Authors:

Avinash Singh, Sunita Singh

Download free PDF

Greenhouse Ventilation Systems Market Size & Share 2026-2035

Report ID: GMI16076

|

Published Date: June 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Greenhouse Ventilation Systems Market

Get a free sample of this report

Get a free sample of this report Greenhouse Ventilation Systems Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Greenhouse Ventilation Systems Market Size

The greenhouse ventilation systems market was valued at USD 1.03 billion in 2025, with rising global food security concerns accelerating controlled environment agriculture (CEA) adoption. The market is projected to advance from USD 1.15 billion in 2026 to USD 2.13 billion by 2035, representing a compound annual growth rate (CAGR) of 7.1% over the forecast period, according to the latest report published by Global Market Insights Inc.

Greenhouse Ventilation Systems Market Key Takeaways

Market Leader: Priva B.V. led with over 2.3% market share in 2025.

Leading Players: Top 5 players in this market include Priva B.V, BioTherm Solutions, Argus Controls (CEL Group), Ridder Group, Pinnacle Climate Tech, which collectively held a market share of 7.8% in 2025.

Greenhouse Ventilation Systems Market Trends

IoT, AI & Sensor-Driven Smart Greenhouse Ventilation Systems

One of the major advancements being made in the field of greenhouse ventilation system technology includes the fast embracement of Internet of Things (IoT), Artificial Intelligence (AI), and other sensor-based solutions that allow complete automation and smart functionality. The traditional approach to climate control involved manual adjustments and mechanical processes, which could not ensure the desired efficacy. However, with modern ventilation systems using data obtained from sensors of temperature, humidity, CO₂, and other factors, such systems can maintain an ideal environment inside the greenhouse through constant modification of climate control parameters. Through IoT connectivity, these systems can be remotely controlled through cloud-based interfaces, allowing management of several greenhouse units at once.

The implementation of artificial intelligence (AI) and machine learning in ventilation algorithms improves their efficiency through the analysis of past and current environmental data in order to predict climate changes and improve ventilation systems' performance. Energy savings, cost reduction, and increased crop yields are some of the advantages that come along with such systems. Moreover, preventive maintenance allows the prediction of failures within systems in advance, which helps ensure uninterrupted greenhouse work. Smart ventilation technology enables farmers to apply precise agriculture techniques where environmental parameters are adjusted to the needs of particular crops. Greenhouses will become more data-driven in the future, making it necessary for them to use such technologies.

Retrofit and Modernization of Aging Greenhouse Infrastructure

Another notable factor that will influence the growth of the greenhouse ventilation systems market is the need for retrofitting and updating the existing greenhouse infrastructures. A considerable number of greenhouse buildings in developed regions like Europe and North America have been in operation for decades and use outdated ventilation systems. Such systems are not only energy-intensive but also cannot be automated and controlled. As energy prices grow, farmers will have an urgent need to update their greenhouse facilities.

Retrofitting refers to the replacement of traditional manually operated vents and ventilators with energy-efficient systems equipped with various sensors. Retrofitting allows improving climatic conditions, boosting crop production, and minimizing costs without the necessity of rebuilding the entire facility. Moreover, governments stimulate such actions as part of their sustainable development initiatives.

Nonetheless, retrofits also come with various technical challenges, such as compatibility concerns regarding old greenhouse designs and structural restrictions that call for unique engineering solutions. Regardless, the economic and ecological advantages are ensuring high adoption. With the increasing importance of sustainability within the agricultural sector, retrofits are anticipated to be one of the reliable growth drivers, especially among mature markets with existing greenhouse facilities.

Shift Toward Energy-Efficient and Climate-Neutral Greenhouse Operations

One major trend in the greenhouse ventilation systems market is the move towards greater energy efficiency in order to achieve zero emissions from greenhouses. Energy usage is among the major expenses incurred during greenhouse farming activities. This is attributed to the constant need for heating, cooling, and ventilation in greenhouse farming.

Modern greenhouse ventilation systems are characterized by various features such as the use of variable speed fans, an automated natural ventilation system, and a heat recovery system. In some cases, energy saving is achieved through the use of renewable energy resources such as geothermal power. In addition, there is an increased adoption of greenhouse technologies that make use of renewable energy.

Further, energy-efficient ventilation systems allow the growers to obtain certification for their sustainability practices, which plays an increasingly crucial role in the modern global food supply chain. Not only will this approach minimize harm to the environment, but it will also contribute to making the business more profitable due to savings on utility expenses. The growing concerns regarding climate change and unstable energy prices are expected to make these innovations the key trend in the future of the industry.

Greenhouse Ventilation Systems Market Analysis

Based on ventilation type, the market is categorized into natural ventilation, mechanical ventilation, and hybrid ventilation. The mechanical ventilation accounted for revenue of around USD 560 million in 2025 and is anticipated to grow at a CAGR of 7.1% from 2026 to 2035.

Based on application consists of commercial greenhouses, horticulture greenhouses, research & educational, and residential greenhouses. the commercial emerged as leader and held 56.86% of the total market share in 2025 and is anticipated to grow at a CAGR of 7.7% from 2026 to 2035.

By Region

North America Greenhouse Ventilation Systems Market

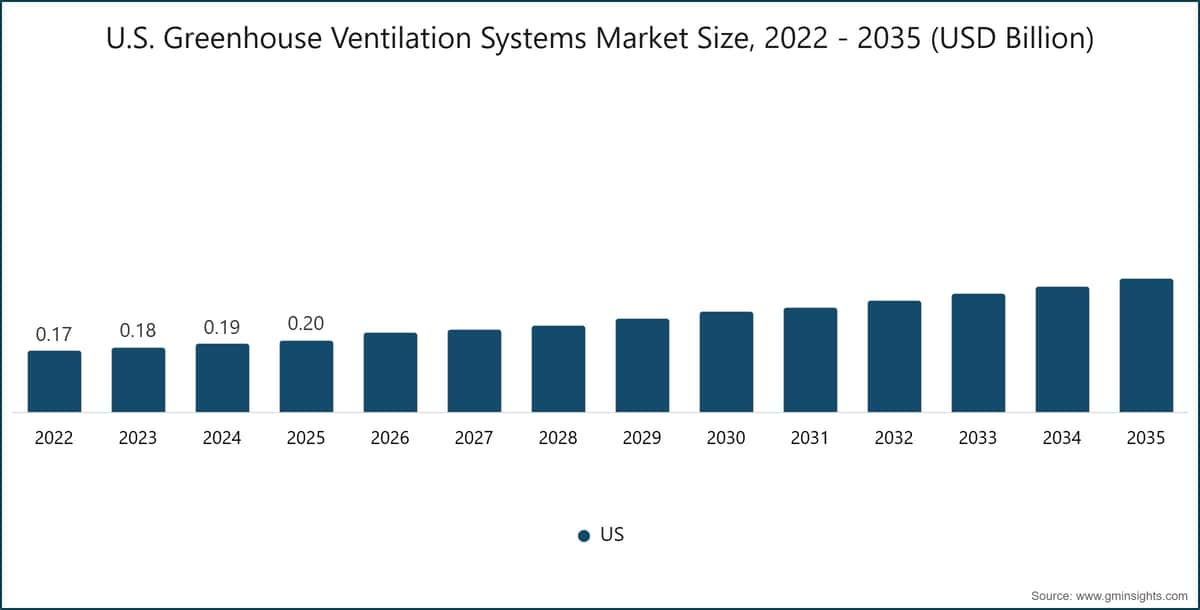

North America is leading the regional growth by generating 210 million in revenue in 2025 and expected to grow with 5.8% due to the rapid pace of innovation, large-scale commercial agriculture farms, and demand for quality pesticide-free products. The US hold 95.1% market share in 2025, allocates substantial resources to the development of controlled agriculture, especially in states such as California and Arizona, and Canadian provinces where winters are severe.

One of the most distinctive features of the North American market is the intensive use of automation. Agricultural enterprises in the region actively use highly sophisticated greenhouse technology with ventilation control, climate monitoring using IoT technology, and artificial intelligence to enhance agricultural productivity and decrease reliance on the labor force.

Demand for organically grown produce, locally available produce, and produce available throughout the year is yet another important growth factor. The retail chains and food service firms are increasingly looking towards greenhouse-produced vegetables and fruits in order to ensure a steady supply of produce.

On the other hand, growth is tempered by heavy investment in capital goods and lengthy returns periods, limiting the ability of the market to grow as fast as that of APAC. The market does not focus on expanding its market but rather on upgrading technology and improving efficiency.

Europe Greenhouse Ventilation Systems Market

Europe is seen as the most developed region by holding 25.57% market share in 2025, with regard to controlled environment agriculture and advanced greenhouse technology because of its early integration of precision farming systems, aggressive regulatory policy that promotes sustainable agriculture, and a wide diffusion rate for cultivation under protective systems.

In Europe, countries like the Netherlands, Spain, France, Germany, and Italy have been utilizing their greenhouse facilities, having invested heavily in climate regulation technologies, irrigation system automation, and energy-efficient facilities.

Specifically, the Netherlands is a world leader in innovative practices and technologies, with its products exported worldwide. In addition, European farmers are constrained by small amounts of farmable land, cold weather conditions, and stringent environmental policies.

Furthermore, there is an incentive through the use of government subsidies for sustainable farming and carbon reduction initiatives that have spurred investments in agricultural technology infrastructure. Europe is also advantaged by the fact that there are leading firms and research institutions that continually develop new technologies for greenhouse automation and ventilation systems. This has ensured that, despite its moderate rate of growth, Europe has remained ahead in terms of market share and technology innovation.

Asia Pacific Greenhouse Ventilation Systems Market

The Asia Pacific region is the fastest-growing region with a CAGR of 8% and is expected to lead the market in the upcoming years due to rapid population growth, high food demands, less arable land, and the increasing adoption of advanced agricultural technologies. Nations such as China, India, Japan, South Korea, and Australia are increasingly adopting greenhouse farming to improve yield productivity and ensure crop availability throughout the year.

Another factor that drives the adoption of greenhouse farming in the APAC is that of food security. This is because traditional agriculture within the APAC relies significantly on monsoons, which makes greenhouse production a dependable choice. The governments of China and India are supporting this trend through subsidies and training of farmers.

Cost-competitiveness is yet another critical factor. The availability of labor at a comparatively lower rate when compared with other regions like Europe or North America makes the scaling of greenhouse infrastructure possible quickly. Furthermore, the uptake of technology in hybrid ventilation systems, which is cost-effective, has increased tremendously, making them extremely favorable in APAC due to its diverse climatic conditions.

Urbanization has been crucial in this sector as well. Urban areas are demanding fresh produce, and this has led to the growth of vertical farming practices. Alongside robust investment from both government and private sectors, APAC is registering the highest compound annual growth rate worldwide, thereby acting as the primary engine of growth of the market.

Greenhouse Ventilation Systems Market Shares

Priva B.V is leading with 2.3% market share. Priva B.V, BioTherm Solutions, Argus Controls (CEL Group), Ridder Group, Pinnacle Climate Tech collectively hold around 7.8%indicating fragmented market concentration. These prominent players are proactively involved in strategic endeavors, such as mergers & acquisitions, facility expansions & collaborations, to expand their product portfolios.

Greenhouse Ventilation Systems Market Companies

Munters Group AB: Munters specializes in air handling and climate control equipment designed for greenhouses and industries. These include manufacturing of dehumidifiers, energy-saving ventilation systems, and air circulation technologies. Munters’ technologies are utilized in greenhouses to control humidity, reduce the incidence of crop disease and regulate climate conditions in large commercial greenhouses. Additionally, the company offers services in the areas of system design, installation and after market service for controlled environment agriculture.

Vostermans Ventilation B.V.: Vostermans specializes in manufacturing of axial fans and air circulation equipment for greenhouses and other agriculture uses. Operations in this company are mainly focused on designing, manufacturing and distributing fans that create a continuous flow of air in greenhouses. The company also designs and manufactures custom air circulation systems for livestock and industry. The manufacturing process in Vostermans is highly technology oriented.

2.3% market share

The collective market share in 2025 is 7.8%

Greenhouse Ventilation Systems Industry News

Greenhouse ventilation systems market research report includes in-depth coverage of the industry, with estimates & forecasts in terms of revenue (USD Billion) volume (Thousand Units) (from 2022 to 2035), for the following segments:

Click here to Buy Section of this Report

Market, By Ventilation Type

Market By Component

Market, By Installation Type

Market, By Application

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Ventilation Type, 2022 - 2035 (USD Billion) (Thousand Units)

Chapter 6 Market Estimates and Forecast, By component, 2022 - 2035 (USD Billion) (Thousand Units)

Chapter 7 Market Estimates and Forecast, By Installation Type, 2022 - 2035 (USD Billion) (Thousand Units)

Chapter 8 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

Chapter 9 Market Estimates & Forecast, By Region, 2022 – 2035, (USD Billion) (Thousand Units)

Chapter 10 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →