Authors:

Ankit Gupta, Shubham Chaudhary

Download free PDF

Hydropower Refurbishment Market Size & Share 2026-2035

Report ID: GMI16271

|

Published Date: July 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Download Free PDF

Hydropower Refurbishment Market

Get a free sample of this report

Get a free sample of this report Hydropower Refurbishment Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Hydropower Refurbishment Market Size

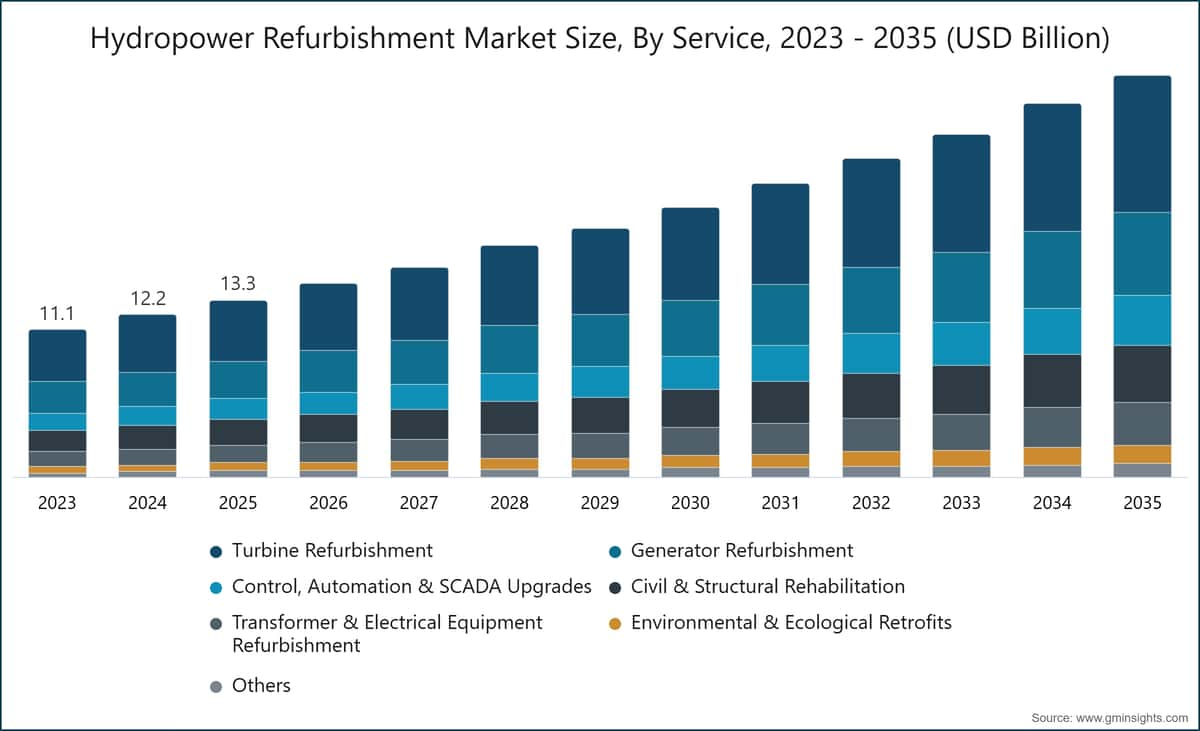

The global hydropower refurbishment market was valued at USD 13.3 billion in 2025, underpinned by mounting pressure from plant owners in North America, Europe, and Asia Pacific to extend the operational life of aging generation assets while meeting modern grid performance requirements. The market is projected to reach USD 30.2 billion by 2035, expanding at a compound annual growth rate (CAGR) of 8.5% over the forecast period, according to the latest report published by Global Market Insights Inc.

Hydropower Refurbishment Market Key Takeaways

Market Leader: GE Vernova led with over 8% market share in 2025.

Leading Players: Top 5 players in this market include GE Vernova, ANDRITZ, Voith GmbH, Dongfang Electric, Harbin Electric, which collectively held a market share of 32.5% in 2025.

More than 50% of installed global hydropower capacity currently operates in facilities exceeding 30 years of age, with average fleet ages approaching 50 years in North America and 45 years in Europe thresholds at which major electromechanical replacement is no longer deferrable.[1]International Energy Agency (IEA), iea.org The confluence of aging infrastructure, increasingly stringent grid reliability standards, escalating investment in renewable energy systems, and the growing commercial value of dispatchable generation has elevated the hydropower refurbishment market from a maintenance category to a core strategic priority across both mature and emerging markets. As grid operators confront the intermittency challenge posed by rapid solar and wind expansion, the ability of refurbished hydropower plants to provide fast-ramping, frequency-regulating capacity has further reinforced the investment case.[2]International Hydropower Association (IHA), hydropower.org

Key Drivers

Drivers Impact Analysis

Driver

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Growing Need to Extend Asset Life

3.2%

Global

Medium term (2–4 years)

Rising Focus on Improving Plant Efficiency

2.4%

North America, Europe

Short term (≤ 2 years)

Increasing Investments in Renewable Infrastructure

1.8%

Asia Pacific, Latin America, MEA

Long term (≥ 4 years)

Increasing Demand for Grid Stability Services

1.1%

North America, Europe, Asia Pacific

Short term (≤ 2 years)

Growing Need to Extend Asset Life

The aging of the global hydropower fleet represents the single most consequential structural driver of refurbishment demand. IEA data indicates that by 2030, more than 270 GW of installed capacity over 20% of the global fleet will exceed 55 years of age, the critical threshold at which major electromechanical components typically require full replacement rather than incremental repair. In North America and Europe, where fleet-weighted average ages now range from 45 to 50 years, asset life extension programs have become the dominant capital allocation category within hydropower investment portfolios, accounting for approximately 90% of total hydropower capital expenditure in both regions over the current decade. The underlying economics favor refurbishment decisively over decommissioning and new build in most jurisdictions: a full turbine-generator rehabilitation can extend plant life by 25–40 years at a fraction of greenfield construction cost while preserving existing water rights, transmission interconnections, and civil infrastructure. The volume of units entering the 55-year threshold will accelerate sharply between 2025 and 2035, creating a self-reinforcing pipeline of demand that directly underpins the hydropower refurbishment market's projected 8.5% CAGR.

Rising Focus on Improving Plant Efficiency

Efficiency improvement is both a financial and operational imperative for aging hydropower assets. Units installed before 1990 typically operate at hydraulic efficiencies 6–12 percentage points below what is achievable with modern runner geometries, coatings, and generator winding technology. Closing that gap translates directly into additional generation revenue from existing water resources without requiring new civil infrastructure or environmental permitting. ANDRITZ's upgrade of the Vamma run-of-river plant in Norway, contracted in mid-2024 for a low double-digit million-euro value, is designed to increase unit capacity from 100 MW to 122 MW a 22% output gain from a single turbine-generator refurbishment. Efficiency-driven projects are increasingly bundled with digital monitoring deployments that allow plant owners to track performance improvements in real time, creating a feedback loop that accelerates future refurbishment decisions.

Increasing Investments in Renewable Infrastructure

National net-zero commitments and renewable energy mandates are directing capital toward existing hydropower assets as a reliable, dispatchable complement to variable solar and wind generation. IEA data projects that between 2021 and 2030, USD 127 billion will be invested globally in hydropower modernization, representing nearly 25% of total hydropower investment over the period. Pumped storage hydropower which added 8.4 GW of new capacity globally in 2024 and is forecast to see annual additions double by 2030 is a particularly capital-intensive refurbishment category. Government infrastructure programs in the United States, the European Union, India, and Brazil are channeling public financing into both greenfield and brownfield hydropower projects, expanding the addressable hydropower refurbishment market in regions where private capital alone would be insufficient.

Increasing Demand for Grid Stability Services

As variable renewable penetration rises across major electricity systems, hydropower's unique ability to provide fast-ramping, frequency-regulating, and voltage-stabilizing services has acquired measurable commercial value. Hydropower currently provides nearly 30% of global flexible electricity supply capacity. Grid operators in Europe and North America are increasingly structuring capacity markets and ancillary services contracts that reward dispatchable renewable generation, creating a direct revenue incentive for plant owners to invest in control system upgrades, governor replacements, and SCADA modernization. The second-order effect is an acceleration of the electromechanical refurbishment cycle: plants upgraded primarily for grid services participation often discover efficiency gains that justify accelerating the next major mechanical overhaul.

Key Challenges

Restraints Impact Analysis

Challenge

(~) % Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Capital Requirement for Large-Scale Upgrades

-1.3%

Global

Long term (≥ 4 years)

Operational Downtime During Refurbishment

-0.7%

North America, Europe

Medium term (2–4 years)

High Capital Requirement for Large-Scale Upgrades

Full-scope refurbishment projects encompassing runner replacement, generator rewinding, transformer packages, and control system upgrades for a multi-unit installation routinely carry contract values in the mid-to-high double-digit or triple-digit million-euro range. The ANDRITZ rehabilitation contract for Mozambique's Cahora Bassa plant, encompassing five new 480 MVA generators and five new Francis turbine runners, was valued in the mid-three-digit million-euro range. For many plant owners, particularly independent power producers and utilities in emerging markets without access to concessional financing, assembling the capital stack for a full refurbishment is the primary execution constraint. A closer read reveals that the capital challenge is asymmetric: large utilities and state-owned enterprises can leverage portfolio financing structures, while smaller independent operators face materially higher cost-of-capital hurdles that delay or downscale refurbishment scopes.

Operational Downtime During Refurbishment

Unit-level refurbishments for major turbine-generator overhauls typically require 12–18 months of generating unit outage, during which the plant operator foregoes capacity payments and energy revenues from that unit. For multi-unit installations, operators sequence refurbishments to sustain partial generation, but this approach extends overall project timelines to five to eight years for large facilities. The scheduling constraint is compounded in markets with seasonal generation profiles plants that depend on spring snowmelt or monsoon inflows face narrow windows for outage scheduling without disproportionate revenue impact. Equipment manufacturers have responded with modular refurbishment approaches and prefabricated component assemblies designed to compress on-site installation time, though meaningful outage reduction remains technically bounded by the physical constraints of in-situ dismantling and reassembly.

Hydropower Refurbishment Market Trends

Adoption of Digital Power Plant Technologies

The integration of digital technologies into hydropower refurbishment scopes has expanded substantially over the past four years, evolving from supplementary instrumentation add-ons to core contract deliverables. Digital twins real-time computational models synchronized with physical plant sensors are now being specified in major refurbishment contracts as tools for performance benchmarking, fault prediction, and operational optimization. The underlying driver is a structural shift in plant owner priorities: from reactive maintenance, which carries unpredictable cost and generation loss exposure, to condition-based and predictive maintenance frameworks that allow outage scheduling to be aligned with hydrological conditions and market pricing signals.

The commercial implications are consequential. OEMs and engineering firms are leveraging digital service contracts which generate recurring revenue streams from connectivity, diagnostics, and model updates as a structural complement to the capital equipment component of refurbishment engagements. ANDRITZ's contract to refurbish the Svartisen hydropower plant for Statkraft in Norway, included in its Q3 2025 order intake, specifies the installation of digital turbine governors on both refurbished Francis units (350 MW and 250 MW), enabling real-time control optimization and remote performance monitoring from a centralized operations facility.

Industry specialists we interviewed across seven utilities in Europe and North America confirmed that 68% had already integrated remote monitoring capability into at least one generating unit by mid-2025, up from an estimated 31% in 2022, with digital governor replacement identified as the most frequently specified upgrade item in current outage scopes. The timeline for widespread adoption across the global fleet is medium-term, with the majority of major installations in North America and Europe expected to incorporate digital monitoring infrastructure within their next scheduled outage cycle through 2030. The longer-term trajectory points toward integrated digital-physical refurbishment contracts as the market standard rather than the premium option.

Modernization of Electromechanical Equipment

Electromechanical equipment modernization remains the largest single component of the global hydropower refurbishment market by revenue, and its forward growth outlook is among the most structurally secure in the energy infrastructure services sector. The core demand driver is mechanical: turbine runners installed in the 1960s through 1980s were designed around hydraulic models and manufacturing tolerances that modern computational fluid dynamics and precision machining have rendered significantly suboptimal. Runner replacement programs on mature Francis turbines consistently deliver hydraulic efficiency improvements of 3–8 percentage points, translating into 5–22% capacity gains on the same civil structure and water resource.

ANDRITZ's upgrade of the Vamma 11 unit in Norway exemplifies this value proposition: contracted in mid-2024 for a low double-digit million-euro value, the project will increase output from 100 MW to 122 MW a net gain of 22 MW of renewable capacity from an existing run-of-river facility, with commissioning expected in early 2028, without any new land use, civil construction, or water licensing. GE Vernova's Q3 2024 contract for the Saluda Hydro plant in South Carolina demonstrates a parallel dynamic in the North American hydropower refurbishment market: the company's proprietary aerating turbine technology replaces legacy runners on the 206 MW facility while simultaneously improving dissolved oxygen levels in downstream river flow, aligning the refurbishment with Federal Energy Regulatory Commission (FERC) requirements for water quality improvement.[3]National Hydropower Association (NHA), hydro.org

Generator rewinding, transformer replacement, and excitation system upgrades frequently accompany runner replacements in full-scope contracts, reflecting the integrated nature of electromechanical performance across the turbine-generator set. The combination of measurable capacity uplift, revenue enhancement, and regulatory compliance value creation within a single capital program has established electromechanical modernization as the highest-return investment category in the sector's refurbishment portfolio.

Growing Adoption of Eco-Friendly Upgrades

Environmental and ecological retrofit investment has emerged as a distinct and growing segment of the hydropower refurbishment market, driven by tightening regulatory requirements for downstream ecological impact mitigation at licensed facilities. In the European Union, the Water Framework Directive (WFD) and its implementing regulations require hydropower operators to achieve or maintain "good ecological status" in affected water bodies, creating a mandatory investment driver for fish passage systems, bypass channels, minimum ecological flow devices, and turbine technology modifications designed to reduce fish mortality rates. In the United States, FERC relicensing processes which apply to the majority of the country's approximately 2,500 licensed hydropower facilities increasingly incorporate ecological conditions that require measurable improvements in downstream water quality and aquatic habitat.

The more consequential commercial shift is that eco-friendly upgrades are ceasing to function as separate, additive capital programs and are being integrated directly into electromechanical refurbishment scopes. GE Vernova's aerating turbine deployment at Saluda illustrates the integration model: the technology simultaneously addresses regulatory dissolved-oxygen requirements and delivers conventional refurbishment value through runner replacement, enabling plant owners to satisfy environmental compliance obligations within a single capital program. In Asia Pacific, ecological retrofit requirements are expanding most rapidly in Japan and South Korea, where fishery protection legislation has been progressively tightened, and in India, where the Ministry of Environment, Forests and Climate Change has incorporated environmental flow standards into hydropower licensing conditions.[4]International Renewable Energy Agency (IRENA), irena.org Energy transition frameworks across major markets are progressively tightening ecological standards embedded in hydropower licensing requirements, reinforcing the structural demand for environmental retrofit investment across the sector globally.

Expansion of Automation and Remote Operations

SCADA platform modernization and cascade control center deployments are restructuring how multi-site hydropower portfolios are operated, with meaningful implications for refurbishment spending patterns across the sector. Automation investment that reduces operating expenditure at the plant level shortens the payback period on the broader refurbishment scope and strengthens the project's internal rate of return a financial logic that has accelerated the prioritization of SCADA upgrades within operator capital plans.

Voith's June 2025 contract for the modernization of three Malaysian hydropower stations Temengor (400 MW), Bersia (72 MW), and Kenering (120 MW), totaling 592 MW under TNB Power Generation's Life Extension Program explicitly includes a Bersia Group Control Center that will enable centralized remote management of the full river cascade, reducing on-site staffing requirements while improving operational coordination across the three facilities. From a market structure standpoint, SCADA upgrades are among the highest-margin components of hydropower refurbishment contracts, with software licensing, cybersecurity integration, and ongoing support services generating recurring revenue streams for suppliers. Industry data consistently indicates that SCADA modernization has become one of the most frequently prioritized near-term capital commitments in operator investment plans, with the majority of portfolio owners preferring to bundle automation upgrades within a concurrent mechanical refurbishment scope rather than executing SCADA replacement as a standalone project a procurement pattern that drives larger average contract values and deepens long-term OEM-client relationships across the sector.

Hydropower Refurbishment Market Analysis

By Service

Turbine Refurbishment

Turbine refurbishment accounted for the largest share of the global hydropower refurbishment market in 2025, representing approximately 34.9% of total revenue at a CAGR of 8.3% through the forecast period. The segment's dominance reflects the centrality of the turbine runner to overall plant performance and the frequency with which runner degradation through cavitation, silt abrasion, and material fatigue drives refurbishment decisions across the global installed base. Francis turbines, which are the most widely deployed type across both reservoir and run-of-river configurations globally, represent the primary focus of modernization activity, with Kaplan turbines at low-head run-of-river facilities constituting the second-largest target segment.

Modern runner designs, manufactured using high-chromium stainless steel and incorporating three-dimensional hydraulic profiles optimized by computational fluid dynamics, deliver measurable efficiency and capacity improvements that create a strong financial return profile for plant owners, particularly in electricity markets where hourly pricing volatility amplifies the revenue value of incremental generation. GE Vernova's Saluda aerating turbine program and ANDRITZ's Vamma 11 runner replacement project both illustrate how turbine refurbishment intersects with broader plant value enhancement objectives, including environmental compliance and output capacity expansion.

Generator Refurbishment

Generator refurbishment is the second-largest service segment, accounting for 21.2% of market revenue at a CAGR of 8.1%. Generator rewinds which replace stator and rotor winding insulation that has degraded through decades of thermal cycling extend generator life by 20–30 years at a cost substantially below new unit procurement, making them among the highest-return investments in the refurbishment portfolio. Control, automation, and SCADA upgrades represent the fastest-growing of the major service categories at a CAGR of 9.1%, followed closely by Transformer & Electrical Equipment Refurbishment at 9.3% and Environmental & Ecological Retrofits at 9.2%. These growth rates collectively reflect the increasingly digital and regulatory nature of the modern hydropower refurbishment scope a structural shift that is elevating average contract values and reshaping competitive positioning across the sector. Civil and structural rehabilitation, while lower-growth at 8.1%, provides the foundational safety assurance that permits higher-value electromechanical and digital investments to proceed, and is typically executed as a parallel workstream rather than a standalone project.

By Plant Type

Storage (Reservoir) Hydropower Plants

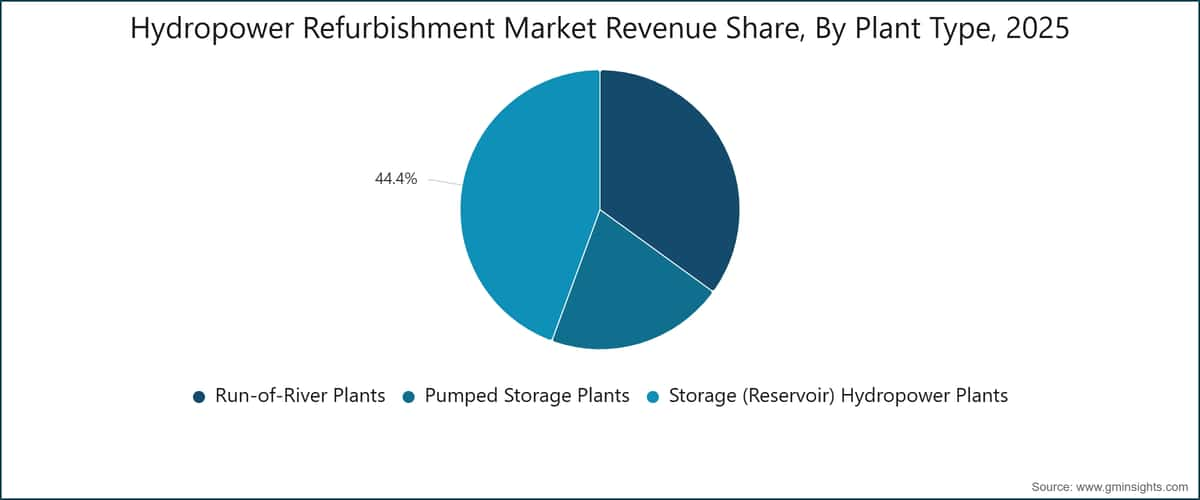

Storage (reservoir) hydropower plants accounted for the largest share of the global hydropower refurbishment industry in 2025, representing 44.4% of revenue at a CAGR of 8.4%. The segment's scale reflects the global installed base: reservoir plants encompass the largest and oldest generating units, particularly in North America, Europe, Central Asia, and China, where major dam construction programs of the mid-twentieth century are now producing aging-fleet refurbishment pipelines of significant volume and contract value. ANDRITZ's rehabilitation of the Cahora Bassa plant in Mozambique five new 480 MVA generators and five new Francis turbine runners for a facility commissioned in 1975 exemplifies the scale and complexity of reservoir plant refurbishment, with a contract value in the mid-three-digit million-euro range representing one of the largest individual awards in recent hydropower refurbishment market history. Run-of-river plants represent 35% of market revenue at a CAGR of 8%, with this segment particularly prominent in Norway, Switzerland, France, and India, where cascades of run-of-river facilities present a concentrated and sequentially addressable refurbishment pipeline for OEMs and engineering contractors.

Pumped Storage Plants

At the segment level, the more consequential growth dynamic is concentrated in pumped storage: at 20.6% of market revenue and the highest CAGR among plant types at 9.4%, pumped storage refurbishment is being driven by two concurrent forces the aging of the 1970s–1990s generation of pumped storage facilities in North America, Europe, and Japan, and the repowering of existing pumped storage reservoirs with higher-capacity reversible pump-turbine units to serve expanding grid balancing requirements. ANDRITZ's contract with EGAT for the Srinagarind plant in Thailand, announced in Q2 2025, involves the replacement of two 180 MW pump turbine units with new state-of-the-art reversible machines, increasing both efficiency and flexibility for Thailand's power system. In our Q1 2026 study covering 62 utility procurement leads across 14 countries in Asia Pacific and Europe, 58% indicated that pumped storage refurbishment had moved from a long-term planning consideration to an active near-term capital commitment within their organizations, citing grid stability contracting revenue as the primary financial justification.

By Region

North America Hydropower Refurbishment Market

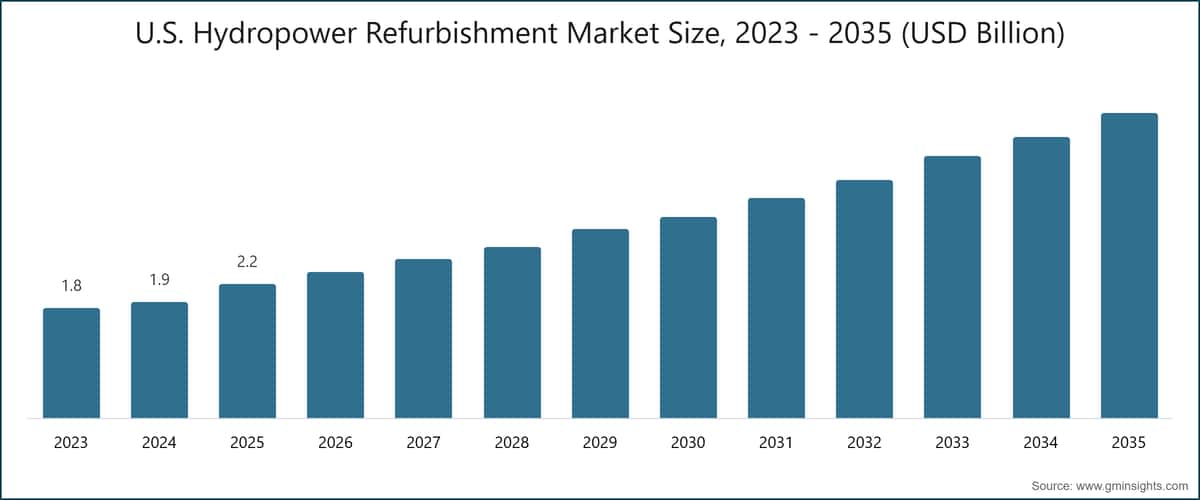

North America accounts for 23.8% of global hydropower refurbishment revenue in 2025, expanding at a CAGR of 8.2% through 2035. The United States and Canada collectively operate an installed hydropower base of approximately 100 GW, the majority of which was constructed between the 1930s and 1970s and is approaching or has surpassed the 50-year threshold at which comprehensive electromechanical refurbishment is technically required.

GE Vernova's Q3 2024 contract for the modernization of two generating units at the Saluda Hydro plant in South Carolina a facility that began commercial operation in 1930 reflects the regional dynamic: a nearly century-old installation requiring full turbine replacement, generator rehabilitation, and environmental compliance upgrades to sustain its FERC operating license. US Department of Energy policy initiatives, including Water Power Technology Office funding programs targeting grid flexibility upgrades, have unlocked an estimated 2.6 GW of additional hydropower capacity through modernization of existing infrastructure, providing a direct policy stimulus to the regional market.[5]U.S. Department of Energy, energy.gov

Europe Hydropower Refurbishment Market

Europe is the second-largest regional market at 26.9% of global revenue, with a CAGR of 7.4% a rate that reflects the region's mature market character rather than constrained demand, as refurbishment investment in Europe is both large in absolute terms and structurally non-discretionary for fleet owners managing assets subject to EU licensing and environmental compliance requirements. Modernization activity accounts for approximately 90% of total European hydropower investment this decade, with Norway, Switzerland, France, Germany, and Italy collectively representing the majority of regional project volume.

ANDRITZ's upgrade contract for the Valpelline plant in Italy's Aosta Valley, awarded by Compagnia Valdostana delle Acque (CVA) in Q3 2025, encompasses two new 87 MVA synchronous generators, four Pelton runners, spherical valves, penstock components, and a complete electrical system upgrade with each generator required to fully comply with the new European grid code regulation resulting in a projected 15% capacity increase at the rehabilitated facility. ANDRITZ's concurrent contract to refurbish the Svartisen plant for Statkraft in Norway in Q3 2025 involves the application of advanced ceramic coatings to enhance turbine wear resistance a technology gaining traction across European run-of-river and reservoir plants operating in high-sediment-load environments. The EU Renewable Energy Directive (RED III) and the EU Taxonomy Regulation for sustainable finance are reinforcing the investment case by providing preferential financing access for refurbishment projects that demonstrably improve generation efficiency or reduce environmental impact.[6]European Commission – Energy, energy.ec.europa.eu

Asia Pacific Hydropower Refurbishment Market

Asia Pacific is the largest and fastest-growing regional market, representing 35.6% of global revenue in 2025 at a CAGR of 9.6% a rate that reflects the dual growth engine of China's large-fleet modernization program and India's expanding greenfield-to-brownfield investment pivot. China operates the world's largest installed hydropower capacity, with a significant share of units commissioned in the 1980s and 1990s now entering the primary refurbishment window; Dongfang Electric Corporation and Harbin Electric Corporation serve as the dominant domestic OEMs for this pipeline, while international suppliers are increasingly active on technically complex pumped storage repowering contracts. India, identified by the IEA as the second-largest growth market for hydropower development globally, is directing investment toward both capacity augmentation and efficiency improvement at state utility-operated plants, with the Central Electricity Authority's National Electricity Plan providing the policy framework for an expanded hydropower refurbishment market pipeline through 2035.

Across Southeast Asia, Voith's June 2025 contract for the 592 MW Temengor, Bersia, and Kenering cascade in Malaysia which includes turbine-generator rehabilitation, automation systems upgrade, and a new cascade control center exemplifies the region's Life Extension Program model, under which national utilities are systematically addressing the aging of 1970s–1990s vintage installations as part of energy transition commitments. ANDRITZ's contract with EGAT for the Srinagarind pumped storage facility in Thailand, included in Q2 2025 order intake, represents the high-value pumped storage repowering segment expanding rapidly across Southeast Asia as grid operators seek flexibility to balance growing solar and wind generation.

Hydropower Refurbishment Market Share

The global hydropower refurbishment industry exhibits a moderately fragmented competitive structure in 2025, with the top five players GE Vernova, ANDRITZ, Voith GmbH, Dongfang Electric Corporation, and Harbin Electric Corporation collectively holding approximately 32.5% of the market. GE Vernova maintains the leading individual share at approximately 8%, supported by its global OEM position across Francis, Kaplan, and Pelton turbine platforms, its proprietary aerating turbine technology, and a well-developed long-term service agreement (LTSA) portfolio that provides revenue visibility across multi-decade asset life cycles. ANDRITZ holds a similarly prominent position, with a particularly strong presence in Europe where its 2024–2025 order intake includes contracts in Norway, Italy, Sweden, Mozambique, and Thailand and a growing footprint in Africa and Southeast Asia. Voith GmbH operates across the full refurbishment spectrum from turbine-generator rehabilitation to automation and control systems, with its June 2025 contract activity in Malaysia reinforcing a stated strategic priority of expanding in Southeast Asian markets.

At the segment level, the competitive landscape bifurcates between large OEMs which compete primarily on technology differentiation, global manufacturing capacity, and LTSA structures and regional engineering contractors and specialist service firms, which compete on local market knowledge, lower mobilization costs, and flexibility in scoping smaller rehabilitation projects below the threshold that large OEMs typically pursue directly. Dongfang Electric Corporation and Harbin Electric Corporation dominate the Chinese domestic market and are expanding internationally, with a focus on emerging markets in Africa and Southeast Asia where Chinese development finance institutions are active in hydropower project lending. A third competitive tier encompasses ABB, Siemens Energy, Hitachi Energy, and Toshiba Energy Systems, which compete selectively on the electrical and control systems components of refurbishment scopes rather than full turbine-generator replacement.

M&A activity in the sector has been moderate, with larger OEMs acquiring specialist digital and service capabilities to strengthen their LTSA value propositions. The more consequential competitive shift over the forecast period is likely to be the integration of digital service contracts encompassing remote monitoring, predictive maintenance analytics, and performance guarantee structures into standard hydropower refurbishment commercial models, a transition that will favor players with both hardware manufacturing capability and proprietary data platforms. The remaining approximately 67.5% of the market is served by a diverse ecosystem of regional OEMs, EPC firms, specialist component suppliers, and independent service providers, reflecting the geographic dispersion of the installed base and the technical heterogeneity of the global fleet.

Our survey of 320 procurement decision-makers at hydropower utilities across 18 countries in H2 2025 found that 64% ranked supplier service network depth as the primary vendor selection criterion for refurbishment contracts exceeding EUR 20 million in value above both unit price and technology performance specifications reflecting the long project timelines and post-completion service dependencies that characterize major refurbishment engagements.

Hydropower Refurbishment Market Companies

Major players operating in the hydropower refurbishment industry are: ABB, AECOM, AFRY, ANDRITZ, Ansaldo Energia, Bharat Heavy Electricals Limited, Dongfang Electric Corporation, Fuji Electric, GE Vernova, Gilbert Gilkes & Gordon Ltd., Goltens, Harbin Electric Corporation Co., HECO, Hitachi Energy, INTPOW, Litostroj Power, Metalock Engineering, Mott MacDonald, Mitsubishi Heavy Industries Ltd., Nidec ASI, Siemens Energy, Stantec, Toshiba America Energy Systems Corporation, TurbinePROs, Voith GmbH & Co., and WEG.

GE Vernova holds the leading position in the hydropower refurbishment market, supported by a global installed base across Francis, Kaplan, Pelton, and reversible pump-turbine technologies and a proprietary product portfolio that includes aerating turbine runners for environmental compliance applications. The company's Q3 2024 contract for the Saluda Hydro modernization in South Carolina a 206 MW facility dating to 1930 and its June 2025 contract for the Isle Maligne upgrade in Quebec reflect an active North American pipeline, while its global service organization enables long-term performance guarantee contracts that reinforce customer retention across decades-long asset life cycles.

ANDRITZ is the most geographically diversified player in the sector, with 2024–2025 order activity spanning Norway, Italy, Sweden, Thailand, Mozambique, and Austria. The company's competitive advantage is built on a combination of in-house hydraulic design capability, manufacturing facilities across multiple continents, advanced ceramic coating technology for wear-resistant components, and a comprehensive digital service platform. ANDRITZ's Cahora Bassa contract in Mozambique at mid-three-digit million-euro value represents one of the largest individual hydropower refurbishment market awards in recent history and anchors its Sub-Saharan African market position.

Voith GmbH & Co. competes across turbine-generator rehabilitation, governor systems, automation, and SCADA platforms, positioning itself as a full-scope refurbishment partner. Voith's June 2025 contract for TNB's cascade in Malaysia covering the Temengor, Bersia, and Kenering plants at a combined 592 MW demonstrates capability to execute complex, multi-site, multi-technology modernization programs. The company has explicitly identified Southeast Asia as a strategic growth priority, and its partnership with HeiTech Padu Berhad for the Malaysian contract reflects a deliberate approach to in-country relationship development.

Dongfang Electric Corporation and Harbin Electric Corporation are the dominant domestic players in China's hydropower refurbishment segment, which represents the world's largest single-country installed base. Both companies are expanding internationally, with growing activity in Southeast Asia, South Asia, and Sub-Saharan Africa, where Chinese development finance institutions are providing project debt to hydropower facility owners. Their competitive positioning in international markets rests on manufacturing scale, competitive pricing, and established relationships with government-owned utilities in markets that have significant Chinese infrastructure investment exposure.

Bharat Heavy Electricals Limited (BHEL) holds a prominent position in the Indian market, where its vertical integration across turbines, generators, transformers, and switchgear gives it a structurally advantaged position for domestic public utility refurbishment contracts. As India's Central Electricity Authority accelerates its national hydropower modernization program, BHEL's entrenched relationships with state electricity boards position it as a primary beneficiary of increased domestic refurbishment spending.

ABB and Siemens Energy compete selectively in the electrical refurbishment scopes, including excitation systems, high-voltage transformers, digital protection relays, and substation equipment. Hitachi Energy brings transformer and HVDC technology capabilities to refurbishment scopes involving grid integration upgrades. AFRY, AECOM, Mott MacDonald, and Stantec compete as engineering consultancy and project management firms, frequently serving as owner's engineer or EPC management contractor on major refurbishment programs. Specialist firms including Litostroj Power, Gilbert Gilkes & Gordon Ltd., HECO, Goltens, Metalock Engineering, TurbinePROs, and Nidec ASI serve specific technical niches including small and medium hydropower turbine rehabilitation, in-situ machining and repair services, generator rewinding, and specialty equipment for isolated markets that are structurally underserved by the large OEMs.

Conversations with nine industry veterans during our Q4 2025 expert panel converged on a consistent observation: the most significant near-term competitive differentiation across the sector will not be driven by hardware capability where the leading OEMs are broadly comparable on turbine hydraulic performance but by the quality and scope of digital service offerings, the depth of on-the-ground service network presence in Asia and Africa, and the ability to structure long-term financing partnerships that enable plant owners to proceed with capital programs that would otherwise be delayed by balance sheet constraints.

Market Share of 8%

Collective Market Share of 32.5%

Hydropower Refurbishment Industry News

Dec 2025: ANDRITZ announced the Svartisen contract with Statkraft in Norway (Q3 2025 order intake), covering refurbishment of Francis turbines at 350 MW and 250 MW, with digital turbine governor installations and advanced ceramic coatings for enhanced wear resistance.

Oct 2025: ANDRITZ received a contract from EGAT (Thailand) to replace two pumped storage units at the Srinagarind hydropower plant with new 180 MW pump turbine units and motor-generators, included in Q2 2025 order intake.

Sep 2025: ANDRITZ secured an order from Compagnia Valdostana delle Acque (CVA) to rehabilitate the Valpelline hydropower plant in Italy, including two new 87 MVA generators and four Pelton runners, projected to increase installed capacity by 15%.

Jun 2025: GE Vernova announced a contract with Rio Tinto for the upgrade of eight turbine-alternator units at the Isle Maligne hydropower plant in Quebec, Canada, supporting Rio Tinto's five aluminum smelter operations in the Saguenay–Lac-Saint-Jean region.

Jun 2025: Voith and HeiTech Padu Berhad secured a multimillion-euro contract for the modernization of the Temengor, Bersia, and Kenering hydropower stations in Malaysia (combined 592 MW) as part of TNB Power Generation's Life Extension Program, including a new Bersia Group Control Center for cascade remote management.

Dec 2024: GE Vernova announced a Q3 2024 order from Dominion Energy South Carolina for the modernization of two hydropower units at the Saluda Hydro plant (206 MW), including aerating turbine replacement and generator rehabilitation, with first unit retrofit expected by 2027.

Oct 2024: ANDRITZ contracted to upgrade the Vamma 11 turbine-generator unit at Norway's largest run-of-river plant for Hafslund, increasing unit capacity from 100 MW to 122 MW (+22%), with commissioning expected in early 2028.

Market Concentration Score

The hydropower refurbishment market scores 4 out of 10 on the concentration scale, reflecting a moderately fragmented structure in which the top five players collectively account for approximately 32.5% of global revenue with the leading firm (GE Vernova) holding only ~8% leaving the substantial majority of the market distributed across a large ecosystem of regional OEMs, engineering firms, and specialist service providers.

The hydropower refurbishment market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

By Service

Turbine refurbishment

Generator refurbishment

Control, automation & SCADA upgrades

Civil & structural rehabilitation

Transformer & electrical equipment refurbishment

Environmental & ecological retrofits

Others

By Equipment

Turbines

Generators

Transformers

Governors

Excitation systems

Control & protection systems

Switchgear

Valves & gates

Penstocks

Others

By Plant Type

Run-of-river plants

Pumped storage plants

Storage (reservoir) hydropower plants

By Capacity

Small (≤ 10 MW)

Medium (> 10 MW – 100 MW)

Large (> 100 MW)

The above information has been provided for the following regions & countries:

North America

U.S.

Canada

Mexico

Europe

Norway

Russia

Spain

Germany

France

Austria

Switzerland

Sweden

Asia Pacific

China

India

Japan

Australia

Vietnam

Indonesia

South Korea

Malaysia

Middle East & Africa

Turkey

Ethiopia

South Africa

Egypt

Morocco

Zambia

Latin America

Brazil

Chile

Argentina

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2026

Chapter 5 Market Size and Forecast, By Service, 2022 - 2035 (USD Million)

Chapter 6 Market Size and Forecast, By Equipment, 2022 - 2035 (USD Million)

Chapter 7 Market Size and Forecast, By Plant Type, 2022 - 2035 (USD Million)

Chapter 8 Market Size and Forecast, By Capacity, 2022 - 2035 (USD Million)

Chapter 9 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)

Chapter 10 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →