Summary

Table of Content

Organic Food Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Organic Food Market Size

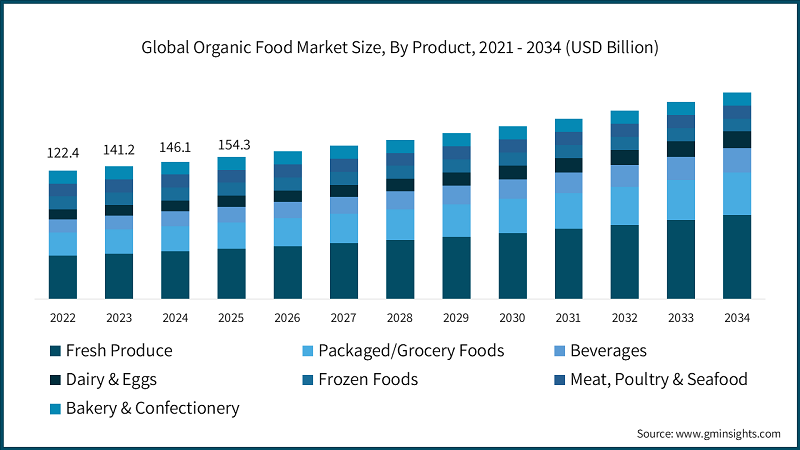

The organic food market was valued at USD 154.3 billion in 2024 and is expected to grow from USD 168.2 billion in 2025 to USD 364.4 billion in 2034, at a 9% CAGR, according to latest report published by Global Market Insights Inc.

Organic Food Market Key Takeaways

Market Size & Growth

- 2024 Market Size: USD 154.3 Billion

- 2025 Market Size: USD 168.2 Billion

- 2034 Forecast Market Size: USD 364.4 Billion

- CAGR (2025–2034): 9%

Key Market Drivers

- Health-led adoption underpins steady repeat purchases in the organic food market.

- Policy and certification support expands supply and reduces price gaps in the organic food industry.

- Environmental values align with organic methods, strengthening retention in the market.

Challenges

- Higher production costs constrain conversion; scale and agronomy support can mitigate in the market.

Opportunity

- Seasonal and logistics constraints limit availability; cold-chain and co-packing expand reach in the market.

Key Players

- Market Leader: Whole Foods Market Inc led with over 15% market share in 2024.

Get Market Insights & Growth Opportunities

- Health awareness consumers visit the organic food market. Organic purchases have risen in the U.S. by about 76% to adults eating organic food for only health purposes, indicating that this trend has become more important when it comes to health and wellness in consumer choices. With this trend among consumers likely to continue to drive increased demand for organic foods, it is also contributing to the market growth, primarily among those consumers who want to avoid artificial additives, pesticides, and genetically modified organisms. This has not only affected what consumers purchase but has further influenced producers to innovate and include a wider array of organic varieties.

- Buying behaviors are slowly swaying under increasing environmental awareness, becoming another reason why consumers demand organic and sustainable agricultural practices. The public has become aware of what is happening with soil degradation, and carbon emissions that are building up. Organic farming is perceived as an health substitute which encourages the growth of healthy soils, besides being pollution free and conserving the water. This thing is dragging consumers to organic products thus, liquifying the market and pushing farmers towards greener reforms.

- The government initiatives and certification programs have indeed rendered a significant impact in promoting organic food industry expansion. Examples include the USDA's USD 281 billion Organic Transition Initiative, which is expected to help pay and bring incentives to farmers converting their farming styles to organic methods. Certification schemes ensure the authenticity of products and enhance consumer trust, thus increasing demand. These government efforts account for approximately 50% of market growth, which indicates the importance of the measures that could encourage organic farming practices and expand this industry. When this is combined, it creates an enabling environment for the growth of the organic food sector.

To get key market trends

Organic Food Market Trends

- Clean-Label and Minimally Processed Demand- Consumers are zeroing in on ingredients and processing methods, rewarding brands that keep formulations simple and transparent in the market. Breaking it down, fresh organic produce remains the largest category in the U.S. at USD 21.5 billion in 2024, supported by shoppers who prefer foods closer to their natural state in the organic food market. Clean labels earn repeat purchases and justify moderate premiums, especially when sourcing stories are verifiable in the market. Millennials and Gen Z who show 36% higher preference for organic and value-based eating become primary household decision-makers in the market.

- Plant-Based and Vegan Organic Integration- The intersection of organic and plant-based is pulling new users into beverages, proteins, and functional foods within the market. Consider organic dairy alternatives, which rose 13.5% in 2024 to about USD 850 billion, reflecting improved taste profiles and broader distribution in the organic food market. Dual-positioned products carry health and sustainability benefits that resonate with younger consumers, especially in urban markets where trial is easy.

- Digital Commerce and Direct-to-Consumer Platforms- Subscription boxes, farm-direct models, and specialty e-commerce are now embedded in the go-to-market playbook for the market. The numbers tell us DTC channels are compounding at roughly 12.2% per year, outpacing traditional retail, and expanding access to premium assortments in the market.

Organic Food Market Analysis

Learn more about the key segments shaping this market

The fresh produce segment held approximately 37% of the market share in 2024. This figure is largely supported by an 8.7% CAGR in the forecasted period and visibility quality cues for the consumer. The packaged and grocery foods are pegged at almost 24.1% market share in 2024 and estimated to achieve 7.9% CAGR following the adoption of clean-label formulations, sustainable packaging, and private-label penetration. Then there is the burgeoning beverages category, almost 15.5% market share, and posting the fastest mix of growth levers by nearly 10.8% CAGR in the forecast period.

Fresh produce benefits from the incentive of habitual purchasing with well-understood health benefits, while packaged foods ride on the convenience and pantry-stocking patterns in organic food consumers. Clear sourcing and minimal processing create repeat purchases, especially where residue concerns are significant. Beverages have the most rapid cycles of innovation in the areas of functional ingredients and flavor, brand advantages that have more weight than price alone in the organic food market ota.com. As private-label assortments widen, branded players use taste, format variety, and traceability storytelling to maintain customer stickiness.

Learn more about the key segments shaping this market

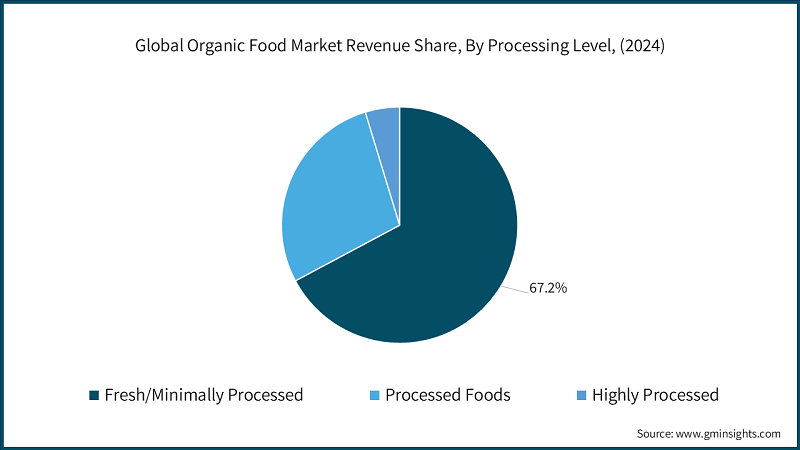

Around 67.2% of sales in organic formats are minimally processed and strongly reflect clean-label preferences in the organic food industry. Processed foods account for 28.1% market share in 2024 and is estimated to register at a 8.9% CAGR from 2025-2034, balancing the efficiency in certified markets of organic foods. Highly processed types of organic formats remain small at about 4.7% market share in 2024 and is likely to register about 9.3% CAGR through 2034 as supplements, protein powders, and functional items grow in special channels in the organic food market. Compared to conventional categories, you would find a stronger premium tolerance where the processing is restricted, and provenance is clear.

In a nutshell, fresh and minimally processed commodities benefited from shorter value chains and easy certification while processed products had costs and complexities that could broaden the tenders of higher price gaps in the market. However, innovation in better-for-you snacks and frozen meals keeps convenience alive in the living space, especially for dual-income households. Brands that can deliver short ingredients, verifiable claims, and tight pricing will drive repeat purchase behavior even as competition gets tighter in the organic market.

Looking for region specific data?

- The U.S. organic food market reached USD 57.8 billion in 2024 and estimated to reach USD 127.4 billion by 2034. North America leads with around 47.4% market share in 2024 anchored on the adoption of the mature category by the U.S. market. Traffic into the U.S. market is expected to grow to about USD 71.6 billion in 2024, which is almost 6% of total food sales and indicates slow but steady mainstreaming throughout aisles. Though small, Canada's increasing organic acreage and strength in grain and oilseed exports will contribute to a more balanced regional supply in the market. Retailers have been increasing the number of private label organics as they keep entry prices in check and broaden household penetration within the organic food market.

- Europe has approximately 40.2% market share in 2024 with expected CAGR of around 7.8% in the forecasted period spurred mainly by Germany, France, and the United Kingdom. Backed up by EU policy support governing national allocations under the Third Action Plan concerning Organic Farming, the supply development and consumer trust in the market are reinforced. Leading in regional consumption are Germany, the country that has stable retail, and one that is on the rise in breadth of category within the organic food market among France and the UK. Part of the national allocations under the Third Action Plan are multibillion euro commitments in Italy and Germany, which act as bolstering conversion incentives.

- Fastest growing region in Asia Pacific, by about 12.1% CAGR in the forecasted period off a small base, it's growing near 10% market share in 2025. Urbanization, emerging incomes and food-safety awareness cause this organic status in the market. The sales of the China organic food industry stay near USD 11.3 billion in 2024, conditions indicating large headroom as retail access improves. Interest quickly rises in India's middle class consumers, starting with staples and baby foods first, and then into higher-value categories in the market. The region's momentum is expected to continue with maturing certification systems and scaling distribution of localized brands.

Organic Food Market Share

The organic food industry is moderately concentrated, the top 5 players in the market are Whole Foods Market, Cliff Bar & Company, Danone, Unilever, and Nestlé, the top five players sharing a collective 55% of the market and leading with Whole Foods Market Inc. at around 15% for 2024. The extent of concentration makes it possible to achieve economies of scale in sourcing, logistics, and certification management while leaving some room for midsized specialists and fast-moving insurgents. Consequently, this makes competitive intensity manifest in two forms, the price-accessible private labels that expand the base and the premium-positioned brands that monetize differentiation in the organic food market.

Among the strategies, vertical integration, long-term grower contracts, and retail media are used by leaders to fine-tune demand planning and inventory turns in the market. The real winner here when dealing with farm practices and residue management wins most of the repeat purchases in this category, which has proved challenging for customers who switch to other categories. Players like Danone, Unilever, and Nestle; they scale up organic offering through their economies of procurement and research and development and through portfolio management, mainstream with a sustainability narrative in the organic food market. Authenticity, focus on category, and direct relationships with farmers all contribute to maintaining loyalty in the market for specialized brands such as Organic Valley, Amy's Kitchen, and Clif Bar.

As merger and acquisition activity proceeds, organic brands are among the many being snapped up by major food companies to add to their portfolios and increase distribution, while many established organic players are pursuing strategic alliances in scaling up production and stabilizing ingredient supply for processing in the organic foods market.

Organic Food Market Companies

Major players operating in the organic food industry are:

- Whole Foods Market

- Clif Bar & Company

- Danone

- Unilever

- Nestlé

- Organic Valley

- Amy's Kitchen

- General Mills

- The Kroger

- Eden Foods

- Nature's Path Foods

- Stonyfield Farm

- Earthbound Farm

- Whole Foods Market Inc

Whole Foods Market Inc. is creating visibility and depth of assortment in categories through certified sourcing standards and merchandising to shape trial and repeat across fresh, grocery, and beverages in the organic food market. Organic brands like Cascadian Farm and Annie's complete the portfolio. These brands make an organic house pay off with mass distribution tied into big capabilities empowering retail partnerships across the organic foods market. The Kroger Co. extends its footprint through the house organics that meet specifications, enabling access to the price-sensitive shopper and keeping the organic goods everyday simple.

- Danone S.A.

Danone S.A hold all their organic portfolios across categories and link these to sustainability initiatives with product innovation to lure growth in dairy, beverages, and packaged foods in the market. Organic Valley presents itself as the principal organic farmer cooperative in North America, comprising over 1,800 farms in dairy, eggs, produce, and meat, having a model aimed at stabilizing prices and upholding an authentic practice in organic food. Amy's Kitchen Inc. is involved in organic frozen meals, soups, and convenience food, matching vertical control with innovation in plant-forward recipes to the time-pressed shopper in the organic food market.

- Clif Bar & Company

Clif Bar & Company continues scaling up organic energy formats and protein-forward offerings into outdoor, athletic, and wellness community channels in the market. Company build consumer loyalty through category expertise coupled with sustainability commitments that resonate with organic buyers values within the organic food market. Cliff bar & Companys builds brand equity in organic fresh produce and continuously applies qualitative standards to ensure reliability in the supply chain to maintain retailer trust and support shelf continuity from this market.

- Unilever

Unilever is an international player in the consumer goods trade, occupying a large, diversified market where it has different foods, beverages, beauty, and personal care brands. In the organic food sector, Unilever focuses on sustainability in sourcing, health-oriented products, and innovation, which the customer wants more and more of it. Unilever has pledged to leave a reduced environmental footprint by improving the number of organic and eco-friendly products in its ecosystem. Unilever holds a vast global footprint; thus, it utilizes a wide range of distribution channels for promoting organic food products across varied markets.

- Nestle

Nestlé is the key player in the worldwide Food and Beverages' casinos, famous for an array of product lines, from dairy to coffee, snacks, and health sciences. Nestlé is increasingly focused on being organic with healthier and natural food and beverages, in line with the consumer market's rising awareness about wellness and sustainability. Nestlé is quite heavily invested in research and development, trying hard to innovate organic products and maintain good quality standards. With its international operating capacity, foods and beverages sold under Nestlé are, in large scale, organic products, in support of its mission to promote a better quality of life through nutrition.

Organic Food Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 154.3 Billion |

| Market Size in 2025 | USD 168.2 Billion |

| Forecast Period 2025-2034 CAGR | 9% |

| Market Size in 2034 | USD 364.4 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Health-led adoption underpins steady repeat purchases in the organic food market | Increasing health-conscious consumer preferences drive repeat purchases of organic foods. |

| Policy and certification support expands supply and reduces price gaps in the organic food industry | Regulatory frameworks and certifications help expand supply and reduce price disparities. |

| Environmental values align with organic methods, strengthening retention in the market | Consumers environmental concerns reinforce loyalty to organic farming methods. |

| Pitfalls & Challenges | Impact |

| Higher production costs constrain conversion; scale and agronomy support can mitigate in the market | Higher production costs hinder large-scale conversion without adequate support and resources. |

| Opportunities: | Impact |

| Seasonal and logistics constraints limit availability; cold-chain and co-packing expand reach in the market | Seasonal and logistical challenges can be addressed through cold-chain solutions and co-packing to broaden market reach. |

| Market Leaders (2024) | |

| Market Leader |

15% market share |

| Top 5 Players |

Collective market share in 2024 is 55% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | North America |

| Fastest growing market | Asia Pacific |

| Emerging countries | China, Japan, India |

| Future outlook |

|

What are the growth opportunities in this market?

Organic Food Industry News

- In June 2025, Kroger declared the launching of a new high-protein private label product line catering to the consumer demand for healthier alternatives. This endeavor intends to further advance Kroger's offerings into the booming health and wellness category. The new products will come in exciting new packaging and a plethora of protein-rich choices in various categories. This step illustrates Kroger's commitment towards health-conscious shoppers and solidifying its market presence further.

In June 2025, LT Foods announced the opening of its new organic food facility in Rotterdam to strengthen its global supply chain. The plant has been developed to enhance the production of premium organic products to cater to the growing demands of European customers. This demonstrates LT Foods' zeal for making a name in organic produce and for versatility as consumer lives become more saturated with demand for nutritious sustainable foods. This gives the company continued competitive advantage towards innovation and international growth in the organic food sector.

The organic food market research report includes in-depth coverage of the industry, with estimates & forecast in terms of revenue (USD Billion) and volume (Kilo Tons) from 2021 to 2034, for the following segments:

Market, By Product Category

- Fresh produce

- Organic fruits

- Organic vegetables

- Organic herbs & spices

- Dairy & eggs

- Organic milk products

- Organic cheese & fermented dairy

- Organic egg products

- Alternative dairy products

- Meat, poultry & seafood

- Organic beef & pork

- Organic poultry

- Organic seafood & aquaculture

- Packaged/grocery foods

- Organic canned & preserved foods

- Organic dry goods & pantry staples

- Organic snacks & convenience foods

- Organic oils & vinegars

- Beverages

- Organic juices & smoothies

- Organic coffee & tea

- Organic alcoholic beverages

- Functional & health beverages

- Frozen foods

- Organic frozen vegetables & fruits

- Organic frozen meals & entrees

- Organic frozen desserts

- Bakery & confectionery

- Organic baked goods

- Organic confectionery & sweets

- Artisanal & specialty products

Market, By Processing Level

- Fresh/minimally processed

- Processed foods

- Highly processed

Market, By Distribution Channel

- Supermarkets & grocery stores

- Specialty food stores

- Food service channel

- Direct-to-consumer channel

- Wholesale distribution

Market, By End Use Industry

- Food retail industry

- Food service industry

- Food processing industry

- Institutional sector

- Others

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia Pacific

- Latin America

- Brazil

- Mexico

- Argentina

- Rest of Latin America

- Middle East & Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of Middle East & Africa

Frequently Asked Question(FAQ) :

What is the market size of the organic food market in 2024?

The market size was USD 154.3 billion in 2024, with a CAGR of 9% expected through 2034, driven by rising health-conscious consumer preferences.

What is the projected value of the organic food market by 2034?

The organic food market is expected to reach USD 364.4 billion by 2034, propelled by health awareness, environmental concerns, and expanding distribution channels.

What is the current organic food market size in 2025?

The market size is projected to reach USD 168.2 billion in 2025.

How much revenue did the fresh produce segment generate in 2024?

The fresh produce segment accounting for approximately 37% of the market share in 2024.

What was the valuation of the packaged and grocery foods segment in 2024?

The packaged and grocery foods segment held a 24.1% market share in 2024.

What is the growth outlook for beverages in the organic food market from 2025 to 2034?

The beverages segment is projected to grow at a 10.8% CAGR through 2034, driven by innovation in functional ingredients and flavors.

Which region leads the organic food market?

The U.S. organic food market reached USD 57.8 billion in 2024 and is projected to reach USD 127.4 billion by 2034.

What are the upcoming trends in the organic food market?

Key trends include clean-label demand, plant-based and vegan organic integration, and the rise of digital commerce and direct-to-consumer platforms.

Who are the key players in the organic food market?

Key players include Whole Foods Market, Clif Bar & Company, Danone, Unilever, Nestlé, Organic Valley, Amy's Kitchen, General Mills, The Kroger, Eden Foods, Nature's Path Foods, Stonyfield Farm, and Earthbound Farm.

Organic Food Market Scope

Related Reports