Summary

Table of Content

Backside Power Delivery Network Technology Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Backside Power Delivery Network Technology Market Size

The global backside power delivery network technology market was valued at USD 3.1 billion in 2024. The market is expected to grow from USD 3.9 billion in 2025 to USD 37.9 billion in 2034, at a CAGR of 28.7% during the forecast period, according to the latest report published by Global Market Insights Inc. This growth is driven by the increasing demand for advanced semiconductor architectures that enhance power efficiency, reduce signal interference, and improve chip performance in AI, 5G, and high-performance computing applications. The technology’s ability to minimize IR drop and support transistor scaling is fueling its adoption across leading foundries and chipmakers, positioning BSPDN as a key innovation in next-generation semiconductor manufacturing.

Backside Power Delivery Network Technology Market Key Takeaways

Market Size & Growth

- 2024 Market Size: USD 3.1 Billion

- 2025 Market Size: USD 3.9 Billion

- 2034 Forecast Market Size: USD 37.9 Billion

- CAGR (2025–2034): 28.7%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: North America

Key Market Drivers

- Growing demand for advanced semiconductor nodes (below 3nm) requiring improved power efficiency and reduced IR drop..

- Increasing adoption of AI and high-performance computing (HPC) chips driving need for higher transistor density..

- Rising use of mobile and data center processors demanding better power integrity and thermal management..

- Technological innovation by key players like Intel and TSMC accelerating BSPDN commercialization..

Challenges

- Complex integration process and new design methodologies increase development costs..

- Limited manufacturing capacity and dependence on advanced fabs slow large-scale adoption..

Opportunity

- Growing use of BSPDN in AI accelerators, GPUs, and next-generation processors..

- Expansion of 2.5D/3D packaging technologies complementing backside power delivery..

Key Players

- Market Leader: Taiwan Semiconductor Manufacturing Company (TSMC) led with over 28% market share in 2024.

- Leading Players: Top 5 players in this market include Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, Samsung Electronics (Samsung Foundry), Applied Materials, Inc., Lam Research Corporation, which collectively held a market share of 87% in 2024.

Get Market Insights & Growth Opportunities

The shift toward smaller semiconductor nodes, such as 3nm and beyond, is fueling demand for backside power delivery network technology. BSPDN enables improved power routing and reduced IR drop, supporting efficient transistor operation and enhancing chip performance for next-generation processors used in AI, 5G, and high-performance computing applications. For instance, in October 2025, Intel launched Panther Lake, its first AI PC platform built on the advanced 18A process technology, marking a major step in next-generation semiconductor innovation. The platform integrates backside power delivery network (BSPDN) technology to enhance power efficiency, performance, and transistor density. Panther Lake is designed to support AI-intensive workloads and advanced computing applications, positioning Intel at the forefront of energy-efficient chip design and next-gen AI-driven PC architectures.

The growing adoption of artificial intelligence, cloud computing, and large-scale data center operations is driving the need for chips with higher power efficiency and density. BSPDN technology optimizes power distribution and heat management, making it ideal for powering AI accelerators and high-performance GPUs efficiently and reliably. For instance, February 2024, Intel partnered with Cadence and expanded their partnership to advance system-on-chip (SoC) design using Intel’s cutting-edge process technologies, including the 18A node with backside power delivery network (BSPDN). This partnership focuses on optimizing design tools, improving power efficiency, and accelerating time-to-market for high-performance computing, AI, and next-generation semiconductor applications.

Between 2021 and 2023, the backside power delivery network technology market experienced significant growth, rising from USD 1.2 billion in 2021 to USD 2.3 billion in 2023. A major trend during this period was SoC architecture integrates more functional blocks, managing power delivery becomes challenging. BSPDN provides a separate layer for power distribution on the wafer’s backside, improving signal integrity and space utilization. This design innovation enhances chip performance and reliability, supporting the semiconductor industry’s transition to more compact and efficient designs.

Leading semiconductor foundries such as TSMC, Intel, and Samsung are investing heavily in backside power delivery technologies to maintain competitiveness. These investments aim to overcome power delivery bottlenecks and improve transistor scaling efficiency, enabling the production of more powerful and energy-efficient chips across various computing and mobile platforms.

The increasing adoption of 3D packaging and chiplet architectures is accelerating BSPDN implementation. By separating power and signal layers, backside power delivery improves interconnect density and performance in stacked chips. This advancement supports the development of high-performance, compact semiconductor devices used in automotive, IoT, and next-generation computing applications.

To get key market trends

Backside Power Delivery Network Technology Market Trends

- A key trend shaping the backside power delivery network (BSPDN) technology market is the shift toward advanced semiconductor nodes such as 2nm and below, where BSPDN enhances power integrity, reduces IR drop, and improves performance-per-watt. This technology enables efficient power delivery directly through the wafer’s backside, optimizing chip density and performance.

- For instance, in 2025, Intel and Cadence expanded their partnership to develop advanced SoC designs leveraging Intel’s 18A process with BSPDN integration. This collaboration focuses on improving power efficiency, thermal management, and design automation tools, accelerating commercialization of high-performance computing chips for AI, data centers, and edge applications.

- Rising adoption of 3D integration and chiplet architectures is further fueling demand for BSPDN technology. By decoupling power and signal interconnects, BSPDN improves signal integrity and simplifies inter-die communication, making it vital for heterogeneous integration in AI accelerators, GPUs, and networking processors used in high-performance computing systems.

- The transition toward AI-driven workloads, cloud computing, and data-intensive applications is increasing the need for energy-efficient and compact semiconductor designs. BSPDN plays a critical role by reducing power losses and supporting higher transistor density, enabling chipmakers to meet the performance and efficiency requirements of next-generation computing platforms.

- Another major trend is the advancement in wafer processing and metallization techniques for backside routing. Leading foundries such as TSMC and Samsung are investing heavily in developing scalable BSPDN-compatible fabrication methods that improve reliability, reduce defect density, and enable high-yield production for sub-2nm process nodes.

- Investments in advanced EDA software and simulation tools are accelerating the design optimization of BSPDN structures. These tools allow designers to accurately model power delivery paths, optimize via placement, and balance thermal distribution, ensuring robust performance across diverse semiconductor architectures and manufacturing conditions.

- Ongoing collaborations between semiconductor foundries, equipment suppliers, and material science companies are fostering innovation in backside metallization, dielectric materials, and via etching processes. These partnerships are critical to achieving manufacturability, reducing costs, and enhancing scalability for mass production of BSPDN-based chips.

- Thus, with increasing demand for performance scaling beyond Moore’s Law, the backside power delivery network technology market is poised for rapid expansion. Its integration across advanced computing, AI, and 3D packaging ecosystems will redefine chip design, power efficiency, and performance optimization in the semiconductor industry’s next generation.

Backside Power Delivery Network Technology Market Analysis

")

Learn more about the key segments shaping this market

The global market was valued at USD 1.2 billion and USD 1.6 billion in 2021 and 2022, respectively. The market size reached USD 3.1 billion in 2024, growing from USD 2.3 billion in 2023.

Based on the component type, the global backside power delivery network technology industry is divided into manufacturing equipment, materials & consumables, metrology & inspection systems, and design & simulation software. The manufacturing equipment segment accounted for 34.2% of the market in 2024.

- The manufacturing equipment segment holds the largest share in the backside power delivery network technology market due to the high demand for advanced power delivery solutions in manufacturing processes. Manufacturers are increasingly adopting backside power delivery network technologies to improve efficiency, reduce energy consumption, and enhance overall productivity. Additionally, these technologies offer benefits such as improved thermal management, faster data transmission, and higher power density, making them essential for modern manufacturing equipment.

- Manufacturers should focus on investing in advanced power delivery solutions to streamline manufacturing processes and improve operational efficiency. The manufacturing equipment segment currently dominates the market, indicating a strong demand for innovative power delivery solutions in industrial settings.

- The design & simulation software segment of the backside power delivery network technology market, valued at USD 900 million in 2024 and projected to grow at a CAGR of 30.1%, is driven by the growing demand for advanced tools for designing and simulating power delivery networks in electronic devices. This segment is benefiting from the growing complexity of electronics, as well as the need for more efficient and reliable power delivery solutions. The rising adoption of new technologies such as artificial intelligence, Internet of Things, and 5G is also driving the growth of the design & simulation software segment in the market.

- Manufacturers should focus on developing advanced processing units with integrated AI and machine learning capabilities to improve real-time biometric analysis and decision-making. Prioritizing low-power consumption, faster data throughput, and enhanced cybersecurity will help meet automakers’ requirements for reliable, high-performance biometric systems in connected, electric, and autonomous vehicle platforms.

Learn more about the key segments shaping this market

Based on the application, the backside power delivery network technology market is segmented into driver high-performance computing processors, mobile & consumer processors, automotive semiconductor devices, industrial & IoT applications, and others. The high-performance computing processors segment dominated the market in 2024 with a revenue of USD 900 million.

- High-Performance Computing (HPC) processors dominate the market due to their need for efficient, high-density power delivery to support massive computational loads. These processors require advanced packaging solutions like TSVs to minimize latency and maximize bandwidth. As AI, scientific simulations, and data analytics grow, HPC systems demand robust power architectures, making backside power delivery essential. Their complexity and performance requirements drive innovation in power delivery technologies, positioning HPC processors as key drivers of market growth and technological advancement in semiconductor design.

- Manufacturers should focus on optimizing power delivery architectures, enhancing TSV integration, and improving thermal management for HPC processors. Investing in advanced packaging and energy-efficient designs will ensure reliable performance under heavy workloads, helping meet the growing demand for AI, scientific computing, and data-intensive applications in the evolving semiconductor landscape.

- On the other hand, the automotive semiconductor devices segment in the backside power delivery network technology market is anticipated to grow at a CAGR of 30.5% during the forecast period. This growth is driven by the increasing adoption of biometric technologies, such as fingerprint, facial, and voice recognition, to enable secure and seamless in-car transactions. As connected vehicles evolve into digital platforms, biometric semiconductors enhance payment security for fuel, tolls, parking, and infotainment services. Advancements in low-power, AI-integrated sensors and secure processing chips are improving authentication speed and reliability, encouraging automakers and payment providers to integrate biometric payment solutions.

- Manufacturers should focus on developing low-power, AI-integrated biometric sensors and secure processing chips tailored for automotive environments. Enhancing authentication speed, reliability, and system integration will support secure in-car transactions, helping automakers deliver smarter, safer, and more connected vehicle experiences in the rapidly growing automotive semiconductor market.

Based on technology, the backside power delivery network technology market is segmented into through-silicon via (TSV) based systems, buried power rail systems, direct backside contact systems, and hybrid integration systems. The through-silicon via (TSV) based systems segment dominated the market in 2024 with a revenue of USD 600 million.

- Through-silicon via (TSV) based systems account for the largest share of the backside power delivery network technology industry due to their ability to provide high bandwidth and low latency connections between different integrated circuits. TSV technology enables dense integration of components, reducing the need for long power delivery lines and improving overall system efficiency. This makes TSV-based systems ideal for high-performance applications such as data centers, networking equipment, and advanced computing devices. As a result, TSV technology dominates the backside power delivery network market, offering unrivaled performance and scalability.

- Manufacturers should focus on advancing TSV fabrication techniques, optimizing thermal management, and reducing production costs to meet growing demand. By investing in TSV innovation, they can deliver scalable, high-performance solutions for data-intensive applications, ensuring competitiveness in the evolving backside power delivery network market.

- Hybrid Integration Systems are anticipated to witness significant growth at a CAGR of 29.7% over the analysis period, reaching USD 11.4 billion by 2034. This growth is driven by the increasing adoption of AI-powered driver monitoring and in-cabin safety systems. Facial recognition enables features such as driver authentication, fatigue detection, and emotion analysis. Advancements in 3D imaging, infrared sensing, and AI-based vision processors are improving accuracy and reliability, making facial recognition a key component in connected and autonomous vehicle ecosystems.

- Manufacturers should focus on integrating advanced AI vision processors, enhancing 3D imaging and infrared sensing capabilities, and ensuring seamless system compatibility. Prioritizing innovation in facial recognition technologies will enable safer, smarter in-cabin experiences, positioning them at the forefront of the rapidly growing hybrid integration systems market.

Based on the end use, the backside power delivery network technology market is segmented into semiconductor foundries, integrated device manufacturers (IDMs), equipment & materials suppliers, system integrators & OEMs, and others. The semiconductors foundries segment dominated the market in 2024 with a revenue of USD 900 million.

- Semiconductor Foundries account for the largest share of the market due to their advanced manufacturing capabilities, enabling precise integration of through-silicon vias (TSVs) and other high-density interconnects. Their expertise in scaling and optimizing power delivery for complex chips supports high-performance computing, AI, and data center applications, driving widespread adoption.

- Manufacturers should focus on enhancing TSV integration techniques, improving yield and reliability, and investing in advanced lithography and packaging technologies. By streamlining power delivery and supporting complex chip architectures, they can meet the growing demand for high-performance applications, securing a competitive edge in the semiconductor foundry-driven market.

- Equipment & Materials Suppliers are anticipated to witness significant growth at a CAGR of 29.5% over the analysis period, reaching USD 10.7 billion by 2034. This growth is driven by rising demand for advanced packaging technologies, including through-silicon vias (TSVs), hybrid bonding, and wafer-level processing. The surge in AI, 5G, and autonomous vehicle applications is driving the need for high-performance, reliable materials and precision equipment. Suppliers are investing in innovations that enhance yield, reduce defects, and support miniaturization. As semiconductor complexity increases, the role of specialized materials and equipment becomes critical, positioning suppliers as key enablers of next-generation chip manufacturing and backside power delivery networks.

- Manufacturers should focus on developing precision equipment and high-purity materials tailored for advanced packaging needs. Emphasizing innovation in defect control, process scalability, and material compatibility will help meet the rising demand from AI, 5G, and automotive sectors, ensuring strong positioning in the rapidly expanding semiconductor supply chain.

Looking for region specific data?

North America Backside Power Delivery Network Technology Market

The North America market dominated the global backside power delivery network technology market with a industry share of 29.4% in 2024.

- The North America market is driven by strong demand for high-performance computing, AI, and data center infrastructure. The region benefits from a robust semiconductor ecosystem, advanced R&D capabilities, and strategic investments in chip packaging and integration technologies. Government support and collaborations between tech giants and foundries further accelerate innovation, making North America a key hub for cutting-edge power delivery solutions. This dynamic environment fosters rapid adoption of TSVs and other advanced interconnects, propelling market growth across multiple high-tech sectors.

- Manufacturers should focus on strengthening partnerships with North American tech firms and research institutions, investing in advanced packaging and TSV technologies, and aligning with government initiatives. Prioritizing innovation and scalability will help meet the region’s growing demand for high-performance computing and AI, securing leadership in power delivery solutions.

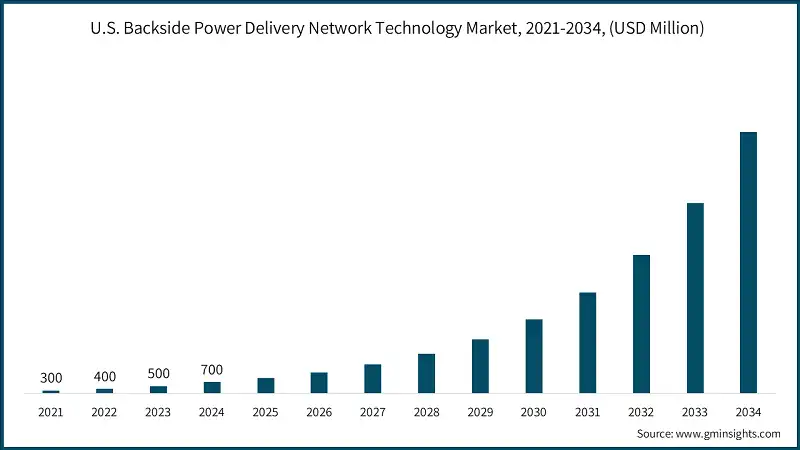

The U.S. backside power delivery network technology market was valued at USD 300 million and USD 400 million in 2021 and 2022, respectively. The market size reached USD 700 million in 2024, growing from USD 500 million in 2023.

- The U.S. continues to dominate the backside power delivery network technology industry, driven by its leadership in semiconductor innovation, strong presence of major foundries, and high demand for advanced computing applications. Strategic investments in AI, data centers, and chip packaging technologies, along with government support, fuel rapid adoption of TSVs and other advanced interconnects. The country’s robust R&D infrastructure and collaboration between industry and academia further accelerate technological advancements, positioning the U.S. as a global hub for next-generation power delivery solutions across diverse high-tech sectors.

- Manufacturers should focus on leveraging the U.S.'s strong R&D and semiconductor infrastructure by investing in advanced packaging, TSV technologies, and AI-driven power delivery solutions. Collaborating with leading foundries and academic institutions will accelerate innovation, helping meet growing demand for high-performance computing and secure the U.S.'s market leadership.

Europe Backside Power Delivery Network Technology Market

Europe market accounted for USD 700 million in 2024 and is anticipated to show lucrative growth over the forecast period.

- Europe holds a significant share of the global backside power delivery network technology industry, driven by its strong focus on sustainable semiconductor manufacturing, advanced automotive electronics, and robust research initiatives. The region benefits from strategic investments in AI, IoT, and electric vehicles, which demand efficient power delivery solutions. Collaborative efforts between governments, academic institutions, and industry players foster innovation in chip packaging and integration technologies. Europe's emphasis on energy efficiency and digital transformation continues to propel the adoption of advanced backside power delivery systems across multiple sectors.

- Manufacturers should focus on developing energy-efficient power delivery solutions, advancing chip packaging technologies, and aligning with Europe’s sustainability goals. Collaborating with research institutions and automotive leaders will help drive innovation, meet regional demands for AI and EV applications, and strengthen their position in Europe’s growing semiconductor ecosystem.

UK dominates the Europe market, showcasing strong growth potential.

- Within Europe, the U.K. holds a substantial share of the backside power delivery network technology market due to its strong semiconductor research ecosystem, government-backed innovation programs, and growing demand for advanced automotive and AI applications. The country’s focus on chip design, packaging technologies, and secure computing drives adoption of TSVs and other high-density interconnects. Collaborations between universities, startups, and global tech firms further accelerate development, positioning the U.K. as a key player in next-generation power delivery solutions across high-performance and energy-efficient electronics sectors.

- Manufacturers should focus on advancing secure, energy-efficient chip packaging and power delivery technologies tailored to the U.K.’s automotive and AI sectors. Collaborating with universities and startups will accelerate innovation, while aligning with government-backed initiatives ensures strategic growth and strengthens their role in the U.K.’s semiconductor ecosystem.

Asia Pacific Backside Power Delivery Network Technology Market

The Asia-Pacific market is anticipated to grow at the highest CAGR of 34.2% during the analysis timeframe.

- The Asia-Pacific region is experiencing rapid growth in the global backside power delivery network technology industry, driven by its expanding semiconductor manufacturing base, rising demand for consumer electronics, and government-backed initiatives supporting digital infrastructure. Countries like China, South Korea, Taiwan, and Japan are investing heavily in advanced packaging technologies, including TSVs and wafer-level integration. The region’s focus on AI, 5G, and electric vehicles further accelerates adoption of efficient power delivery solutions, positioning Asia-Pacific as a key driver of innovation and market expansion in the global semiconductor landscape.

- Manufacturers should focus on scaling production capabilities, enhancing TSV and wafer-level packaging technologies, and aligning with regional demands for AI, 5G, and EV applications. Collaborating with local governments and tech firms will accelerate innovation, helping them capitalize on Asia-Pacific’s booming semiconductor market and maintain competitive advantage.

China backside power delivery network technology market is estimated to grow with a significant CAGR 29.6% from 2025 to 2034, in the Asia Pacific market.

- China dominates the global backside power delivery network technology industry, driven by its vast automotive production base, growing consumer electronics demand, and aggressive investments in semiconductor manufacturing. The country is rapidly advancing in chip packaging technologies like TSVs and wafer-level integration to support AI, 5G, and electric vehicle applications. Government-backed initiatives and strategic partnerships with global tech firms further accelerate innovation, making China a powerhouse in next-generation power delivery solutions and a key contributor to global semiconductor supply chain resilience and growth.

- Manufacturers should focus on expanding local production capabilities, advancing TSV and wafer-level packaging technologies, and aligning with China’s strategic goals in AI, EVs, and consumer electronics. Collaborating with domestic tech firms and leveraging government support will ensure competitiveness and sustained growth in the rapidly evolving Chinese semiconductor market.

The Latin America backside power delivery network technology market, valued at USD 200 million in 2024, is driven by rising demand for advanced automotive electronics, growing semiconductor investments, and increasing adoption of AI and IoT across consumer and industrial sectors.

The Middle East and Africa market is projected to reach USD 2.7 billion by 2034, driven by rising investments in smart infrastructure, growing automotive demand, and expanding semiconductor manufacturing capabilities.

UAE market to experience substantial growth in the Middle East and Africa backside power delivery network technology industry in 2024.

- The UAE is demonstrating significant growth potential in the Middle East and Africa backside power delivery network technology market, driven by its strategic investments in semiconductor infrastructure, smart mobility, and AI-powered automotive technologies. Government initiatives promoting digital transformation and partnerships with global tech firms are accelerating the adoption of advanced chip packaging solutions like TSVs. The country’s focus on electric vehicles, autonomous systems, and secure in-car technologies further boosts demand for efficient power delivery networks, positioning the UAE as a rising hub for innovation in the regional semiconductor landscape.

- Manufacturers should focus on developing advanced chip packaging and power delivery solutions tailored to the UAE’s smart mobility and EV initiatives. Collaborating with tech firms and leveraging government support will accelerate innovation and secure a strong foothold in the region’s growing semiconductor market.

Backside Power Delivery Network Technology Market Share

The global backside power delivery network (BSPDN) technology market is marked by rapid advancements in semiconductor packaging, increasing demand for high-performance computing, and widespread adoption of AI-driven applications. Key players such as Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, Samsung Electronics (Samsung Foundry), Applied Materials, Inc.,and Lam Research Corporation collectively hold a significant market share of ~87% in the global backside power delivery network (BSPDN) Technology Market. Strategic collaborations between foundries, automotive OEMs, and AI solution providers are accelerating integration into data centers, autonomous vehicles, and smart devices. Emerging companies are contributing with compact, energy-efficient chip designs optimized for biometric sensing and edge computing. These innovations are driving global deployment, improving system reliability, and shaping the future of semiconductor power delivery.

In addition, emerging players and niche semiconductor developers are strengthening the global backside power delivery network (BSPDN) technology market by introducing compact, scalable, and energy-efficient chip solutions tailored for high-performance computing, AI, and edge devices. Their innovations in TSV integration, low-power design, and advanced packaging are improving bandwidth, latency, and thermal efficiency. Collaborations with cloud providers, data center operators, and device manufacturers are accelerating deployment across diverse sectors. These efforts are enhancing system reliability, reducing costs, and enabling widespread adoption of next-generation power delivery architectures in the global semiconductor ecosystem.

Backside Power Delivery Network Technology Market Companies

Prominent players operating in the backside power delivery network technology industry are as mentioned below:

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Intel Corporation

- Samsung Electronics (Samsung Foundry)

- GlobalFoundries

- ASE Technology Holding Co., Ltd. (ASE Group)

- Amkor Technology

- Applied Materials, Inc.

- Lam Research Corporation

- ASML Holding N.V.

- Tokyo Electron Limited

- KLA Corporation

- Cadence Design Systems, Inc.

- Synopsys Inc.

- Ansys, Inc.

- Advantest Corporation

- Entegris, Inc.

- Screen Holdings Co., Ltd.

- Veeco Instruments Inc.

- Onto Innovation Inc.

- Infineon Technologies AG

- Taiwan Semiconductor Manufacturing Company (TSMC)

Taiwan Semiconductor Manufacturing Company (TSMC) is a key player in the global BSPDN technology market, holding an estimated 28% market share. The company leads in developing advanced TSV-based packaging and wafer-level integration for high-performance computing and AI applications. TSMC’s innovations in backside power delivery architectures enhance bandwidth, reduce latency, and improve thermal efficiency. Through strategic collaborations with global tech firms and automotive OEMs, TSMC is accelerating deployment of scalable, energy-efficient semiconductor solutions across data centers, autonomous vehicles, and smart infrastructure, reinforcing its leadership in next-generation chip manufacturing and power delivery technologies. - Intel Corporation

Intel Corporation plays a pivotal role in the global BSPDN technology market, leveraging its expertise in AI-driven semiconductor design and edge computing. The company focuses on integrating backside power delivery into biometric modules and driver monitoring systems, enhancing performance and energy efficiency. Intel’s advancements in TSVs, signal processing, and secure architecture support real-time facial recognition, fatigue detection, and in-vehicle authentication. Collaborations with OEMs and foundries enable Intel to scale its solutions across premium automotive platforms and smart mobility ecosystems, contributing to safer, more personalized, and connected driving experiences worldwide.

Samsung Electronics holds a significant share of around 11% in the global BSPDN technology market, specializing in compact, cost-effective semiconductor platforms for biometric sensing and smart devices. The company’s innovations in chip miniaturization, low-power design, and TSV integration support facial, fingerprint, and iris recognition across automotive and consumer electronics. Samsung’s strategic partnerships with Tier 1 suppliers and OEMs accelerate the adoption of backside power delivery solutions in next-generation vehicles, enhancing safety, personalization, and connectivity. Its continued investment in fabrication efficiency and AI-based sensing technologies strengthens its global position in the BSPDN landscape.

Backside Power Delivery Network Technology Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 3.1 Billion |

| Market Size in 2025 | USD 3.9 Billion |

| Forecast Period 2025 - 2034 CAGR | 28.7% |

| Market Size in 2034 | USD 37.9 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Growing demand for advanced semiconductor nodes (below 3nm) requiring improved power efficiency and reduced IR drop. | Drives approximately 35% of the backside power delivery network technology market demand, fueled by the rapid transition to sub-3nm process nodes requiring improved power integrity and reduced IR drop. The growing need for faster and more efficient chips in AI, data centers, and advanced computing is accelerating BSPDN adoption. |

| Increasing adoption of AI and high-performance computing (HPC) chips driving need for higher transistor density. | Expected to account for 30% of growth, driven by advancements in semiconductor fabrication and 3D integration that enhance power delivery efficiency. Foundries such as Intel and TSMC are integrating BSPDN in next-generation logic designs to reduce voltage droop and optimize performance for high-density transistor architectures. |

| Rising use of mobile and data center processors demanding better power integrity and thermal management. | Contributes around 25% to market expansion, supported by the increasing adoption of AI accelerators, GPUs, and high-performance processors. The shift toward heterogeneous integration and chiplet architectures requires improved power distribution networks, creating demand for backside power delivery solutions to ensure stable, low-resistance paths for current flow. |

| Technological innovation by key players like Intel and TSMC accelerating BSPDN commercialization. | Projected to drive 10% of growth, owing to rising investments in R&D and advanced packaging technologies such as hybrid bonding and wafer-level integration. These innovations enable scalable BSPDN implementation, reduce power losses, and enhance thermal management, making them critical for future semiconductor design and energy-efficient computing systems. |

| Pitfalls & Challenges | Impact |

| Complex integration process and new design methodologies increase development costs. | These challenges increase development costs, extend design cycles, and require advanced manufacturing capabilities, making adoption difficult for smaller semiconductor firms and slowing commercialization across the broader chip industry. |

| Limited manufacturing capacity and dependence on advanced fabs slow large-scale adoption. | The high cost of EUV lithography tools, complex process integration, and restricted access to advanced nodes make it difficult for manufacturers to scale production and meet growing industry demand efficiently. |

| Opportunities: | Impact |

| Growing use of BSPDN in AI accelerators, GPUs, and next-generation processors. | As it enables higher performance, improved power efficiency, and reduced signal interference essential for advanced computing and data-intensive workloads in AI and high-performance applications. |

| Expansion of 2.5D/3D packaging technologies complementing backside power delivery. | By supporting higher interconnect density, shorter power paths, and enhanced thermal management. This integration enables chipmakers to design more compact, efficient, and scalable semiconductor architectures suited for AI, HPC, and advanced mobile devices. |

| Market Leaders (2024) | |

| Market Leaders |

28% market share. |

| Top Players |

Collective market share in 2024 is 87% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest Growing Market | North America |

| Emerging Countries | China, India, Brazil, Mexico, South Africa |

| Future outlook |

|

What are the growth opportunities in this market?

Backside Power Delivery Network Technology Industry News

- In November 2024, TSMC launched its A16 (1.6 nm-class) process, which introduces its Super Power Rail (SPR) technology, a backside power delivery system that supplies power directly to transistor terminals. This innovation boosts chip performance by 8–10%, reduces power consumption by 15–20%, and increases chip density by 10% compared to its previous N2P process, marking a major leap in semiconductor efficiency and scalability.

- In April 2025, Intel launched 18A process technologies, resulting in superior power, performance, and density scaling. The implementation of PowerVia, which has greatly enhanced overall PPA (power, performance, area) capabilities, is primarily responsible for this achievement. The utilization of advanced technology has enabled Intel to outperform its previous generation and stay ahead in the semiconductor industry.

- In October 2025, GlobalFoundries partnered with Silicon Labs to advance wireless connectivity solutions and bolster U.S. chip manufacturing capabilities. The partnership will focus on leveraging innovative technologies, such as Backside Power Delivery Network (BPDN) technology, to enhance the performance and efficiency of wireless devices.

- In August 2024, Samsung has announced its intention to integrate Back Side Power Delivery Network (BSPDN) technology into its upcoming 2nm process, known as SF2Z. BSPDN is a cutting-edge innovation that enhances power delivery and efficiency within a semiconductor chip by optimizing the distribution of power from the backside of the device.

- In October 2025, ASML, a leading supplier of lithography scanners, launched a new scanner specifically designed for 3D chip packaging. This technology enables advanced packaging techniques such as Backside Power Delivery Network (bPDN) Technology, which allows for more efficient power delivery to stacked chips.

The backside power delivery network technology market research report includes in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Billion from 2021 – 2034 for the following segments:

Market, By Component

- Manufacturing Equipment

- Materials & Consumables

- Metrology & Inspection Systems

- Design & Simulation Software

Market, By Technology Type

- Through-Silicon Via (TSV) Based Systems

- Buried Power Rail Systems

- Direct Backside Contact Systems

- Hybrid Integration Systems

Market, By Application

- High-Performance Computing Processors

- Mobile & Consumer Processors

- Automotive Semiconductor Devices

- Industrial & IoT Applications

- Others

Market, By End Use

- Semiconductor Foundries

- Integrated Device Manufacturers (IDMs)

- Equipment & Materials Suppliers

- System Integrators & OEMs

- Others

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Netherlands

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

What is the market size of the backside power delivery network technology industry in 2024?

The market size was USD 3.1 billion in 2024, with a CAGR of 28.7% expected through 2034, driven by the rising demand for advanced semiconductor architectures and efficient power delivery solutions in AI and high-performance computing applications.

What is the current backside power delivery network technology market size in 2025?

The market size is projected to reach USD 3.9 billion in 2025.

What is the projected value of the backside power delivery network technology market by 2034?

The market size for backside power delivery network technology is expected to reach USD 37.9 billion by 2034, fueled by rapid advancements in sub-3nm semiconductor nodes, 3D integration, and adoption in AI, data centers, and high-performance computing sectors.

How much revenue did the manufacturing equipment segment generate in 2024?

The manufacturing equipment segment leading the industry with a 34.2% share in 2024 due to strong adoption of advanced power delivery and wafer-level integration technologies.

What was the valuation of through-silicon via (TSV) based systems segment in 2024?

The through-silicon via (TSV) based systems segment was valued at USD 600 million in 2024, driven by high bandwidth, low latency interconnects, and growing use in data centers and advanced computing devices.

What is the growth outlook for hybrid integration systems from 2025 to 2034?

Hybrid integration systems are projected to grow at a 29.7% CAGR through 2034, supported by increasing demand for AI-enabled processors, 3D imaging, and energy-efficient semiconductor packaging solutions.

Which region leads the backside power delivery network technology market?

The U.S. dominated the market with USD 700 million in 2024, supported by its strong semiconductor ecosystem, AI adoption, and advanced chip packaging innovations.

What are the upcoming trends in the backside power delivery network technology industry?

Key trends include integration of backside power delivery in sub-2nm process nodes, rising adoption of 3D chiplet architectures, and increasing collaboration between foundries, EDA tool providers, and material suppliers to enhance power efficiency and reduce IR drop.

Who are the key players in the backside power delivery network technology market?

Key players include Taiwan Semiconductor Manufacturing Company (TSMC), Intel Corporation, Samsung Electronics (Samsung Foundry), Applied Materials, Inc., Lam Research Corporation, ASML Holding N.V., Cadence Design Systems, Synopsys Inc., Amkor Technology, and GlobalFoundries.

Backside Power Delivery Network Technology Market Scope

Related Reports