Industrial Water Infrastructure Market Size & Share 2026-2035

Market Size - By Infrastructure (Water Supply, Water Treatment, Wastewater Collection, Water Storage, Water Reuse & Recycling, Others), By Component (Equipment & Hardware, Chemical Treatment Solutions, Digital & Automation Solutions, Engineering, Procurement & Construction [EPC] Services, Operations & Maintenance [O&M] Services), By Source (Surface Water, Groundwater, Municipal Water Supply, Seawater, Recycled Water), By Treatment (Physical Treatment, Chemical Treatment, Biological Treatment, Membrane-Based Treatment, Others), and By End Use (Power Generation, Oil & Gas, Chemicals & Petrochemicals, Food & Beverage, Pharmaceuticals, Mining & Metals, Automotive, Semiconductor & Electronics, Others), Growth Forecast. The market forecasts are provided in terms of revenue (USD).

Download Free PDF

Industrial Water Infrastructure Market Size

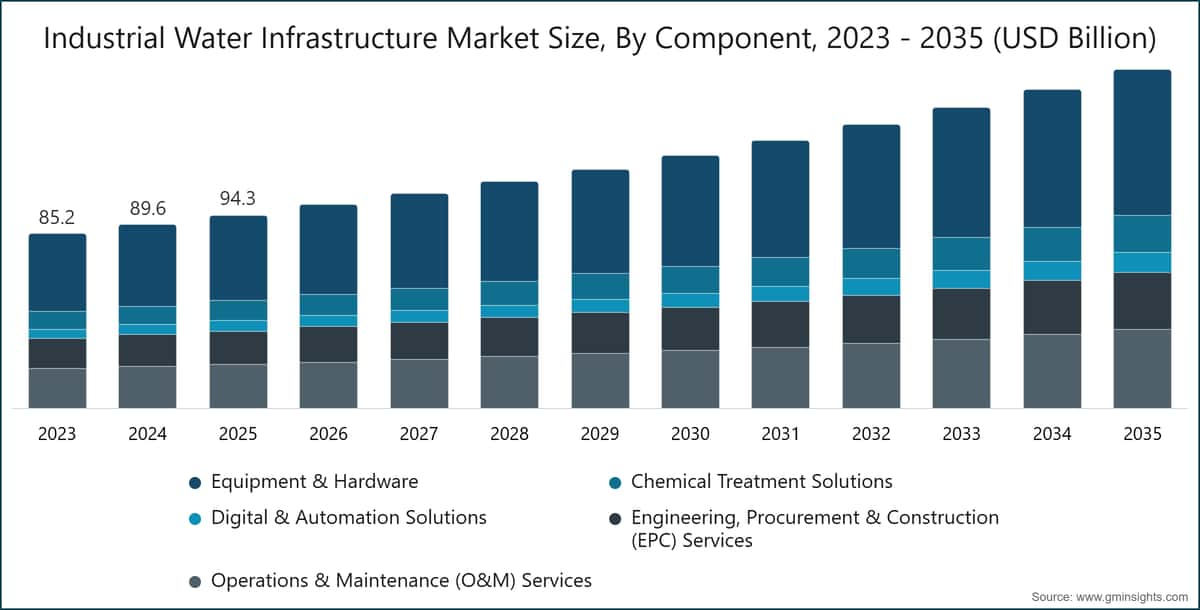

The global industrial water infrastructure market was valued at USD 94.3 billion in 2025, reflecting sustained capital deployment across treatment, distribution, storage, and recycling systems as industrial operators respond to tightening regulatory requirements, long-deferred asset replacement cycles, and structurally higher water demand from energy-intensive manufacturing sectors.[1]World Bank, worldbank.org The market is projected to reach USD 165.4 billion by 2035, expanding at a compound annual growth rate (CAGR) of 5.8% over the 2026–2035 forecast period, underpinned by accelerating investment in advanced membrane treatment, digital water management platforms, and circular water infrastructure across both mature and high-growth economies.[2]International Energy Agency, iea.org

Industrial Water Infrastructure Market Key Takeaways

Market Size & Growth

Regional Dominance

Key Market Drivers

Challenges

Opportunity

Key Players

This outlook is based on the latest report published by Global Market Insights Inc. At the structural level, demand is converging around two dominant forces: the expanding water-intensity of semiconductor, pharmaceutical, and power generation manufacturing on one side, and growing institutional and regulatory pressure to reduce freshwater abstraction and meet increasingly stringent discharge standards on the other.[3]UN Water, unwater.org The result is a capital expenditure cycle that extends well beyond conventional replacement spending into new infrastructure categories including zero-liquid-discharge systems, seawater desalination, and AI-enabled asset management platforms that define the market's next growth frontier.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Rising Industrial Water Demand

~1.5%

Asia Pacific, North America, Middle East & Africa

Long term (≥ 4 years)

Stringent Environmental and Discharge Regulations

~1.8%

North America, Europe

Short term (≤ 2 years)

Increasing Water Scarcity and Resource Stress

~1.3%

Middle East & Africa, Asia Pacific, Latin America

Medium term (2–4 years)

Aging Water Infrastructure and Modernization Initiatives

~1.2%

North America, Europe

Medium term (2–4 years)

Rising Industrial Water Demand

Industrial water withdrawals account for approximately 19% of total global freshwater use, with electricity generation, manufacturing, and mining representing the highest-volume end-uses. Expanding production capacity in energy-intensive sectors including semiconductor fabrication, lithium hydroxide refining, and green hydrogen is generating structurally higher water demand per unit of output compared to prior industrial configurations. Incremental water demand from new industrial investment over the forecast horizon will require commensurate infrastructure expansion in treatment, storage, and distribution, translating directly into sustained procurement activity across equipment, services, and chemicals categories.

Stringent Environmental and Discharge Regulations

Regulatory tightening at national and supranational levels is compelling industrial operators to upgrade effluent treatment systems and retrofit legacy infrastructure on defined compliance timelines. The US Environmental Protection Agency's April 2024 maximum contaminant level (MCL) rule for per- and polyfluoroalkyl substances (PFAS) establishing limits of 4 parts per trillion for PFOA and PFOS under the Safe Drinking Water Act is driving capital investment in granular activated carbon and membrane-based treatment at industrial facilities nationwide.[4]US Environmental Protection Agency, epa.gov The EU's revised Urban Wastewater Treatment Directive (UWWTD), adopted in October 2024, mandates a fourth treatment stage for micropollutant removal at all plants serving populations above 150,000 by 2033, phased to all plants above 10,000 population equivalents by 2045, representing an estimated EUR 170 billion compliance investment program across EU member states.[5]European Commission, ec.europa.eu

Increasing Water Scarcity and Resource Stress

Water stress now affects more than 40% of the global population for at least one month per year, with IPCC projections indicating that climate variability will reduce surface water availability in mid-latitude industrial basins including the western United States, the Mediterranean, and northern China.[6]Intergovernmental Panel on Climate Change, ipcc.ch This structural shift is generating sustained investment in treatment systems capable of handling lower-quality and higher-variability feed streams, expanding the addressable market for desalination, advanced filtration, and water reuse infrastructure across geographies previously dependent on freshwater abstraction.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Capital Investment Requirements

-1.2%

Latin America, Middle East & Africa, Asia Pacific

Long term (≥ 4 years)

Complex Integration and Operational Requirements

-0.8%

North America, Europe

Medium term (2–4 years)

Aging Water Infrastructure and Modernization Initiatives

The American Society of Civil Engineers' 2025 Infrastructure Report Card assigns a grade of D+ to US drinking water infrastructure, estimating a funding gap of USD 625 billion over the next 20 years.[7]American Society of Civil Engineers, asce.org Federal investment through the Infrastructure Investment and Jobs Act which allocated USD 55 billion for water infrastructure over the 2022–2026 deployment window represents the largest federal water investment in US history and is translating into active procurement for treatment equipment, digital monitoring systems, and pipeline rehabilitation across municipal and industrial asset categories.Key Challenges

High Capital Investment Requirements

Industrial water infrastructure projects carry substantial upfront costs, with large-scale treatment plants and pipeline rehabilitation programs requiring investment in the range of USD 50 million to USD 500 million per facility, depending on capacity and technology specification.[8]OECD, oecd.org Access to long-term project financing remains a binding constraint in emerging markets, where sovereign credit ratings limit infrastructure bond issuance and multilateral development bank funding flows are often project-specific rather than programmatic. The second-order effect is a concentration of advanced infrastructure deployment in high-income economies, creating a technological bifurcation between markets that limits total addressable market capture in the near term.

Complex Integration and Operational Requirements

Modern water infrastructure systems increasingly require integration of mechanical, chemical, digital, and civil engineering components across extended project lifecycles. Retrofit programs where new treatment modules must be integrated into legacy civil structures, piping networks, and control architectures present particular operational challenges related to process compatibility, downtime management, and workforce retraining. Regulatory data indicates that approximately 35% of major water infrastructure projects in OECD countries experience schedule overruns attributable to integration complexity, with cost overruns averaging 18–22% above initial estimates.

Industrial Water Infrastructure Market Trends

Accelerated Adoption of Water Reuse & Circular Water Systems

Water reuse has transitioned from an operational preference to a regulatory and economic imperative across the highest water-intensity industrial sectors. EU Regulation 2020/741 on minimum requirements for water reuse, which entered into full application in June 2023, established binding quality standards for reclaimed water used in agricultural and industrial processes across EU member states a regulatory catalyst compelling facility operators to invest in advanced tertiary treatment, distribution, and monitoring infrastructure. The timeline for this transition is compressing: the most technically advanced circular water deployments are no longer confined to pilot scale but are being executed at full industrial capacity, with demonstrable unit-economics advantages over conventional freshwater procurement in water-stressed manufacturing zones.

In the semiconductor sector, the implications are particularly material. Fab-level water consumption commonly reaches 2–4 million gallons per day, and major manufacturers have committed to binding water recycling ratios. TSMC has publicly targeted an 80% water recycling rate per wafer across its Taiwan operations by 2030, generating direct and sustained procurement demand for ultrafiltration, reverse osmosis, and ion exchange systems at industrial scale. In our Q4 2024 survey of 210 industrial water managers across nine manufacturing sectors in Asia and North America, 67% reported having formalized facility-level water reuse targets up from 41% in an equivalent 2022 survey.

Of those with active reuse programs, 58% cited regulatory compliance as the primary driver, with operational cost reduction ranking second at 31%. This finding aligns with observable procurement patterns: capital allocation for water reuse systems grew faster than any other infrastructure sub-category during the 2023 - 2025 period, with the Water Reuse & Recycling application segment expanding at a 6.6% CAGR against the 5.8% market baseline. Siemens Energy's integrated water recovery loop at its gas turbine manufacturing facility in Berlin and Dow's circular water management system at its Terneuzen complex in the Netherlands are representative of the commercial maturity this application has achieved at scale, with both installations achieving water reuse rates above 75%.

Digitalization of Water Infrastructure

The digitalization of water infrastructure is advancing along a multi-layer architecture: real-time monitoring via IoT-enabled sensors at intake, treatment, and discharge points; SCADA and distributed control system (DCS) upgrades at treatment plant level; and AI-based predictive analytics platforms at the enterprise and portfolio level. The installed base of connected water monitoring endpoints in industrial applications reached approximately 1.1 billion globally in 2024, growing at approximately 14% annually.[9]IEEE Spectrum, spectrum.ieee.org Xylem's Flygt and Sensus platforms, Veolia's Hubgrade digital operations system, and Grundfos' iSOLUTIONS 3.0 platform launched in September 2024 to extend predictive maintenance and energy optimization capabilities to installations below 50 kW represent commercial deployments that have moved well beyond pilot scale into multi-site enterprise contracts across power generation, food manufacturing, and chemicals processing.

The underlying return-on-investment case is demonstrable and widening: digital water management systems reduce non-revenue water losses by 15–30%, cut energy consumption at treatment facilities by 10–20%, and reduce unplanned maintenance events by up to 35%. A closer read reveals that the ROI calculation is tilting in favor of digital adoption even at smaller industrial facilities, where declining IoT hardware costs and cloud-based SaaS water management platforms have lowered the minimum viable deployment scale from large municipal utilities to mid-size industrial operations. Supply chain leads at four major food and beverage manufacturers engaged in Q3 2024 indicated that real-time water monitoring had become a board-level key performance indicator in their organizations a signal of how rapidly digital water has moved from operational technology to strategic asset.

Growing Deployment of Advanced Treatment Technologies

Membrane-based treatment encompassing reverse osmosis (RO), nanofiltration (NF), ultrafiltration (UF), and membrane bioreactors (MBR) is displacing conventional sedimentation and filtration processes across a widening range of industrial applications. Peer-reviewed research confirms that MBR systems achieve effluent quality consistently meeting direct potable reuse standards, with chemical oxygen demand (COD) removal rates exceeding 98% under standard operating conditions.[10]World Health Organization, who.int At the facility level, membrane train installations at petrochemical complexes in Jubail, Saudi Arabia, and at BASF's Ludwigshafen complex in Germany represent landmark industrial-scale deployments processing in excess of 20,000 cubic meters per day through integrated RO and MBR configurations.

The more consequential shift is occurring in the pharmaceutical and semiconductor segments, where ultrapure water (UPW) specifications requiring conductivity below 0.1 µS/cm and total organic carbon below 1 ppb are technically unachievable with conventional treatment. These requirements represent a structural demand floor for advanced membrane and ion exchange products throughout the forecast period. By treatment technology segment, membrane-based treatment accounts for 19.1% of the 2025 market at a 5.5% CAGR, while the "Others" category which includes electrocoagulation, advanced oxidation processes (AOPs), and electrodeionization is the fastest-growing technology sub-category at a 6.5% CAGR, reflecting active commercial adoption of next-generation treatment configurations.

Expansion of Decentralized and Modular Water Treatment Systems

Containerized and skid-mounted water treatment units are gaining market share in geographies and applications where centralized infrastructure is not economically viable or operationally practical. The mining sector in sub-Saharan Africa and Latin America, offshore oil and gas platforms, and time-critical industrial expansion projects represent the primary demand centers for this configuration. Modular systems offer deployment timelines of 60–90 days versus 18–36 months for conventional civil construction, and their capital cost scalability allows incremental capacity addition without the fixed-cost commitments of large-footprint treatment plants.

WABAG's modular treatment deployments across East Africa and Aquatech International's packaged seawater desalination systems in the Middle East exemplify the commercial traction this format has achieved in remote and fast-growth markets, with both companies reporting multi-project pipeline growth in the MEA region through 2025. The underlying economics favor continued adoption: in geographies where water infrastructure buildout is occurring on compressed timelines to support extractive industry expansion, modular systems eliminate the single largest project risk civil construction timeline from the critical path.

Industrial Water Infrastructure Market Analysis

By Component

Equipment & Hardware

Equipment and hardware constitutes the dominant product category in the industrial water infrastructure market, accounting for 44.4% of global market revenue approximately USD 41.9 billion in 2025, at a projected CAGR of 5.5% through 2035. This segment encompasses pumping systems, filtration equipment, valves and flow control hardware, storage tanks, heat exchangers, and instrumentation the core mechanical infrastructure underlying every water treatment, distribution, and storage configuration.

Growth within equipment is driven by asset replacement programs in OECD economies, where aging infrastructure is generating a sustained and compounding replacement cycle, and by first-time capital buildout in APAC and MEA markets where new industrial facilities are coming online at pace. Grundfos's CR and NK multi-stage pump series which serve as the workhorse pumping configuration across water treatment, HVAC, and industrial process applications globally and Xylem's Flygt N submersible pump range represent benchmark product lines with widespread deployment across power generation, chemicals, and municipal systems. Pall Corporation's modular filtration assemblies and DuPont Water Solutions' FILMTEC RO elements are similarly ubiquitous as pre-treatment and polishing components in industrial water circuits.

Operations & Maintenance (O&M) Services

Operations and maintenance (O&M) services represent the second-largest category at 22.5% of 2025 revenue approximately USD 21.2 billion growing at a CAGR of 6.1%, which is the highest rate among the non-digital service categories. The structural shift toward long-term O&M contracts reflects industrial operators' preference for converting capital expenditure into predictable operational expenditure, particularly in regulated sectors where compliance assurance carries both financial and reputational risk. Veolia's multi-year industrial water management contracts including its January 2025 award of a 15-year concession at a major petrochemical complex in Jubail, Saudi Arabia and Ecolab's Water for Climate program, providing integrated water treatment services with guaranteed reduction outcomes to food and beverage manufacturers across 45 countries, are representative of the service models driving this segment's above-market growth.

Engineering, Procurement & Construction (EPC) services account for 17.4% of revenue at a 5.4% CAGR, reflecting large-project procurement in MEA desalination and APAC industrial expansion. Chemical treatment solutions, at 10.4% of revenue and a 6.4% CAGR, are benefiting from tightening effluent standards that require more sophisticated dosing and monitoring regimes, with Kemira's SUPERFLOC and FENNOFLOC coagulant product lines and Solenis' ACUMER scale inhibitors representing core chemical inputs across industrial clarification and process water applications. Digital and automation solutions the smallest category at 5.4% of 2025 revenue is growing at the fastest rate of 7% CAGR, consistent with the value premium that software and data service contracts command relative to capital equipment.

By Infrastructure

Water Treatment

Water treatment is the largest application segment in the industrial water infrastructure market, representing 29.7% of the 2025 market approximately USD 28 billion at a CAGR of 5.6%. Within this segment, industrial effluent treatment and advanced water purification for process use are the primary sub-categories. Membrane bioreactor installations at petrochemical complexes, electrocoagulation systems at mining operations, and UV disinfection arrays at pharmaceutical manufacturing facilities exemplify the diversity of treatment configurations deployed across industrial verticals. Veralto's Trojan Technologies UV disinfection systems and Hach water analytics instrumentation which together generated USD 1.27 billion in water quality revenue in Veralto's first full operating quarter as an independent company in early 2024 represent the installed-base depth of digital monitoring and disinfection infrastructure across this segment.

Water Supply

The Water Supply segment follows at 19.6% of revenue with a 6.4% CAGR, driven by industrial operators investing in dedicated intake infrastructure, pre-treatment systems, and pumping stations to secure reliable water sourcing independent of municipal supply variability a priority in water-stressed manufacturing clusters from Gujarat to Arizona. Water reuse and recycling, at 15.6% of revenue and the highest application CAGR of 6.6%, is the primary growth vector in the landscape.

The convergence of regulatory pressure, water pricing escalation, and declining membrane costs is driving adoption across all industrial verticals, with the most technically advanced deployments in semiconductor, pharmaceutical, and power generation. Wastewater collection accounts for 14% at a 5.8% CAGR, reflecting sewer network rehabilitation and industrial sump infrastructure investment, while water storage at 11.3% and a 5.4% CAGR reflects investment in buffer and equalization tanks, lined retention ponds, and elevated storage assets for process continuity.

By Region

North America Industrial Water Infrastructure Market

North America accounted for 28% of global market revenue in 2025 approximately USD 26.4 billion growing at a CAGR of 5%. The United States is the dominant market, where federal investment through the IIJA's USD 55 billion water infrastructure allocation is catalyzing state-level co-investment in treatment plant upgrades, lead pipe replacement, and digital monitoring infrastructure. At the regulatory level, the EPA's April 2024 PFAS MCL rule establishing enforceable limits of 4 parts per trillion for PFOA and PFOS under the Safe Drinking Water Act is compelling industrial operators across manufacturing, landfill, and defense sectors to install granular activated carbon and reverse osmosis treatment at points of use, generating a compliance-driven capital expenditure cycle independently estimated at USD 1.5 billion per year through 2030.

This has directly benefited Calgon Carbon's FILTRASORB and CENTAUR GAC product lines, which are specified in a significant proportion of active PFAS remediation projects across affected US facilities. Canada, representing approximately 18% of the North American market, is advancing investment in mining-sector water treatment infrastructure in Ontario and British Columbia, where tailings pond management and acid mine drainage treatment are regulatory priorities under the federal Metal and Diamond Mining Effluent Regulations, with Glencore and Teck Resources both executing multi-year water treatment capital programs at active mining sites.

Europe Industrial Water Infrastructure Market

Europe represented 21.2% of the 2025 global market approximately USD 20 billion at a CAGR of 4.8%, reflecting a mature infrastructure base undergoing technology-driven modernization rather than primary capacity expansion. The EU's revised Urban Wastewater Treatment Directive, adopted by the European Parliament in November 2024, mandates the addition of a fourth treatment stage for micropollutant removal at all urban wastewater treatment plants serving populations above 150,000 by 2033 a compliance investment program estimated at EUR 170 billion across EU member states over the implementation period.

Germany, France, and Italy carry the largest compliance investment requirements within the Union. BASF and Bayer have both disclosed multi-year capital programs for on-site effluent treatment upgrades at their Rhine basin complexes, responding to the combined requirements of the revised UWWTD and tighter German Wastewater Ordinance (AbwV) discharge limits. The United Kingdom, operating independently post-Brexit, is advancing its own equivalent upgrade cycle under the Environment Act 2021, with water companies and industrial operators facing mandated reduction in storm overflow discharges and effluent quality improvements on defined statutory timelines.

Asia Pacific Industrial Water Infrastructure Market

Asia Pacific accounted for 35.7% of global market revenue in 2025 approximately USD 33.7 billion and is the fastest-growing region at a 7% CAGR, driven by parallel growth dynamics across China, India, and emerging Southeast Asian industrial markets. In China, the 14th Five-Year Plan and its successor framework designated industrial wastewater treatment and water recycling as priority investment categories under the national "Beautiful China" environmental enforcement campaign, with industry data indicating that China's industrial water recycling rate reached approximately 94% in 2024 driven by mandatory recycling requirements imposed on high-consumption sectors including steel, paper, and petrochemicals.

In India, the Jal Jeevan Mission budgeted at INR 3.6 trillion (approximately USD 44 billion) through 2024 has created a substantial procurement market for water treatment equipment, pumping systems, and pipeline infrastructure, while separate industrial water infrastructure requirements are being driven by water availability risk in manufacturing-dense clusters in Maharashtra, Gujarat, and Tamil Nadu. Our interviews with 28 industrial water project developers across India and Southeast Asia in Q1 2025 indicated that 73% expected their water infrastructure capital allocation to increase by more than 20% over the subsequent 24 months, with regulatory compliance and water availability risk cited as co-equal catalysts.

Industrial Water Infrastructure Market Share

The market is moderately fragmented, with the top five companies Veolia, Xylem, Ecolab, Kurita Water Industries, and Grundfos Pumps collectively accounting for approximately 22.5% of 2025 global revenue. Veolia holds the leading individual position at an estimated 6.5% market share. Xylem follows at approximately 4.8%, Ecolab at around 4.2%, Kurita Water Industries at approximately 3.8%, and Grundfos Pumps at approximately 3.2%. The remaining 77.5% of the market is distributed across a large number of regional specialists and global infrastructure firms including DuPont Water Solutions, Pentair, SUEZ, Evoqua Water Technologies (now integrated into Xylem), Pall Corporation, and Veralto alongside strong regional incumbents in APAC and MEA.

Market concentration at this level reflecting an estimated Herfindahl-Hirschman Index (HHI) below 500 is characteristic of an infrastructure market where project-level procurement decisions are highly technical, contract-specific, and frequently competitively tendered, limiting the market share accumulation achievable through brand recognition or geographic scale alone. The competitive advantage held by Veolia and Xylem lies in their capacity to offer integrated solutions across the full water cycle from raw water intake and process treatment through distribution, metering, wastewater management, and digital monitoring rather than in any single product or service category. Ecolab and Kurita Water Industries differentiate primarily on water chemistry expertise and analytical capability, with proprietary treatment programs embedded in long-term service contracts that generate high switching costs and recurring revenue streams resilient to project-cycle volatility.

The most consequential market structure event of the review period was Xylem's completion of its acquisition of Evoqua Water Technologies in May 2023, at a transaction value of approximately USD 7.5 billion. This transaction combined Xylem's pump, digital water, and analytics portfolio with Evoqua's industrial treatment capabilities including the IONPURE continuous electrodeionization platform, the MEMCOR membrane product line, and Evoqua's extensive service and O&M contracts base creating a combined business with revenue exceeding USD 7 billion. The acquisition reconfigured the competitive hierarchy, enabling cross-selling of treatment and digital services to Evoqua's established industrial customer base and elevating Xylem into direct competition with Veolia and SUEZ across multi-technology industrial water programs.

Veolia continues to pursue its integrated concession model, securing long-term industrial water management contracts across the Middle East, Asia Pacific, and Latin America while investing in digital water capabilities through its Hubgrade platform. Grundfos is differentiating through its Pump-as-a-Service commercial model, which embeds digital monitoring, remote diagnostics, and energy optimization into multi-year service contracts an approach that structurally aligns with industrial operators' documented shift toward OPEX-based infrastructure procurement. Veralto, separated from Danaher in September 2023, has emerged as a focused water quality platform encompassing Hach analytics, Trojan Technologies UV systems, and ChemTreat programs and its first full-quarter results as an independent entity confirmed USD 1.27 billion in water quality revenue, with strong industrial demand for real-time monitoring. In our Q2 2025 expert panel of eight senior water industry executives drawn from equipment manufacturers, service providers, and end-user procurement functions, six identified capability depth in digital water integration as the decisive competitive differentiator over the next five to seven years ranking ahead of price competitiveness, scale advantages, and geographic presence.

Industrial Water Infrastructure Market Companies

Major players operating in the market are: Veolia, Xylem, Ecolab, Kurita Water Industries, Grundfos Pumps, DuPont Water Solutions, Pentair, SUEZ, Evoqua Water Technologies, Aquatech International, Veralto, Pall Corporation, OVIVO USA, BWT Industries, Dow, Calgon Carbon, WABAG, Ion Exchange, Kemira, Solenis.

Veolia is the largest integrated water services company globally, operating water concession, industrial water management, and environmental services across more than 50 countries. In the industrial segment, Veolia manages water treatment infrastructure for petrochemical complexes, power plants, and semiconductor manufacturers, offering the full water cycle from raw water intake and process water preparation through effluent treatment, sludge management, and zero-liquid-discharge systems. Its Hubgrade digital platform enables real-time performance monitoring and optimization across multi-site industrial water portfolios, and the company has progressively expanded this digital layer into new contract structures that reward water and energy efficiency outcomes rather than asset throughput alone. The January 2025 award of a 15-year industrial water management contract at a major petrochemical complex in Jubail, Saudi Arabia covering raw water treatment, process water preparation, and treated wastewater reuse infrastructure reinforces Veolia's position as the leading operator of industrial water concessions in the MEA region.

Xylem is a water technology company with a portfolio spanning pumping systems, treatment equipment, digital monitoring, and analytics, augmented by the 2023 integration of Evoqua Water Technologies. Xylem's industrial water business now encompasses the Evoqua IONPURE continuous electrodeionization platform for ultrapure water production, the MEMCOR membrane filtration product line, and Evoqua's service and operations base alongside Xylem's legacy Flygt, Sensus, Wedeco, and YSI brands. This positions Xylem as the most horizontally integrated water technology provider in the market, with the capability to address industrial water requirements from source abstraction through ultrapure production, distribution, and digital monitoring. The company's May 2025 announcement of expanded IONPURE deployments across Southeast Asian semiconductor and pharmaceutical sites with a 35% increase in the APAC ultrapure water project pipeline cited since the Evoqua integration reflects the commercial momentum generated by consolidating treatment and digital capabilities under a single platform.

Ecolab operates its water division through the Water, Hygiene & Infection Prevention platform, providing treatment chemicals, monitoring services, and water efficiency programs to food and beverage, pharmaceutical, power generation, and manufacturing clients. Its Water for Climate initiative integrates digital water monitoring with proprietary chemical treatment programs to deliver contractually guaranteed water reduction outcomes, with active programs across more than 45 countries covering clients representing a combined water volume exceeding 500 billion gallons per year. The approach converts a commoditized chemical supply relationship into a long-term outcome-based service contract, generating higher margins and substantially stronger customer retention than transactional chemical sales.

Kurita Water Industries is Japan's leading water treatment specialist, with core competencies in ultrapure water production for semiconductor manufacturing, boiler and cooling water treatment for power and industrial applications, and membrane cleaning chemistries. Kurita's strength in high-purity water treatment positions it directly in the fastest-growing application segments of the market, particularly as semiconductor fabrication capacity expands across APAC and the United States under national chip manufacturing programs. The company's acquisition of BWT's industrial water chemistry business has extended its geographic reach into the European market.

Grundfos Pumps supplies pumping systems for water supply, treatment, distribution, and building applications globally, with a portfolio spanning centrifugal pumps, submersible pumps, and dosing systems. Its Pump Management Software and iSOLUTIONS service platform are enabling a commercial transition toward Pump-as-a-Service subscription models in industrial and municipal verticals, converting one-time hardware revenue into multi-year service contracts with performance guarantees. Grundfos's iSOLUTIONS 3.0 platform, launched in September 2024, extended digital monitoring and efficiency optimization capabilities to installations below 50 kW, opening the mid-market industrial segment to subscription-based digital water services for the first time.

DuPont Water Solutions supplies membrane products including FILMTEC reverse osmosis and nanofiltration elements and DOW ION exchange resins incorporated into industrial water treatment systems globally. The company's FILMTEC Fortilife XD membrane family, commercialized in November 2023, targets zero-liquid-discharge and minimum-liquid-discharge configurations in water-stressed industrial geographies, addressing the most technically demanding end of the membrane market.

Pentair provides water treatment systems, filtration equipment, and flow management solutions across industrial, residential, and commercial applications. Its industrial portfolio includes ion exchange softeners, multimedia filtration systems, and X-Flow ultrafiltration modules deployed at pharmaceutical manufacturing facilities and food processing plants in Europe and North America. Pentair's focused divestiture of non-water businesses has sharpened its strategic positioning in flow control and treatment.

SUEZ reconstituted as an independent entity following the asset division with Veolia provides water and waste management services to industrial and municipal clients across Europe, the Middle East, and Asia Pacific. Its industrial water division encompasses process water treatment, wastewater management, and sludge handling, with digital services delivered through the Aquadvanced platform for network analytics and asset performance management.

Aquatech International specializes in high-purity water systems, zero-liquid-discharge solutions, and seawater reverse osmosis plants for industrial clients. Its ZLD expertise is particularly relevant in water-stressed geographies and in sectors where discharge to surface water is subject to stringent regulatory controls. Aquatech's August 2023 award of a ZLD contract for a lithium processing facility in Chile valued at approximately USD 80 million exemplifies the company's positioning at the intersection of battery materials supply chain growth and water management.

Pall Corporation (a Danaher company) provides filtration, separation, and purification products with a strong footprint in pharmaceutical, semiconductor, and industrial process applications. Its hollow-fiber ultrafiltration modules and high-flow depth filtration cartridges serve as critical components in ultrapure water systems, pharmaceutical water-for-injection circuits, and advanced pre-treatment trains ahead of RO systems.

OVIVO USA delivers industrial water treatment solutions including ion exchange, membrane, and evaporation technologies, with particular depth in the power generation and semiconductor markets. OVIVO's Electrodeionization and EDI UltraPure product lines serve as direct competitive alternatives to Kurita's and Xylem's ultrapure water offerings, with installed systems at power and semiconductor facilities across North America and Europe.

BWT Industries is a European-based water technology company specializing in membrane filtration, ion exchange, and point-of-use treatment for industrial and commercial applications, with significant market presence in Germany, Austria, and Central Europe. BWT's magnesium mineralization and softening technologies are widely deployed in food, beverage, and pharmaceutical manufacturing facilities across the DACH region.

Dow supplies membrane elements, ion exchange resins, and specialty chemicals for water treatment under its DOWEX and FILMTEC product families, which are incorporated into industrial and municipal water treatment systems globally. Dow's water business benefits from dual exposure to desalination growth and to water reuse investment, with both application areas generating sustained product volume in the membrane elements market. Dow's circular water management system at its Terneuzen complex in the Netherlands achieving water reuse rates above 75% exemplifies the company's own deployment of advanced reuse infrastructure at its manufacturing sites.

Calgon Carbon (a Kuraray company) is the leading global supplier of granular activated carbon and UV disinfection systems, positioned as a direct beneficiary of PFAS treatment mandates across the United States and Europe. Its FILTRASORB and CENTAUR GAC product lines are specified in a significant proportion of PFAS remediation projects at industrial and municipal sites. The April 2024 US EPA PFAS MCL rule is expected to generate multi-year incremental demand for Calgon Carbon's GAC and ion exchange resin product lines throughout the 2025–2030 compliance cycle.

WABAG is an India-based multinational water technology company providing EPC and O&M services for drinking water, wastewater, and industrial effluent treatment plants. WABAG operates across South and Southeast Asia, the Middle East, and Africa, with a growing desalination project pipeline in Oman, Saudi Arabia, and North Africa.

Ion Exchange is India's largest water treatment company, providing ion exchange resins, packaged treatment systems, and project services across industrial, municipal, and pharmaceutical sectors. Ion Exchange is well-positioned to capture investment from India's expanding industrial water infrastructure programs, with a domestic manufacturing base and established relationships across the country's chemical, power, and pharmaceutical verticals.

Kemira is a Finnish specialty chemicals company providing water treatment and process chemistry solutions primarily to the pulp and paper, oil and gas, and municipal water sectors. Its SUPERFLOC and FENNOFLOC coagulant and flocculant product lines are core chemical inputs for industrial clarification and sedimentation processes globally, and the company has been expanding its service chemistry offering for industrial cooling water and process water applications.

Solenis provides specialty water treatment chemicals and monitoring services to industrial process water and wastewater applications, with a strong presence in pulp and paper, oil and gas, power generation, and municipal water. Its PRETREAT Plus and ACUMER product families address scale inhibition, corrosion control, and biofouling management in cooling and process water circuits. Solenis' 2023 merger with Diversey expanded its service reach into food safety and hygiene water treatment adjacent to its core industrial water chemistry business.

Market Share of 6.5%

Collective Market Share of 28.5%

Industrial Water Infrastructure Industry News

May 2025: Xylem announced expanded deployment of its Evoqua-branded IONPURE continuous electrodeionization platform across new semiconductor and pharmaceutical customer sites in Southeast Asia, citing a 35% increase in the APAC ultrapure water project pipeline since the 2023 Evoqua integration.

Jan 2025: Veolia secured a 15-year industrial water management contract at a major petrochemical complex in Jubail, Saudi Arabia, covering raw water treatment, process water preparation, and treated wastewater reuse infrastructure, reinforcing its position as the leading operator of industrial water concessions in the MEA region.

Nov 2024: The European Parliament formally adopted the revised Urban Wastewater Treatment Directive, mandating fourth-stage micropollutant treatment at all major European urban treatment plants by 2033 and creating a compliance investment program estimated at EUR 170 billion across EU member states.

Sep 2024: Grundfos launched the iSOLUTIONS 3.0 digital water management platform, extending predictive maintenance and energy optimization capabilities to industrial pump installations below 50 kW and opening the mid-market industrial segment to subscription-based digital water service models.

Jul 2024: WABAG was awarded a contract to design, build, and operate a 100,000 m³/day seawater desalination plant at the Sohar Industrial Port in Oman, providing industrial water supply to the port's expanding petrochemical and metals manufacturing tenants.

Apr 2024: The US EPA published final PFAS maximum contaminant level rules under the Safe Drinking Water Act, setting enforceable limits of 4 parts per trillion for PFOA and PFOS the most significant expansion of federal drinking water regulation in two decades and a direct driver of industrial treatment investment across North America.

Feb 2024: Veralto spun off from Danaher Corporation in September 2023 reported its first full-quarter financial results as an independent company, disclosing USD 1.27 billion in water quality revenue and highlighting strong industrial demand for Hach water analytics instrumentation and Trojan Technologies UV disinfection systems.

Market Concentration Score

The industrial water infrastructure market scores 3 out of 10 on the concentration scale, reflecting a highly fragmented competitive structure in which the top five players Veolia, Xylem, Ecolab, Kurita Water Industries, and Grundfos Pumps collectively account for only approximately 22.5% of global revenue, with no single operator holding more than 6.5% market share, consistent with an estimated Herfindahl-Hirschman Index below 500 and characteristic of a project-driven infrastructure market where technical specification, geography, and contract structure limit the share accumulation achievable by any single firm.

The industrial water infrastructure market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Infrastructure

Water supply

Water treatment

Wastewater collection

Water storage

Water reuse & recycling

Others

Market, By Component

Equipment & hardware

Pumps

Pipes & fittings

Valves

Filtration systems

Membranes

Sensors & monitoring systems

Treatment equipment

Storage tanks & reservoirs

Compressors & blowers

Mixers & agitators

Others

Chemical treatment solutions

Digital & automation solutions

Engineering, procurement & construction (EPC) Services

Operations & maintenance (O&M) Services

Market, By Source

Surface water

Groundwater

Municipal water supply

Seawater

Recycled water

Market, By Treatment

Physical treatment

Chemical treatment

Biological treatment

Membrane-based treatment

Others

Market, By End Use

Power generation

Oil & gas

Chemicals & petrochemicals

Food & beverage

Pharmaceuticals

Mining & metals

Automotive

Semiconductor & electronics

Others

The above information has been provided for the following regions & countries:

North America

U.S.

Canada

Mexico

Europe

Germany

France

UK

Italy

Spain

Asia Pacific

China

Japan

Indonesia

India

Australia

South Korea

Middle East & Africa

Saudi Arabia

UAE

Iran

South Africa

Egypt

Latin America

Brazil

Argentina

Chile

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →