Authors:

Preeti Wadhwani, Aishvarya Ambekar

Download free PDF

Data Center Refrigerant Market Size & Share 2026-2035

Report ID: GMI10746

|

Published Date: April 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Data Center Refrigerant Market

Get a free sample of this report

Get a free sample of this report Data Center Refrigerant Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Data Center Refrigerant Market Size

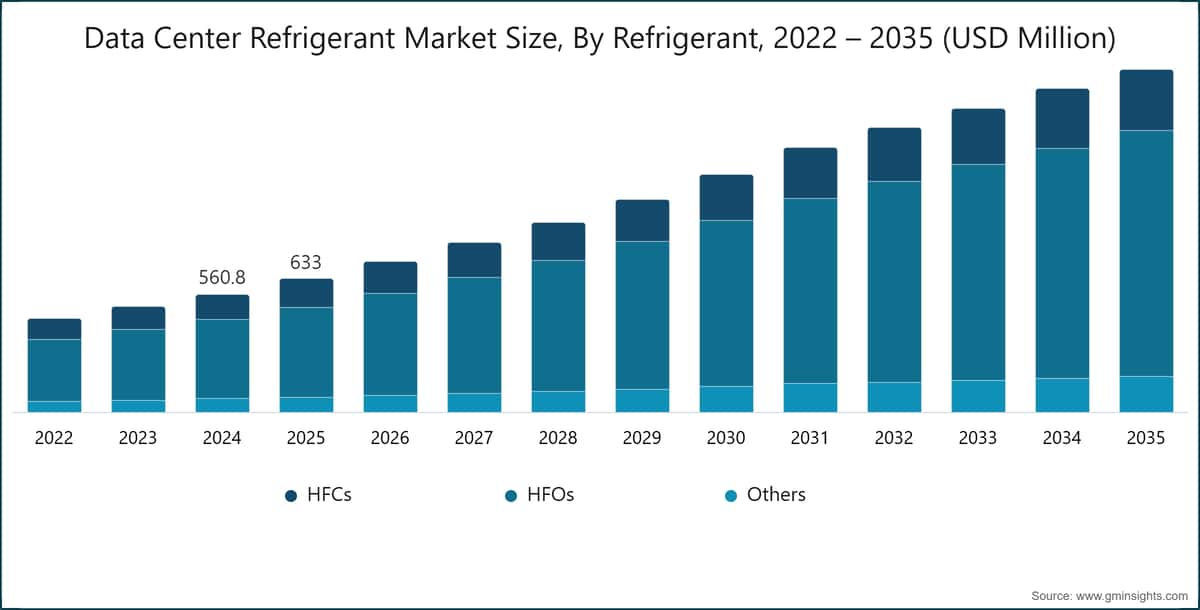

The global data center refrigerant market was estimated at USD 633 million in 2025. The market is expected to grow from USD 714.5 million in 2026 to USD 1.62 billion in 2035, at a CAGR of 9.6%, according to latest report published by Global Market Insights Inc.

Data Center Refrigerant Market Key Takeaways

Market Leader: Honeywell led with over 22.28% market share in 2025.

Leading Players: Top 5 players in this market include Arkema, Chemours, Daikin Industries, Dongyue, Honeywell, which collectively held a market share of 69.04% in 2025.

The rapid expansion of digital infrastructure, driven by cloud computing, hyperscale data center growth, and increasing data consumption, is significantly transforming the market. Traditionally reliant on high-GWP refrigerants and conventional air-based cooling, the market is evolving toward advanced, energy-efficient, and environmentally sustainable cooling solutions. Modern data centers, including enterprise, colocation, and hyperscale facilities, increasingly depend on high-performance refrigerants to manage rising thermal loads, ensure operational reliability, and optimize energy usage in high-density computing environments.

Growing environmental concerns and stringent regulatory frameworks are accelerating the transition toward low-global warming potential refrigerants. Regulations such as the Kigali Amendment and region-specific policies are pushing operators to phase out traditional HFCs in favor of HFOs and natural refrigerants. Compliance requirements related to refrigerant emissions, leakage control, and lifecycle management are becoming critical, prompting organizations to adopt advanced refrigerant technologies that align with sustainability goals while maintaining system efficiency.

Rising emphasis on energy efficiency and operational cost optimization is further reshaping the market. Cooling systems account for a significant share of data center energy consumption, leading operators to invest in next-generation refrigerants that enhance heat transfer efficiency and reduce power usage effectiveness (PUE). The integration of refrigerants with innovative cooling architectures such as liquid cooling, immersion cooling, and hybrid systems is gaining traction, particularly in facilities supporting AI and high-performance computing workloads

For instance, in February 2025, Vertiv launched its global Liquid Cooling Services portfolio to support deployment, integration, and maintenance of liquid cooling systems in AI and hyperscale data centers. The initiative focuses on improving efficiency and enabling large-scale adoption of advanced thermal management architectures.

The increasing scale and complexity of data center operations are driving the adoption of integrated and scalable cooling ecosystems. Operators are moving toward centralized and modular cooling solutions that leverage advanced refrigerants for improved efficiency and flexibility. This shift supports large-scale deployments, reduces operational complexity, and enhances system reliability across geographically distributed data center networks.

Technological innovation plays a transformative role in redefining refrigerant applications and cooling system performance. Advanced developments such as AI-driven thermal management, smart monitoring systems, and optimized refrigerant cycles are improving cooling efficiency and reducing environmental impact. Additionally, innovations in chiller design, heat exchangers, and refrigerant blends are enabling better performance in high-density and mission-critical environments.

Sustainability has become a central focus in the data center refrigerant market, driven by corporate ESG commitments and global climate targets. Operators are prioritizing refrigerants with ultra-low GWP, adopting closed-loop cooling systems, and implementing heat recovery solutions to minimize environmental impact. Alignment with global standards and green building certifications is further encouraging the adoption of sustainable refrigerant technologies across new and existing data center facilities.

North America and Europe represent mature markets for the data center refrigerant industry, supported by stringent environmental regulations, strong focus on energy efficiency, and early adoption of low-global warming potential refrigerants. The presence of leading hyperscale operators, advanced cooling infrastructure, and strict compliance frameworks such as the Kigali Amendment continue to drive innovation, system upgrades, and the transition toward sustainable refrigerant solutions across these regions.

Asia-Pacific is the fastest-growing market for data center refrigerants, driven by rapid expansion of digital infrastructure, increasing cloud adoption, and rising demand for high-performance computing. Countries such as China, India, Japan, and Southeast Asian nations are witnessing strong investments in hyperscale and colocation facilities, creating significant demand for energy-efficient and environmentally compliant cooling technologies.

Data Center Refrigerant Market Trends

The market is undergoing a major transition toward low-global warming potential (GWP) refrigerants due to increasing environmental regulations and sustainability commitments. Policies such as the Kigali Amendment are accelerating the phase-down of high-GWP HFCs. Data center operators are adopting HFOs and natural refrigerants to reduce carbon emissions while maintaining cooling efficiency. This shift is also driving innovation in refrigerant formulations and system compatibility, ensuring compliance without compromising performance.

For instance, in February 2025, Vertiv Holdings Co. launched a global liquid cooling services portfolio designed to support AI and high-density computing environments, improving cooling efficiency and enabling scalable deployment of advanced thermal management systems.

The rise of high-density computing workloads, including AI and high-performance computing, is driving the adoption of liquid and hybrid cooling technologies. These systems offer superior heat dissipation compared to traditional air cooling, enabling efficient thermal management in compact environments. Refrigerants play a critical role in supporting these advanced cooling systems by enhancing heat transfer efficiency. As data centers continue to scale, liquid and hybrid cooling solutions are becoming essential for maintaining operational stability and energy efficiency.

Artificial intelligence is increasingly being integrated into data center cooling systems to optimize refrigerant usage and improve thermal management. AI-driven platforms analyze real-time data on temperature, workload, and system performance to dynamically adjust cooling operations. This enables predictive maintenance, reduces energy consumption, and enhances overall system reliability. By optimizing refrigerant flow and cooling cycles, AI technologies help operators achieve better efficiency and lower operational costs in complex data center environments.

Energy efficiency has become a critical priority for data center operators, with a strong focus on reducing power usage effectiveness (PUE). Advanced refrigerants are being adopted to improve cooling system performance and lower energy consumption. Efficient thermal management helps reduce operational costs while supporting sustainability goals. As energy demand from data centers continues to rise, optimizing PUE through innovative refrigerant technologies and cooling strategies is becoming a key factor driving market growth.

A significant number of existing data centers rely on outdated cooling systems and high-GWP refrigerants. To meet regulatory requirements and improve efficiency, operators are increasingly retrofitting legacy infrastructure with modern refrigerants and advanced cooling technologies. This process enhances performance, reduces emissions, and extends the operational lifespan of facilities. Retrofitting also provides a cost-effective alternative to building new data centers, making it an attractive option for organizations aiming to modernize their operations.

Data Center Refrigerant Market Analysis

Based on refrigerant, the market is divided into HFCs, HFOs, and Others. The HFOs segment dominated the data center refrigerant market, accounting for around 67.7% in 2025 and is expected to grow at a CAGR of more than 10.2% through 2035.

Based on data center, the market is categorized into enterprise, colocation, cloud, and hyperscale. The hyperscale segment dominates the market accounting for around 40% share in 2025, and the segment is expected to grow at a CAGR of over 10.4% from 2026-2035.

Based on cooling, the data center refrigerant market is divided into air cooling, liquid cooling, and free cooling providers. The air cooling segment held the major market share in 2025.

Based on application, the data center refrigerant market is divided into IT cooling system, and facility cooling system. The IT cooling system segment dominated the market.

U.S. dominated the data center refrigerant market in North America with around 79% share and generated USD 176.3 million in revenue in 2025.

The data center refrigerant market in Germany is expected to experience significant and promising growth from 2026 to 2035.

The data center refrigerant market in China is expected to experience significant and promising growth from 2026-2035.

The data center refrigerant market in Brazil is expected to experience significant and promising growth from 2026 to 2035.

The data center refrigerant market in UAE is expected to experience significant and promising growth from 2026-2035.

22.28% market share

Collective Market Share in 2025 is 69.04%

Data Center Refrigerant Market Share

Data Center Refrigerant Market Companies

Major players operating in the data center refrigerant industry are:

Data Center Refrigerant Market News

The data center refrigerant market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($Bn), from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Refrigerant

Market, By Data Center

Market, By Cooling

Market, By Application

Market, By End Use

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Refrigerant, 2022 - 2035 ($Bn)

Chapter 6 Market Estimates & Forecast, By Data Center, 2022 - 2035 ($Bn)

Chapter 7 Market Estimates & Forecast, By Cooling, 2022 - 2035 ($Bn)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Bn)

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →