Summary

Table of Content

AI Orchestration Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

AI Orchestration Market Size

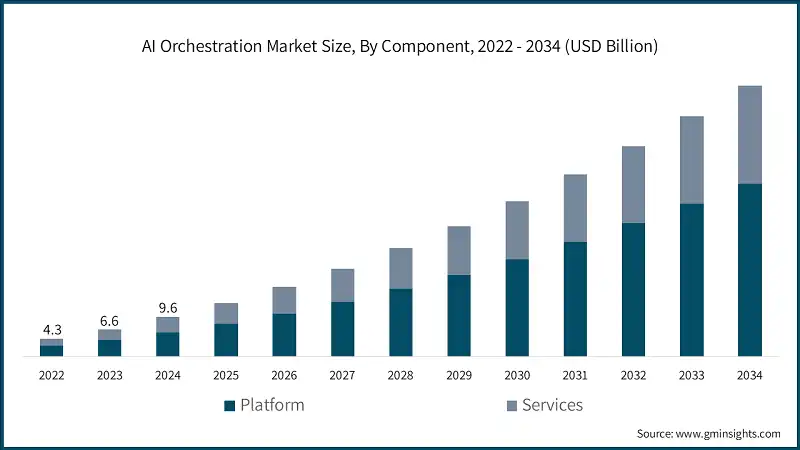

The global AI orchestration market size was estimated at USD 9.6 billion in 2024. The market is expected to grow from USD 12.9 billion in 2025 to USD 65.4 billion in 2034, at a CAGR of 19.8% according to latest report published by Global Market Insights Inc.

To get key market trends

The AI orchestration market is growing quickly with a strong government commitment to AI frameworks. The OECD reported total public R&D expenditure on AI reached over USD 22 billion in 2024 to enable workflow automation, model orchestration, and multi-cloud integration across sectors.

The rate of public sector adoption is increasing quickly, with more than 60% of Fortune 1000 companies deploying AI orchestration for workflow automation, real-time analytics, and managing and accessing the lifecycle of models. National innovation agencies stress the importance of orchestration to drive efficiency in the allocation of resources and establish scalable, data-driven decision-making processes.

Research institutions and supercomputing centers around the world underpin the ecosystem processing large-scale AI-enabled workloads. For instance, the EU now has a system of EuroHPC high-performance centres across 20 locations and leverages orchestration to develop training of AI models, simulations, and predictive analytics to improve manufacturing, the health sector, and scientific purposes.

The public sector initiatives are increasingly deploying AI orchestration for smart governance, transportation, and energy. Governments in the US, China, Germany and Brazil note that 40-55% of their agencies have implemented AI orchestrated systems to automate administrative processes while improving operational efficiency.

The adoption of AI-enabled industrial automation is also influencing demand for orchestration, and respectively orchestration platforms are being integrated with other AI technologies to enable predictive maintenance, adaptive production, and real-time work monitoring in manufacturing, logistics, and energy, with governments noting that they are working with over 4,000 AI based start-ups globally integrating orchestrated AI platforms with operational models to enable predictive maintenance, adaptive production, and real-time monitoring that supports sustainable, efficient and resilient operations.

AI Orchestration Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 9.6 Billion |

| Market Size in 2025 | USD 12.9 Billion |

| Forecast Period 2025 - 2034 CAGR | 19.8% |

| Market Size in 2034 | USD 65.4 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Growing enterprise adoption of generative AI & LLMs | Drives need for orchestration platforms to automate multi-model workflows |

| Expansion of hybrid and multi-cloud deployments | Increases demand for unified orchestration across distributed AI infrastructures |

| Rising focus on operationalizing AI (MLOps + AIOps convergence) | Enhances efficiency and governance of end-to-end AI lifecycle |

| Surge in AI application scaling for real-time decisioning | Boosts adoption of low-latency orchestration layers for continuous model deployment |

| Pitfalls & Challenges | Impact |

| Integration complexity across heterogeneous environments | Increases implementation cost and slows enterprise adoption |

| High dependency on cloud providers & vendor lock-in | Limits flexibility for enterprises using diverse AI tools |

| Opportunities: | Impact |

| Growth of AI orchestration for edge and IoT ecosystems | Expands market scope into real-time and low-power environments |

| Rising demand for autonomous orchestration (self-optimizing workflows) | Enables AI-driven decision automation across industries |

| Market Leaders (2024) | |

| Market Leaders |

20% market share |

| Top Players |

Collective market share in 2024 is 58% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | North America |

| Fastest growing market | Asia Pacific |

| Emerging countries | India, South Korea, Singapore, Brazil |

| Future outlook |

|

What are the growth opportunities in this market?

AI Orchestration Market Trends

Unified platform convergence is reshaping AI orchestration, as organizations begin to adopt packaged integrated solutions including data management, model lifecycle, and workflow orchestration. Governments are reporting that globally more than 65% of enterprises are moving towards unified platforms as a means to reduce complexity and improve AI governance.

Another notable mention is the ecosystem integration that orchestration platforms are building, which offer APIs and pre-built connectors to integrate enterprise systems and third-party tools. Public data coming from the EU Digital Innovation Hub cites ecosystem integration as the highest priority, with 58% of organizations indicating these needs to leverage existing technology investments effectively.

Hybrid orchestration approaches are also making headway by supporting on-premise and cloud deployment approaches. Reports from the US National Institute of Standards and Technology (NIST), note that 62% of enterprises deploy hybrid AI workloads to both meet performance and security/compliance requirements while not indemnifying against inefficient use of resources.

Multi-cloud orchestration is becoming increasingly relevant to eliminate vendor lock-in and assure optimized workloads. Research done by the German Federal Ministry for Economic Affairs indicate that for organizations, 47% operate across multiple cloud providers, while leveraging transport orchestration solutions to provide alignment of governance and optimized resource allocation.

No-code and low-code orchestration interfaces allow for democratization of AI workflow management. Reports from Brazil's Ministry of Science and Technology states 51% of small and medium enterprises are adopting visual workflow tools, and of self-automated configuration features to accelerate AI adoption without deep technical expertise.

AI Orchestration Market Analysis

Learn more about the key segments shaping this market

Based on component, the AI orchestration market is divided into platform and services. The platform segment dominated the market in 2024, accounting for 61% share of total revenue.

- The platform segment leads in AI orchestration, and offers sophisticated functionalities such as automated model deployment, intelligent resource allocation, integrated governance, and real-time monitoring of model performance. Government reports show that 70% of large enterprises place significant priority on developing robust platform infrastructures to effectively manage their multi-cloud and on-premise AI workflows.

- Cloud-native platforms are a significant growth driver for orchestration, taking advantage of the scalability and flexibility, along with the overall cost efficiency, of modern cloud infrastructures. The US Department of Energy states that more than 65% of AI research projects now utilize cloud-native orchestration platforms for high performance model training and deployment processes.

- The services segment includes consulting, implementation, training, and managed services that facilitate the adoption of orchestration technology. Based on Germany’s EU Digital Innovation Hub, about 58% of enterprises rely on formalized and specialized services to overcome the complexities of the integration process, regulatory compliance, and established protocols required to operationalize an AI orchestration platform.

- Professional services are being increasingly specialized by industry and application. Germany’s Federal Ministry for Economic Affairs reports that 62% of orchestration service providers are specifically focusing on solutions relating to a sector, including manufacturing, finance, and healthcare industries, to ensure compliance and alignment with regulatory and stakeholder guidelines.

- The managed services segment continues to expand in importance, for ongoing the optimization of the platform, monitoring, and platform governance. In Brazil, the Ministry of Science and Technology reports 49% of users utilizing managed services to outsource operations of their AI orchestration platform.

Learn more about the key segments shaping this market

Based on deployment, the AI orchestration market is segmented into on-premise, cloud-based and hybrid. The cloud-based segment dominated the market in 2024 and is expected to grow at a CAGR of 21.1% from 2025 to 2034.

- Cloud-based deployment is the dominant model due to its scalability, flexibility, and speed in provisioning resources. The European Commission has stated that according to a recent survey, more than 60% of AI projects within EU research institutions use some form of cloud-based orchestration to facilitate high-performance training of models and manage workflows across multiple clouds.

- Cloud-based orchestration appears highly valued among small and medium enterprises as well. Brazil’s Ministry of Science and Technology reports that 55% of small and medium enterprises are using cloud-based AI platforms to accelerate workflow automation, reduce infrastructure costs, and access advanced machine learning without incurring high capital costs.

- The on-premise deployment option is still relevant for organizations that must closely control their data and AI workloads. For example, the US Department of Commerce’s National Institute of Standards and Technology recently reported that in regulated sectors like finance or healthcare, 52% of enterprises preserve on-premise orchestration in the interest of compliance and security.

- Hybrid orchestration provides the ability to optimize workload placement across environments while providing consistent governance across the environments. The Office of Artificial Intelligence in the United Arab Emirates reported that 46% of governmental agencies are currently leveraging hybrid orchestration for their AI workloads.

Based on organization size, the AI orchestration market is segmented into large enterprises and small & medium enterprises (SMEs). The large enterprises segment dominated the market in 2024 and is expected to grow at a CAGR of 18.7% from 2025 to 2034.

- Large Enterprises tend to be the first adopters of AI orchestration, using these platforms to manage multifaceted AI environments across multiple clouds. According to the US Government Accountability Office, 68% of Fortune 500 Companies are using orchestration to organize and align AI efforts across the world and across business units.

- Large organizations are investing in orchestration teams, often doing so as internal specialized teams of, or alongside, compliance, performance, or risk teams, to better coordinate performance and compliance across departments. And Germany’s Federal Ministry for Economic Affairs has indicated that 64% of industrial conglomerates are using artificial intelligence operations teams to manage the rollout of platforms, workflow automation, and resource management.

- Small & Medium Enterprises (SMEs) are also seeing adoption of AI orchestration to streamline their operations, but generally with limited technical staff to execute. According to Brazil’s National Institute of Industrial Property, 57% of SMEs in technology and services effectively utilize cloud-based orchestration to assist with automating repeated processes to enhance efficiencies.

- SMEs are also taking advantage of existing designed templates, and no-code orchestration interfaces, which both reduce the difficulty of deploying orchestration. The UK Department for Business, Energy & Industrial Strategy noted that 52% of SMEs have already utilized low-code frameworks on AI orchestration with the intention of expediting model deployment to limit dependence on internal AI authorities.

Based on application, the AI orchestration market is segmented into model lifecycle management, data pipeline orchestration, workflow automation, resource optimization, monitoring & governance. The model lifecycle management segment dominated the market, accounting for share of 32% in 2024.

- Model Lifecycle Management enables end-to-end supervision of AI models, from versioning to deployment, and drift detection. The US office of Management and Budget reports that 62% of federal AI initiatives are now using Model Lifecycle Management practices to improve consistency, and support compliance.

- Data Pipeline Orchestration is an important capability that brings data together from multiple sources to work within an AI process. The Brazilian National Institute for Science and Technology reports that 58% of research institutions are operationalizing automated data pipelines to support high-volume analytics and real-time processing in AI-driven projects.

- Workflow Automation allows us to reduce manual efforts in AI processes to improve speed and reliability. Germany´s Federal Statistical Office reports that 54% of manufacturers and logistics firms have begun automating workflow orchestration to improve production planning, predictive analytics and scheduling maintenance.

- Resource Optimization, a key capability of orchestration platforms, focuses on the efficient use of computed and storage resources. The Office for Artificial Intelligence, United Kingdom, identifies that 47% of businesses using orchestration platforms, are now running dynamic resource scheduling to improve the use of idle compute cycles, and optimize the use of GPUs for large-scale AI workloads.

- Monitoring & Governance allows organizations to monitor AI performance and manage risk and compliance. The Telecommunications and Digital Government Regulatory Authority (TDGRA) identify that 51% of government agencies are employing automated monitoring dashboards, from orchestration platforms for governance purposes.

")

Looking for region specific data?

US dominates the North America AI orchestration market, generating USD 3.3 billion revenue in 2024.

- The US is rapidly bringing AI orchestration into enterprises, buoyed by deep federal investments in AI infrastructure. The US National AI Initiative Act supports interoperability and responsible AI adoption, bridging public and private uses of scalable orchestration frameworks.

- Federal government departments have allocated more than USD 2.3 billion of the US taxpayer's money to AI research and development programs many of these investments focused on automation and orchestration of data analyses, modeling, and supercomputing applications to improve efficiencies and US competitiveness in the market.

- In the enterprise sector, nearly 64% of Fortune 500 companies have implemented orchestration platforms to increase the efficiency of deploying AI models, and to decrease manual supervision while increasing decision automation, with a particular emphasis on the finance, manufacturing, and healthcare industries.

- In the US, the prominence of multi-cloud strategies has fueled interest in the orchestration tools sector to aid in enabling seamless management of AI workloads across AWS/Azure/Google Cloud and ensure that the dependencies comply with government data sovereignty and cybersecurity standards such as FedRAMP and NIST frameworks.

The AI orchestration market in the Germany is expected to experience robust growth of 21% from 2025 to 2034, driven by government AI initiatives and widespread adoption of cloud-based orchestration across industrial and public sectors.

- The government of Germany is encouraging AI orchestration adoption through its Federal Government AI Strategy over €5 billion has been pledged supporting initiatives through 2025. This initiative will foster the scaling of the nation’s AI infrastructure through orchestration platforms, and automation tools across multiple industrial, public administration and research sectors to support the national competitiveness agenda.

- The Federal Ministry for Economic Affairs and Climate Action (BMWK) announced several programs under “Digital Germany” to facilitate the integration of the workflow of AI into public administration. In Germany, over 60% of large enterprises have begun utilizing orchestration solutions to increase optimization of manufacturing, logistics automation and predictive analytics in a competitive environment.

- Four German institutes (The Fraunhofer Institutes and DFKI-German Research Center for Artificial Intelligence) are leading the way in national development of orchestration architectures that are interoperable. Through the AI Innovation Competition more than 200 active AI research-based projects are receiving funding with the goal of enhancing automation and real-time decision frameworks.

- The modernization of public administrations is driving the demand for orchestration and automation projects across German Federal Government agencies. The “GovTech Campus Germany” initiative will look to automate digital public services. Approximately 45% of Germany's federal government agencies are piloting various applications of AI-driven orchestration to assist processes such as document processing systems, systems for citizen engagement, and monitoring of cybersecurity to support enhanced data governance and efficiency.

- The push for industrial automation under the “Industry 4.0” agenda in Germany heavily depends on AI orchestration for smart manufacturing applications. Germany’s government has pledged €2.5 billion through the “Future Fund for AI Startups” to continue advancing the integration of orchestration platforms into enterprises to enable deferentially adaptive, data-driven production and energy efficient operations.

The AI orchestration market in China is expected to experience strong growth from 2025 to 2034, fueled by national AI strategies, high-tech manufacturing automation, and large-scale deployment of cloud-native orchestration platforms.

- Efforts by the Chinese government to promote AI are spurring the use of orchestration, particularly with the “New Generation Artificial Intelligence Development Plan," which has allocated in excess of ¥150 billion since 2020. The plan emphasizes automation of the AI infrastructure, orchestration of AI models, and data governance across national and industrial ecosystems.

- The Ministry of Industry and Information Technology has initiated over 200 pilot projects that promote AI orchestration for manufacturing, logistics, and smart cities. Approximately 68% of state-owned enterprises have embraced orchestration frameworks to manage multi-cloud AI workflows and drive efficient resource use.

- China’s National Supercomputing Centers in Guangzhou, Wuxi, and Tianjin have orchestration capabilities for large-scale AI workloads. Together these centers account for more than 70% of national AI model training, using orchestration layers to improve parallel computation and real-time data analytics.

- Public sector projects such as "Digital China" are accelerating the adoption of orchestrated AI in healthcare, education, and transportation. The government reports that over 45 provincial departments are using orchestration tools to manage AI enabled administrative and citizen service platforms.

- The rapid adoption of smart manufacturing as a result of “Made in China 2025” is powering orchestration in industrial automation. Additionally, over 6,000 AI-related startups registered in China by 2024. Government funding is supporting the development of orchestrated AI ecosystems with self-optimizing production and energy-efficient digital transformation.

The AI orchestration market in the UAE is anticipated to register consistent growth from 2025 to 2034, supported by smart city projects, federal AI initiatives, and increasing adoption of cloud-based orchestration in government and enterprise sectors.

- UAE is setting an ambitious pace with AI orchestration through its National Artificial Intelligence Strategy 2031 backed up with a federal investment exceeding AED 3 billion. The strategy is predicated on automation, orchestration and governance models for AI in order to establish the UAE as a technology hub in the region.

- The Office of Artificial Intelligence and the Telecommunications and Digital Government Regulatory Authority (TDRA) in the UAE advocate for orchestration frameworks across the areas of smart governance, utility services, and data analytics. Over 55% of government entities are already using AI orchestration to enhance efficiency of operations and automate public services.

- As part of the “UAE Digital Government 2025 initiatives”, key infrastructure projects involve the deployment of orchestrated AI systems that enable improved efficiency in traffic management, predictive maintenance, and energy distribution in smart buildings as in the Dubai Electricity and Water Authority (DEWA) which employs orchestration principles to monitor and optimize national utility networks in real-time.

- Also in the enterprise context, the UAE Ministry of Economy disclosed that nearly 47% of UAE companies are deploying AI orchestration to manage workflows in hybrid cloud scenarios; and to automate decision-making, particularly in finance and logistics as well as in smart construction sectors.

- The UAE has invested into an AI research ecosystem, with the Mohamed bin Zayed University of Artificial Intelligence (MBZUAI), focused on enabling self-optimizing orchestration systems. Federal partnerships are being established to build interoperable and secure AI orchestration platforms with global providers across the public and private sectors.

The Brazil AI orchestration market is anticipated to grow at a robust pace of 17.7% from 2025 to 2034, driven by AI adoption in agriculture, logistics, and SME digital transformation supported by federal innovation programs.

- Brazil is making progress in the adoption of AI orchestration through the National Artificial Intelligence Strategy (Estrategia Brasileira de Inteligência Artificial) with backing of more than BRL 1.2 billion in federal investment. The agenda focuses on AI workflow automation and orchestration, as well as private-public partnerships to improve efficiencies in government and industry.

- The Ministry of Science, Technology and Innovation (MCTI) has implemented over 150 pilot projects in agriculture, logistics, and smart city operations utilizing AI orchestration. Approximately 50% of large companies are utilizing an orchestration framework to improve decision-making and resource allocation, based on AI.

- Brazil’s research institutions such as the National Institute for Space Research (INPE) and the Brazilian Center for Research in Energy and Materials (CNPEM) are using orchestration in the training and simulation of AI models. These institutions are responsible for managing high-volume workloads for high-performance computing for predictive analytics and real-time applications.

- Adoption by the public sector under the “Gov.br Digital Transformation Program” uses AI orchestration for citizen services, tax collection and management, and health analytics. Reports from the federal government suggest that nearly 40% of government agencies are using orchestration to automate workflows and improve the governance of data assets.

- Industrial automation, in particular agriculture and manufacturing, is driving the uptake in orchestration. Given the reported 1,800 AI-oriented startups in 2024, the government is incentivizing orchestration-oriented platforms in support of adaptable production processes, predictive maintenance, or operational energy efficiencies in commercial and industry settings.

AI Orchestration Market Share

- The top 7 companies in the AI orchestration industry are Microsoft, Amazon (AWS), Google (Alphabet), DataRobot, Domino Data Lab, Palantir Technologies, NVIDIA, contributing around 67.5% of the market in 2024.

- Microsoft provides a unified AI orchestration experience with Azure AI, integrating capabilities such as MLOps, automated deployment, and model monitoring. Microsoft heavily targets enterprise-scale applications, enabling deployment and execution of multi-cloud AI workflows with governance, security, and compliance features.

- Amazon (AWS) delivers an AI orchestration experience through SageMaker and Bedrock, which are focused on deploying models, monitoring models, and optimizing AI models. Amazon emphasizes scalable, hybrid data center integration and end-to-end automation of workflows for both enterprise AI applications.

- Google (Alphabet) offers orchestration functionality through Vertex AI, which allows for management of the model lifecycle, automation of the data analytics and machine learning workflow, and deployment of models in a multi-cloud environment. Vertex AI enables enterprises to scale workflow across their cloud-based analytics and security functions while streamlining AI development.

- DataRobot offers scalable instant AI and orchestration, with instant deployment tools, with basic workflows enabled for both technical and non-technical users through low-code / AI-driven automation.

- Domino Data Lab provides AI orchestration tools for hybrid and on-premise enterprise deployment. It combines explained model repeatability with collaborative model development while allowing integration within their existing IT infrastructure and cloud services.

- Palantir Technologies provides AI orchestration capabilities with emphasis on data integration, governance, and real-time, large scale operational decision making in the governmental, defense and enterprise sectors, with powerful orchestrating workflows. Featuring relevant decision making and analytics for their social and governmental clients.

- NVIDIA provides AI orchestration technology with GPU-accelerated platforms (software development kits) to train and deploy models and optimize workflows. It specializes in high-performance computing, multi-cloud orchestration, and AI infrastructure for research and commercial use.

AI Orchestration Market Companies

Major players operating in the AI orchestration industry are:

- Amazon (AWS)

- DataRobot

- Domino Data Lab

- Google (Alphabet)

- IBM

- Microsoft

- NVIDIA

- Oracle

- Palantir Technologies

- Salesforce

- The AI orchestration market is evolving rapidly, as organizations invest in integrated platforms for model lifecycle management, workflow automation, and resource optimization. Governments around the world are funding AI infrastructure, with a public investment, enabling enterprises to run scalable, cloud-native solutions and orchestration tools designed for real-time AI analytics, predictive modeling, and multi-cloud AI workflows.

- Enterprises in all sectors are investing in orchestration to improve efficiency, governance, and decision-making. Public institutions and industrial organizations are deploying automated data pipelines, monitoring frameworks, and compliance-driven governance. Hybrid and cloud-based deployment models and no-code interfaces are democratizing access to AI, allowing small- to medium-sized enterprises to leverage orchestration capability to optimize operations.

AI Orchestration Industry News

- In January 2025, Microsoft announced enhancements to its Azure AI Orchestration Suite, introducing advanced multi-model workflow management, automated scaling reducing costs by up to 40%, and improved governance for audit trails and compliance.

- In December 2024, Google Cloud launched the Vertex AI Orchestration Platform, providing end-to-end workflow management, multi-cloud orchestration capabilities, and unified governance for complex AI deployments.

- In November 2024, DataRobot completed a $300 million Series G funding round led by Tiger Global Management, bringing total funding over $1 billion to expand product development, international operations, and orchestration platform capabilities.

- In October 2024, AWS introduced enhanced SageMaker Orchestration Services, including automated model deployment pipelines, comprehensive monitoring, and integration with AWS AI services, simplifying management of complex AI workflows.

- In September 2024, NVIDIA announced its AI Enterprise Orchestration Framework optimized for GPU workloads, featuring advanced scheduling to improve GPU utilization and performance by up to 60% for enterprise AI applications.

- In August 2024, Domino Data Lab acquired Cerebro Data, enhancing platform capabilities for distributed data processing, analytics orchestration, and integration with big data technologies.

- In July 2024, IBM launched its Watson Orchestration Platform, offering enterprise-grade AI workflow management across hybrid cloud environments with governance, security, and compliance features for regulated industries.

The AI orchestration market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) from 2021 to 2034, for the following segments:

Market, By Component

- Platform

- AI orchestration software

- Workflow engines

- MLOps integration tools

- Services

- Deployment

- Integration

- Maintenance

- Consulting

- Training

Market, By Deployment

- On-Premise

- Cloud-Based

- Hybrid

Market, By Organization Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

Market, By Application

- Model Lifecycle Management

- Data Pipeline Orchestration

- Workflow Automation

- Resource Optimization

- Monitoring & Governance

Market, By End-Use

- BFSI

- Healthcare

- Automotive

- Manufacturing

- Retail & E-commerce

- IT & Telecom

- Government & Public Sector

- Others

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Nordics

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Southeast Asia

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

Who are the key players in the AI orchestration industry?

Major players include Amazon (AWS), DataRobot, Domino Data Lab, Google (Alphabet), IBM, Microsoft, NVIDIA, Oracle, Palantir Technologies, and Salesforce.

What are the upcoming trends in the AI orchestration market?

Key trends include unified platform convergence, hybrid orchestration approaches, multi-cloud orchestration, no-code/low-code interfaces, and ecosystem integration to enhance AI governance and resource optimization.

Which region leads the AI orchestration sector?

The United States leads the North American market, generating USD 3.3 billion in revenue in 2024, supported by federal investments and the US National AI Initiative Act.

What is the growth outlook for the large enterprises segment from 2025 to 2034?

The large enterprises segment is expected to witness over 18.7% CAGR up to 2034, as these organizations lead in adopting AI orchestration to manage complex AI environments.

What was the valuation of the cloud-based segment in 2024?

The cloud-based segment is set to expand at a CAGR of 21.1% till 2034, led by scalability and multi-cloud adoption.

What is the expected size of the AI orchestration industry in 2025?

The market size is expected to grow to USD 12.9 billion in 2025.

How much revenue did the platform segment generate in 2024?

The platform segment generated 61% of the total market revenue in 2024, offering functionalities like automated model deployment, intelligent resource allocation, and real-time monitoring.

What is the projected value of the AI orchestration market by 2034?

The market is poised to reach USD 65.4 billion by 2034, fueled by advancements in unified platforms, hybrid orchestration, and ecosystem integration.

What is the market size of the AI orchestration in 2024?

The market size was estimated at USD 9.6 billion in 2024, growing at a CAGR of 19.8% through 2034, driven by increasing adoption of AI frameworks, workflow automation, and multi-cloud integration.

AI Orchestration Market Scope

Related Reports