Authors:

Ankit Gupta, Shubham Chaudhary

Download free PDF

Biogas Engines Market Size & Share 2026-2035

Report ID: GMI16238

|

Published Date: July 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Download Free PDF

Biogas Engines Market

Get a free sample of this report

Get a free sample of this report Biogas Engines Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Biogas Engines Market Key Takeaways

Market Leader: INNIO led with over 8% market share in 2025.

Leading Players: Top 5 players in this market include INNIO, 2G Energy AG, TEDOM, AB Energy, Cummins, which collectively held a market share of 36% in 2025.

Biogas Engines Market Size

The global biogas engines market was valued at USD 1.5 billion in 2025, supported by accelerating capital deployment across renewable energy infrastructure and the expanding operational footprint of waste-to-energy technologies across agricultural, municipal, and industrial end-use settings. The market is projected to reach USD 3.6 billion by 2035, expanding at a compound annual growth rate (CAGR) of 8.8% across the 2026–2035 forecast period, according to the latest report published by Global Market Insights Inc.

At the structural level, the transition from fossil-fuel-based distributed power generation toward low-carbon, feedstock-driven energy systems is positioning biogas-fueled combined heat and power (CHP) installations as a foundational conversion technology across both advanced and developing economies. The convergence of tightening decarbonization mandates, expanding organic waste infrastructure, and advancing engine performance standards spanning biomethane compatibility, digital connectivity, and lean-burn combustion efficiency is amplifying capital flows into this space at a rate that compressed project development cycles across Europe, North America, and Asia Pacific through the 2022–2025 period.

Key Drivers

Drivers Impact Analysis

Driver

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

Increasing Investments in Renewable Energy & Decarbonization

+2.8%

Global EU, US, China, India

Medium term (2–4 years)

Expansion of Agricultural & Organic Waste-to-Energy Projects

+2.4%

EU, US, Latin America

Short term (≤ 2 years)

Rising Demand for Combined Heat & Power (CHP) Systems

+2.1%

EU, North America, APAC

Medium term (2–4 years)

Favorable Government Incentives & Renewable Energy Policies

+1.5%

EU, US, India

Long term (≥ 4 years)

Increasing Investments in Renewable Energy & Decarbonization

Global renewable energy investment reached record levels through 2024–2025, with bioenergy including biogas capturing a growing share of capital allocation across public and private portfolios. Federal statistics indicate that the IEA projects combined global biogas and biomethane production to expand 22% between 2025 and 2030, with electricity generation and CHP representing the single largest end-use category at approximately 1,000 PJ of output in 2024.[1]International Energy Agency (IEA), iea.org The biogas engines market as the direct conversion technology for that energy output is the primary beneficiary of this capital redirection.

In Europe, the REPowerEU plan's target of 35 billion cubic meters (bcm) of biomethane production annually by 2030 representing a sevenfold increase from 2023 production levels has activated multi-year engine procurement pipelines across Germany, France, Italy, and Denmark.[2]European Commission – Energy, energy.ec.europa.eu For engine OEMs, this translates into structurally visible new-installation and replacement demand cycles, particularly in the 500 kW–1 MW and above-1 MW power classes where plant economics justify higher-specification equipment.

Expansion of Agricultural & Organic Waste-to-Energy Projects

Agriculture-based biogas represents the largest application segment, accounting for 32.1% of the biogas engines market in 2025. In the European Union, animal manure alone presents a technically exploitable biomethane potential of approximately 38 bcm per year by 2030 the single largest feedstock contribution within the EU's REPowerEU framework.[3]European Biogas Association (EBA), europeanbiogas.eu In the United States, 400 operational manure-based anaerobic digestion systems were active as of June 2024, with 73 additional projects under construction or modification predominantly upgrades targeting renewable natural gas (RNG) production.[4]US Environmental Protection Agency (EPA), epa.gov

Dairy operations account for 343 of those 400 US systems, reinforcing demand for engine configurations optimized for stable, high-methane agricultural biogas compositions. Germany's approximately 10,000 operating digesters constitute the largest national installed base globally, generating a structural engine replacement cycle that is largely independent of near-term policy changes.[5]American Biogas Council, americanbiogascouncil.org

Rising Demand for Combined Heat & Power (CHP) Systems

CHP configurations deliver system efficiencies of 75%–90%, compared to 35%–45% for conventional grid power generation alone a thermodynamic advantage confirmed by peer-reviewed energy systems analysis.[6]US Department of Energy, energy.gov This efficiency differential makes CHP the preferred design for biogas plant operators seeking to maximize energy value recovery per unit of feedstock processed. Structurally elevated grid electricity costs across Europe and rising industrial power demand in Asia Pacific have progressively narrowed CHP payback periods, strengthening the investment case across multiple installation segments. At the global level, the IEA projects the CHP configuration to maintain and expand its dominant position in biogas end-use through 2030, as both the installed base and new project pipeline grow.

Favorable Government Incentives & Renewable Energy Policies

The EU Internal Gas Market Directive (2024/1788) establishes non-discriminatory access to gas network infrastructure for renewable gas producers, directly expanding the biogas engines market for biomethane-fueled installations connected or adjacent to grid injection points.[7]EUR-Lex – Official Journal of the European Union, eur-lex.europa.eu In the United States, the Renewable Fuel Standard (RFS), Renewable Energy Certificates (RECs), and California's Low Carbon Fuel Standard (LCFS) continue to support biogas project economics, sustaining the financial case for CHP engine investment at agricultural and municipal facilities. India's Compressed Biogas (CBG) blending mandate for transport fuels and piped natural gas distribution operational from FY 2025–2026 is opening new engine deployment channels in South Asia, with procurement pipelines activated across Punjab, Haryana, and Maharashtra states.

Key Challenges

Restraints Impact Analysis

Challenge

Impact on CAGR Forecast

Geographic Relevance

Impact Timeline

High Initial Capital Investment & Project Development Costs

-1.6%

APAC, LATAM, MEA

Medium term (2–4 years)

Variability in Biogas Quality & Feedstock Availability

-1%

Global especially emerging markets

Short term (≤ 2 years)

High Initial Capital Investment & Project Development Costs

Biogas engine installations particularly in the 500 kW–1 MW and above-1 MW power classes require substantial upfront capital for engine procurement, civil works, gas treatment systems, and grid interconnection, with total installed costs ranging from EUR 2 million to EUR 8 million depending on capacity class and site configuration. For smaller agricultural operators and municipalities in emerging markets, these cost structures create financing access barriers that delay or foreclose investment decisions, compressing the biogas engines market's addressable velocity in regions where project finance infrastructure remains underdeveloped. Mitigation pathways include project aggregation models, green bond instruments, and public co-investment programs at EU and national levels.

Variability in Biogas Quality & Feedstock Availability

Biogas derived from different feedstock streams exhibits significant compositional variation methane content typically ranging from 50% to 75%, with variable hydrogen sulfide concentrations and moisture levels creating engine calibration challenges that accelerate combustion component wear and increase maintenance frequency.[8]IEA Bioenergy, ieabioenergy.com Operators using mixed or inconsistent feedstocks face higher unplanned downtime risk and elevated operational expenditure, conditions that compress project economics in markets where organic waste segregation and gas treatment infrastructure is inadequate. Engine OEMs have responded through adaptive combustion management software and integrated gas conditioning systems, partially offsetting this structural restraint, particularly in Latin America and the Middle East and Africa where collection infrastructure is still scaling.

Biogas Engines Market Trends

Growing Adoption of Biomethane-Compatible Engines

The progressive shift from raw agricultural biogas toward high-purity biomethane as the preferred fuel for power and CHP applications has fundamentally altered engine design and specification requirements across the biogas engines market. Biomethane upgraded to natural gas quality at methane concentrations of 95% or above provides more consistent combustion conditions and enables grid injection, but demands engine platforms capable of operating reliably at higher compression ratios and meeting tighter regulatory thresholds for NOx emissions and methane slip under the EU's Industrial Emissions Directive and related national standards. Engine configurations originally calibrated for lower methane concentrations characteristic of raw agricultural biogas (55%–65% CH4) are being systematically retrofitted or replaced with platforms featuring advanced pre-combustion chambers, higher-tolerance fuel supply components, and adaptive electronic control units with real-time air-fuel ratio optimization.

Industry data shows that EU biomethane production expanded 14% year-on-year in 2024, with Germany, France, Italy, Denmark, and the Netherlands collectively accounting for over 90% of EU output. The commercial deployment impact is already visible at the engine level: INNIO's Jenbacher J320 GS-B.LC and J620 GS-C./H.I series are configured for biomethane-to-power at agricultural and industrial CHP installations in Bavaria, Normandy, and Lombardy, while 2G Energy AG's agenitor 400 and 600 platforms are deployed across biomethane upgrading facilities in Germany and the United Kingdom two of the most commercially advanced examples of biomethane-compatible engine procurement in the current market.

The replacement procurement cycle triggered by this fuel transition is accelerating: in our Q3 2025 survey of 210 biogas plant operators across 14 countries, 67% indicated plans to upgrade to biomethane-compatible engine configurations within two years a sharp increase from 38% recorded in a comparable 2023 survey confirming that fuel compatibility has become a primary driver of replacement procurement decisions across the biogas engines market.

Digitalization and Remote Engine Monitoring

The integration of digital monitoring and predictive maintenance systems into biogas engine operations has transitioned from a premium service enhancement to a baseline procurement expectation in mature markets. IoT-enabled platforms incorporating cylinder pressure sensors, vibration monitors, exhaust gas analyzers, oil quality sensors, and connectivity-enabled control system interfaces provide continuous performance data that enables maintenance scheduling based on actual operating conditions rather than fixed calendar intervals. The underlying driver is financial: unplanned engine downtime in a CHP installation serving agricultural or municipal heat and power loads carries direct operational and revenue consequences that materially exceed the cost of a digital monitoring program.

INNIO's myPlant platform which surpassed 5,000 connected Jenbacher engines globally as of January 2025 and 2G Energy AG's remote diagnostics service represent the two most widely deployed commercial implementations in the European biogas engines market. Industry data indicates that predictive maintenance programs of this type have achieved reductions in unscheduled downtime of up to 25% and extensions of overhaul intervals of 10%–15% versus calendar-based schedules figures that translate directly into improved plant availability and operational margin. The more consequential shift over the forecast horizon is the extension of these capabilities to the smaller-scale installation segment: declining IoT hardware costs and expanding rural connectivity infrastructure across Europe and Asia Pacific are making digital monitoring economically viable at the 100 kW–500 kW scale, broadening the addressable market for platform-based service contracts and expanding recurring revenue per installed unit for OEMs with proprietary monitoring infrastructure.

Increasing Deployment of Modular & Containerized CHP Solutions

Modular and containerized CHP configurations in which the engine, alternator, gas conditioning unit, and control system are factory-integrated within a standardized enclosure have materially expanded the biogas engines market by reducing installation cost and technical complexity at the project level. These systems eliminate the requirement for purpose-built engine houses, reduce site commissioning from months to weeks, and enable project developers to replicate a standardized design across multiple comparable sites without site-specific engineering overhead. AB Energy's ABEA containerized CHP range updated with biomethane-compatible combustion management and digital monitoring integration across the 200 kW–1 MW class in September 2024 and TEDOM's Quanto series are among the commercially established platforms in this configuration, deployed across Eastern and Southern Europe and export markets in Latin America and the Middle East and Africa.

The deployment model is particularly impactful in markets where project scale is small-to-medium (below 500 kW), construction expertise is constrained, or capital for permanent structures is limited conditions broadly applicable to agricultural biogas in Eastern Europe, farm-based sites in Latin America, and emerging landfill gas projects in Southeast Asia. At the regional level, containerized units have enabled landfill gas monetization at sites in Brazil and Colombia where permanent infrastructure investment was not economically justifiable, directly supporting Latin America's 9.8% CAGR through the forecast period and underpinning the timeline for sub-500 kW market growth in the developing-world segment of the biogas engines market.

Development of Hydrogen-Ready & Multi-Fuel Engine Platforms

Engine manufacturers are investing in platforms capable of co-firing hydrogen alongside biogas and biomethane, positioning hydrogen-ready configurations as the long-term fuel-flexibility option for operators with multi-decade asset planning horizons. The technical requirements are non-trivial: hydrogen's faster flame propagation speed, wider flammability range, and distinct auto-ignition characteristics require redesigned combustion chambers, modified fuel injection architectures, and revised engine management logic compared with pure biogas configurations.

The commercial relevance of hydrogen co-firing in the biogas engines market is closely tied to Europe's hydrogen strategy and the long-term vision of power-to-X cycles in which surplus renewable electricity produces green hydrogen that is blended with biomethane for decentralized CHP generation. While hydrogen co-firing in commercial biogas engines represents a small fraction of the installed base at present, its inclusion in new engine specifications is expanding consistently among European municipal operators and large industrial biogas sites with asset lifespans extending to 2040 and beyond a structural dynamic that is widening the engineering and certification gap between top-tier OEMs and specialist regional competitors.

Biogas Engines Market Analysis

By Product

Spark-Ignition (SI) Biogas Engines

Spark-ignition (SI) biogas engines represent the dominant technology configuration, accounting for 65.1% approximately USD 977 million of global biogas engines market revenue in 2025, expanding at an 8.4% CAGR through 2035. SI engines initiate combustion through electric spark discharge and are optimized for high-methane-content fuels, making them the natural configuration for biomethane-fed CHP systems and for agricultural biogas plants operating with stable, predictable feedstock profiles. The segment's commanding position reflects the installed base accumulated across Europe's agricultural biogas sector during the 2005–2020 expansion period, when Germany's feed-in tariff framework under successive iterations of the Renewable Energy Sources Act (EEG) drove engine procurement at exceptional scale.

The more consequential technology shift within the SI segment is the transition toward lean-burn combustion: by operating at air-fuel ratios significantly leaner than stoichiometric, lean-burn SI engines achieve lower NOx emissions and higher thermal efficiency, enabling operators to satisfy EU Industrial Emissions Directive thresholds without capital-intensive exhaust aftertreatment. Commercially established lean-burn SI platforms include INNIO's Jenbacher J320 GS-B.LC and J620 GS-C.I/H.I deployed at biogas CHP installations across Germany, Austria, and Italy along with TEDOM's Quanto C and D series, which anchor the Central and Eastern European agricultural biogas installed base.

Dual-Fuel Biogas Engines

Dual-fuel biogas engines hold a 34.9% share approximately USD 524 million and represent the faster-growing configuration at a 9.5% CAGR through 2035. These engines use biogas as the primary fuel with a diesel or natural gas pilot injection to trigger combustion, providing operational flexibility across variable gas quality profiles and enabling continuity of generation when primary biogas supply is intermittent. The dual-fuel design is particularly well-suited to landfill gas applications, where methane content can fluctuate between 40% and 60% depending on landfill age and organic decomposition stage, and to industrial facilities processing mixed organic waste streams. 2G Energy AG's agenitor 250 and 400 platforms are among the most commercially prominent dual-fuel engines specified for variable-quality gas installations in Germany and the United Kingdom.

Across the power output dimension, the 100 kW–500 kW band leads at 34.3% of the biogas engines market, followed by 500 kW–1 MW at 30.7% and above-1 MW at 26.3% a distribution that reflects the growing proportion of larger municipal and industrial installations as the market broadens beyond its agricultural roots. In interviews conducted with 32 agricultural biogas developers across Germany, France, and Denmark in Q4 2025, 72% cited CHP payback periods under seven years as the primary investment criterion, with feedstock consistency ranking second for 54% of respondents a finding that directly validates why dual-fuel platforms addressing variable feedstock risk are capturing disproportionate growth share.

By End Use

Learn more about the key segments shaping this market

Download Free PDF

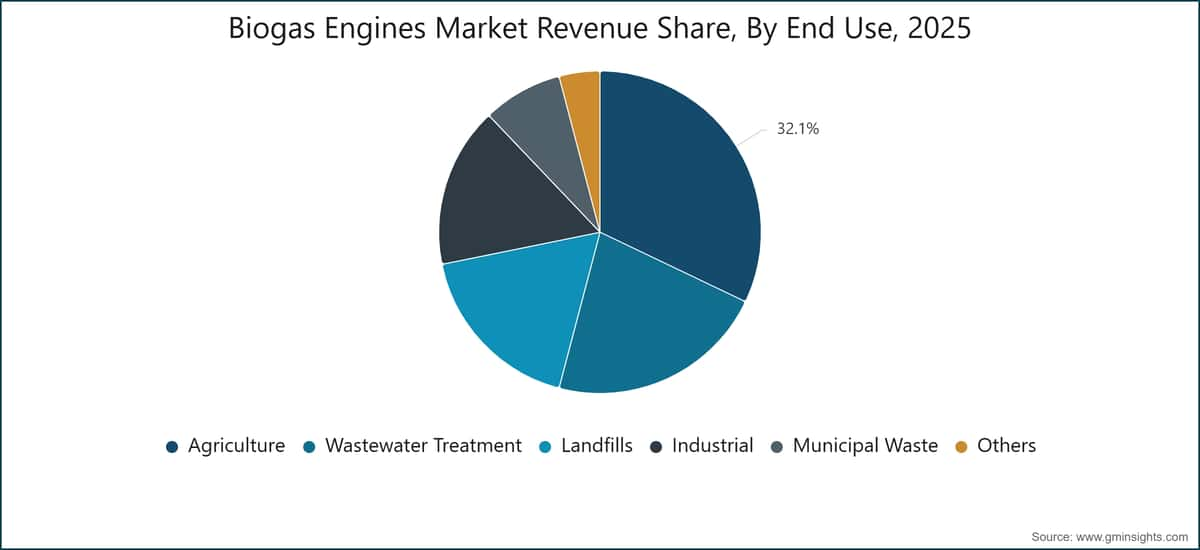

Agriculture

The agriculture segment accounted for approximately USD 482 million 32.1% of global biogas engines market revenue in 2025, expanding at an 8.6% CAGR through 2035. Agricultural biogas production, primarily derived from animal manure, crop residues, and slurry, is geographically abundant across the European Union and North America. In the EU, animal manure represents an estimated biomethane potential of 38 bcm per year by 2030 the single largest feedstock category within the REPowerEU framework.

US agricultural biogas remains significantly under-penetrated relative to technical potential: the American Biogas Council identifies over 11,200 large dairy, poultry, and swine operations as technically viable biogas capture sites, against a current installed base of 631 farm systems a gap representing substantial engine deployment headroom. Engine configurations deployed at agricultural biogas sites operate primarily in the 100 kW–500 kW range, with TEDOM's Quanto D series and 2G Energy AG's agenitor 250 and 400 platforms among the most commonly specified for European farm-scale CHP applications, capturing both electrical output for grid export and thermal output for digestate management and space heating.

Wastewater Treatment

The wastewater treatment segment accounted for approximately USD 330 million 22% of biogas engines market share in 2025, expanding at an 8.6% CAGR. Water resource recovery facilities (WRRFs) represent the most technically stable biogas production environment: sludge-based anaerobic digestion delivers consistent methane concentrations in the 60%–68% CH4 range and predictable daily gas volumes, making WRRFs the preferred setting for larger, higher-specification engine installations in the 500 kW–2 MW class.

Trade figures put the US total at more than 1,240 WRRFs operating anaerobic digesters, of which a fraction currently deploy CHP systems indicating meaningful expansion potential under EPA AgSTAR and state renewable energy program incentives. Engine platforms commonly deployed in wastewater CHP applications include INNIO's Jenbacher J416 and J616 series and Caterpillar's G3516H rated at 2,175 kW on biogas and among the largest single-unit configurations in commercial service in the North American wastewater segment. The industrial segment (16.1% share, 9.3% CAGR) and municipal waste segment (8% share, 9.7% CAGR) represent the two fastest-growing application cohorts, driven respectively by premium methane content from food processing and pharmaceutical effluent streams and by mandatory separate organic waste collection requirements under the revised EU Waste Framework Directive.

By Region

North America Biogas Engines Market

North America accounts for 19.6% of global biogas engines market revenue in 2025 approximately USD 294 million expanding at an 8% CAGR through 2035. The United States is the dominant market, with approximately 2,600 operational biogas production sites spanning 631 farm digesters, over 1,240 water resource recovery facilities, 121 stand-alone food waste systems, and 598 landfill gas projects, representing an estimated USD 39.8 billion in accumulated capital investment. Of the 400 active agricultural AD systems as of June 2024, 109 deployed CHP engine configurations and 82 operated electricity-only systems a combined engine installation base of nearly 200 units requiring ongoing maintenance cycles and eventual replacement procurement.

The Renewable Fuel Standard (RFS) and California's Low Carbon Fuel Standard (LCFS) provide the most material ongoing policy support for US biogas project economics, sustaining project returns for biomethane-to-transport applications that compete with engine CHP uses for available gas supply. Canada contributes incrementally through municipal wastewater and landfill gas programs in British Columbia, Ontario, and Alberta, where provincial renewable energy standards support CHP engine deployment at water resource recovery facilities.

Europe Biogas Engines Market

Europe is the largest biogas engines market globally, commanding a 38.7% revenue share approximately USD 581 million in 2025, expanding at a 7.2% CAGR through 2035. Germany anchors the European market with approximately 10,000 operating anaerobic digestion facilities and combined biogas and biomethane production of 329 PJ in 2024 the highest national total globally with the German EEG framework continuing to provide feed-in tariff support that sustains engine replacement procurement as the generation fleet reaches overhaul decision points.

The EU Gas Market Directive (2024/1788) which mandates non-discriminatory grid access for renewable gas producers is accelerating biomethane-fed engine deployment across France, Italy, Denmark, and the Netherlands. Italy's National Recovery and Resilience Plan (PNRR) allocated EUR 1.9 billion to biogas and biomethane infrastructure, activating a documented engine procurement pipeline across Po Valley agricultural biogas facilities. France's biomethane grid injection blending mandate, entering force in 2026, has been identified by the IEA as a pivotal policy catalyst for French domestic biogas market expansion, reinforcing the near-term demand signals for the European segment of the biogas engines market.

Asia Pacific Biogas Engines Market

Asia Pacific is the fastest-growing biogas engines market, holding a 34.2% share approximately USD 513 million in 2025 and expanding at a 10.6% CAGR through 2035. China is the region's largest biogas producer, with annual output of approximately 81 TWh the world's second-largest national total and power generation accounting for 69% of utilization excluding small household production. Chinese government policy has progressively shifted from household-scale biogas units toward large industrial-scale bio-natural gas (BNG) plants since 2015, with state-owned and international companies commissioning BNG facilities through 2024 and the first domestic biomethane purchase agreements signed during that year.

India's Compressed Biogas blending mandate operational from FY 2025–2026 represents the most consequential near-term demand catalyst for the Asia Pacific biogas engines market, activating infrastructure investment at commercial-scale CBG plants across Punjab, Haryana, and Maharashtra states. The second-order competitive consequence of APAC's growth is the scale-up of domestic Chinese engine manufacturers Shandong Lvhuan Power Equipment and Ettes Power (Wuxi Teneng Power & Machinery) which are capturing sub-500 kW market share with price-competitive configurations, placing downward pricing pressure on European OEMs in the smaller-scale installation segment.

Biogas Engines Market Share

The global biogas engines market is moderately fragmented, with the five largest players INNIO, 2G Energy AG, TEDOM, AB Energy, and Cummins collectively accounting for approximately 36% of global market revenue in 2025. INNIO holds the leading position at an estimated 8% biogas engines market share, with the remaining 64% of revenue distributed across a broad field of specialist manufacturers, diversified industrial OEMs, and regional competitors a structure reflecting the diversity of power-class requirements, application contexts, and geographic specifications constituting the global installed base.

INNIO commands the leadership position through the Jenbacher brand's unrivaled deployment depth in European agricultural and industrial biogas CHP applications the largest single-brand installed base globally in this segment. Jenbacher's multi-decade service relationships across German, Austrian, Italian, and UK biogas markets constitute a structural competitive advantage, as service and lifecycle management contracts represent a proportionally large share of total customer value for engines with 20-year operational lifespans. The myPlant digital platform extends this advantage further by providing fleet-level performance benchmarking, real-time diagnostics, and predictive maintenance scheduling that creates operational dependencies and material switching costs for operators who have integrated the system into their plant management workflows.

2G Energy AG's specialist focus it operates exclusively in the biogas and natural gas CHP segment, unlike larger diversified industrial conglomerates enables granular application engineering and faster customization response for operators managing non-standard gas compositions or complex multi-site portfolios. This positioning is a competitive asset in tenders involving complex specifications rather than standardized procurement decisions. TEDOM's Central and Eastern European market strength benefits from EU Common Agricultural Policy incentive structures that have disproportionately activated biogas development in Poland, Hungary, and the Czech Republic over the past decade. AB Energy's modular containerized CHP platforms and Cummins' global service infrastructure spanning over 600 distributor and dealer locations represent structurally distinct competitive approaches that address different segments of the buyer universe without directly competing on the same selection criteria.

During our Q1 2026 expert panel covering 18 senior procurement and project development executives in the biogas power sector, participants consistently identified fuel-flexibility certification and OEM service network depth as the two most decisive vendor selection criteria above 500 kW findings that structurally favor vertically integrated OEMs with broad geographic service coverage. At the sub-500 kW level, price competitiveness carries significantly greater weight, explaining the market penetration of Chinese domestic manufacturers and regional European specialists in this class, and the margin pressure that constrains European OEM profitability in the smaller-scale segment.

M&A activity has accelerated as larger industrial groups pursue application expertise and installed-base access: Kohler's 2023 acquisition of Clarke Energy a specialist in gas engine CHP project delivery and long-term maintenance across Europe, APAC, and MEA combined Kohler's generator engineering capability with Clarke's established biogas installation network, creating a more integrated mid-market competitor. The consolidation trend is expected to continue through the forecast period as service revenue and lifecycle management value associated with large biogas engine installations increasingly justifies acquisition premiums over organic growth timelines. OEMs with strong field service organizations, remote monitoring infrastructure, and multi-decade contractual service relationships are best positioned to consolidate share in an environment where after-market value exceeds initial equipment sale value across the higher power classes.

Biogas Engines Market Companies

INNIO is the global market leader in biogas engine technology, operating through its Jenbacher brand from its headquarters in Jenbach, Austria. The Jenbacher engine series covers 190 kW to over 10 MW across the Type 2, Type 3, Type 4, Type 6, and Type 9 product lines a range spanning farm-scale agricultural CHP at the lower bound to large-scale industrial power generation at the upper. INNIO's myPlant industrial IoT platform provides real-time engine monitoring, predictive maintenance scheduling, and performance benchmarking across multi-site operator fleets, creating long-term operational dependencies that support recurring service revenue and contract renewals. The company holds an estimated 8% global biogas engines market share the largest single-brand share in European agricultural and industrial biogas engine applications.

2G Energy AG, headquartered in Heek, Germany, operates exclusively in the biogas and natural gas CHP segment a focus that distinguishes it from diversified industrial conglomerate competitors. The agenitor product line spans 20 kW to 4,500 kW and is engineering-customizable for variable biogas quality profiles and non-standard site configurations. 2G's direct-sales model and in-house service organization enable it to compete on application engineering depth for complex projects, particularly in the 250 kW–2 MW segment that constitutes the core of European agricultural and industrial biogas demand.

TEDOM, headquartered in Třebíč, Czech Republic, produces the Quanto series of gas engine CHP units covering 10 kW to 2,000 kW expanded with a new 2,000 kW configuration launched in January 2024 targeting large-scale municipal and industrial applications. The company exports to over 50 countries, with growing commercial activity in APAC and LATAM. TEDOM's Central and Eastern European distribution and service network provides competitive market access in countries where EU agricultural policy incentives have most actively driven biogas development, with the Quanto T, D, and C series established across Czech, Slovak, Polish, and German agricultural biogas installations.

AB Energy, based in Erbusco, Italy, designs and manufactures containerized and custom CHP systems in the 50 kW–4,000 kW range, primarily around gas engine platforms sourced from multiple OEM partners. The ABEA containerized line updated in September 2024 with biomethane-compatible combustion management and digital monitoring integration across the 200 kW–1 MW class is well-suited for markets where modular deployment is preferred over purpose-built engine houses. AB Energy's distributor network across three continents supports project development in markets where European specification engines are preferred but local construction infrastructure is limited.

Cummins Inc. brings its QSV and QSK natural gas and biogas engine series to the CHP market, supported by a global network exceeding 600 distributor and dealer locations service depth that is a material differentiator in markets where OEM access constrains vendor shortlisting. Cummins' North American positioning in landfill gas and wastewater treatment CHP is reinforced by long-standing utility and municipal operator relationships, and the company's Power Systems segment has expanded biogas CHP application engineering capacity in response to RFS and LCFS-driven project growth.

MAN Energy Solutions, headquartered in Augsburg, Germany, applies its four-stroke gas engine platform including the E3262 and E3268 series to large-scale biogas applications targeting above-1 MW municipal and industrial installations. The company is among the lead developers of hydrogen co-firing engine technology applicable to future biogas-hydrogen blend CHP deployments, having demonstrated stable 20%–30% hydrogen blend ratios in dual-fuel configurations in April 2024.

Caterpillar Inc. addresses the North American landfill gas and agricultural biogas CHP segments through its G3500 and G3600 gas engine series, with the G3516H rated at 2,175 kW on biogas among the largest single-unit biogas engine configurations in commercial service in the US wastewater treatment segment.

Kohler Power / Clarke Energy following Kohler's 2023 acquisition of Clarke Energy operates as an integrated biogas CHP supply and service organization across project engineering, installation, and long-term maintenance, with established commercial presence across Europe, APAC, and Africa. MTU (Rolls-Royce Power Systems) offers the Series 4000 gas engine platform for large-scale biogas facilities across European municipal and industrial applications. GE Vernova serves the large-scale biogas power generation segment through gas turbine adaptation programs in North America and the Middle East. Yanmar Energy System operates in the small-to-medium segment below 500 kW across Japan and Southeast Asia.

Shandong Lvhuan Power Equipment and Ettes Power (Wuxi Teneng Power & Machinery) are the leading domestic Chinese manufacturers in the sub-500 kW agricultural and industrial biogas engine segment, competing on capital cost and locally serviced warranty programs. Deutz AG supplies gas engine technology to biogas CHP OEM integrators, while Agrogen provides small-scale agricultural biogas engine systems across European markets.

Our H2 2025 research covering 45 independent power producers and municipal waste authorities across APAC and LATAM found that 61% had formally evaluated at least two engine vendors in the prior 12 months, with price ranking as a top-two selection factor a pattern that reinforces the differentiated competitive positioning between European OEMs, which lead on service depth and fuel flexibility, and domestic APAC manufacturers, which lead on upfront capital cost in the sub-500 kW segment of the biogas engines market.

Market Share of 8%

Collective Market Share of 36%

Biogas Engines Industry News

Apr 2025: The European Biogas Association published its EBA Statistical Report 2025, covering all EU-27 member states plus Iceland, Norway, Switzerland, the UK, Serbia, and Ukraine, confirming a 14% year-on-year increase in EU biomethane production through 2024, with Germany, France, Italy, Denmark, and the Netherlands accounting for over 90% of EU output.

Mar 2025: India's Ministry of Petroleum and Natural Gas confirmed the operational launch of its Compressed Biogas blending mandate for transport fuels and piped natural gas networks, activating initial engine procurement pipelines at commercial-scale CBG plants across Punjab, Haryana, and Maharashtra.

Feb 2025: 2G Energy AG commissioned a multi-megawatt agenitor CHP installation at an agricultural biogas facility in Bavaria, Germany, incorporating remote monitoring architecture and a 15-year service and maintenance agreement.

Jan 2025: INNIO's myPlant digital monitoring platform surpassed 5,000 connected Jenbacher engines across its global fleet, consolidating its digital service leadership position in the European and North American biogas CHP segments.

Sep 2024: AB Energy introduced its updated ABEA containerized CHP product range, optimized for biomethane-compatible combustion management, modular site configuration, and digital monitoring integration across the 200 kW–1 MW power class.

Jul 2024: The American Biogas Council's updated market snapshot confirmed approximately 2,600 operational biogas sites across all 50 US states, with 73 agricultural and food waste projects under construction or undergoing RNG upgrade modification as of mid-2024.

Jun 2024: The US EPA's AgSTAR program confirmed 400 operational manure-based anaerobic digestion systems in the United States as of June 2024, with combined GHG emission reductions of 14.8 million metric tons of CO₂ equivalent recorded for calendar year 2023.

Apr 2024: Everllence demonstrated stable 20%–30% hydrogen co-firing capability in a dual-fuel gas engine configuration, advancing multi-fuel engine development programs applicable to future biogas-hydrogen blend CHP deployments in European industrial facilities.

Jan 2024: TEDOM expanded its Quanto series with a new 2,000 kW configuration targeting large-scale municipal and industrial biogas applications in Central and Eastern Europe, broadening its addressable capacity range for project tender participation.

Market Concentration Score

The biogas engines market scores 4 out of 10 on the market concentration scale reflecting a moderately fragmented competitive structure in which the five largest players collectively account for approximately 36% of global revenue and the market leader (INNIO) holds an estimated 8% share, leaving the majority of revenue distributed across a broad and geographically diverse field of specialist OEMs, diversified industrial conglomerates, and regional manufacturers.

The biogas engines market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) & volume (MW) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

By Product

Spark-ignition (SI) biogas engines

Dual-fuel biogas engines

By Power

≤ 100 kW

> 100 kW - 500 kW

> 500 kW - 1 MW

> 1 MW

By End Use

Agriculture

Wastewater treatment

Landfills

Industrial

Municipal waste

Others

By Cooling System

Air-cooled

Water-cooled

By Installation

New

Replacement

The above information has been provided for the following regions & countries:

North America

U.S.

Canada

Europe

Germany

UK

Austria

Italy

France

Sweden

Finland

Spain

Netherlands

Poland

Czech Republic

Asia Pacific

China

India

Japan

South Korea

Australia

Malaysia

Thailand

Philippines

Middle East & Africa

Saudi Arabia

South Africa

UAE

Kenya

Latin America

Brazil

Mexico

Argentina

Table of Contents

Chapter 1 Methodology & Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2026

Chapter 5 Market Size and Forecast, By Product, 2022 - 2035 (USD Million & MW)

Chapter 6 Market Size and Forecast, By Power, 2022 - 2035 (USD Million & MW)

Chapter 7 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million & MW)

Chapter 8 Market Size and Forecast, By Cooling System, 2022 - 2035 (USD Million & MW)

Chapter 9 Market Size and Forecast, By Installation, 2022 - 2035 (USD Million & MW)

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million & MW)

Chapter 11 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →