Summary

Table of Content

U.S. Sustainable Interior Finishing Materials Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

U.S. Sustainable Interior Finishing Materials Market Size

The U.S. sustainable interior finishing materials market was valued at USD 12 billion in 2024. The market is expected to grow from USD 12.4 billion in 2025 to USD 17.6 billion in 2034, at a CAGR of 3.9%, according to the latest report published by Global Market Insights Inc.

U.S. Sustainable Interior Finishing Materials Market Key Takeaways

Market Size & Growth

- 2024 Market Size: USD 12 Billion

- 2025 Market Size: USD 12.4 Billion

- 2034 Forecast Market Size: USD 17.6 Billion

- CAGR (2025–2034): 3.9%

Key Market Drivers

- Federal procurement mandates & GSA specifications.

- LEED certification requirements & green building adoption.

- Indoor air quality regulations & health consciousness.

Challenges

- Higher initial cost premiums & ROI challenges.

- Limited manufacturing capacity for bio-based materials.

Opportunity

- Carbon-negative product development potential.

- Circular economy integration & take-back programs.

Key Players

- Market Leader: Armstrong World Industries led with over 7.9% market share in 2024.

- Leading Players: Top 5 players in this market include Armstrong World Industries, BASF, Mannington Commercial, 3M, Benjamin Moore & Co., which collectively held a market share of 32.4% in 2024.

Get Market Insights & Growth Opportunities

Sustainable interiors finishing materials are environmentally friendly, healthy, and energy-saving products intended for application indoors in flooring, wall covers, ceilings, or any other surface finishing in general. Generally, these materials are made from renewable sources and low-toxicity products and are designed to maximize recycling. The U.S. Environmental Protection Agency reports that entities like the General Services Administration must give preference to purchasing more environmentally sustainable products, promoting the use of low-VOC and environmentally friendly materials in federal buildings. Such mandates are also reinforced through extensive adoption of LEED (Leadership in Energy and Environmental Design) provisions-holding materials-specific criteria for enhance indoor air quality and overall sustainability characteristics of buildings.

According to the data of the U.S. Green Building Council, LEED-certified buildings had therefore multiplied tremendously, with countries being host to over 90,000 projects, which speaks to a shift toward greener building practices. Indoor air quality regulations, on the other hand, are getting tighter, due to the raising of awareness on health impacts of several volatile organic compounds (VOCs) outgassed by conventionally used interior finishes. Federal regulations by the EPA and the American Occupational Safety Health Administration (OSHA) promote the use of low-emitting material to protect occupant health. This synergy of policies and standards creates a competitive platform for the support of producers in the development and provision of sustainable health-promoting interior finishes.

A surge in demand for bio-based low-emission finishes is expected, reflecting an imminent new business model from the increasing emphasis on environmentally responsible and health-oriented building materials by government agencies and private sector players. This interconnected regulatory landscape, driven by federal procurement policies, LEED standards, and indoor air quality regulations, acts as a strong growth driver for the U.S. sustainable interior finishing materials market, fostering innovations, installations, and transitions toward healthier and sustainable building environments.

To get key market trends

U.S. Sustainable Interior Finishing Materials Market Trends

- The adoption of low-VOC and environmentally friendly materials is perhaps one of the most powerful trends in the sustainable interior finishing market in the US. Consumers and regulators are now demanding, in increasing numbers, for products to have negligible levels of Volatile Organic Compounds, indoor air pollution and its health effects have been raised to a much more seriously high-notched concern with these effects in consumers' minds. Adoption of such materials is not just a health consideration, for such materials are made more stimulating in market competition, as consumers start to demand that their interiors be safer and environmentally accountable according to the marketer’s trend among eco-conscious consumers.

- The transforming dynamic that's affecting the industry is on the introduction of recycled and bio-based materials into application through the strong principles of the circular economy. Interior finishes now include recycled content such as reclaimed wood, recycled plastics, or metal, thus lowering the dependence on virgin resources. Staying in the same lane, bio-based materials derive renewably-sourced, such as soy-based foams and plant-derived wall coverings, are increasingly popularized due to their lighter environmental footprint and biodegradability. This trend is partly a consequence of regulatory pressure and consumer demand toward manifest transparency and sustainability, thereby driving innovations in sourcing and processing raw materials, resulting in what the market now presents in diverse products with good performance but eco-consciousness which meets broader sustainability objectives.

- The unique demand for innovative and sustainable finishes is progressively elevating the innovation bar towards next-generation materials that integrate the best-of-breed technologies. Nanotechnology-enhanced coatings improve durability and reduce chemical consumption, while smart surfaces are engineered to have self-cleaning or air-purifying powers. Industry reshaped by investment in both R&D and production into multifunctional finishes meeting aesthetics and health as well as environmental needs has brought this trend. These innovations propel the market toward a future of more sustainable, adaptable, and technologically advanced interior finishes, meeting future demands of the industry.

U.S. Sustainable Interior Finishing Materials Market Analysis

Learn more about the key segments shaping this market

- Resilient flooring systems dominate the market, due to their durability, ease of maintenance, and affordability, high suitability for heavy-duty commercial spaces like offices, healthcare, and educational institutions. With diversified innovations such as bio-based and recycled-content eco-friendly resilient products, their prominence in sustainable projects increases ever more. The performance abilities of these resilient flooring systems and versatility pose a tendency to advance their high growth rate in the market.

- Increasingly, low-emitting chemical systems are adopted in all types of interiors with ever-growing stringent indoor air quality regulations and rising health awareness. Symptoms associated with VOC exposure are reduced in space safety for occupants, particularly in healthcare, hospitality, and residential applications. Growing use of these systems aligns with certifications such as Green Building to nurture developing manufacturers toward improved formulations.

- Aesthetic value, the beauty of carpets and textile systems, acoustical performance, and comfort lend credence to their use in commercial and institutional facilities. Thus, the growth rate of such systems is moderate in rising climates due to growing concerns of VOC emissions and access to alternative flooring opportunities.

- Hard surface flooring is preferred for areas requiring high hygiene or maintained aesthetics of design. Tile and stone are less flexible in their applications than resilient systems but are increasingly demanded for their long life span and ease of cleaning.

- Bio-based and rapid renewable materials appear as the most promising and now emerging eco-friendly alternatives, particularly because consumers prefer natural and biodegradable finishes.

- Recycled content composites are increasingly penetrating markets, reducing some of the vital waste and establishing circular economy practices. Their use in various applications is expanding.

Learn more about the key segments shaping this market

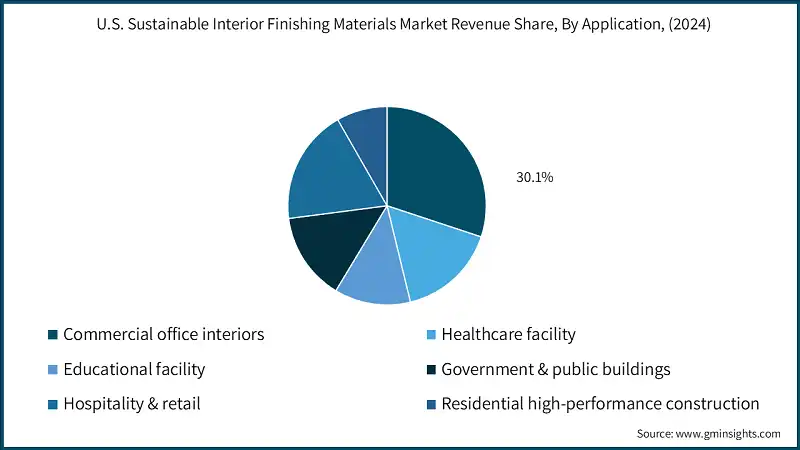

Based on application, the market is segmented into commercial office interiors, healthcare facility, educational facility, government & public buildings, hospitality & retail and residential high-performance construction. The commercial office interiors segment held around 30.1% of the market share in 2024.

- Commercial office interiors are the prime applications driving the market. Most of these spaces emphasize eco-friendly finishes that fit indoor air quality standards and support LEED certifications. Flooring resilient paints with low VOCs and those with recycled content-finish materials are most demanded here because companies prefer to spend a lot in durable, cost-effective, and very sustainable solutions that enhance their productivity and corporate image. With the additional scale of green projects in building construction and new sustainability commitments by the corporate sector, it is expanding this segment even further.

- Healthcare facilities are one of the most important able application segments owing to their necessity of being hygienic, low-emission, and anti-microbial finishes ensuring patient safety and meeting highly intense regulations.

- Educational facilities want to adopt sustainable interior to promote healthy learning environments and to meet green building standards. The argument for children and their health and responsibility for the environment fuels a demand for low-emitting, durable, and easy-to-maintain materials. Initiatives of sustainability within schools and universities are further inspiring innovations in eco-friendly, resilient, and recyclable finishes.

- They use sustainable materials in government and public buildings mostly to reduce costs, lessen their impact on the environment, and adhere to various regulations. High-performance, long-lasting finishes are often a requirement in such projects and are often specification requirements for LEED or WELL, which promote the use of recycled content and low-VOC products, allowing applications to remain steadily growing.

- Increasing uses of green finishes in the hospitality setting and retail environment are witnessed because most consumers prefer touching the finished products before making considered purchases. These applications promote innovative and attractive-sustainable materials that assist brands in building their green credentials.

- High-performance residential constructions are on the rise due to the increasing realization and concern of consumers over health and environmental issues. With changing consumer preferences, the growth of this new market segment in continuing demand for bio-based, recyclable and low-emission finishes is significant.

Looking for region specific data?

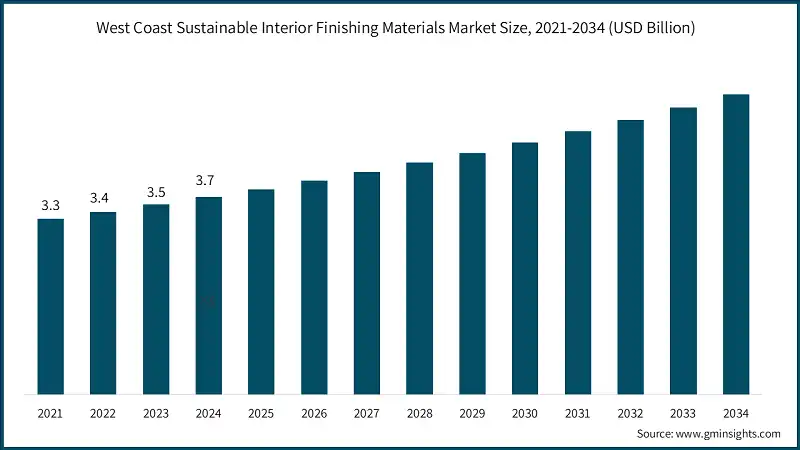

West Coast sustainable interior finishing materials market accounted for USD 3.7 billion in 2024.

- The West Coast is the standout region in the U.S. for sustainable interior finishing materials, owing to the strong green building focus of its constituents, the intensive adoption of eco-friendly products, and the many progressive architecture firms vying to push the standards of sustainability. Early regional adoption of LEED and WELL certifications has stimulated demand for innovative environmentally sustainable finishes in commercial, residential, and institutional projects alike. This heavy concentration of tech companies and environmentally conscious consumers in the region is accelerating the pace of adoption of high-performance sustainable materials, specifically in commercial office spaces, identified as the largest application segment.

- Economic growth is being experienced in the Southeast through urbanization and expansion of healthcare and educational infrastructure as well as policies at the state level that add to the demand for eco-friendly finishes and so much more. Also, with the rising population and economic development within the region, there exists increased construction activity across many sectors, mostly in hospitals and schools, which are significant contributors to the market.

- With inherently extensive green building activities mainly in commercial and government projects throughout the Northeast, the market is more mature. The focus on historic preservation and renovation of existing buildings promotes the sustainable use of durable finishes under more stringent standards.

- Growth in the Midwest market is driven by continuing industrial & commercial redevelopment, developing sustainable residential projects. Although slower than development on the West Coast, the Midwest has a distinct advantage in being able to work with cost-effective, durable, and locally sourced materials, thus supporting a steady regional growth for sustainable finishes.

- The Southwest plays host to growing commercial developments and eco-conscious residential projects into the marketplace. Favorable climate and the rise of energy-efficient, sustainable building practices raise demand for high-performance environmentally friendly interior finishes, most especially in urban centers like Phoenix and Dallas.

U.S. Sustainable Interior Finishing Materials Market Share

- Armstrong World Industries, BASF, Mannington Commercial, 3M, Benjamin Moore & Co. accounts 32.4% of the market share.

- The sustainable interior finishing materials market consists of such leading companies, operating mostly in their regional areas. Their long years of experience with finishing interior materials allow these companies to maintain a strong market position worldwide. Their product offerings are diverse and majorly supported by production capacities and distribution networks, which can serve the increasing demand for sustainable interior finishing materials in various regions.

U.S. Sustainable Interior Finishing Materials Market Companies

Major players operating in the sustainable interior finishing materials industry are:

- 3M

- ARCAT

- Armstrong World Industries

- BASF

- Benjamin Moore & Co.

- Chaparral Materials

- Emnett Interiors

- Mannington Commercial

- RASTRA INC

- Rimex Metals Group

Armstrong World Industries: Armstrong World Industries specializes in creating ceilings and walls that are inherently and inherently sustainable, alongside eco-friendly, low-VOC finishes. It is an investment in innovation for developing durable, recyclable and environmentally responsible interior materials that live by the green building specifications such as the LEED so as also to cater for commercial and residential projects with long-lasting options that are concerned with health.

BASF: The major strength of BASF are their portfolio of sustainable coatings, adhesives and construction chemicals. The focus at BASF is on producing low emissions, bio-based, recyclable material that effectively improves indoor air quality as well as durability. BASF endeavors with all its might to bring forth innovative formulation technologies matching green building certification so as to extend its reach in eco-friendly interior finishes.

Mannington Commercial: Mannington Commercial resilient flooring creates a crutch on sustainability: It includes products containing recycled materials, low-emission and bio-based materials that have been designed for extreme durability and dramatic aesthetic performance. Mannington, molded from the figure of mind of environmental responsibility, endeavors beyond the manufacture-standardized demands of green building on its products.

3M: 3M manufactures a range of sustainable adhesives, tapes and surface protection solutions. Their products are formulated to minimize VOC emissions and incorporate recycled content, hence providing healthier indoor environments. 3M invests in the research and development of eco-friendly innovations that conform to strict environmental standards for use above interior applications.

Benjamin Moore & Co: Benjamin Moore brings out its low- and no-VOC developed paints and coatings for green interiors and high-quality yet environmentally friendly finishes which will improve indoor air quality and qualify for green certifications. The firm affirms the continuous innovative spirit in developing eco-conscious formulations..

U.S. Sustainable Interior Finishing Materials Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 12 Billion |

| Market Size in 2025 | USD 12.4 Billion |

| Forecast Period 2025 - 2034 CAGR | 3.9% |

| Market Size in 2034 | USD 17.6 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Federal procurement mandates & GSA specifications | Drive increased demand for sustainable materials in government projects, promoting market expansion |

| LEED certification requirements & green building adoption | Encourage builders and developers to choose eco-friendly interior finishes that meet certification standards, thereby boosting market growth |

| Indoor air quality regulations & health consciousness | Promote the adoption of low-emission, non-toxic interior materials to improve indoor environments, supporting market development |

| Pitfalls & Challenges | Impact |

| Higher initial cost premiums & ROI challenges | May deter adoption by customers and slow market penetration due to concerns over long-term financial benefits |

| Limited manufacturing capacity for bio-based materials | Restricts supply availability, increases production costs, and hampers the scalability of sustainable solutions |

| Opportunities: | Impact |

| Carbon-negative product development potential | Enables companies to differentiate and meet sustainability goals, opening new market segments |

| Circular economy integration & take-back programs | Promote resource efficiency and create new business models within the industry |

| Market Leaders (2024) | |

| Market Leaders |

7.9% market share |

| Top Players |

Collective market share in 2024 is 32.4% |

| Competitive Edge |

|

| Future outlook |

|

What are the growth opportunities in this market?

U.S. Sustainable Interior Finishing Materials Industry News

- September 2025, Perfect Finish Painting had expanded its already established services in interior painting spaces in Littleton, CO. One of the products introduced at that time was a professional cabinet and interior painting service coming from oil-finished houses in styles extending durability and fashion.

- April 2024, Armstrong World Industries announced ULTIMA Low Embodied Carbon ceiling panels that contain embodied carbon at a 43% lower rate than normal ceiling material. Not only that; they are allowed to borrow biobased materials from USDA to achieve the ultimate finish in place of finishing products and biological materials.

This U.S. sustainable interior finishing materials market research report includes an in-depth coverage of the industry with estimates and forecast in terms of revenue in USD Billion and volume in terms of Kilo Tons from 2021-2034 for the following segments:

Market, By Product Technology Type

- Low-emitting chemical systems

- Water-based paints & coatings

- VOC-compliant adhesives & sealants

- Bio-based additive

- Resilient flooring systems

- Luxury vinyl tile (LVT)

- Sheet vinyl & heterogeneous systems

- Rubber flooring

- PVC-free alternative technologies

- Carpet & textile systems

- Recycled content fiber

- Bio-based backing systems & carbon storage

- Hard surface flooring

- FSC-certified wood flooring

- Waterproof engineered wood

- Ceramic tile with recycled content integration

- Bio-based & rapidly renewable materials

- Bamboo flooring

- Cork & linoleum system

- Pla-based flooring

- Recycled content composites

Market, By Application

- Commercial office interiors

- Healthcare facility

- Educational facility

- Government & public buildings

- Hospitality & retail

- Residential high-performance construction

The above information is provided for the following regions:

- Northeast

- West Coast

- Southeast

- Midwest

- Southwest

Frequently Asked Question(FAQ) :

What is the market size of the U.S. sustainable interior finishing materials in 2024?

The market size was USD 12 billion in 2024, with a CAGR of 3.9% expected through 2034 driven by demand for low-emission, non-toxic materials that enhance indoor environments.

What is the projected value of the U.S. sustainable interior finishing materials market by 2034?

The U.S. sustainable interior finishing materials market is expected to reach USD 17.6 billion by 2034, propelled by green building standards, LEED certifications, and rising demand for healthier indoor environments.

What is the current U.S. sustainable interior finishing materials market size in 2025?

The market size is projected to reach USD 12.4 billion in 2025.

How much revenue did the resilient flooring systems segment generate in 2024?

Resilient flooring systems generated USD 2.8 billion in 2024, dominating the market due to their durability, ease of maintenance, and affordability.

What was the market share of commercial office interiors segment in 2024?

Commercial office interiors held around 30.1% market share in 2024, representing the prime application segment driving the market.

Which region leads the U.S. sustainable interior finishing materials market?

The West Coast held the leading position with USD 3.7 billion in 2024, fueled by strong green building focus, intensive adoption of eco-friendly products, and progressive architecture firms pushing sustainability standards.

What are the upcoming trends in the U.S. sustainable interior finishing materials market?

Key trends are low-VOC materials, recycled and bio-based content for circular economy, and advanced coatings or smart surfaces with self-cleaning or air-purifying functions.

Who are the key players in the U.S. sustainable interior finishing materials market?

Key players include 3M, ARCAT, Armstrong World Industries, BASF, Benjamin Moore & Co., Chaparral Materials, Emnett Interiors, Mannington Commercial, RASTRA INC, and Rimex Metals Group.

U.S. Sustainable Interior Finishing Materials Market Scope

Related Reports