Authors:

Monali Tayade, Jignesh Rawal

Download free PDF

Knee Braces Market Size & Share 2026-2035

Report ID: GMI4238

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Knee Braces Market

Get a free sample of this report

Get a free sample of this report Knee Braces Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Knee Braces Market Size

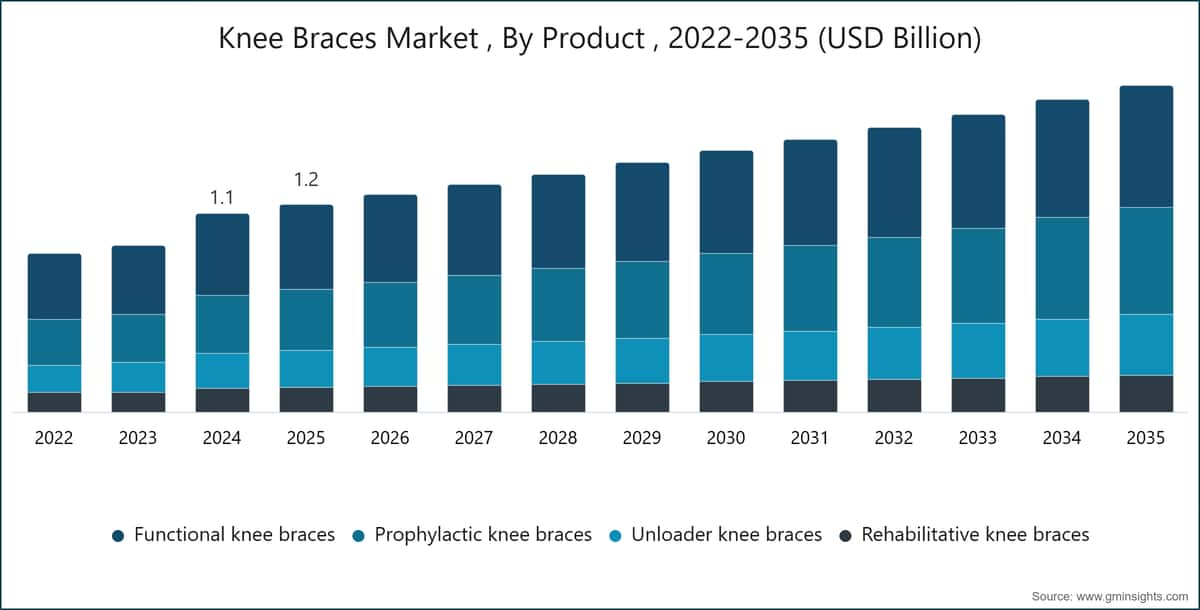

The global knee braces market was estimated at USD 1.15 billion in 2025. The market is expected to grow from USD 1.21 billion in 2026 to USD 1.81 billion in 2035, at a CAGR of 4.6% during the forecast period, according to the latest report published by Global Market Insights Inc.

Knee Braces Market Key Takeaways

Market Leader: enovis led with over 22% market share in 2025.

Leading Players: Top 5 players in this market include enovis, BAUERFEIND, OSSUR, BREG, Ottobock, which collectively held a market share of 37% in 2025.

The market is driven by numerous factors, such as the surging prevalence of osteoarthritis and orthopedic conditions, and the rising number of road accidents and sport-related injuries, among other factors.

A knee brace is a type of medical device that has been designed to offer support, protection, and stabilization to the knee joint. Knee braces are meant to be preventive of injury, assist during the recovery phase after an injury or surgical procedure, and help manage chronic conditions such as osteoarthritis.

Increasing geriatric population prone to knee ailments is expected to fuel the industry's growth. enovis, BAUERFEIND, OSSUR, BREG, and Ottobock are among the leading players operating in the market. These players mainly focus on product innovation, geographic expansion, research and development, and collaboration with local or regional healthcare providers, among other factors.

The market has increased from USD 879.2 million in 2022 and reached USD 1.1 billion in 2024, with a historic growth rate of 12%. The surging prevalence of osteoarthritis and other orthopedic knee conditions is emerging as a major growth driver for the market, significantly increasing long-term demand for non-invasive treatment solutions. Factors such as aging populations, sedentary lifestyles, and rising participation in high-impact sports have contributed to a sharp increase in joint-related disorders, particularly in the knee. Osteoarthritis, one of the most common degenerative joint conditions, is a leading cause of chronic pain and mobility limitations. According to a study published in the medRxiv Journal, osteoarthritis affected approximately 607 million people globally in 2021, highlighting the substantial disease burden and its impact on healthcare systems. Alongside this, sports-related knee injuries, including ligament tears and meniscus damage, are also rising among both professional athletes and recreational users. These conditions are driving sustained demand for knee braces as a cost-effective, non-surgical solution for pain management, joint stabilization, and rehabilitation, enabling improved mobility while reducing the need for surgical intervention and long-term healthcare costs.

Additionally, the rising incidence of road traffic accidents and sports-related injuries is significantly contributing to the expansion of the market, driven by the increasing burden of acute musculoskeletal trauma and joint instability among global populations. Road traffic injuries remain a major public health concern, with the World Health Organization (2025) reporting that approximately 1.19 million people die annually, while 20 to 50 million individuals sustain non-fatal injuries, many involving lower-limb trauma such as ligament tears, fractures, and joint damage. Notably, a significant proportion of these injuries occur among vulnerable road users, including pedestrians, cyclists, and motorcyclists, further increasing the incidence of knee-related conditions. Furthermore, growing participation in both professional and recreational sports is leading to a higher frequency of injuries such as anterior cruciate ligament (ACL) tears, meniscus damage, and joint sprains. Collectively, these trends are driving increased adoption of knee braces for injury stabilization, rehabilitation support, and prevention of further damage, thereby contributing to sustained demand and long-term growth in the market.

Knee Braces Market Trends

Technological advancements in knee brace design and orthopedic support systems play a significant role in driving market growth by improving product effectiveness, patient comfort, and clinical outcomes, while supporting better injury management and rehabilitation.

Knee Braces Market Analysis

Based on product, the market is segmented into functional knee braces, prophylactic knee braces, unloader knee braces, and rehabilitative knee braces. The functional knee braces segment accounted for a dominant market share of 40.8% in 2025, driven by its widespread use in providing stability and controlled mobility for patients with ligament injuries and joint instability. The segment is expected to reach USD 680.9 million by 2035, growing at a CAGR of 3.7% during the forecast period.

Based on application, the knee braces market is segmented into sports use, ligament, and other applications. The sports use segment dominates the market with a revenue of around USD 517.1 million in 2025.

Based on end use, the knee braces market is segmented into hospitals, orthopedic clinics, and other end users. The hospitals segment dominates the market with a revenue of around USD 492.5 million in 2025.

North America Knee Braces Market

The North America market accounted for a majority share of 38.5% in 2025 and is anticipated to show notable growth over the forecast period.

Europe Knee Braces Market

Europe accounted for a significant share of the market and was valued at USD 304.2 million in 2025.

Asia Pacific Knee Braces Market

The Asia Pacific market accounted for a substantial share of the market and was valued at USD 303.3 million in 2025.

Latin America Knee Braces Market

The Latin America market is anticipated to exhibit remarkable growth during the analysis period.

Middle East and Africa Knee Braces Market

The Middle East and Africa market is expected to experience substantial growth over the analysis timeframe.

Market share ~22%

Collective market share of top 5 players is ~37%

Knee Braces Market Share

Knee Braces Market Companies

A few of the prominent players operating in the global knee braces industry include:

enovis is a global leader in orthopedic solutions with a USP centered on innovation in bracing and rehabilitation technologies. Its strength lies in a comprehensive portfolio of functional, prophylactic, and rehabilitative knee braces designed for sports medicine and post-surgical recovery. enovis differentiates itself through advanced hinge systems, lightweight composite materials, and customizable fit technologies that enhance patient comfort and compliance.

BAUERFEIND stands out for its USP of premium-quality orthopedic braces and support products, backed by decades of German engineering excellence. Its knee braces are recognized for ergonomic designs, superior comfort, and medical-grade materials, making them a preferred choice for both clinical and sports applications. BAUERFEIND’s competitive edge lies in its commitment to precision fit, durability, and patient-centric solutions, supported by continuous R&D and collaborations with healthcare professionals.

OSSUR’s USP is built on innovation in mobility and functional bracing solutions, with a strong focus on osteoarthritis management and sports injury prevention. The company excels in proprietary hinge systems, lightweight designs, and smart bracing technologies that integrate sensor-based monitoring for real-time rehabilitation feedback. OSSUR’s emphasis on digital health, customization, and evidence-based product development ensures superior clinical outcomes and patient satisfaction.

Knee Braces Industry News:

The knee braces market research report includes an in-depth coverage of the industry with estimates and forecasts in terms of revenue in (USD Million) from 2022 - 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Product

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Research Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Product, 2022 - 2035 ($ Mn)

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 ($ Mn)

Chapter 7 Market Estimates and Forecast, By End Use, 2022 - 2035 ($ Mn)

Chapter 8 Market Estimates and Forecast, By Region, 2022 - 2035 ($ Mn)

Chapter 9 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →