Summary

Table of Content

High Voltage Circuit Breaker Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

High Voltage Circuit Breaker Market Size

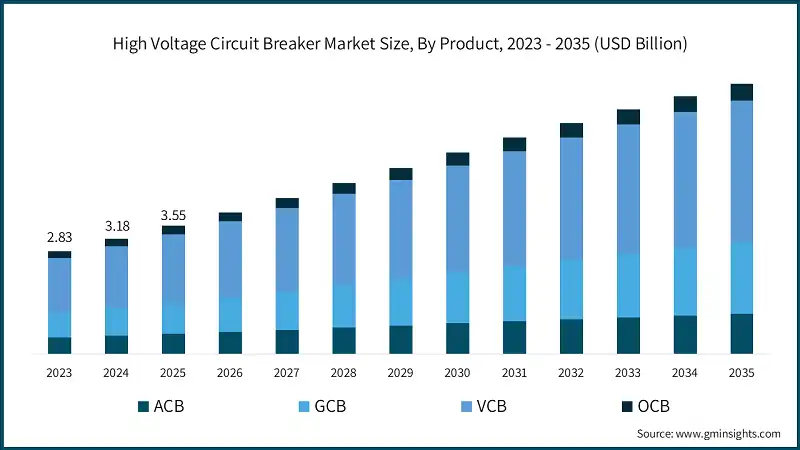

According to a recent study by Global Market Insights Inc., the high voltage circuit breaker market was estimated at USD 3.5 billion in 2025. The market is expected to grow from USD 3.9 billion in 2026 to USD 7.4 billion by 2035, at a CAGR of 7.4%.

High Voltage Circuit Breaker Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 3.5 Billion

- 2026 Market Size: USD 3.9 Billion

- 2035 Forecast Market Size: USD 7.4 Billion

- CAGR (2026–2035): 7.4%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: Latin America

Key Market Drivers

- Expansion of Smart Grid Networks.

- Increasing Electricity Demand.

- Refurbishment & Retrofit of Existing Grid Infrastructure.

Challenges

- High Initial Capital Costs.

Opportunity

- Integration of Renewable Energy.

- Digitalization and Smart Monitoring.

- Expansion in Emerging Economies.

Key Players

- Market Leader: ABB led with over 12% market share in 2025.

- Leading Players: Top 5 players in this market include ABB, GE Vernova, Hitachi Energy, Schneider Electric, Mitsubishi Electric, which collectively held a market share of 40% in 2025.

Get Market Insights & Growth Opportunities

To get key market trends

- High voltage circuit breakers (HVCBs) are propelled by the rapid build-out of transmission needed to integrate large-scale wind and solar, relieve congestion, and improve reliability. Consequently, global grid investment and supply-chain attention have intensified, raising demand for advanced high-voltage equipment across projects. For instance, the IEA’s 2025 report highlights accelerating transmission expansion needs above 66 kV and longer lead times, urging coordinated planning to deliver timely infrastructure.

- Electrification of industry, transport, and buildings, coupled with more frequent extreme weather, is driving utilities to harden and expand high-voltage networks, boosting HVCB demand for fault interruption and grid flexibility. For instance, the U.S. DOE’s GRIP program selected USD 7.6 billion for 105 projects since 2023–2024 to enhance resilience and increase capacity, including innovative transmission approaches, directly stimulating high-voltage equipment deployments.

- Load growth from data centers, manufacturing, and electrification is spurring high-voltage expansion, reconductoring, and GETs, raising procurement of HVCBs for stations and lines. In August 2024, DOE awarded USD 2.2 billion for eight transmission projects (approximately 600 miles new lines, 400 miles reconductoring) adding about 13 GW of capacity, underscoring near-term demand for high-voltage switchgear.

- EU ambitions to triple renewables and electrify end uses require significant transmission reinforcement, interconnections, and smart grids, expanding HVCB installations across voltage classes. As an illustration, the European Commission’s 2023 Grids Action Plan estimates over USD 680 billion in electricity network investments this decade, with dedicated measures to accelerate permitting and cross-border infrastructure, making high-voltage equipment pivotal.

- China’s push to move desert solar and northern wind to coastal load centers via UHV AC/DC corridors is a prime driver for HVCBs rated at the highest voltages. For example, State Grid announced a USD 70 billion grid investment in 2024, focused on UHV lines, with multiple projects commencing, amplifying demand for extra-high-voltage substations and breaker fleets.

- India’s Green Energy Corridor programs are scaling interstate and intrastate transmission to evacuate about 33 GW+ of renewables, requiring substantial high-voltage substations and breakers. For instance, in October 2023, the Cabinet approved GEC Phase II ISTS for a 13 GW Ladakh project using HVDC and EHVAC systems, including 5 GW terminals at Pang and Kaithal, demonstrating strong near-term procurement for HVCBs.

- Regulatory auctions and multilateral financing are accelerating high-voltage buildouts, increasing HVCB demand in substations and interties. For example, Brazil signed contracts in April 2024 for 4,471 km of lines and 9,840 MVA in substations from the December 2023 ANEEL auction; and AfDB approved Kenya’s Transmission Network Improvement Project in July 2023, both backing high-voltage equipment needs.

High Voltage Circuit Breaker Market Trends

- OEMs and utilities are prioritizing SF-free technologies (e.g., fluoroketone, dry air) to meet tightening climate policies and ESG goals. This transition elevates demand for compatible high-voltage circuit breakers and retrofit kits, alongside updated maintenance practices. For instance, the UK’s Ofgem Strategic Innovation Fund advanced projects to remove insulating gas SF across transmission networks in 2024–2025, funding feasibility and beta-phase demonstrations that accelerate commercial deployment.

- Utilities are embedding sensors, analytics, and digital twins into substations to enable predictive maintenance, faster fault location, and optimized breaker duty cycles. This boosts demand for digitally enabled HVCBs and monitoring systems. For example, National Grid’s SIF-funded projects in 2024–2025 include AC/DC cable health monitoring and decision-support platforms for future scenarios, demonstrating regulator-backed momentum toward data-driven asset management.

- Surging renewables and storage have outpaced grid integration capacity, making HVCBs central to relieving constraints via new lines, uprates, and station reinforcements. For example, the IEA’s 2023 global stocktake shows grids becoming a bottleneck, calling for modernization and expanded corridors to sustain clean energy transitions, directly implying more high-voltage switching equipment across transmission nodes.

- Planning frameworks increasingly convert long-term blueprints into “actionable” transmission portfolios, accelerating procurement of high-voltage components. For instance, Australia’s AEMO 2024 Integrated System Plan declared over USD 5 billion of new actionable projects and outlines about 10,000 km of lines by 2050, supported by financing reforms and Rewiring the Nation concessional funds, stimulating substation builds and HVCB purchases.

- ENTSO E’s TYNDP 2024/2025 indicates substantial increases in interconnection and storage to reduce system costs, promoting large transformer bays and HVCBs for interties and offshore hubs. For example, the draft TYNDP highlights that by 2040, 108 GW of additional cross-border capacity would be beneficial, with each euro of grid investment saving over two euros, driving procurement of high-voltage switchgear across multiple jurisdictions.

- Even where new line mileage lags, utilities are spending at record levels on reliability upgrades, reconductoring, and station equipment, sustaining HVCB demand. For example, U.S. analyses in 2024–2025 show over USD 25 billion year in transmission spending and a DOE-documented need for approximately 57% grid growth by 2035, underscoring continued buildout of high-voltage protection assets.

- National outlooks foresee electrification and renewable growth reshaping grids, requiring modern high-voltage substations and breakers to manage higher flows and variability. For instance, Canada Energy Regulator’s 2023 “Energy Future” scenarios project electricity taking a lead role under net zero, implying expanded clean generation and transmission with earlier sector decarbonization milestones, supporting sustained HVCB upgrades and deployments.

- Japan and other Asian economies are revisiting master plans for interregional coordination, HVDC links, and storage integration amid data center growth and battery deployments, requiring advanced HVCBs. For example, Japan’s OCCTO aggregated 2024 supply plans and METI is reviewing cross-regional grid strategies that envisage HVDC corridors and multi-trillion-yen investment, expanding breaker installations at new interties and substations.

High Voltage Circuit Breaker Market Analysis

Learn more about the key segments shaping this market

- Based on product, the industry is segmented into air circuit breaker, gas circuit breaker, vacuum circuit breakers and others. The vacuum circuit breaker market holds a share of about 53% in 2025 and is projected to grow at a growth rate of over 7% through 2035.

- Vacuum circuit breakers are gaining dominance due to their environmentally friendly design, eliminating greenhouse gases like SF. Global sustainability mandates and carbon reduction targets are accelerating their adoption, particularly in renewable energy projects and smart grid applications where eco-efficiency is a priority. Their minimal environmental impact, combined with high reliability and low maintenance requirements, positions vacuum breakers as a preferred solution for utilities seeking compliance with stringent emission regulations and long-term operational sustainability.

- Vacuum breakers offer exceptional reliability and minimal maintenance, making them ideal for medium-to-high voltage networks. Their growing use in renewable integration and industrial grids supports rapid adoption in voltage classes above 72.5 kV. As utilities expand transmission capacity to accommodate rising electricity demand and variable renewable generation, vacuum breakers provide robust performance and cost efficiency. This trend is reinforced by their compatibility with digital monitoring systems, enabling predictive maintenance and improved grid resilience.

- Gas-insulated circuit breakers dominate in ultra-high-voltage networks and harsh environments such as offshore wind farms and desert solar projects. Their sealed design ensures superior insulation and protection against moisture, dust, and contaminants, making them indispensable for projects requiring compact, high-performance solutions. As renewable installations expand into challenging terrains, demand for gas breakers continues to rise, supported by their ability to deliver reliable switching under extreme conditions and maintain operational integrity in mission-critical transmission systems.

- Gas circuit breakers are essential for substations in space-limited areas, such as urban centers or mountainous regions, where compact GIS layouts are critical. Their ability to integrate multiple components within a small footprint makes them ideal for high-density environments. For example, Japan’s METI-backed 2024 grid upgrade plan emphasizes GIS substations for constrained sites, reinforcing the role of gas breakers in modern transmission networks. This trend aligns with global urbanization and the need for efficient land utilization in power infrastructure.

- Air circuit breakers are widely deployed in urban substations due to their reliability and ease of maintenance. As cities expand and electrification accelerates, utilities are upgrading transmission and distribution systems to meet rising demand. Air breakers offer proven performance for high-voltage switching in metropolitan environments, ensuring safety and operational continuity. Their adaptability to modern protection schemes makes them essential for reinforcing city grids, particularly in regions investing heavily in smart infrastructure and urban energy resilience.

- Aging infrastructure in developed economies requires modernization, and air circuit breakers provide a cost-effective retrofit option. Their simpler design and lower installation costs compared to gas-insulated systems make them attractive for utilities seeking budget-friendly upgrades without compromising reliability. These breakers are ideal for replacing outdated equipment in substations, improving operational safety and compliance with modern standards. As utilities prioritize lifecycle cost optimization, air breakers remain a preferred choice for refurbishment projects across mature power networks.

- Advanced breaker designs support flexible AC/DC grids and dynamic load balancing, enabling utilities to manage complex power flows efficiently. For instance, ENTSO-E’s 2024 TYNDP highlights hybrid AC/DC nodes for cross-border integration, driving demand for innovative breaker technologies in future-ready transmission systems. These solutions enhance grid flexibility, improve fault isolation, and support digital substations, making them critical for next-generation networks that prioritize resilience, automation, and interoperability across diverse energy sources.

Learn more about the key segments shaping this market

- Based on end use, the industry is bifurcated into industrial, commercial and utility. The utility scale high voltage circuit breaker market holds a share of 64.6 % in 2025 and is set to reach over USD 4.8 billion by 2035.

- Utilities dominate the high-voltage circuit breaker market as they lead large-scale transmission projects to integrate renewable energy and meet rising electricity demand. Their focus on grid reliability and resilience drives significant investments in substations and switching equipment. With global decarbonization targets and electrification trends, utilities require advanced breakers for fault protection and automation, ensuring stable operations across vast networks. This segment’s share of 64.6% in 2025 reflects its critical role in modernizing power infrastructure worldwide.

- Utility-scale projects benefit from strong policy support and financing programs aimed at accelerating energy transition. Governments and regulators are prioritizing grid modernization through initiatives like HVDC corridors, interconnections, and smart substations. These programs create sustained demand for high-voltage circuit breakers in transmission networks. For example, Australia’s Rewiring the Nation initiative allocates billions for new transmission lines and substations, reinforcing the utility sector’s dominance in breaker procurement for future-ready grids.

- Industrial facilities such as steel, cement, and chemical plants require robust high-voltage protection systems to manage large power loads and ensure operational safety. As industries adopt electrification and renewable integration to reduce emissions, demand for advanced circuit breakers grows. These breakers enable reliable switching and fault isolation in high-capacity networks, supporting uninterrupted production and compliance with stringent safety standards. Industrial modernization and energy efficiency programs further accelerate adoption of high-voltage breakers in manufacturing hubs globally.

- The rapid expansion of data centers and semiconductor manufacturing drives demand for high-voltage infrastructure to support continuous, high-quality power supply. Circuit breakers play a vital role in protecting sensitive equipment and maintaining uptime in these critical facilities. With global investments in digitalization and cloud services, industrial end-users increasingly deploy advanced breakers with smart monitoring capabilities. This trend strengthens the industrial segment’s contribution to market growth, particularly in regions with strong technology and IT ecosystems.

- Commercial complexes, airports, and large institutional facilities require reliable high-voltage systems for uninterrupted power. As urbanization accelerates, demand for circuit breakers in commercial substations grows to support HVAC systems, elevators, and lighting loads. Smart building initiatives and energy efficiency regulations further drive adoption of advanced breakers with digital monitoring features, ensuring safety and operational continuity in high-density environments.

- The rise of electric vehicle charging infrastructure and electrified public transport systems creates new opportunities for high-voltage circuit breakers in commercial settings. Large campuses, malls, and transit hubs need robust protection systems to manage fluctuating loads and prevent outages. Investments in sustainable mobility and green infrastructure amplify this trend, making commercial installations an emerging growth area for high-voltage breaker manufacturers worldwide.

")

Looking for region specific data?

- The U.S. high voltage circuit breaker market was valued at USD 351.6 million, USD 389.5 million and USD 428 million in 2023, 2024 and 2025 respectively, reflecting steady grid investment and electrification. A key near-term driver is the modernization of transmission substations to handle renewable integration and rising data center loads, which requires reliable fault interruption, reclosing, and automation, sustaining demand for advanced breakers across utility, industrial, and commercial networks.

- Europe’s energy transition emphasizes interconnectivity and offshore integration, driving demand for high-voltage breakers in new substations and interties. For instance, ENTSO E’s January 2025 draft TYNDP highlights that every USD 1 invested in grids saves USD 2 in system costs, urging rapid reinforcement of cross-border links and storage. This strategic focus accelerates procurement of advanced breakers for interconnection nodes, ensuring stability and flexibility as Europe scales renewable generation and electrification across multiple member states.

- Ontario’s industrial growth and SMR projects require robust transmission capacity, boosting breaker installations. For example, in June 2025, Ontario announced approximately 160 km of new and upgraded transmission lines to support manufacturing and nuclear expansion. These projects aim to strengthen reliability and meet rising load demands, creating significant opportunities for high-voltage circuit breakers in substations and interconnection points as Canada advances toward a cleaner and more resilient electricity system.

- India’s push for renewable integration and green hydrogen hubs drives HVDC and EHVAC expansion, increasing breaker demand. For example, the National Electricity Plan (2024) targets adding 191 thousand circuit kilometers of transmission lines and 33 GW HVDC capacity by 2032. This massive infrastructure build-out will require advanced high-voltage circuit breakers for new substations and inter-regional corridors, ensuring grid stability and supporting India’s ambitious clean energy transition goals.

- Brazil’s concession auctions stimulate substation construction and breaker procurement. For instance, ANEEL’s October 2025 auction offered 1,081 km of transmission lines and 2,000 MVA of substation capacity, attracting approximately USD 1 billion in investment. These projects aim to expand renewable integration and urban grid reliability, creating a strong pipeline for high-voltage circuit breaker installations across multiple states and reinforcing Brazil’s commitment to modernizing its power infrastructure.

- Saudi Arabia’s growing electricity demand and interconnection projects fuel breaker installations. For example, SEC’s Q1 2025 report noted revenue growth linked to new transmission assets and progress on the 3 GW Saudi.Egypt link. These developments highlight the Kingdom’s focus on expanding grid capacity and resilience, driving demand for advanced high-voltage protection systems in substations and interconnection points to support regional energy security.

- The UAE invests in advanced grid technologies to enhance stability and renewable integration. For instance, Abu Dhabi’s TRANSCO commissioned the nation’s largest STATCOM and two phase-shifting transformers in late 2024, enabling tighter control over renewable flows and reducing transmission losses. These upgrades require high-voltage circuit breakers for reactive power systems and substation modernization, reinforcing the UAE’s commitment to building a resilient and efficient electricity network.

- Türkiye’s modernization program focuses on HVDC readiness and SCADA upgrades, driving breaker demand. For example, the World Bank approved over USD 730 million in 2025 for the Transforming Power Transmission System Project, enabling new substations, digital control systems, and preparatory work for HVDC corridors. These initiatives will significantly increase the need for high-voltage circuit breakers to ensure reliable operation and support Türkiye’s growing renewable energy integration.

- The UK’s offshore wind expansion requires major grid reinforcements and breaker fleets. For instance, the ESO “Beyond 2030” report proposes USD 78 billion investment to connect 21 GW of offshore wind by 2035, including new onshore and offshore transmission infrastructure. This large-scale development will drive substantial demand for high-voltage circuit breakers in substations and converter stations, ensuring system reliability and flexibility as the UK accelerates its clean energy transition.

High Voltage Circuit Breaker Market Share

- The top five companies, ABB, GE Vernova, Hitachi Energy, Schneider Electric, and Mitsubishi Electric, collectively account for approximately 40% of the global high-voltage circuit breaker market share in 2025, reflecting their strong technological capabilities and extensive global presence.

- ABB holds a substantial share due to its leadership in eco-efficient and digital switchgear solutions. Its portfolio includes SF-free high-voltage circuit breakers, hybrid systems, and advanced monitoring technologies. ABB’s strong focus on sustainability and smart grid integration positions it as a preferred supplier for utilities and industrial projects worldwide, supported by its global service network and innovation in grid automation.

- GE Vernova commands a significant market share through its expertise in high-voltage AC and HVDC systems. Its product landscape features advanced gas-insulated and hybrid breakers designed for ultra-high-voltage applications. GE’s strong presence in large-scale transmission projects and its ability to deliver integrated solutions for renewable integration and grid modernization make it a key player in the industry.

- Hitachi Energy excels in ultra-high-voltage technologies and HVDC systems, enabling long-distance renewable power transfer. Its portfolio includes gas-insulated, air-insulated, and eco-efficient breakers tailored for complex grid environments. The company’s commitment to digital substations and energy transition solutions strengthens its competitive edge, ensuring reliable performance for global transmission networks and reinforcing its substantial market share.

High Voltage Circuit Breaker Market Companies

- Siemens Energy’s USD 46.01 billion FY2025 revenue and USD 162.37 billion backlog signal scale, delivery capacity, and long-term visibility, key ingredients for preferred vendor status in high-voltage switchgear. Utilities value partners that can fund capacity, execute globally, and de-risk schedules; Siemens’ Grid Technologies momentum reinforces that trust. Its SF free Blue live-tank circuit breakers combine clean air insulation with vacuum interruption, aligning with tightening F-gas rules and sustainability mandates, another pull factor for procurement teams seeking future-proof assets.

- CG Power’s approximate USD 1.10 billion FY24–25 sales, coupled with strong order inflow highlighted in its annual report and analyst coverage, underpin production resilience and service reach, vital for utility and EPC confidence. Its portfolio of EHV/HV SF circuit breakers (live/dead tank) and GIS up to 800 kV meets IEC/ANSI standards, enabling compact, reliable substations for dense or harsh sites. This breadth, spanning MV to UHV, helps CG win diverse bids and sustain market presence in India and export geographies.

- Hyosung Heavy’s USD 3.39 billion sales and USD 154 million net income in 2024 reflect healthy margins and execution, supporting ongoing capacity investments and global deliveries. Its GIS/GCB lineup to 800 kV, with certifications from KEMA/CESI, offers sealed, compact designs and low leakage, an advantage in coastal, urban, or corrosive environments. Proven performance across more than 40 countries strengthens bid credibility and lifecycle support, reinforcing competitive positioning in the high-voltage circuit breaker market.

- Powell’s USD 1.10 billion FY 2025 revenue and USD 1.4 billion backlog demonstrate robust demand from utilities, data centers, and industrials, translating into predictable production runs and service scale. Its PowlVac/Power/Vac vacuum circuit breakers (up to 38 kV, 63 kAIC) with onboard/remote racking reduce outage risk and maintenance, attractive for transmission-adjacent MV substations and grid-tie projects. That blend of performance and safety keeps Powell on shortlists where reliability, operability, and turnaround times shape procurement outcomes.

- Toshiba’s first-half FY2025 USD 2.02 billion net income and USD 739 million operating income underscore financial recovery and capacity to invest in T&D solutions. Its VK/HVK vacuum breakers (5–15 kV), with axial magnetic field interrupters, deliver compact, low-surge switching, while GIS/GCB offerings to 1100 kV serve dense, high-capacity substations. The dual portfolio lets Toshiba address both MV grid nodes and EHV hubs, maintaining presence across project tiers and geographies where performance, footprint, and lifecycle support win bids.

Major players operating in the high voltage circuit breaker market are:

- ABB

- CG Power & Industrial Solutions

- GE Vernova

- Hitachi Energy

- Honle Group

- Hyosung Heavy Industries

- Liyond

- Mitsubishi Electric

- Powell Industries

- Pfiffner Group

- Schneider Electric

- Siemens Energy

- TE Connectivity

- Toshiba International

- Zhejiang Tengen Electric

- Zhejiang Zhegui Electric

- Zhiyue Group

High Voltage Circuit Breaker Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Size in 2026 | USD 3.9 Billion |

| Forecast Period 2026 - 2035 CAGR | 7.4% |

| Market Size in 2035 | USD 7.4 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Expansion of Smart Grid Networks | Smart grids require advanced monitoring, automation, and fault management, which depend on reliable high-voltage circuit breakers for protection and control. As utilities modernize networks with digital technologies and renewable integration, demand for HVCBs rises to ensure stability and safety in complex, interconnected systems. |

| Increasing Electricity Demand | Rising consumption from industrialization, urbanization, and electrification of transport drives the need for new transmission infrastructure. High-voltage circuit breakers are essential for managing higher loads and maintaining grid reliability, making them critical components in expanding power systems worldwide. |

| Refurbishment & Retrofit of Existing Grid Infrastructure | Aging transmission networks in developed and emerging economies require upgrades to meet modern standards and integrate renewables. Retrofitting substations with advanced high-voltage circuit breakers enhances operational safety, efficiency, and compliance, creating a steady replacement market alongside new installations. |

| Pitfalls & Challenges | Impact |

| High Initial Capital Costs | High-voltage circuit breakers involve significant upfront investment for procurement, installation, and integration into substations. These costs can strain utility budgets, especially in emerging markets, delaying projects or limiting adoption despite long-term reliability benefits. Financial constraints often hinder modernization efforts, slowing overall market growth potential. |

| Opportunities: | Impact |

| Integration of Renewable Energy | The global shift toward clean energy requires extensive transmission infrastructure to connect remote renewable plants. This creates strong demand for advanced HVCBs to ensure grid stability and manage variable power flows efficiently. |

| Digitalization and Smart Monitoring | Utilities are adopting IoT-enabled and predictive maintenance solutions for substations. Incorporating smart HVCBs with sensors and analytics offers opportunities for manufacturers to deliver value-added products that improve reliability and reduce downtime. |

| Expansion in Emerging Economies | Rapid urbanization and industrial growth in Asia, Africa, and Latin America are driving large-scale transmission projects. These regions present significant opportunities for HVCB suppliers to meet rising electricity demand and modernize aging infrastructure. |

| Market Leaders (2025) | |

| Market Leaders |

Over 12% |

| Top Players |

|

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Latin America |

| Emerging Country | U.S., Germany, Italy, China & Japan |

| Future outlook |

|

What are the growth opportunities in this market?

High Voltage Circuit Breaker Industry News

- In October 2025, CG Power’s board approved USD 83 million greenfield switchgear plant in Western India, designed to double MV/EHV capacity and produce EHV circuit breakers/GIS, substation automation, and power electronics. Planned on 35 acres with a 72,000 m² built-up area, completion is targeted within 33 months, boosting domestic supply and exports for large utility/EPC projects.

- In September 2025, Hyosung announced a roadmap to expand SF free high-voltage circuit breakers (GIS) using C4-FN gas, targeting 145 kV by 2026 and 800 kV by 2030. The plan builds on commercialization achievements and positions Hyosung as a key supplier of low-carbon HV breakers, aligning with global decarbonization and regulatory trends for eco-efficient switchgear.

- In March 2022, National Grid selected Siemens Energy’s SF free “Blue” 145 kV circuit breakers for an Ayer, Massachusetts substation upgrade, replacing fluorinated gases with clean-air insulation and vacuum switching. The project, commissioning in 2023, marked a major U.S. deployment of zero-GWP HV breakers, reinforcing utility confidence in eco-efficient technology and supporting net-zero goals.

- In June 2021, Toshiba Energy Systems & Solutions and Meidensha agreed to jointly develop SF free GIS (72/84 kV) using dry-air insulation and a vacuum circuit breaker, aiming for type tests by March 2022 and commercialization by March 2023. The collaboration advances low-GWP GIS and integrates VCB technology to meet performance and reliability standards while reducing environmental impact.

The high voltage circuit breaker market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) and volume (‘000 Units) from 2022 to 2035, for the following segments:

Market, By Product

- ACB

- GCB

- VCB

- OCB

Market, By End Use

- Commercial

- Industrial

- Utility

The above information has been provided for the following regions & countries:

- North America

- U.S.

- Canada

- Mexico

- Europe

- Germany

- France

- Italy

- UK

- Russia

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Middle East & Africa

- Saudi Arabia

- UAE

- Qatar

- Oman

- South Africa

- Latin America

- Brazil

- Chile

Frequently Asked Question(FAQ) :

What is the market size of the high voltage circuit breaker in 2025?

The market size was USD 3.5 billion in 2025, with a CAGR of 7.4% expected through 2035 driven by expanding transmission infrastructure and renewable energy integration.

What is the projected value of the high voltage circuit breaker market by 2035?

The high voltage circuit breaker market is expected to reach USD 7.4 billion by 2035, propelled by smart grid deployment, renewable integration, and global decarbonization targets.

What is the current high voltage circuit breaker market size in 2026?

The market size is projected to reach USD 3.9 billion in 2026.

How much revenue did the vacuum circuit breaker segment generate in 2025?

Vacuum circuit breakers held 53% market share in 2025, driven by their environmentally friendly design and minimal maintenance requirements.

What was the valuation of utility end-use segment in 2025?

Utility scale held 64.6% market share and is set to reach over USD 4.8 billion by 2035.

What is the growth outlook for vacuum circuit breakers from 2025 to 2035?

Vacuum circuit breakers are projected to grow at over 7% CAGR through 2035, due to sustainability mandates, low maintenance needs, and compatibility with digital monitoring systems.

Which region leads the high voltage circuit breaker market?

The U.S. high voltage circuit breaker market was valued at USD 428 million in 2025, supported by steady grid investments and electrification.

What are the upcoming trends in the high voltage circuit breaker market?

Key trends include adoption of SF₆-free technologies, digitalization with predictive maintenance, renewable integration bottlenecks driving grid modernization, and actionable transmission planning frameworks.

Who are the key players in the high voltage circuit breaker market?

Key players include ABB, CG Power & Industrial Solutions, GE Vernova, Hitachi Energy, Honle Group, Hyosung Heavy Industries, Liyond, Mitsubishi Electric, Powell Industries, Pfiffner Group, Schneider Electric, Siemens Energy, TE Connectivity, Toshiba International, Zhejiang Tengen Electric, Zhejiang Zhegui Electric, and Zhiyue Group.

High Voltage Circuit Breaker Market Scope

Related Reports