Authors:

Preeti Wadhwani, Aishvarya Ambekar

Download free PDF

Automotive Pump for Thermal System Market Size & Share 2026-2035

Report ID: GMI13378

|

Published Date: May 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Automotive Pump for Thermal System Market

Get a free sample of this report

Get a free sample of this report Automotive Pump for Thermal System Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Automotive Pump for Thermal System Market Size

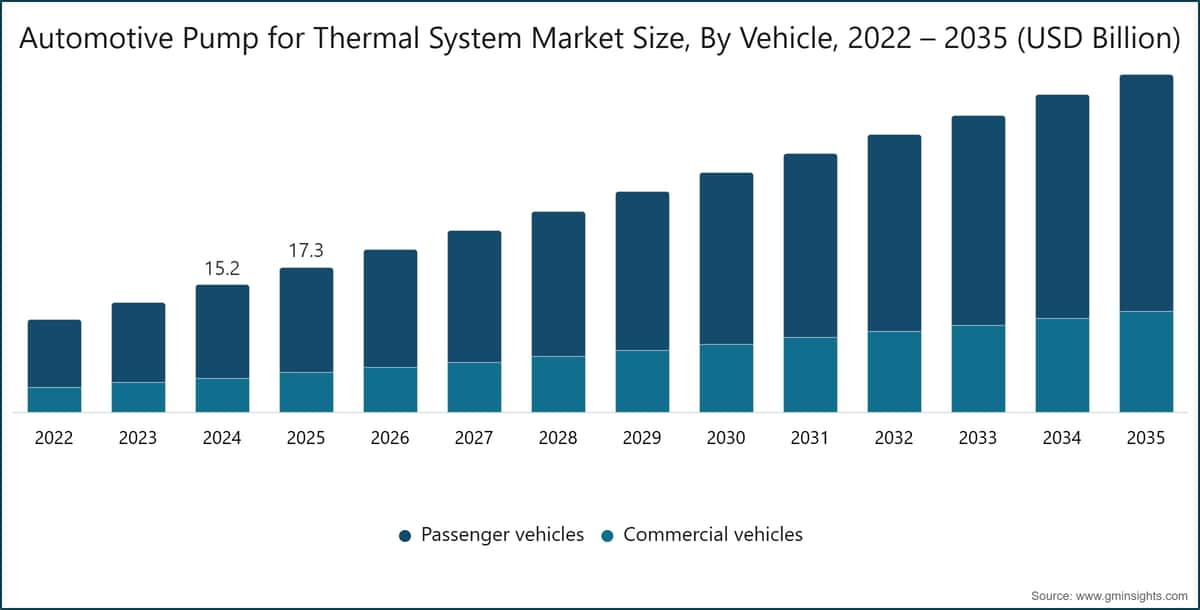

The global automotive pump for thermal system market was estimated at USD 17.3 billion in 2025. The market is expected to grow from USD 19.4 billion in 2026 to USD 40.4 billion in 2035, at a CAGR of 8.5%, according to latest report published by Global Market Insights Inc.

Automotive Pump for Thermal System Market Key Takeaways

Market Leader: Denso led with over 14.5% market share in 2025.

Leading Players: Top 5 players in this market include Aisin, Bosch, Denso, Hanon Systems, MAHLE, Valeo, which collectively held a market share of 59.1% in 2025.

The market volume was estimated at 162.5 million units in 2025. The market is projected to grow from 173.6 million units in 2026 to 304.4 million units by 2035, registering strong double-digit growth over the forecast period.

The market is undergoing a structural transformation as vehicle architectures evolve from mechanically driven internal combustion platforms to fully electrified, software-managed energy ecosystems. Thermal pumps, once considered auxiliary components supporting radiator circulation and cabin heating, are now mission-critical systems responsible for regulating battery temperature, safeguarding power electronics, maintaining inverter efficiency, and stabilizing cabin comfort without compromising driving range. In electrified vehicles including BEVs, PHEVs, HEVs, and FCEVs thermal pumps directly influence battery longevity, fast-charging capability, cold-weather performance, and overall energy consumption efficiency, positioning them as strategic enablers rather than peripheral hardware.

For instance, the new EV models launched by BYD during March 2025 provided vehicles with more than 250 miles of extended range using only five minutes of charging time thereby resolving consumer concerns about charging duration and range limitations.

The acceleration of vehicle electrification globally is intensifying the technical requirements for next-generation coolant and refrigerant pump systems. Electric pumps must now operate with variable speed control, intelligent flow modulation, and integration with vehicle energy management systems. Unlike belt-driven mechanical pumps in ICE vehicles, electrically driven coolant pumps are optimized for demand-based operation, reducing parasitic losses while enhancing thermal precision. This shift supports automakers’ efforts to extend EV driving range and comply with stringent efficiency standards across major automotive markets.

Technological advancement within the market is centered on efficiency optimization and sustainability. Manufacturers are focusing on low-global-warming-potential refrigerants, electronically commutated motors, integrated coolant distribution modules, and compact pump assemblies designed for modular EV platforms. Heat pump-based HVAC systems, which significantly reduce winter energy consumption compared to resistive heaters, rely heavily on precise refrigerant circulation enabled by advanced pump technologies. In cold climates, this integration improves real-world driving range while maintaining passenger comfort, a critical purchase consideration in Europe and North America.

The transition toward high voltage 800V electrical architectures and ultra-fast charging infrastructure is creating additional growth opportunities. Rapid charging generates substantial thermal loads within battery packs and power electronics. To manage these heat spikes, vehicles require high-flow liquid cooling pumps with superior thermal stability and redundancy capabilities. Direct battery immersion cooling and chiller-assisted systems are emerging in high-performance EV platforms, further elevating the technical specifications of automotive thermal pumps. Thermal runaway mitigation and predictive cooling algorithms are also gaining importance as battery energy density increases.

Commercial vehicle electrification presents a parallel growth trajectory. Electric buses, delivery vans, and heavy-duty trucks operate under high duty cycles and continuous load conditions, necessitating robust liquid cooling circuits. Scalable, high-capacity pump systems are critical to maintaining drivetrain reliability and minimizing downtime, directly influencing fleet total cost of ownership (TCO). As logistics and public transport fleets electrify, demand for durable, service-friendly pump architectures is increasing across markets.

Digital integration is redefining system architecture within the automotive pump for thermal system market. Modern pumps are embedded within coordinated vehicle thermal management networks, interfacing with battery management systems (BMS), traction inverters, and centralized vehicle control units (VCUs). Software-enabled predictive thermal control allows pre-conditioning prior to charging, optimized coolant routing during high-load driving, and remote climate adjustments via over-the-air updates. Compliance with functional safety frameworks such as International Organization for Standardization standards is becoming critical, as thermal failure can directly impact battery safety and vehicle operability.

From a channel perspective, the OEM segment remains dominant, as thermal pump systems are integrated during vehicle platform design. However, the aftermarket is gradually expanding, particularly in coolant replacement services, refrigerant maintenance, and retrofitting upgraded pump modules in early-generation electric vehicles. Sustainability considerations including refrigerant recovery, fluid recycling, and environmentally compliant disposal are also shaping service strategies.

Regionally, North America and Europe continue to represent high-value markets due to aggressive decarbonization policies, advanced charging ecosystems, and strong consumer demand for long-range EV performance. In the United States and key European nations, range stability in extreme temperatures and reliable fast-charging performance are primary differentiators that elevate the importance of advanced thermal pump systems.

Asia-Pacific is positioned as the fastest-growing long-term opportunity. China’s vertically integrated EV manufacturing ecosystem and battery production dominance are driving localized innovation in thermal pump technology. Meanwhile, Japan and South Korea are advancing compact, energy-efficient pump systems aligned with hybrid and fuel-cell vehicle development. India’s expanding EV two-wheeler, three-wheeler, and public transport electrification initiatives are further stimulating demand for cost-optimized and scalable thermal management components.

Automotive Pump for Thermal System Market Trends

The transition from mechanically driven pumps to fully electric variable-speed coolant pumps is transforming thermal efficiency in modern vehicles. Electric pumps operate on demand, adjusting flow rates based on real-time thermal loads from batteries, inverters, and HVAC systems. This reduces parasitic energy losses, improves overall vehicle efficiency, enhances battery longevity, and enables precise temperature control essential for electrified powertrains.

Automakers are increasingly consolidating multiple cooling functions into centralized thermal management modules. These integrated systems combine pumps, valves, sensors, heat exchangers, and chillers into compact assemblies. This modular architecture improves packaging efficiency, reduces system complexity, lowers weight, and enables coordinated thermal control across battery packs, power electronics, traction motors, and cabin climate systems.

For example, in April 2024, Vitesco Technologies and Sanden International announced an integrated thermal management system for BEVs that combines coolant distribution, pumps, and refrigerant circuits into a unified architecture, underscoring the industry move toward centralized thermal management modules.

Growing environmental regulations are accelerating the shift toward low-GWP refrigerants in automotive HVAC and heat pump systems. This transition impacts pump material compatibility, sealing technologies, and pressure management design. Manufacturers are adapting pump architectures to ensure safe handling of alternative refrigerants while maintaining system efficiency, durability, and compliance with global sustainability and emissions standards.

Thermal management is becoming increasingly software-driven, integrating coolant pumps with battery management systems and vehicle control units. Predictive algorithms optimize coolant flow, enable pre-conditioning before fast charging, and dynamically balance thermal loads during operation. This software-defined approach enhances range stability, charging performance, and system reliability while supporting over-the-air updates and continuous performance optimization.

To support EV range optimization and platform flexibility, manufacturers are developing lightweight and compact pump designs using advanced polymers and aluminum components. Smaller, modular architectures improve packaging within tight EV layouts while reducing vehicle mass. This trend enhances energy efficiency, simplifies assembly processes, and supports scalable deployment across different vehicle segments and electrified platforms.

Automotive Pump for Thermal System Market Analysis

Based on vehicle, the market is divided into passenger cars, and commercial vehicles. The passenger cars segment dominated the automotive pump for thermal system market, accounting for around 72.98% in 2025 and is expected to grow at a CAGR of more than 8.1% through 2035.

Based on sales channel, the market is categorized into OEM, and aftermarket. The OEM segment dominates the market accounting for around 84% share in 2025, and the segment is expected to grow at a CAGR of over 8.2% from 2026-2035.

The automotive pump for thermal system market is dominated by the OEMs segment due to the direct integration of advanced thermal management systems during vehicle manufacturing, particularly in electric and hybrid platforms. Automakers increasingly design integrated multi-loop cooling architectures that require precise calibration of electric coolant pumps, battery chillers, and HVAC modules at the production stage. Major OEMs such as Tesla, Toyota Motor Corporation, and Volkswagen Group embed customized thermal systems directly into new vehicle platforms to optimize performance, safety, and energy efficiency.

Based on propulsion, the automotive pump for thermal system market is divided into ICE, BEV, PHEV, and HEV. The ICE segment held the major market share in 2025.

Based on pump type, the automotive pump for thermal system market is divided into centrifugal pumps, positive displacement pumps, and variable displacement pumps. The variable displacement pump segment dominated the market.

China dominated the automotive pump for thermal system market in Asia Pacific with around 64.21% share and generated USD 4 billion in revenue in 2025.

The automotive pump for thermal system market in Germany is expected to experience significant and promising growth from 2026 to 2035.

The automotive pump for thermal system market in US is expected to experience significant and promising growth from 2026-2035.

The automotive pump for thermal system market in Brazil is expected to experience significant and promising growth from 2026 to 2035.

The automotive pump for thermal system market in UAE is expected to experience significant and promising growth from 2026-2035.

14.5% market share

Collective Market Share in 2025 is 59.1%

Automotive Pump for Thermal System Market Share

Automotive Pump for Thermal System Market Companies

Major players operating in the automotive pump for thermal system industry are:

Automotive Pump for Thermal System News

The automotive pump for thermal system market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($Bn), and shipment (Units) from 2022 to 2035, for the following segments:

Click here to Buy Section of this Report

Market, By Vehicle

Market, By Pump Type

Market, By Application

Market, By Propulsion

Market, By Sales Channel

Market, By Power Rating

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn, Units)

Chapter 6 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn, Units)

Chapter 7 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn, Units)

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn, Units)

Chapter 9 Market Estimates & Forecast, By Pump Type, 2022 - 2035 ($Bn, Units)

Chapter 10 Market Estimates & Forecast, By Power Rating, 2022 - 2035 ($Bn, Units)

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn, Units)

Chapter 12 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →