Summary

Table of Content

Automotive Energy Recovery System Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Automotive Energy Recovery System Market Size

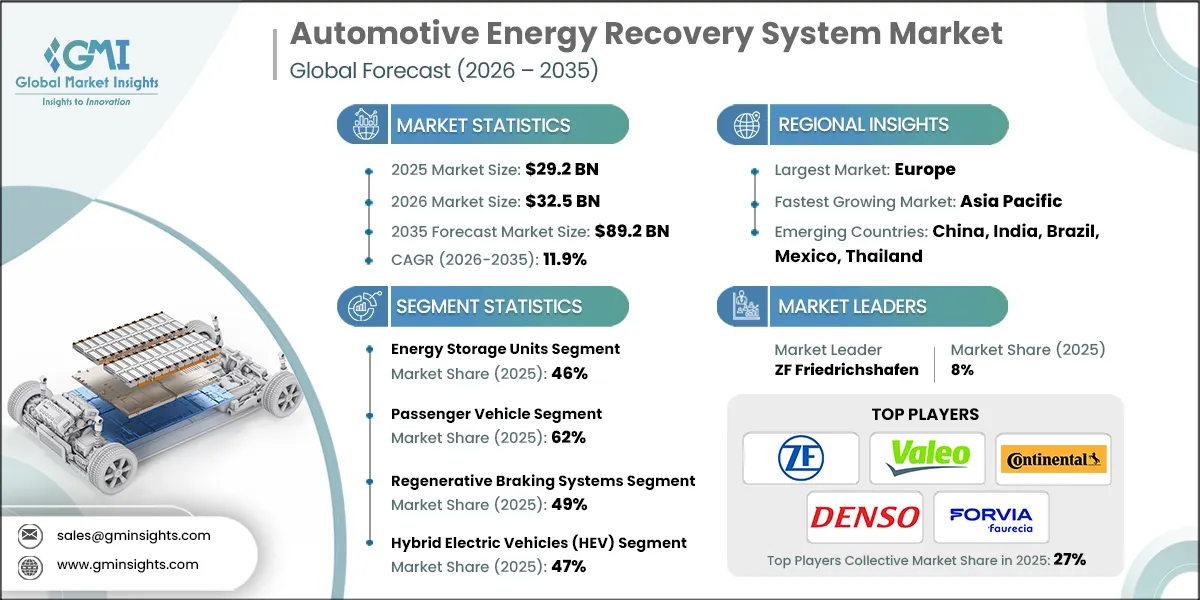

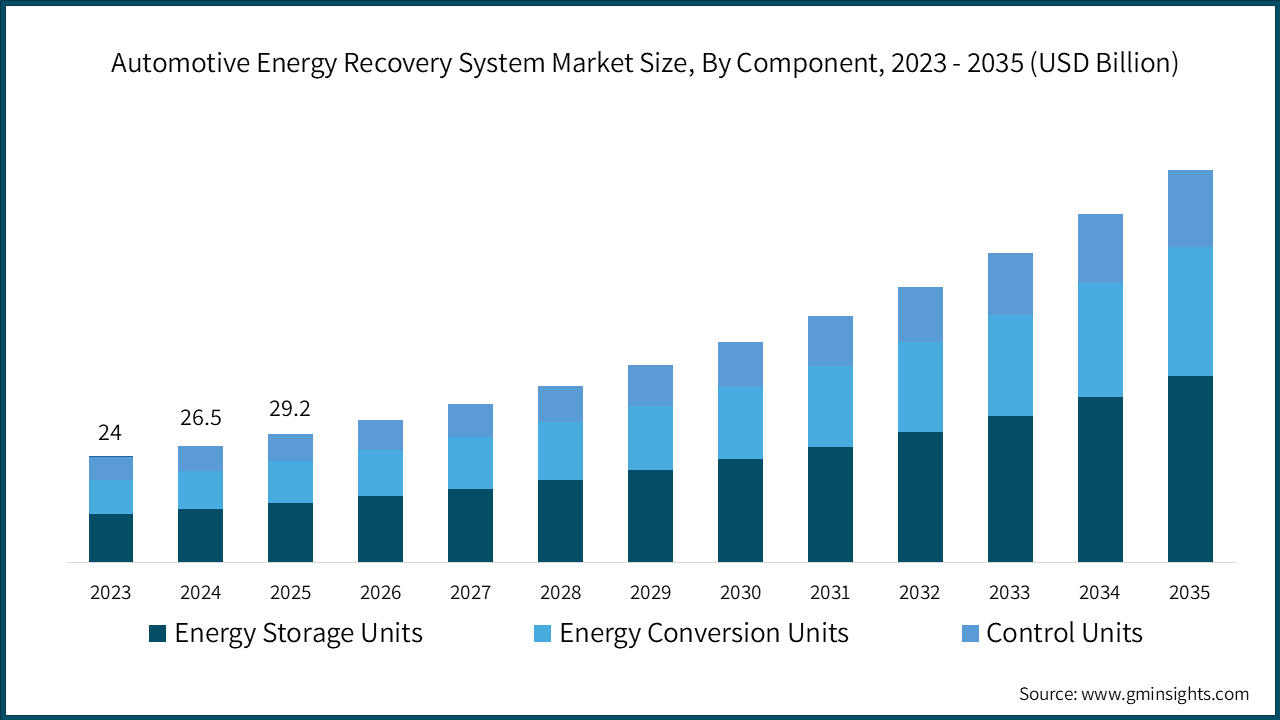

The global automotive energy recovery system market size was estimated at USD 29.2 billion in 2025. The market is expected to grow from USD 32.5 billion in 2026 to USD 89.2 billion in 2035, at a CAGR of 11.9% according to latest report published by Global Market Insights Inc.

To get key market trends

The automotive energy recovery system market represents a transformative segment within the global automotive industry, driven by the imperative to enhance fuel efficiency, reduce emissions, and support the transition toward electrified powertrains.

In 2024, global motor vehicle production reached 92.5 million units, creating opportunities for energy recovery system integration. Emerging economies led with 53.79 million units, highlighting growth potential as regulations and consumer preferences shift toward efficiency.

According to the International Energy Agency (IEA), electric vehicle sales are expected to reach 17 million in 2024 (20% of global new car sales) and exceed 20 million in 2025 (25% market share). This growth highlights the critical need for regenerative braking system integration in electric and hybrid vehicles.

Energy recovery systems, such as regenerative braking, turbochargers, and exhaust gas recirculation (EGR) technologies, harness energy typically lost as heat during vehicle operation. This innovation directly tackles the challenges of escalating fuel costs and tightening environmental regulations.

In 2024, global electric vehicle sales exceeded 17 million units, accounting for over 20% of worldwide new car sales. This surge underscores the growing importance of integrating energy recovery technologies to enhance vehicle efficiency, spanning internal combustion engines (ICE), hybrids, and battery electric vehicles (BEVs).

The automotive sector's shift to electrification is driving energy recovery system adoption. The International Energy Agency predicts global electric car sales will exceed 20 million by 2025, accounting for 25% of total car sales. This trend demands advanced regenerative braking technologies to capture 50-70% of braking energy in passenger BEVs.

Rapid urbanization and rising traffic congestion globally highlight the need for energy recovery systems like regenerative braking. In 2022, U.S. traffic congestion wasted 3.3 billion gallons of fuel, with stop-and-go traffic consuming 30-40% more fuel than free-flow conditions.

Automotive Energy Recovery System Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 29.2 Billion |

| Market Size in 2026 | USD 32.5 Billion |

| Forecast Period 2026 - 2035 CAGR | 11.9% |

| Market Size in 2035 | USD 89.2 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Increasing adoption of electric and hybrid vehicles | Expands integration of regenerative braking and energy recovery systems to improve vehicle range and energy efficiency. |

| Stringent emission regulations and fuel efficiency standards | Accelerates OEM adoption of energy recovery technologies to meet regulatory compliance and reduce CO2 emissions. |

| Advancements in energy recovery technologies | Improves system efficiency, reliability, and cost-effectiveness, enabling wider deployment across vehicle segments. |

| Growing consumer demand for environmentally friendly and cost-efficient vehicles | Drives automakers to incorporate energy recovery systems to enhance fuel savings and reduce operating costs. |

| Traffic congestion & urbanization pressures | Increases energy recovery opportunities through frequent breaking in urban driving conditions. |

| Pitfalls & Challenges | Impact |

| High initial costs of energy recovery systems | Increase vehicle pricing and slows adoption, particularly in cost-sensitive markets. |

| Limited awareness and understanding of energy recovery technologies among consumers | Reduces demand due to unclear value perception and benefits. |

| Opportunities: | Impact |

| Rising adoption of electric and hybrid vehicles | Expands demand for regenerative breaking and advanced energy recovery systems to improve vehicle range and efficiency. |

| Growing focus on fleet and commercial vehicle efficiency | Drives adoption of energy recovery systems to lower fuel costs and improve total cost of ownership. |

| Advancements in energy storage and power electronics | Enhances recovery efficiency and system performance, enabling broader application across vehicle segments. |

| Emerging opportunities in developing automotive markets | Supports market expansion as vehicle production and electrification increase in cost-sensitive regions. |

| Market Leaders (2025) | |

| Market Leader |

8% Market Share |

| Top 5 Players |

Collective Market Share is 27% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Europe |

| Fastest growing market | Asia Pacific |

| Emerging countries | China, India, Brazil, Mexico, Thailand |

| Future outlook |

|

What are the growth opportunities in this market?

Automotive Energy Recovery System Market Trends

The automotive industry's shift to electrified powertrains drives advancements in energy recovery systems, particularly regenerative braking. In 2024, global EV sales exceeded 17 million units, over 20% of new car sales. The International Energy Agency predicts sales will surpass 20 million units in 2025.

In 2024, BEVs accounted for 70% of the global electric car stock, with a BEV-to-PHEV model ratio of nearly 2:1, reflecting a preference for full electrification. China led the market with over 11 million electric car sales and aims for a 60% EV sales share by 2025. Europe maintained a 25% EV sales share, while the U.S. reached 10% penetration with 1,412,298 PEVs sold by November 2024.

As electrification surges, regenerative braking systems are becoming essential across all EV and HEV platforms. These systems play a crucial role in extending electric range, optimizing battery use, and aligning with consumer range expectations. According to the U.S. EPA, in the 2023 model year, electrified technologies, encompassing BEVs and PHEVs, made up 36% of total car and SUV sales.

Progressively stringent government emissions and fuel economy regulations globally compel automotive manufacturers to deploy comprehensive, multi-layered energy recovery strategies encompassing regenerative braking, advanced turbocharging, exhaust gas recirculation, and waste heat recovery technologies.

On March 20, 2024, the U.S. Environmental Protection Agency (EPA) finalized its Multi-Pollutant Emissions Standards for Model Years 2027 and beyond. These groundbreaking standards, centered on performance-based metrics, aim to boost battery electric vehicle sales to 55% by 2028 (MY2029) and further escalate this target to 67% by the end of the rule's timeline in 2032.

Escalating urbanization and intensifying traffic congestion in metropolitan areas worldwide create operational environments that disproportionately favor energy recovery systems, particularly regenerative braking technologies optimized for frequent stop-and-go driving cycles.

The energy recovery system market is transitioning from discrete component supply toward comprehensive system-level integration, where regenerative braking, thermal management, turbocharging, and power electronics function as coordinated subsystems within holistic powertrain architectures.

Advanced brake-blend control strategies, detailed in SAE technical papers such as 2019-01-5089, employ cooperative control and real-time optimal allocation for dual-motor hybrid electric vehicle braking, increasing braking energy recovery rates through sophisticated motor-loss and hydraulic system models.

Automotive Energy Recovery System Market Analysis

Learn more about the key segments shaping this market

Based on component, the automotive energy recovery system market is segmented into energy storage units, energy conversion units, control units. The energy storage units segment dominates the market with 46% share in 2025, and the segment is expected to grow at a CAGR of 12.2% from 2026 to 2035.

- Energy storage units lead the component segment. This segment includes battery systems and energy storage devices that capture, and store recovered energy for later use, whether for propulsion, auxiliary power, or grid discharge.

- Energy storage units include lithium-ion battery packs (NMC, NCA, LFP chemistries) for battery electric and plug-in hybrid vehicles. High-voltage battery modules (400V, 800V architectures) integrate with regenerative braking systems, while 48-volt battery systems enable mild hybrid regenerative functionality in ICE vehicles.

- Ultracapacitors and supercapacitors provide high-power-density storage for transient regeneration and support battery systems during aggressive braking. Battery management systems (BMS) ensure optimal charge acceptance with cell monitoring and thermal management. Bidirectional DC-DC converters connect energy storage units to vehicle electrical systems.

- In 2024, global electric vehicle sales surpassed 17 million units, representing 20% of new cars. This highlights the critical demand for energy storage in electrified powertrains.

- Energy conversion units hold a 33% share and are growing at a 12.0% CAGR during forecast period. This segment includes systems that convert kinetic braking energy into electrical energy or stored electrical energy into mechanical propulsion.

- Power electronics and electric motors hold a significant market share due to their high component value. Advanced traction motor-inverter systems add $1,500-$3,000 per vehicle, while premium brake-by-wire systems contribute $800-$1,200 per vehicle.

- Control Units hold a 21% share of the component segment. This segment includes ECUs, energy management controllers, sensor networks, and software platforms that optimize energy recovery, battery charge acceptance, and integrate with vehicle dynamics and autonomous systems.

- Control units include regenerative brake controllers that manage torque allocation between electric motors and friction brakes based on real-time vehicle dynamics. Battery management system controllers monitor cell conditions and communicate charge power to braking systems. Vehicle energy management controllers also play a vital role.

- The segment's growth highlights the automotive industry's shift toward software-defined vehicles. Advanced regenerative braking strategies improve energy capture by 15-25% through optimized torque allocation, predictive deceleration management, and coordinated vehicle dynamics control.

Learn more about the key segments shaping this market

Based on vehicle, the automotive energy recovery system market is divided into passenger cars, commercial vehicles, and electric and hybrid vehicles. The passenger vehicle segment dominates with 62% market share in 2025 and is growing at CAGR of 12% between 2026 and 2035.

- Passenger cars segment encompasses conventional sedans, SUVs, crossovers, hatchbacks, and coupes across all propulsion types (ICE, hybrid, electric).

- In 2024, passenger cars dominated global vehicle production, accounting for 60-65% of the 92.5 million units produced (OICA). This dominance is driven by stringent emissions regulations and rapid electrification, with EV sales reaching 20% (IEA).

- In 2023, BEVs and PHEVs accounted for 36% of car and SUV sales, highlighting electrification's growth. Regenerative braking leads energy recovery in electrified cars, while turbochargers dominate ICE vehicles.

- Consumer demand for fuel efficiency, government incentives for low-emission vehicles, and the availability of electrified passenger cars across price segments are driving segment growth.

- Premium vehicles adopt advanced regenerative braking and turbocharging systems, while mass-market models increasingly use 48V mild hybrid systems and single turbochargers.

- LCVs encompass vans, pickup trucks, small delivery vehicles, and commercial utility vehicles typically serving urban delivery, service fleet, and small business transportation applications.

- This segment's growth is driven by the rise of e-commerce and last-mile delivery services, increasing demand for urban delivery vehicles. Fleet operators prioritize fuel-efficient and electrified LCVs due to cost benefits, while global zero-emission regulations mandate low-emission commercial vehicles.

- HCVs include long-haul trucks, regional haulers, coaches, city buses, and heavy-duty construction/agriculture equipment.

- The energy recovery system demand in this segment differs from passenger vehicles. Turbochargers dominate due to diesel engine usage and slower electrification. Waste heat recovery systems offer strong payback periods, while regenerative breaking is prevalent in vehicles with frequent stops like urban buses and delivery trucks.

- By 2025, electric vehicles and hybrid vehicles are expected to reach USD 3.1 billion, growing 12.5% CAGR from 2026 to 2035.

- Energy recovery systems for battery and hybrid electric platforms are distinct from traditional vehicle categories. These segments show modest growth as they integrate into broader categories like passenger EVs and LCV EVs.

Based on system, the automotive energy recovery system market is segmented into kinetic energy recovery systems (KERS), regenerative braking systems, exhaust energy recovery systems (EERS), and suspension-based energy recovery systems. The regenerative braking systems segment dominates with 49% market share in 2025.

- Regenerative braking systems dominate the fastest-growing technological segment. Their widespread adoption is driven by their necessity across all electrified powertrains, including battery electric, plug-in hybrid, full hybrid, and mild hybrid (48V) systems.

- Global EV sales are expected to reach 17 million in 2024 (20% of new car sales) and exceed 20 million in 2025 (25% market share), driving demand for regenerative braking systems.

- Regulatory mandates drive electrification in the segment. The EPA targets 55-67% BEV penetration by MY2032, while California mandates 100% ZEVs by 2035, ensuring sustained growth.

- Supportive government policies, strict emission norms, and rising demand for eco-friendly vehicles drive the dominance of regenerative braking. OEMs are integrating advanced systems to enhance energy recovery and ensure sustainability.

- Exhaust energy recovery systems (EERS) are growing rapidly with a CAGR of 12.2% from 2026 to 2035, due to their ability to convert exhaust heat into usable energy. This technology enhances fuel economy and supports compliance with strict CO2 and emission regulations.

- Advancements in thermoelectric materials, turbo-compounding, and integrated powertrain solutions drive EERS growth. Automakers increasingly adopt EERS to improve energy efficiency without sacrificing engine performance, focusing on hybrid and electric commercial vehicles.

- Kinetic energy recovery systems (KERS) store braking energy as mechanical or electrical energy for reuse. This technology boosts efficiency acceleration, saves fuel, and reduces emissions, especially in stop-and-go driving conditions.

- Advancements in energy storage and compact designs, along with rising demand for fuel-efficient vehicles, are driving KERS adoption. OEMs are integrating KERS with hybrid powertrains to enhance energy efficiency and sustainability in passenger and commercial vehicles.

- Suspension-based energy recovery systems capture energy from a vehicle's vertical suspension movements. This technology is ideal for heavy-duty vehicles, buses, and urban transit systems, which frequently encounter uneven roads or stop-and-go traffic.

Based on propulsion, the automotive energy recovery system market is divided into internal combustion engine (ICE) vehicles, hybrid electric vehicles (HEV), plug in hybrid electric vehicles (PHEV) and battery electric vehicles (BEV). The hybrid electric vehicles (HEV) dominate with 47% market share in 2025.

- The Hybrid Electric Vehicles (HEVs/PHEVs) segment includes full hybrids (e.g., Toyota Prius, Honda Insight), plug-in hybrids (e.g., BMW 5-series, Ford Escape), and mild hybrids with 48V battery-integrated starter-generator systems.

- Hybrid architecture integrates regenerative braking as core functionality, capturing braking energy and storing it in battery packs for subsequent electric motor propulsion, engine-off operation, or electric accessory power.

- Hybrids are seen as "transition" technologies, offering extended range over BEVs and better efficiency than ICE vehicles. California's Advanced Clean Cars II regulations include PHEVs as zero-emission vehicles, maintaining their relevance in North America.

- However, hybrid market share faces long-term pressure from improving BEV range, declining battery costs, and expanded charging infrastructure reducing the compromises that historically favored hybrid architecture.

- The internal combustion engine (ICE) vehicles segment includes conventional gasoline and diesel vehicles, utilizing turbochargers, EGR systems, and waste heat recovery to enhance efficiency.

- ICE vehicles will dominate global production in 2024, accounting for 75-80%. However, their share is projected to decline to 40-45% by 2034 as electrification accelerates.

- Regulatory pressures, such as NHTSA's 50.4 mpg target by MY2031 and the EU's 37.5% CO2 reduction goal, are driving growth in the ICE segment. These regulations are boosting turbocharger adoption and advanced technologies like EGR systems, electric turbo-compounding, and waste heat recovery in commercial applications.

- BEVs universally require regenerative braking systems as fundamental powertrain components, with energy recovery capabilities directly impacting electric range, battery cycle life, and consumer acceptance.

- With 17 million global EV sales in 2024 (20% new car share) projected to exceed 20 million in 2025 (25% share), the BEV segment constitutes the fastest-growing vehicle propulsion category.

Looking for region specific data?

Germany dominates the Europe automotive energy recovery system market, showcasing strong growth potential, with a CAGR of 10% from 2026 to 2035.

- In Germany, automotive OEMs and component manufacturers are enhancing energy recovery systems by merging regenerative braking, exhaust energy recovery, and thermal management solutions with electrified and hybrid powertrains.

- Government regulations, emission reduction mandates, and sustainability programs are driving the swift adoption of advanced energy recovery technologies across passenger vehicles, commercial fleets, and urban transport.

- German vehicle manufacturers are adopting advanced powertrain systems, energy storage solutions, and electrification to improve energy recovery, reduce fuel use, and lower CO2 emissions.

- German OEMs and technology providers are developing modular energy recovery platforms for seamless integration across vehicle segments, strengthening Germany’s role in sustainable mobility and advanced automotive technologies.

Europe dominated the automotive energy recovery system market, which accounted for USD 9.2 billion in 2025 and is anticipated to show growth of 9.7% CAGR over the forecast period.

- Europe's market is growing due to decarbonization policies, high electrification rates, and concentrated production in Germany, Spain, France, and Italy. This drives demand for technologies like regenerative breaking.

- In response to stringent emissions regulations, such as the Euro 7 standards and a mandated 37.5% CO2 reduction by 2030, OEMs are now integrating energy recovery systems into both passenger and commercial vehicles.

- European OEMs such as Volkswagen Group, Stellantis, Renault-Nissan-Mitsubishi, BMW, Mercedes-Benz, and Volvo are actively committing to electrification roadmaps, driving widespread adoption of regenerative braking systems and other energy recovery technologies.

- Stricter urban air quality regulations in cities like London, Paris, and German locales are driving the electrification of commercial vehicles. This trend highlights the rising significance of energy recovery solutions.

- Rising fuel prices and a growing consumer preference for fuel-efficient vehicles are driving the adoption of energy recovery technologies, such as turbochargers and exhaust energy recovery systems, even in internal combustion engine (ICE) vehicles.

- Germany's robust industrial base, significant vehicle production volume, and forward-thinking regulatory landscape position it at the forefront of Europe's automotive energy recovery system market.

- The market in Spain, France, Italy, and the Nordics is driven by government decarbonization policies, rising EV adoption, and Euro 7 emissions standards. Spain and Italy focus on automotive production, while France and the Nordics emphasize sustainability and technology.

China leads in Asia Pacific automotive energy recovery system market growing with a CAGR of 12.2% from 2026 to 2035.

- China's market is growing rapidly, driven by large-scale automotive production, increased adoption of electric and hybrid vehicles, and government policies like the NEV policy and zero-emission zones.

- Government policies and incentives are driving OEMs to adopt advanced energy recovery technologies, ensuring compliance with CO2 and emission reduction targets.

- China's strong automotive supply chain and advanced manufacturing enable cost-efficient, large-scale production of energy recovery systems.

- BYD, SAIC Motor, NIO, and Geely, prominent OEMs and component manufacturers, are adopting solutions like regenerative braking, exhaust energy recovery, and thermal management to enhance energy efficiency, extend vehicle range, and boost operational performance.

- Advancements in energy storage, power electronics, and vehicle integration enhance system efficiency and reliability, driving the adoption of energy recovery technologies in hybrid and electric vehicles.

- China leads the Asia Pacific market for automotive energy recovery systems, driven by strong regulations, urbanization-induced traffic congestion, and growing demand for eco-friendly, cost-efficient vehicles.

Asia Pacific is the fastest growing automotive energy recovery system market, which is anticipated to grow at a CAGR of 14.1% between 2026 and 2035.

- The Asia Pacific leads the market, driven by China's vehicle production, EV leadership, and supportive government policies. These factors boost demand for regenerative breaking and energy recovery technologies.

- Japan's automotive sector, driven by OEMs like Toyota, Honda, and Nissan, leads in hybrid vehicles and energy recovery solutions such as regenerative braking and turbochargers.

- India's automotive market is expanding rapidly. With the push for electrification through the FAME program and the rollout of Bharat Stage VI emissions standards, the market for energy recovery systems is seeing a significant boost. This surge spans across passenger cars, two-wheelers, and commercial vehicles.

- Hyundai Motor drives South Korea's investments in vehicle electrification, integrating regenerative braking and thermal management into passenger and commercial vehicles.

- Thailand and Indonesia, among other ASEAN nations, play a pivotal role in production volumes. Their advancements in domestic supply chains have not only reduced costs but also bolstered the widespread adoption of energy recovery technologies.

- Rapid urbanization in Asia Pacific worsens traffic congestion, driving demand for energy recovery systems. These systems enhance fuel efficiency, reduce emissions, and strengthen the region's market leadership.

The automotive energy recovery system market in US is expected to experience significant and promising growth from 2026 to 2035.

- Strong electrification policies, a robust automotive manufacturing infrastructure, and a high adoption rate of hybrid and electric vehicles propel the United States to the forefront of North America's automotive energy recovery system market.

- OEMs, fleet operators, and commercial vehicle manufacturers are adopting regenerative breaking, exhaust energy recovery, and thermal management systems to boost fuel efficiency and meet EPA and state regulations.

- Federal and state incentives, including the Inflation Reduction Act, California's Advanced Clean Cars II mandate, and EPA MY2027+ standards, are driving the adoption of energy recovery technologies in passenger and commercial vehicles.

- Vehicle manufacturers are adopting modular energy recovery platforms with advanced powertrain control, energy storage, and thermal management solutions to improve efficiency and performance.

- Advancements in energy recovery systems are driven by strong R&D, technological partnerships, and investments in electrified powertrains. These efforts enhance regenerative braking, waste heat recovery, and vehicle sustainability.

North America dominated the automotive energy recovery system market is anticipated to grow at a CAGR of 10.1% during the analysis timeframe.

- North America dominates the market due to high vehicle production in the U.S., Mexico, and Canada. Advanced infrastructure, a mature supply chain, and policies like the Inflation Reduction Act and EPA MY2027+ standards drive growth.

- The U.S. leads regional growth with rising adoption of hybrid and electric vehicles. Large pickup trucks, SUVs, and heavy-duty vehicles drive demand for advanced systems like regenerative braking and turbocharging to meet CO2 and fuel economy standards.

- Urban fleet electrification, government incentives, and a rising adoption of energy recovery technologies in both passenger and commercial vehicles are driving Canada's market growth.

- Clear state-level regulations in California, Arizona, and Texas drive OEMs to adopt advanced energy recovery systems, meeting ZEV mandates and fuel economy standards. This fosters technological adoption across vehicle segments.

- North America's strong domestic supply chain supports the energy recovery system market by enabling cost-effective, localized production of regenerative braking, exhaust energy recovery, and thermal management systems.

- North America's diverse deployment scenarios and rising demand for fuel-efficient vehicles drive market growth, aiding passenger and commercial fleets in meeting evolving standards.

Brazil leads the Latin American automotive energy recovery system market, exhibiting remarkable growth of 15.4% during the forecast period of 2026 to 2035.

- Brazil's market is growing due to a large vehicle fleet, rising hybrid and electric vehicle adoption, and government efforts to enhance fuel efficiency and reduce emissions.

- Low awareness and high initial costs limit the adoption of energy recovery technologies, especially in cost-sensitive sectors.

- Automotive OEMs and fleet operators are adopting regenerative braking, exhaust heat recovery, and thermal management systems to boost efficiency and lower costs.

- Brazilian technology providers and component manufacturers are collaborating with automakers to develop cost-effective, durable energy recovery solutions.

- With the rise of electrification and smart technologies, passenger vehicles, commercial fleets, and urban transport are adopting energy recovery systems to improve sustainability and efficiency.

South Africa to experience substantial growth in the Middle East and Africa automotive energy recovery system market in 2025.

- South Africa's market is growing due to rising hybrid and electric vehicle adoption, fuel efficiency focus, and government incentives for cleaner mobility.

- Infrastructure limitations, such as uneven road networks, inconsistent electricity supply, and a lack of awareness about energy recovery technologies, hinder widespread adoption.

- National and regional initiatives are driving OEMs and fleet operators to adopt regenerative braking, exhaust heat recovery, and thermal management systems for improved efficiency and sustainability.

- In South Africa, component manufacturers and tech providers are teaming up with automakers and fleet operators. Their goal To craft energy recovery solutions that are not only cost-effective and durable but also optimized for local driving conditions.

- Energy recovery systems are increasingly adopted in passenger vehicles, commercial fleets, and urban transport to improve efficiency, reduce fuel use, and support sustainability.

Automotive Energy Recovery System Market Share

- The top 7 companies in the automotive energy recovery system industry are ZF Friedrichshafen, Valeo, Continental, Denso, Hyundai Mobis, Forvia and Robert Bosch contributed around 31% of the market in 2025.

- ZF Friedrichshafen leads the automotive market with its advanced chassis systems, driveline technologies, and active safety solutions. On January 6, 2025, ZF announced a major deal with a global OEM to equip nearly 5 million vehicles with Electro-Mechanical Braking systems as part of a hybrid by-wire/hydraulic setup.

- Valeo focuses on 48-volt mild hybrid systems, thermal management technologies, and electrification solutions for passenger vehicles. Its affordable hybrid system targets mass-market ICE vehicles, enhancing efficiency through mild hybridization and expanding regenerative braking beyond full hybrids and battery electric platforms.

- Continental utilizes its diverse portfolio, including powertrain electronics, brake systems, turbocharging (via Siemens VDO acquisition), and sensors/actuators. Its expertise in power electronics and integrated brake systems strengthens its position in regenerative braking for electric vehicles.

- Denso, drawing on its deep expertise in hybrid and electric vehicle components, has forged long-standing partnerships with Toyota Motor Corporation and other Japanese OEMs.

- Hyundai Mobis provides energy recovery solutions, regenerative braking systems, and chassis systems. It primarily serves Hyundai Motor Group's Hyundai, Kia, and Genesis brands.

- Forvia, formed through the Faurecia-Hella merger, focuses on emission control, clean mobility, and interior systems. Its expertise in exhaust and catalytic technologies supports EGR systems, while Hella's electronics enhances energy management solutions.

- Robert Bosch, a leader in automotive technology, holds a notable share in energy recovery systems. Its expertise spans regenerative braking, brake-by-wire development, turbocharger technologies, and power electronics.

Automotive Energy Recovery System Market Companies

Major players operating in the automotive energy recovery system industry are:

- Continental

- Denso

- Forvia

- Hyundai Mobis

- Mahle

- Mando

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- Continental, Denso, and Forvia are bolstering their foothold in the automotive energy recovery system market. They're doing this by weaving in solutions like regenerative braking, exhaust energy recovery, and hybrid powertrains into both passenger and commercial vehicles. Leveraging technological innovations, forging strategic partnerships with OEMs, and deploying advanced energy management systems, these firms are not only boosting vehicle efficiency but also curbing emissions and elevating overall performance.

- Robert Bosch, Schaeffler, Valeo, and ZF Friedrichshafen lead the charge in energy recovery solutions. By focusing on cutting-edge control electronics, waste heat recovery, and regenerative braking, and bolstered by global partnerships and pioneering platform innovations, these companies are at the forefront of promoting efficient, sustainable, and electrified vehicle technologies on a global scale.

- Hyundai Mobis, Mahle, and Mando are at the forefront of providing advanced, modular energy recovery solutions. These innovations not only enhance fuel efficiency but also bolster the shift towards electrification. Through a strategic emphasis on R&D, the integration of hybrid powertrains, and cutting-edge thermal management technologies, these companies empower OEMs to navigate stringent regulatory benchmarks, all while ensuring reliability and adaptability across diverse vehicle segments.

Automotive Energy Recovery System Industry News

- In January 2025, ZF Friedrichshafen Secures Major Brake-By-Wire Deal ZF Friedrichshafen AG announced on January 6, 2025, that it won a contract to equip nearly 5 million vehicles with Electro-Mechanical Braking (EMB) as part of a hybrid by-wire/hydraulic braking system.

- In September 2024, BorgWarner launched its largest passenger car twin turbochargers for the General Motors Corvette ZR1, designed to power its 5.5-liter V8 engine, delivering 1,064 horsepower and 828 lb-ft of torque. The turbochargers feature a patented decoupled ball bearing system, offering faster response time, improved durability, and reduced noise.

- In January 2024, Cummins Turbo Technologies (CTT) launched the 8th generation Holset Series 400 Variable Geometry Turbocharger (HE400VGT), following the success of the 7th generation. This new turbocharger is engineered for the 10-15L heavy-duty truck market, offering a 5% efficiency improvement over its predecessor. It features advancements like a new bearing system, tighter clearances, and enhanced transient response.

The automotive energy recovery system market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Bn) and shipment (units) from 2022 to 2035, for the following segments:

Market, By Component

- Energy storage units

- Batteries

- Supercapacitors

- Flywheels

- Energy conversion units

- Electric motors/generators

- Hydraulic or pneumatic converters

- Control units

- Electronic control modules (ECM)

- Power management systems

Market, By Vehicle

- Passenger cars

- Hatchback

- SUV

- Sedan

- Commercial Vehicles

- Light commercial vehicles (LCVs)

- Medium commercial vehicles (MCVs)

- Heavy commercial vehicles (HCVs)

- Electric and hybrid vehicles

Market, By System

- Kinetic energy recovery systems (KERS)

- Regenerative braking systems

- Exhaust energy recovery systems (EERS)

- Suspension-based energy recovery systems

Market, By Propulsion

- Internal combustion engine (ICE) vehicles

- Hybrid electric vehicles (HEV)

- Plug in hybrid electric vehicles (PHEV)

- Battery electric vehicles (BEV)

Market, By Application

- Braking energy recovery

- Exhaust heat recovery

- Thermal management & waste heat utilization

- Powertrain efficiency enhancement

- Fuel economy improvement

- Performance boosting

- Others

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Nordics

- Benelux

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Singapore

- Thailand

- Indonesia

- Vietnam

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- MEA

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

Who are the key players in the automotive energy recovery system industry?

Key players include Continental, Denso, Forvia, Hyundai Mobis, Mahle, Mando, Robert Bosch, Schaeffler, Valeo, and ZF Friedrichshafen.

What are the key trends and growth prospects in the Automotive Energy Recovery System Market, and how are major players responding to emerging industry challenges?

The Automotive Energy Recovery System Market is experiencing significant growth due to increasing demand for fuel-efficient vehicles and stringent government regulations. Key trends include the adoption of regenerative braking systems, kinetic energy recovery systems, and exhaust energy recovery systems. Major players such as Bosch, Continental, and Denso are investing heavily in research and development to improve the efficiency and affordability of these systems. The market is expected to witness substantial growth over the next five years, driven by the rising demand for hybrid and electric vehicles, particularly in the Asia-Pacific region. However, industry challenges such as high development costs, complex system integration, and limited consumer awareness are hindering market growth, prompting major players to focus on collaborative partnerships, technology advancements, and targeted marketing strategies to address these challenges and capitalize on emerging opportunities.

What are the upcoming trends in the automotive energy recovery system market?

Key trends include integration of regenerative braking, thermal management, turbocharging, and power electronics into unified powertrain systems, advanced brake-blend control, and adoption of energy recovery systems optimized for urban stop-and-go driving.

What is the market size of the automotive energy recovery system in 2025?

The market size was USD 29.2 billion in 2025, with a CAGR of 11.9% expected through 2035. The market is driven by the need for fuel efficiency, emission reduction, and the transition to electrified powertrains.

What was the market share of the regenerative braking systems segment in 2025?

Regenerative braking systems held a 49% market share in 2025, emerging as the fastest-growing technological segment due to their necessity across all electrified powertrains.

Which region leads the automotive energy recovery system sector?

Germany leads the European market with a projected CAGR of 10% from 2026 to 2035.

What was the market share of the passenger vehicle segment in 2025?

The passenger vehicle segment dominated with a 62% market share in 2025 and is set to expand at a CAGR of 12% till 2035.

What was the market share of the energy storage units segment in 2025?

The energy storage units segment held a 46% market share in 2025 and is expected to grow at a CAGR of 12.2% up to 2035.

What is the expected size of the automotive energy recovery system industry in 2026?

The market size is projected to reach USD 32.5 billion in 2026.

What is the projected value of the automotive energy recovery system market by 2035?

The market is poised to reach USD 89.2 billion by 2035, fueled by advancements in regenerative braking, thermal management, and integrated powertrain systems.

Automotive Energy Recovery System Market Scope

Related Reports