Authors:

Preeti Wadhwani, Satyam Jaiswal

Download free PDF

Parking Management Market Size & Share 2026-2035

Report ID: GMI2956

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Parking Management Market

Get a free sample of this report

Get a free sample of this report Parking Management Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Parking Management Market Size

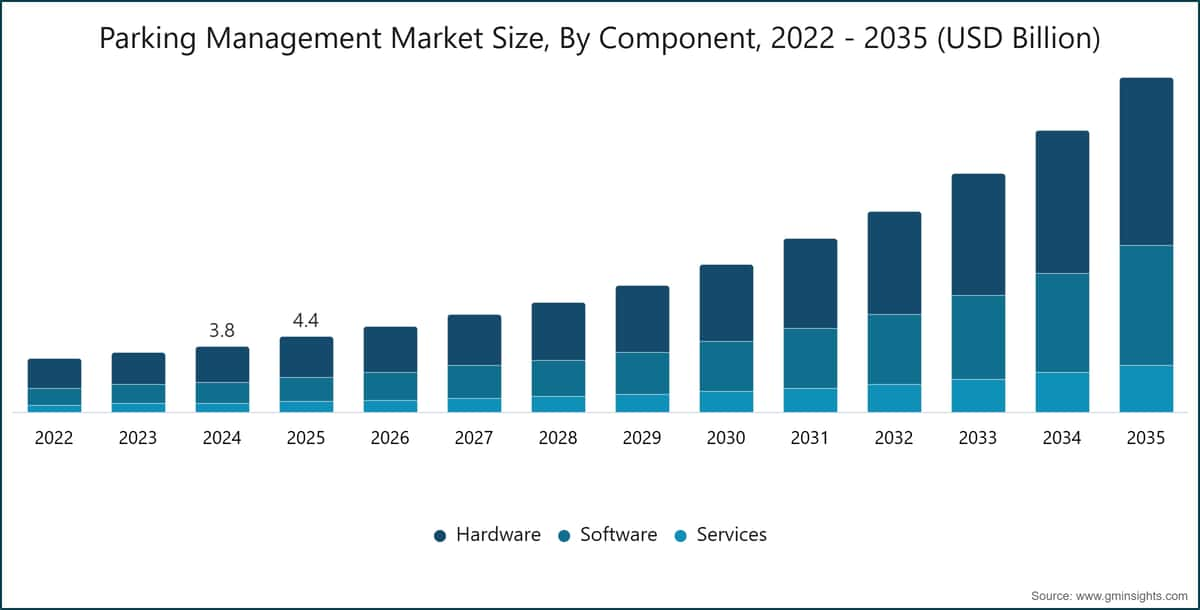

The global parking management market was valued at USD 4.4 billion in 2025, after expanding from USD 3.8 billion in 2024 as cities and private operators accelerated digital parking upgrades. The market is projected to reach USD 19.4 billion by 2035, advancing at a 16.4% CAGR over 2026–2035, according to the latest report published by Global Market Insights Inc.

Parking Management Market Key Takeaways

Market Leader: SWARCO led with over 3.1% market share in 2025.

Leading Players: Top 5 players in this market include SWARCO, Siemens, Amano, TKH, HUB Parking Technology, which collectively held a market share of 9.6% in 2025.

Growth is being shaped by a practical constraint: vehicle density continues to rise faster than urban parking supply can be physically expanded. The result is a stronger procurement case for sensor-based occupancy detection, cloud-connected revenue control, mobile payments, and analytics platforms that let operators improve utilization without adding new land or structures.

Key Drivers

Drivers Impact Analysis

Driver

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Rapid Urbanization and Vehicle Ownership Growth

+3.5%

Global — highest in APAC and LATAM

Long term (≥ 4 years)

Smart City Initiatives and Digital Infrastructure Investments

+3.2%

North America, Europe, GCC/MEA

Medium term (2-4 years)

Growing Adoption of Mobile and Contactless Payments

+2.8%

Global — fastest in APAC and LATAM

Short term (≤ 2 years)

Demand for Real-Time Parking Availability Solutions

+2.5%

North America, Europe, Urban APAC

Medium term (2-4 years)

Rapid Urbanization and Vehicle Ownership Growth

Urban growth is intensifying pressure on parking assets in city centers, university districts, airports, hospitals, and mixed-use commercial developments. The United Nations projects that 68% of the global population will live in urban areas by 2050, with much of the incremental growth concentrated in emerging economies.[1]United Nations, https://www.un.org For the parking management market, that demographic shift converts directly into demand for systems that raise space turnover, improve guidance, and enforce payment compliance. Physical parking expansion remains difficult in dense districts because land costs, zoning restrictions, and public opposition limit new construction. Digital management therefore becomes the more scalable option.

Smart City Initiatives and Digital Infrastructure Investments

Smart city programs are turning parking management from a facility-level operating tool into a municipal infrastructure priority. The European Commission’s Sustainable and Smart Mobility Strategy and broader urban mobility framework emphasize digital transport infrastructure, data sharing, and lower-emission urban movement.[2]European Commission, https://commission.europa.eu In North America, US Department of Transportation programs have supported intelligent transportation systems that include parking availability, dynamic curb management, and demand-responsive pricing.[3]U.S. Department of Transportation, https://www.transportation.gov The second-order effect matters for vendors: once a city installs connected parking infrastructure, software licensing, maintenance, data integration, and analytics contracts can extend over several budget cycles.

Growing Adoption of Mobile and Contactless Payments

Mobile and contactless payment adoption is changing how operators capture revenue. GSMA data indicates that mobile money and digital payment adoption exceeded 1.75 billion registered accounts globally by end-2024, with faster transaction growth in Southeast Asia, Sub-Saharan Africa, and Latin America.[4]GSMA, https://www.gsma.com In parking operations, mobile-first payment reduces cash handling, improves auditability, and shortens payment queues. It also allows pricing rules to adjust by time, occupancy, event schedules, and location. Operators in London, Singapore and New York have reported lower leakage after replacing cash-accepting assets with app-based or license-plate-recognition payment infrastructure.

Demand for Real-Time Parking Availability Solutions

Parking search behavior remains a measurable source of congestion. The International Transport Forum estimates that vehicles looking for spaces can account for 8%–30% of traffic volume in dense urban cores.[5]International Transport Forum, https://www.itf-oecd.org Real-time parking availability systems address that inefficiency through ultrasonic sensors, magnetic in-ground sensors, camera-based occupancy detection, cloud platforms, and guidance displays. The business case is not limited to driver convenience. Municipalities can use parking availability data to reduce circling, improve curb utilization, support emissions plans, and allocate enforcement resources more precisely.

Key Challenges

Restraints Impact Analysis

Challenge

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Initial Infrastructure and Deployment Costs

-2.0%

Global — most acute in LATAM and MEA

Short term (≤ 2 years)

Data Security and Privacy Concerns

-1.5%

Europe, North America, Urban APAC

Medium term (2-4 years)

Comprehensive smart parking deployments can require sensors, cameras, access barriers, communication networks, civil works, back-end software, and integration with payment or enforcement systems. Ground-sensor installation adds cost in on-street bays and surface lots, while structured facilities often need cabling, power modifications, network upgrades, and lane reconfiguration. This cost profile is most restrictive for mid-tier municipalities and property owners with limited capital budgets. Cloud-based delivery and software-as-a-service procurement help mitigate the barrier by shifting part of the spending from upfront capex to recurring operating budgets.

Data Security and Privacy Concerns

Connected parking systems collect license plate numbers, payment credentials, vehicle movement patterns, and location data. In Europe, the General Data Protection Regulation has made privacy-by-design a procurement requirement for operators handling identifiable vehicle data. Comparable data governance expectations are expanding in North America, Singapore, and Australia. Compliance raises spending on encryption, access controls, audit trails, data minimization, breach procedures, and vendor certification. Suppliers with ISO 27001-aligned controls and edge-processing architectures are better positioned where security scoring influences tender outcomes.[6]

Parking Management Market Trends

AI, IoT, and Smart Sensors Move Occupancy Detection into Core Operations

AI-enabled occupancy detection is becoming a central operating layer in the parking management market. The earlier generation of smart parking relied heavily on individual ground sensors that identified occupied or vacant bays, then transmitted availability data to signs or apps. Current deployments are more varied. Operators now combine ultrasonic sensors, magnetic sensors, camera-based detection, automatic license plate recognition, edge computing, and cloud analytics. IEEE-documented connected parking architectures indicate that edge-computing nodes can process sensor data with latency under 50 milliseconds, which is fast enough to keep driver-facing availability signs closely aligned with actual space status.[7]IEEE, https://www.ieee.org

The clearest use case remains demand-responsive pricing. The SFpark pilot embedded magnetic sensors in more than 8,200 on-street spaces and 12,250 off-street spaces across seven neighborhoods, producing a 30% reduction in parking search traffic in pilot zones relative to control areas. For city planners, the value lies in the ability to influence driver behavior without expanding physical parking supply. For operators, the value is more direct: real-time occupancy data allows pricing, enforcement, maintenance, and staffing decisions to match demand.

In our Q1 2026 primary research covering 68 urban parking operators across 14 countries, 74% reported active deployment or pilot programs for AI-assisted occupancy forecasting, compared with under 30% in a comparable early-2023 survey. The finding indicates that predictive tools have moved beyond demonstration projects. Operators now use occupancy forecasting to prepare for event traffic, direct enforcement teams, manage permit-holder allocation and reduce congestion at facility entrances. The impact on forecast CAGR is medium term because many deployments begin with pilots before expanding to full municipal or multi-site commercial networks.

Cloud-Based Parking Platforms Become the Fastest-Growing Architecture

Cloud-based deployment is the fastest-growing delivery model in the parking management market, with a projected 20.9% CAGR through 2035. The operational logic is straightforward. A cloud platform removes much of the on-site server burden, gives operators a single view of multiple assets, supports remote updates, and enables tariff changes without field intervention. Flowbird has deployed cloud-managed pay station networks across municipalities in France, the United Kingdom, the United States, and Australia, allowing remote diagnostics and tariff updates across distributed sites.

This trend has procurement implications. Municipal buyers often struggle to secure large capital appropriations for full technology replacements, especially where parking revenue flows into general city funds. Subscription-based software models can fit more easily into annual operating budgets. They also create a more predictable vendor relationship, with recurring service-level expectations tied to uptime, cybersecurity, payment processing and reporting.

The deeper shift is architectural. As parking platforms move to the cloud, they become easier to connect through APIs to navigation tools, enforcement platforms, public transit applications, payment gateways and building management systems. That capability matters because parking data is no longer valuable only inside the facility. Real-time space availability, payment status, reservation inventory, and violation records can support broader mobility planning. Over time, this integration layer should become a larger basis of vendor differentiation than stand-alone hardware specifications.

Mobile Reservation and Contactless Payment Reduce Transaction Friction

Mobile reservation and contactless payment tools are changing the customer-facing side of the parking management market. SpotHero operates in more than 300 cities across North America, illustrating the scale at which advance reservation platforms can aggregate demand across fragmented parking assets. Flash Parking has built a technology-enabled network focused on operators managing multi-location commercial facilities. These models link reservation inventory, dynamic pricing, customer accounts, and facility access into a single transaction flow.

Payment modernization produces measurable operating benefits. Municipalities that have shifted toward mobile-primary payment infrastructure have reported revenue capture rates 12%–18% higher than comparable cash-accepting facilities, driven mainly by reduced unpaid overstays and improved digital transaction logs. The link with GSMA’s global mobile payment data is direct: wider mobile wallet adoption gives operators a larger addressable base for app, NFC, QR, and license-plate-based payment models. In practice, this reduces dependence on cash collection, meter maintenance, paper ticket stock, and manual reconciliation.

The strongest near-term implication is tariff flexibility. Once a driver account, license plate, reservation, and payment method are tied to a digital record, operators can apply event pricing, short-stay incentives, validation rules, loyalty pricing, and enforcement triggers with greater precision. That flexibility is particularly important in airports, hospitals, stadium districts, central business districts, and mixed-use retail assets where demand changes sharply by hour and event schedule.

Parking Data Becomes Part of Smart Mobility Integration

The parking management market is increasingly connected to wider urban transport data systems. Singapore’s Land Transport Authority has pursued this model through the OneTransport platform, which integrates parking availability data from more than 1,900 public car park facilities and makes mobility data accessible to third-party application developers.[8]Land Transport Authority Singapore, https://www.lta.gov.sg The European Commission’s Urban Mobility Framework also supports data-sharing obligations for urban transport operators as part of digital infrastructure funding. These programs show how parking data can become an input into route planning, congestion management, transit coordination, and emissions policy.

The operating impact is visible in utilization. Cities pursuing integrated mobility platforms tend to achieve parking occupancy rates 10–15 percentage points higher than comparable cities that operate parking systems in isolation. That improvement does not require every space to be newly built or every facility to be rebuilt. It comes from better information flow: drivers can see availability before entering a congested district, operators can publish inventory across channels, and cities can connect parking rules to curb, transit, and traffic-management objectives.

The forecast impact is long term because system integration depends on data standards, governance models, and public-private coordination. Still, the strategic direction is already set. Parking vendors that treat their systems as closed assets will face pressure from municipal buyers that need interoperable data. Vendors with open APIs, privacy-preserving analytics, and strong cloud operations should benefit as parking becomes one node in the connected urban mobility network.

Parking Management Market Analysis

By Component

Hardware accounted for the largest share of the parking management market in 2025, generating USD 2,384.7 million, or 54.0% of global revenue, and is projected to grow at a 15.5% CAGR through 2035. This segment includes automated barrier arms, access control gates, license plate recognition cameras, ultrasonic sensors, electromagnetic in-ground sensors, multi-space pay stations, and variable message signage.

CAME Parkare and Designa Verkehrsleittechnik supply barrier and access-control equipment for structured facilities, while IPS Group provides the IPS Stinger in-ground sensor and cloud-connected pay station platforms for municipal on-street applications. Hardware demand tracks both new facility construction and retrofits of aging cash-and-ticket systems. The more practical procurement driver is the expectation that physical parking assets now need to generate data, not just control entry.

Software platforms represented USD 1,432.7 million in 2025, or 32.5% share, and are expanding at a 17.6% CAGR through 2035. Services accounted for USD 596.3 million, equal to 13.5% of revenue, covering installation, maintenance, integration, and managed operations. T2 Systems’ University Parking and Transportation Management platform demonstrates how software is tailored for campus permit management, mobile payment, enforcement routing, and customer account administration.

ParkHelp Technologies offers guidance software that connects with variable message signage to show real-time space availability at multi-level car park entrances. The value of software rises as more hardware becomes sensor-capable, because analytics, pricing rules, alerts, and integrations determine how much financial benefit operators extract from the physical network.

By Deployment Mode

Learn more about the key segments shaping this market

Download Free PDF

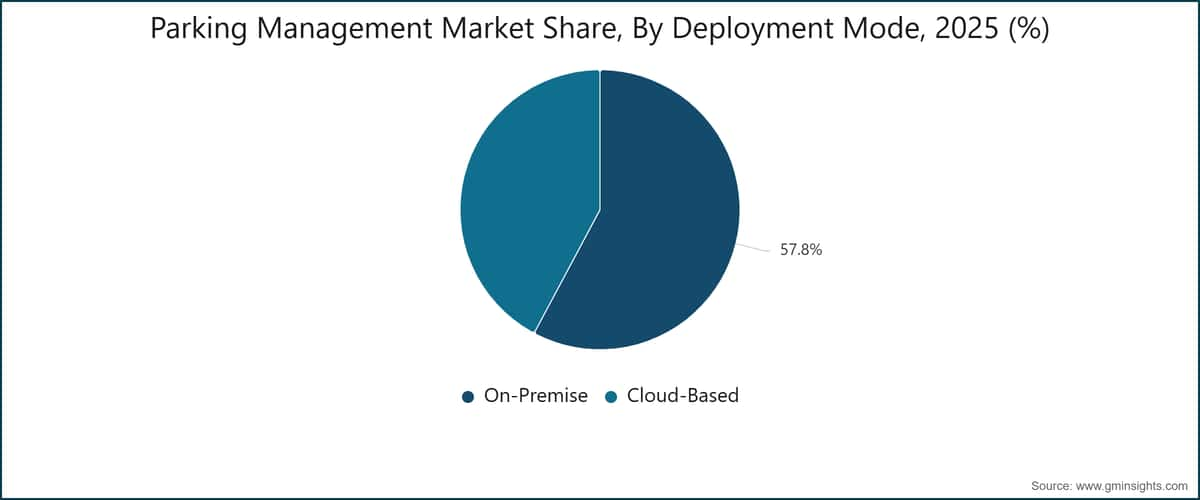

On-premise systems generated USD 2,551.1 million in 2025, representing 57.8% of the parking management market. Many airports, government facilities, universities, and legacy municipal systems still operate on-premise architectures because they have established IT environments, security protocols, and integration dependencies. These systems can remain appropriate where operators need direct control over servers, data storage, and lane equipment. However, on-premise deployment can create upgrade friction because software updates, diagnostics, and reporting often require site-level intervention.

Cloud-based parking platforms are expanding at a 20.9% CAGR through 2035, making them the fastest-growing deployment model. In our H1 2026 interviews across Tier-1 parking infrastructure procurement offices, 58% of respondents said they were actively evaluating camera-based guidance systems as replacements for aging ground-sensor infrastructure, with lower per-bay installation cost and license plate capture capability as the primary decision drivers. Cloud deployment supports that shift because camera feeds, occupancy analytics, payment records, and enforcement workflows can be managed centrally.

Flowbird’s cloud-managed pay station networks and Frogparking’s cloud-native parking management platform illustrate the two ends of the market: large municipal networks on one side, sensor-agnostic mid-size city platforms on the other. Pricing dynamic favors cloud adoption where buyers want predictable operating expenditure and easier multi-location oversight.

By Solution

Parking Access and Revenue Control Systems remained the largest solution category in 2025 at USD 1,569.5 million, equal to 35.6% share, with growth projected at a 15.2% CAGR through 2035. PARCS includes entry management, barrier control, ticketing, validation, payment, and exit processing. SKIDATA AG’s access and revenue systems are deployed across airports, shopping centers, ski resorts, and structured parking assets in more than 100 countries. HUB Parking Technology’s ISEC access system combines license plate recognition, mobile credential acceptance, and cloud-connected reporting for high-throughput facilities. Demand is strongest where aging coin-and-ticket equipment cannot support mobile validation, contactless payment, dynamic pricing, or third-party reservation integration.

Parking Reservation and Payment Solutions are the fastest-growing solution category, rising from USD 1,285.3 million in 2025 to a projected USD 6,734.8 million by 2035 at an 18.4% CAGR. Guidance Systems generated USD 696.0 million in 2025 and are expected to grow at a 17.2% CAGR. Cleverciti Systems has deployed aerial sensor guidance platforms in Germany, the United States, and Australia, using wide-angle cameras to monitor multiple bays without installing individual ground sensors.

Genetec AutoVu supports license plate recognition for permit validation, visitor management, and violation detection, while Nedap’s MACE platform and long-range UHF RFID readers support permit-based access in high-throughput commercial and transit-adjacent parking assets. Product differentiation is increasingly tied to software interoperability, not only lane hardware reliability.

By Region

North America Parking Management Market Trends

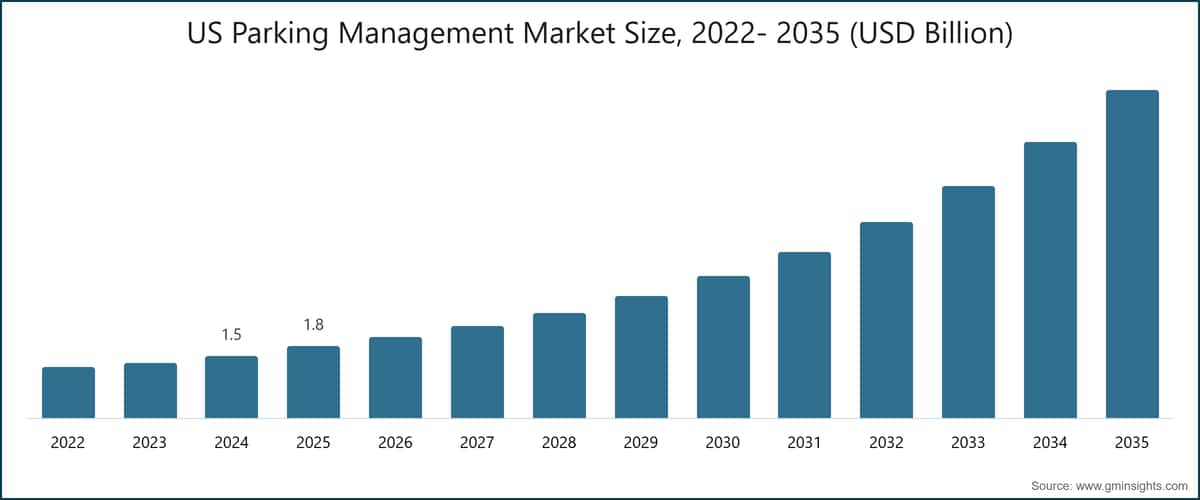

The North America parking management market was the largest regional market in 2025, generating USD 2,034.7 million and representing 46.1% of global revenue. The region is projected to reach USD 9,039.3 million by 2035 at a 16.5% CAGR. The United States parking management market contributed USD 1,764.2 million in 2025 and is growing at a 16.8% CAGR, supported by US Department of Transportation intelligent transportation initiatives in cities including Los Angeles, Chicago, and Seattle.

The LA Express Park program covered 6,000 on-street metered spaces and four city-owned garages, reducing average parking search time by 10% while increasing meter revenue by 15% in the first full year. Canada contributed USD 270.6 million in 2025 at a 14.1% CAGR, with Toronto and Vancouver using urban mobility funding and transit-oriented development requirements to support integrated parking data platforms.

Europe Parking Management Market Trends

The Europe parking management market generated USD 1,281.7 million in 2025 and is forecast to reach USD 5,388.2 million by 2035 at a 15.9% CAGR. Germany is the largest national market in Europe, with USD 372.2 million in 2025 revenue and a 15.3% CAGR, supported by smart infrastructure priorities under the National Action Plan for Smart Cities. SWARCO, headquartered in Austria with broad German operations, has deployed parking guidance and variable messaging infrastructure across German Autobahn service areas and urban parking districts. GDPR requirements directly shape procurement because license plate and vehicle movement data must be minimized, protected, and governed under privacy rules. The European Urban Mobility Framework is also pushing parking data toward interoperable availability feeds, giving vendors with privacy-preserving edge analytics a stronger position in public-sector tenders.

Asia Pacific Parking Management Market Trends

The Asia Pacific parking management market is the fastest-growing regional market, expanding from USD 599.4 million in 2025 to USD 3,260.5 million by 2035 at an 18.9% CAGR. China is the largest APAC country market, with USD 277.0 million in 2025 revenue and a 19.9% CAGR, supported by Sponge City and Smart City initiatives that integrate parking data into municipal digital infrastructure. The Ministry of Housing and Urban-Rural Development’s parking lot data-sharing requirements under the Urban Parking Management Regulations framework create demand for compatible sensors and software in covered cities. India is expanding parking technology through smart city mission command-and-control infrastructure, while Singapore’s OneTransport platform integrates availability data from more than 1,900 public car park facilities. In our H2 2025 survey of 185 smart city technology managers across eight APAC markets, 67% identified parking management as one of their top three near-term digital infrastructure priorities.

Parking Management Market Share

The parking management market share structure indicates a fragmented competitive base rather than a winner-take-most model. The top seven vendors, SWARCO, Amano, Siemens, TKH, HUB Parking Technology, Flowbird and Conduent Transportation collectively held approximately 12.3% of global revenue in 2025. The remaining 87.7% was distributed across regional integrators, parking operators with proprietary technology, municipal software specialists, payment providers, sensor developers, and enforcement solution vendors. This fragmentation is typical of markets where local procurement relationships, site-specific integration requirements, and regulatory needs influence vendor selection.

SWARCO led the parking management market with a 3.1% share in 2025. Its advantage is portfolio breadth: parking guidance, on-street pay station systems, traffic management, and variable messaging can be packaged for municipalities pursuing wider mobility modernization. Amano Corporation held a 2.0% share, supported by strength in Japan, a broad parking equipment portfolio, and distribution relationships across Asia Pacific and North America. Siemens AG held a 1.8% share and competes differently from pure-play parking vendors. It tends to position parking as one function inside smart building, infrastructure, and city management programs.

TKH held 1.4% share, while HUB Parking Technology held 1.2%. The TKH-HUB combination is strategically relevant because it has industrial technology capabilities with specialized parking access, guidance, and revenue-control products. HUB’s focus on airports, convention centers, and high-throughput mixed-use developments gives it exposure to facilities where downtime and lane congestion carry high economic cost. Flowbird Group and Conduent Transportation add further breadth to the top seven group through pay station networks, transportation payment, and municipal service relationships.

Competitive strategy is shifting toward extensibility. Municipal and commercial buyers increasingly expect parking platforms to integrate with payment processors, navigation APIs, enforcement systems, transit data platforms, building management software, and customer-facing reservation apps. M&A activity has followed that logic, with established vendors acquiring mobile payment tools, cloud operations software, sensor capabilities, and occupancy analytics. Flash Parking’s May 2024 acquisition of a cloud-based parking operations software provider reflects this direction, as the company expanded its enterprise parking management capabilities for multi-location operators.

Conversations with six senior parking technology executives during our Q4 2025 expert panel converged on one point: the most important competitive differentiator over the next five years will be the depth and openness of the software integration layer, not the basic capability of lane hardware. That assessment is consistent with the data. Hardware remains necessary, but barriers, meters, and sensors are becoming easier for buyers to compare on cost and reliability. Software, analytics, data governance, uptime, open APIs, and lifecycle support are harder to replicate quickly. The parking management market share picture should therefore remain fragmented, but vendors with scalable cloud platforms and proven public-sector security credentials are likely to gain disproportionate influence.

Parking Management Market Companies

Major players operating in the Parking Management market are: SKIDATA, Amano, Arrive, Genetec, Swarco, Nedap, Verra Mobility, Designa Verkehrsleittechnik, HUB Parking Technology, ParkHelp Technologies, T2 Systems, IPS, SpotHero, Flash, TIBA Parking Systems, Frogparking, Hectronic, CAME Parkare, Cleverciti Systems, and Flowbird.

SKIDATA is headquartered in Gartenau, Austria, and is one of the most widely distributed PARCS vendors in the parking management market. Its systems are used in airports, ski resorts, shopping centers, and urban structures across more than 100 countries. The company’s platform includes RFID credentials, license plate recognition access, mobile validation, and cloud-managed revenue reporting. SKIDATA’s position is strongest in high-throughput locations where access reliability and transaction speed are central to facility economics.

Amano brings a diversified portfolio to the Asia Pacific parking management market. Its offering includes coin parking systems, multi-space meters, pay-on-foot terminals, and enterprise software for large parking estates. The company’s Japanese base gives it a strong reference market, while distribution partnerships extend its reach into Southeast Asia and North America. Amano is well positioned where buyers need established hardware and localized service coverage.

Genetec is a Montreal-based security intelligence and operations platform vendor. Genetec AutoVu is a license plate recognition system used for permit validation, visitor management, enforcement automation, and violation detection. The company’s main advantage is its ability to link parking operations with video surveillance and access control. That makes Genetec especially relevant for campuses, healthcare facilities, commercial properties, and municipalities that want parking enforcement tied to broader security workflows.

Nedap supplies the MACE parking management platform and long-range UHF RFID readers. Its systems are used in permit-based and season-ticket parking applications where high vehicle throughput and reliable credential recognition are operational priorities. Nedap’s European presence is especially relevant in commercial real estate and public transport interchange facilities.

Verra Mobility operates across transportation technology, automated enforcement, tolling, and government payment services. Its role in the parking management market is linked to municipal enforcement, citation workflows, and vehicle identification services. The company benefits where cities want parking, tolling, permit, and enforcement data to operate through connected back-office processes.

Designa Verkehrsleittechnik provides access and revenue control systems for structured parking environments. Its products are relevant in commercial facilities, transport hubs, and multi-level parking assets that need reliable entry, payment, and exit processing. HUB Parking Technology focuses on PARCS, guidance, access control, license plate recognition, and cloud reporting for airports, convention centers, retail centers, and mixed-use facilities. Its ISEC platform is positioned for high-throughput sites that require mobile credentials and integrated reporting.

ParkHelp Technologies develops parking guidance software and associated systems that show real-time space availability in structured facilities. T2 Systems serves universities, municipalities, and institutional operators with permit management, enforcement routing, mobile payment, and customer account tools. IPS Group specializes in smart meters, multi-space pay stations, and in-ground sensors for municipal on-street parking applications. The IPS Stinger sensor and cloud-connected meter platforms support cities seeking better occupancy data and payment compliance.

SpotHero is a reservation platform operating in more than 300 North American cities. Its model aggregates parking inventory and lets drivers book spaces in advance, making it especially relevant in dense urban centers and event-driven districts. Flash focuses on technology-enabled parking operations, dynamic pricing, access integration, and multi-location enterprise management. TIBA Parking Systems competes in PARCS and received ISO/IEC 27001:2022 certification in March 2024, strengthening its positioning in public-sector and aviation procurement where information security is a formal criterion.

Frogparking is a New Zealand-based vendor with a cloud-native platform for mid-size municipalities. Its sensor-agnostic model reduces the hardware lock-in associated with older architectures. Hectronic GmbH, headquartered in Germany, supplies parking meters, pay stations, and management software across Swiss, German, and wider European municipal markets. CAME Parkare, part of the Italian CAME Group, offers barrier gates, column barriers, loop detectors, and integrated parking management software for commercial and mixed-use deployments.

Cleverciti Systems has built a distinct position through aerial sensor technology. Its overhead camera pods monitor multiple parking spaces without requiring ground-level sensor installation, lowering civil works requirements for on-street guidance deployments. Flowbird supplies cloud-managed pay station networks, mobile payment tools, and municipal parking systems across Europe, North America, and Australia. Arrive and Conduent Transportation add further competitive breadth through mobility, payments, and transportation service capabilities, particularly where parking is integrated with wider municipal transport operations.

3.1% market share

Collective Market Share in 2025 is 9.6%

Parking Management Industry News

Parking Management Market Concentration Score

The parking management market concentration score is 2 out of 10, because the top seven vendors held only 12.3% of global revenue in 2025 and the remaining 87.7% was spread across regional integrators, niche software providers, sensor specialists, payment platforms, and municipal service vendors.

The parking management market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Component

Market, By Solution

Market, By Parking Site

Market, By Deployment Mode

Market, By End User

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Mn)

Chapter 6 Market Estimates & Forecast, By Deployment Mode, 2022 - 2035 ($Mn)

Chapter 7 Market Estimates & Forecast, By Parking Site, 2022 - 2035 ($Mn)

Chapter 8 Market Estimates & Forecast, By Solution, 2022 - 2035 ($Mn)

Chapter 9 Market Estimates & Forecast, By End User, 2022 - 2035 ($Mn)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →