufacturers provide a more streamlined user experience, accelerating adoption among educators, hobbyists, and small enterprises seeking scalable and connected fabrication solutions.

Personal 3D Printer Market Analysis

Learn more about the key segments shaping this market

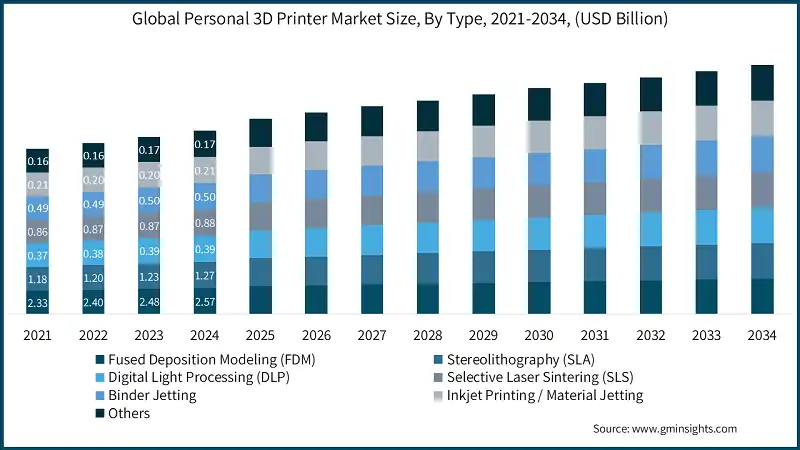

Based on printing technology type, the market is segmented into fused deposition modeling (FDM), stereolithography (SLA), digital light processing (DLP), selective laser sintering (SLS), binder jetting, inkjet printing / material jetting and others.

- The fused deposition modeling (FDM) market has continued exponential growth and is expected to reach USD 2.57 billion in 2024, with a CAGR of 7.1%. This growth is led by broad accessibility, material versatility, and strong adoption across consumer and educational applications. Advancements in fused deposition modelling (FDM) have emerged and introducing printers that automate bed levelling, incorporate silent motor drivers, and feature advanced filament detection. To maintain a competitive edge, FDM manufacturers emphasize on a modular architecture, the capacity to print with multiple materials, and user interfaces that shorten the learning curve.

- The stereolithography (SLA) segment valued USD 1.27 billion in 2024 and will grow at a CAGR of 6.4%. This growth is driven by the rising demand for high-resolution prototyping and intricate model fabrication in industries like healthcare and jewellery, where precision and surface finish are critical. For instance, Elegoo and Anycubic continue to enhance their SLA printer families with new resin formulations, higher resolutions in LCD panels and faster curing.

")

Learn more about the key segments shaping this market

Based on technology, the personal 3D printer market is segmented into thermoplastics, photopolymers / resin, composites, wax, ceramics and others.

- The thermoplastics segment was valued at USD 1.77 billion in 2024 and is projected to grow at a CAGR of 5.3%. This expansion can be attributed to thermoplastics' versatility, low-cost manufacturing, and compatibility with FDM 3D printing, making them the material of choice for hobbyist, educational, and prototyping applications. Companies like Prusa Research and Creality are expanding their filament portfolios with enhanced PLA, ABS, and PETG formulations to meet evolving user needs in strength, flexibility, and sustainability. Moreover, manufacturers are concentrating on the creation of sustainable, recyclable thermoplastics and engineered polymer blends formulated for particular performance criteria, such as enhanced impact resistance suitable for tooling and biocompatibility required in medical prototypes.

- The photopolymers / resin segment accounts for USD 1.51 billion in 2024 and is the fastest growing, with a CAGR of 7.5%. This acceleration is driven by the increasing deployment of resin-based additive manufacturing in fields that demand acute dimensional fidelity and intricate surface finishes, including fine jewellery, dental appliances, and detailed miniatures. Brands like Elegoo and Anycubic have popularized affordable SLA and MSLA printers that deliver professional-grade outputs, making resin printing more accessible to prosumers and small businesses.

On the basis of sales channel, the personal 3D printer market is segmented into online retail (brand-owned websites and e-commerce platforms) and offline retail.

- The online retail segment dominated the market and valued at USD 3.75 billion in 2024. This growth is supported by the increasing traction of e-commerce platforms such as Amazon, AliExpress, and the official Creality store, which together feature an extensive range of products, clear pricing, verified user inspections, and convenient home delivery. In addition, online volume is further strengthened by seasonal discount campaigns, influencer testimonials, and maker communities that supports the democratization of 3D printing. Further, the manufacturers are building direct-to-consumer (D2C) strategies, optimize listings with rich product content, tutorials, and customer support with major e-retailers for global visibility.

- The offline retail segment is USD 2.24 billion as of 2024 and growing at a CAGR of 5.2%. the segment growth is fuelled by rising interest from educational institutions, makerspaces, and walk-in technology shops, where customers favour tactile demonstrations, in-person advice, and accessible local repair service. Specialty electronics retailers and hobbyist chains across urban centers are enhancing their in-store 3D printing offerings, often bundling them with training workshops or filament subscriptions.

Based on end use, the personal 3D printer market is segmented into education, healthcare, aerospace and defense, automotive, consumer goods, manufacturing and jewellery.

- The manufacturing segment accounts for the highest market share of 25.7% in 2024. The growth is driven by increasing demand for rapid prototyping, custom tooling applications, and low-volume part production in sectors such as electronics, robotics, and consumer goods. SMEs have even started incorporating personal 3D printers on the production floor to reduce lead times and material waste, and to improve efficiency.

- The consumer goods segment is witnessing the significant growth at a CAGR of 6.7% during the forecast period. Rising DIY culture and demand for personalized products like home décor, toys, and accessories are fuelling adoption of personal 3D printers. Brands are also using desktop 3D printers for limited-run product testing and customization which increasing the demand for the personal 3D printer in consumer goods.

")

Looking for region specific data?

The North America personal 3D printer market size was valued at USD 2.15 billion in 2024. The market is growing due to increasing consumer adoption for home prototyping, educational applications, hobby use, and the availability of affordable, user-friendly plug-and-play devices.

- The U.S. held the largest share and thus dominated the North America market, worth USD 1.61 billion in 2024. This growth is facilitated from the mature consumer electronics sector and incorporation of 3D printers in K-12 and higher education programs. Leading manufacturers like Prusa, Creality (via U.S. distributors), and Bambu Lab dominate the retail and online eco-systems and there are active online communities and maker spaces for more support. U.S. consumers are equipped with reliable supply chains for filaments, accessories, and repair services providing more benefits for hobbyists and creators generally to adopt 3D printing.

- U.S. manufacturers and distributors are prioritizing superior customer support, broadening the content ecosystem through libraries of pre-sliced STL files and instructional videos, and introducing environmentally responsible initiatives such as filament-recycling programs and low-emission printers. The rising trend of localized micro-manufacturing and bespoke product design is expected to deepen penetration, particularly among independent designers and small-scale enterprises nationwide.

- Canada personal 3D printer market is projected to grow steadily with a CAGR of 4.7%. This growth is supported by growing implementation in K-12 and post-secondary institutions, federal programs that strengthen digital literacy and a rising community of enthusiast users. Municipal makerspaces and public library networks in Toronto, Vancouver, and Montreal have placed open-access desktop printers within reach of citizens of all ages. Canada’s robust e-commerce logistics further enable nationwide distribution of printers, components, and consumables, reducing lead times for educators and hobbyists alike.

Europe personal 3D printer market transacted USD 1.43 billion in 2024. The growth of this market is powered by strong integration of 3D printing in education, government support for digital fabrication, rising maker culture, and increasing demand for sustainable, locally produced custom goods.

- The UK has completely dominated the Europe market, with a market size of USD 414.5 million in 2024. Their strong position can be attributed to consumer awareness, conducive maker and hobbyist communities, and access to 3D printing educational opportunities or environments either through schools or libraries. Government-backed STEM programs and funding associated with innovation have generated increasing demand and access to increasingly low-cost 3D printers from brands like Creality, Prusa, and others. Moreover, UK-based personal 3D printer manufacturers strengthen ties with educational institutions, makerspaces, and tech retail chains to broaden market reach. Offering customized printer kits, free beginner training modules, and school-specific discounts could encourage early adoption among students and hobbyists.

- Germany is projected to be a consistent and favourable market trend at a CAGR of 4.4%. This growth is supported by Germany's strong industrial economy, technical educational system, and active maker community. Local innovations, technology-focused education systems, and high-end European printer brands making national waves which further add to consumer acceptance. Additionally, personal 3D printer manufacturers in Germany focuses on entering in alliances with firms that provide vocational education, education technology, and other business starter kits to early adoption. They promote high-precision, safety certified desktop printers with German language software support and local technical support to build confidence and connection.

The Asia Pacific personal 3D printer market will be valued at USD 1.17 billion by 2024. Market growth influenced by rising adoption in STEM education, increasing affordability of desktop printers, expanding maker communities, and government-led digital manufacturing initiatives across countries like China, India, and Japan.

- China personal 3D printer industry was valued at USD 414.8 million in 2024. The country's dominance is driven by strong consumer enthusiasm for DIY electronics, widespread adoption in education, and a robust domestic manufacturing base. Local brands like Creality and Anycubic have made advanced features accessible at competitive prices, accelerating adoption. Furthermore, government policies supporting STEM education and innovation at the grassroots level continue to fuel market growth. Moreover, 3D printer manufacturers in China design economical, user-friendly 3D printers equipped with curriculum-aligned software tailored for schools and neighbourhood learning environments.

- Japan market is projected to grow steadily with a CAGR of 9.3%. Growth is driven by Japanese culture's strengths in precise engineering, DIY culture, and the educational use of 3D printing. The introduction of personal 3D printers into home prototyping, maker communities, and robotics education, lends itself to increased performance. Japanese tech-savvy consumers consistently prioritize quality and reliability, compact design, and other capabilities which are leading demand in urban households, schools, and education.

- South Korea market is valued at USD 122.9 million market in 2024 and supported by government for digital manufacturing, integration of 3D printers into STEAM education, and a technology-oriented consumer base. The emergence of home-based creators and hobbyists, along with educational robotics programs, coupled with the national push for smart manufacturing, has expanded interest and adoption of desktop 3D printers.

The Middle East and Africa (MEA) personal 3D printer market was valued at USD 509.5 million in 2024. Growth of the market is driven by rising interest in localized manufacturing, educational deployments, innovation hubs, and healthcare applications such as affordable prosthetics and medical models.

- In 2024, Saudi Arabia dominated the MEA market, which had a size of USD 131.1 million. The growth was facilitated by the government's ongoing Vision 2030 initiatives for the realization of a digital transformation agenda in the realms of education technology and localized manufacturing. The alignment of Saudi Arabia’s 3D printing developments, in schools, universities, and local maker spaces; and the government's funding for innovation hubs, significantly stimulated the consumer adoption of personal 3D printers.

- The UAE market is expected to grow steadily with a rate of 5.2% CAGR. The growth is driven by a combination of strong interest in the digital transformation agenda, emphasis on STEM education, and 3D printing as part of smart city initiatives, such as the Dubai 3D Printing Strategy. Government initiatives are stimulating 3D printing projects in labs, public libraries, as well expanding access to household desktop 3D printing through retail and e-commerce.

Personal 3D Printer Market Share

- The top 5 companies Creality 3D, Anycubic, Prusa Research, Elegoo and FlashForge combine 59.9% of the market share, highlighting strong market consolidation driven by their broad product ranges, global retail presence, and consistent innovation in desktop 3D printing technologies.

- Creality 3D accounts for roughly 19.8% of their market share in 2024, attributed to the strength of its desktop FDM printers, ability to reach global markets through online retailer channels, and agile and focused innovation across multiple product lines in exciting new markets creating exciting new products for customers. Its extensive portfolio and price points position it well for personal and prosumer markets.

- Anycubic has a market share of 13.2% in 2024, driven by its extensive range of resin (SLA/DLP) printers and increasing adoption in the hobbyist and professional design communities. The company's investment in R&D and software integration, along with strategic pricing, has enhanced its appeal across both entry-level and mid-range users globally.

- Prusa Research has market share of 11.1% in 2024, owing to its reputation for reliable, open-source hardware and strong community support. The Original Prusa i3 series is widely adopted in both academic and industrial prototyping environments, and its in-house PrusaSlicer software ecosystem strengthens user retention.

- Elegoo is strongly positioned in the market at 8.4% of the total share in 2024, well-regarded for its affordable and high-resolution resin printers such as the Mars and Saturn series. Elegoo’s competitive pricing, growing ecosystem of accessories, and rising popularity among designers and modelers fuel its steady market position.

- FlashForge has a 7.4% share in 2024, which is supported by its dual focus on FDM and professional-grade 3D printers. With user-friendly platforms like the Adventurer and Creator series and increasing visibility in educational and small business use cases.

Personal 3D Printer Market Companies

List of prominent players operating in the personal 3D printer industry include:

- Creality 3D

- Anycubic

- Prusa Research

- Ultimaker (now part of UltiMaker, merged with MakerBot)

- MakerBot

- Elegoo

- FlashForge

- Bambu Lab

- Raise3D

- Artillery 3D

- Voxelab (a sub-brand of FlashForge)

- Phrozen

- Formlabs (mainly professional but offers compact models used personally)

- QIDI Tech

- Snapmaker

- Monoprice

- LulzBot (by Aleph Objects)

- XYZprinting

- Tronxy

- Anycubic Photon

- Wanhao

- Peopoly

- Dremel DigiLab

- Tenlog 3D

- Sindoh

- Creality 3D and Anycubic are the market leaders with strong recognition and global presence, broad product line, and known for aggressive pricing schemes available worldwide in the personal 3D printer market. Creality benefits from popularity with its successful Ender and CR series, while Anycubic has strong offerings both in terms of FDM printers and resin printers like the Photon series. Both companies continue to invest significantly in R&D related to enhanced accuracy, better wireless connectivity, user experience and overall UI/UX experiences, and are expanding into the educational and prosumer segments in various ways to create partnerships, crowdfunding, and direct-to-consumer opportunities.

- Prusa Research is considered a challenger and acknowledged for its open-source innovations and community of loyal users. Prusa Research has focused on delivering premium build quality with strong after sales service and previously offered the flagship Original Prusa i3 MK4 to a substantial universe of 3D printer enthusiasts and professionals.

- Elegoo and FlashForge are viewed as followers, moving along at a steady rate offering value-orientated resin and FDM printers with acceptable quality and availability. Their mission is to benefit from the growing maker and hobbyist base, even though they do not carry the brand or ecosystem advantage as the leaders captured.

- Niche players in this space include newer entrants or local brands focusing on specific materials (e.g., clay 3D printing) or purpose-built printers for jewellery or dental applications. These firms carve out specialization-based footholds but lack scale or global brand visibility.

Personal 3D Printer Industry News

- In March 2025, UltiMaker, a desktop 3D printing company, has introduced the UltiMaker S8 3D printer, which aimed at increasing productivity while maintaining high-quality precision, security, and reliability.

- In March 2025, Formlabs announced that it added two exciting new products to the Formlabs SLA ecosystem, a curing solution and a functional resin which is tougher than the previous iterations.

- In April 2025, AdvancedTek has added Formlabs 3D Printers to its already robust portfolio, providing better access to professional SLA & SLS additive manufacturing solutions throughout the entire Midwest.

The personal 3D printer market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue (USD Million) and Volume (Units) from 2021 – 2034 for the following segments:

Market, By Printing Technology

- Fused Deposition Modeling (FDM)

- Stereolithography (SLA)

- Digital Light Processing (DLP)

- Selective Laser Sintering (SLS)

- Binder jetting

- Inkjet printing / material jetting

- Others

Market, By Material Type

- Thermoplastics

- PLA

- ABS

- PETG

- Nylon

- Others

- Photopolymers / resin

- Standard resin

- Tough resin

- Flexible resin

- Castable resin

- Composites

- Carbon-fiber infused

- Wood-filled

- Metal-filled

- Others

Market, By Price Range

- Low-end (Below USD 300)

- Mid-range (USD 300–1,000)

- High-end (Above USD 1,000)

Market, By Distribution Channel

- Online retail

- Brand-owned websites

- E-commerce platforms

- Offline retail

- Technology & electronics stores

- Educational suppliers & EdTech distributors

- Authorized dealers

Market, By End Use

- Education

- Healthcare

- Aerospace and defense

- Automotive

- Consumer goods

- Manufacturing

- Jewellery

- Others

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Netherlands

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

Frequently Asked Question(FAQ) :

Who are the key players in the personal 3D printer market?

Key players include Creality 3D, Anycubic, Prusa Research, Elegoo, FlashForge, Bambu Lab, Ultimaker, MakerBot, Raise3D, Formlabs, and XYZprinting

Which region leads the personal 3D printer market?

The U.S. dominated the North America market with USD 1.61 billion in 2024. Growth is supported by strong consumer adoption, integration in K–12 and higher education, and robust supply chains

What are the upcoming trends in the personal 3D printer industry?

Key trends include integration with cloud platforms and IoT, expansion of multi-material and biodegradable filaments, and the rise of micro-entrepreneurship through online design marketplaces

What is the growth outlook for the consumer goods segment from 2025 to 2034?

The consumer goods segment is projected to grow at a CAGR of 6.7% till 2034, driven by rising DIY culture and demand for personalized products

How much revenue did the fused deposition modeling (FDM) technology segment generate in 2024?

The FDM technology segment generated USD 2.57 billion in 2024, leading the market with 42.87% share

What was the valuation of the online retail distribution channel in 2024?

Online retail accounted for USD 3.75 billion in 2024, dominating the market due to strong e-commerce platforms and direct-to-consumer strategies

What is the projected value of the personal 3D printer market by 2034?

The market size for personal 3D printer is expected to reach USD 10.47 billion by 2034, supported by rising consumer adoption, customization trends, and home-based fabrication

What is the market size of the personal 3D printer industry in 2024?

The market size was USD 5.99 billion in 2024, with a CAGR of 6% expected through 2034 driven by affordability of desktop models and integration in education

What is the current personal 3D printer market size in 2025?

The market size is projected to reach USD 6.17 billion in 2025

Personal 3D Printers Market Scope

Related Reports