Authors:

Suraj Gujar, Ankita Chavan

Download free PDF

Anti-Corrosion Packaging Market Size & Share 2026-2035

Report ID: GMI15759

|

Published Date: April 2026

|

Report Format: PDF/Excel/Dashboard/Platform

Download Free PDF

Explore Our Licensing Options:

Jump to Content

Market Size

Market Trends

Market Analysis

Market Share

Market Companies

Industry News

Table of Contents

Frequently Asked Questions

Research Methodology

Related Reports

Download Free PDF

Anti-Corrosion Packaging Market

Get a free sample of this report

Get a free sample of this report Anti-Corrosion Packaging Market

Is your requirement urgent? Please give us your business email

for a speedy delivery!

Anti-Corrosion Packaging Market Size

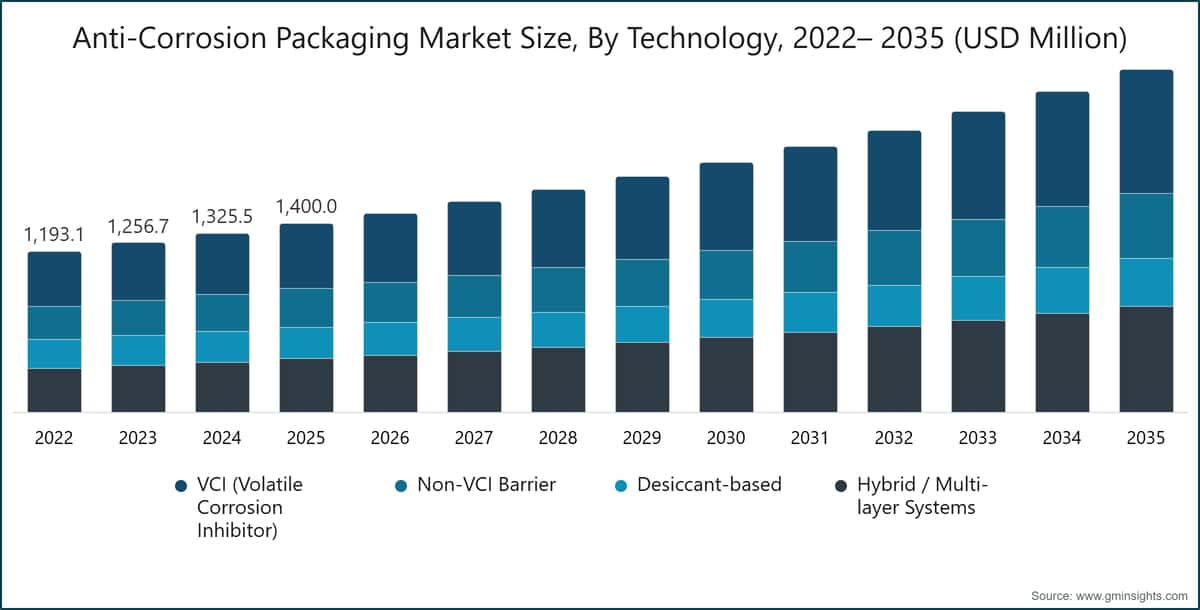

The global anti-corrosion packaging market was valued at USD 1.4 billion in 2025. The market is expected to grow from USD 1.5 billion in 2026 to USD 2 billion in 2031 & USD 2.5 billion in 2035, at a CAGR of 6.2% during the forecast period according to the latest report published by Global Market Insights Inc.

Anti-Corrosion Packaging Market Key Takeaways

Market Leader: Cortec Corporation led with over 14.6% market share in 2025.

Leading Players: Top 5 players in this market include Cortec Corporation, Daubert Cromwell Inc., Branopac GmbH, Armor Protective Packaging, Rust-X (Daubert VCI), which collectively held a market share of 46.2% in 2025.

The growth of the anti‑corrosion packaging market is attributed to rising industrial production and the increasing movement of metal components across global supply chains, which elevates the need for corrosion‑prevention solutions. Expanding shipments of electronics, machinery, and automotive parts have intensified the demand for packaging that protects goods from moisture, oxidation, and chemical exposure during storage and transit. Additionally, industries are prioritizing reduced product damage, lower maintenance costs, and improved durability standards, further reinforcing the adoption of advanced anti‑corrosion packaging across manufacturing, logistics, and export‑oriented sectors.

The anti‑corrosion packaging market is driven by rising output of metal parts, machinery, electronic devices, and vehicles that need effective protection against corrosion both in storage and while being shipped around the world. The U.S. Census Bureau report on durable goods in 2025 shows that the number of orders for durable goods rose by 7.3% in 2025 from 2024 in categories like fabricated metals, machinery, computer and electronic products. The higher levels of corrosion-sensitive durable goods have raised the demand for VCI films and moisture-resistant materials, contributing to the expansion of the market.

Additionally, growth in the anti-corrosion packaging market is further supported by the growing global supply chain of metal products, equipment, and electronics moving through humid, maritime, and climate-changing locations. The likelihood of rusting becomes higher under such circumstances, leading to an increase in the use of high-quality VCI film and moisture-barrier packing. As per WTO Global trade outlook and statistics report 2025, the worth of world merchandise exports has increased by 2% in 2024, totaling to USD 24.43 trillion, which reflects the continuous growth in the international flow of manufactured goods, which further indicates ongoing recovery and expansion in merchandise flows, reinforcing the need for protective packaging as cross border shipping intensifies.

The market increased steadily from USD 1.2 billion in 2022 and reached USD 1.3 billion in 2024, driven by rising industrial production and increased movement of metal components across complex global supply chains, the anti‑corrosion packaging market continues to expand. Growth in the shipment of electronics, machinery, and precision parts has increased the need for protective materials that prevent moisture‑ and oxidation‑related damage. Industries are also focusing more on product durability, reduced rejection rates, and safer long‑distance transport of corrosion‑sensitive goods. Regulatory emphasis on minimizing material losses and improving storage reliability further encourages adoption of corrosion‑preventive packaging which is leading to steady demand for advanced anti‑corrosion packaging across manufacturing, logistics, and export‑driven sectors.

Anti-Corrosion Packaging Market Trends

Anti-Corrosion Packaging Market Analysis

Based on technology, the anti-corrosion packaging market is segmented into VCI (volatile corrosion inhibitor), non-VCI barrier, desiccant-based and hybrid / multi-layer systems

Based on product format, the anti-corrosion packaging market is divided into films, bags & pouches, foils, paper & paperboards and emitters & devices.

Based on base material, the anti-corrosion packaging market is divided into polyethylene (PE), polypropylene (PP), aluminum / metal foil, paper and bio-based polymers.

North America Anti-Corrosion Packaging Market

North America held a share of 28.5% of market in 2025.

The U.S. anti-corrosion packaging market size reached USD 1.1 billion in 2025, growing from USD 1.07 billion in 2024.

Europe Anti-Corrosion Packaging Market

Europe market accounted for USD 254.7 million in 2025 and is anticipated to show lucrative growth over the forecast period.

Germany dominates the Europe anti-corrosion packaging market, showcasing strong growth potential.

Asia Pacific Anti-Corrosion Packaging Market

The Asia Pacific market is anticipated to grow at the highest CAGR of 7% during the forecast period.

China anti-corrosion packaging market is estimated to grow with a significant CAGR, in the Asia Pacific market.

Middle East and Africa Anti-Corrosion Packaging Market

Saudi Arabia market to experience substantial growth in the Middle East and Africa.

Anti-Corrosion Packaging Market Share

The market is led by players such as Cortec Corporation, Daubert Cromwell Inc., Branopac GmbH, Armor Protective Packaging and Rust-X (Daubert VCI), which together account for 46.2% share of the global market. These companies have a dominant position in the market with a diverse array of VCI films, papers, coatings, and multilayered barrier technology for safeguarding metals, equipment, and parts from corrosion during storage and international transportation. Their product lines feature protective solutions that prevent rusting, specific packaging solutions, and rust-inhibiting chemicals.

These companies benefit from excellent manufacturing facilities, good reputation in the industry, and experience in corrosion prevention technology. The investment they make in the research and development of new VCI compounds, environment-friendly material, and superior corrosion protection systems helps them fulfill the demands of the growing industry and exports packaging needs. This further enhances their position in the global market of anti-corrosion packaging.

Anti-Corrosion Packaging Market Companies

Prominent players operating in the anti-corrosion packaging industry are as mentioned below:

Cortec Corporation offers a comprehensive range of VpCI®‑based films, papers, coatings, and emitters engineered to prevent corrosion during storage and global transit of metal components. The company differentiates through advanced vapor‑phase inhibitor chemistry that provides long‑lasting, residue‑free protection across automotive, machinery, and industrial supply chains.

Daubert Cromwell Inc. provides premium VCI papers, films, and protective packaging systems widely adopted in metal fabrication, stamping, and heavy‑equipment manufacturing. The company differentiates through proven corrosion‑inhibitor formulations and consistent performance that meets the handling and export requirements of precision metal parts.

Branopac GmbH delivers specialized BRANOrost and BRANOfol anti‑corrosion packaging solutions designed for high‑value metals and machinery shipped through demanding logistics environments. The company differentiates through engineered material structures that offer durable moisture and oxidation resistance for long‑distance international shipments.

Armor Protective Packaging supplies VCI films, wraps, and rust‑removal products tailored for automotive, industrial, and machinery applications. The company differentiates through its corrosion‑inhibiting nanotechnology designed to provide clean, residue‑free protection and maintain part-cleanliness for immediate downstream processing.

RustX offers an extensive portfolio of VCI films, foams, oils, and packaging solutions engineered for export‑grade corrosion protection across metals and industrial assemblies. The company differentiates through fast‑acting corrosion‑inhibitor chemistry developed for high‑humidity environments common in global shipping and long‑term storage conditions.

14.6% market share in 2025

Collective market share in 2025 is 46.2%

Anti-Corrosion Packaging Industry News

The anti-corrosion packaging market research report includes in-depth coverage of the industry with estimates and forecast in terms of revenue (USD Million) from 2022 – 2035 for the following segments:

Click here to Buy Section of this Report

Market, By Technology

Market, By Product Format

Market, By Base Material

Market, By End-User Application

The above information is provided for the following regions and countries:

Table of Contents

Chapter 1 Methodology and Scope

Chapter 2 Executive Summary

Chapter 3 Industry Insights

Chapter 4 Competitive Landscape, 2025

Chapter 5 Market Estimates and Forecast, By Technology, 2022 – 2035 (USD Million)

Chapter 6 Market Estimates and Forecast, By Product Format, 2022 – 2035 (USD Million)

Chapter 7 Market Estimates and Forecast, By Base Material, 2022 – 2035 (USD Million)

Chapter 8 Market Estimates and Forecast, By End-User Application, 2022 – 2035 (USD Million)

Chapter 9 Market Estimates and Forecast, By Region, 2022 – 2035 (USD Million)

Chapter 10 Company Profiles

Don't see your key competitors?

The companies listed in this report are a curated selection - not the full competitive universe.

Our market revenue calculations use a bottom-up methodology that accounts for all players across all regions - including manufacturers, distributors, and specialists not individually profiled. The profiles section spotlights strategically significant players; it does not define the scope of our market sizing.

Your competitive landscape may also include

Free customization - up to 20% of report value

Need specific data? Request customization and get the insights tailored to your exact requirements.

Research methodology, data sources & validation process

This report draws on a structured research process built around direct industry conversations, proprietary modelling, and rigorous cross-validation and not just desk research.

Our 6-step research process

1. Research design & analyst oversight

At GMI, our research methodology is built on a foundation of human expertise, rigorous validation, and complete transparency. Every insight, trend analysis, and forecast in our reports is developed by experienced analysts who understand the nuances of your market.

Our approach integrates extensive primary research through direct engagement with industry participants and experts, complemented by comprehensive secondary research from verified global sources. We apply quantified impact analysis to deliver dependable forecasts, while maintaining complete traceability from original data sources to final insights.

2. Primary research

Primary research forms the backbone of our methodology, contributing nearly 80% to overall insights. It involves direct engagement with industry participants to ensure accuracy and depth in analysis. Our structured interview program covers regional and global markets, with inputs from C-suite executives, directors, and subject matter experts. These interactions provide strategic, operational, and technical perspectives, enabling well-rounded insights and reliable market forecasts.

3. Data mining & market analysis

Data mining is a key part of our research process, contributing nearly 20% to the overall methodology. It involves analysing market structure, identifying industry trends, and assessing macroeconomic factors through revenue share analysis of major players. Relevant data is collected from both paid and unpaid sources to build a reliable database. This information is then integrated to support primary research and market sizing, with validation from key stakeholders such as distributors, manufacturers, and associations.

4. Market sizing

Our market sizing is built on a bottom-up approach, starting with company revenue data gathered directly through primary interviews, alongside production volume figures from manufacturers and installation or deployment statistics. These inputs are then pieced together across regional markets to arrive at a global estimate that stays grounded in actual industry activity.

5. Forecast model & key assumptions

Every forecast includes explicit documentation of:

✓ Key growth drivers and their assumed impact

✓ Restraining factors and mitigation scenarios

✓ Regulatory assumptions and policy change risk

✓ Technology adoption curve parameter

✓ Macroeconomic assumptions (GDP growth, inflation, currency)

✓ Competitive dynamics and market entry/exit expectations

6. Validation & quality assurance

The final stages involve human validation, where domain experts manually review filtered data to identify nuances and contextual errors that automated systems might miss. This expert review adds a critical layer of quality assurance, ensuring data aligns with research objectives and domain-specific standards.

Our triple-layer validation process ensures maximum data reliability:

✓ Statistical Validation

✓ Expert Validation

✓ Market Reality Check

Trust & credibility

Verified data sources

Trade publications

Security & defense sector journals and trade press

Industry databases

Proprietary and third-party market databases

Regulatory filings

Government procurement records and policy documents

Academic research

University studies and specialist institution reports

Company reports

Annual reports, investor presentations, and filings

Expert interviews

C-suite, procurement leads, and technical specialists

GMI archive

13,000+ published studies across 30+ industry verticals

Trade data

Import/export volumes, HS codes, and customs records

Parameters studied & evaluated

Every data point in this report is validated through primary interviews, true bottom-up modelling, and rigorous cross-checks. Read about our research process →