Summary

Table of Content

Industrial Gas Turbine Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Industrial Gas Turbine Market Size

The rise of emphasis on low-emission technologies in line with the heightened environmental regulation will improve the situation in the industry. Additionally, the digital monitoring solutions and predictive maintenance that are to be incorporated increase the reliability of the system, and they will lead to the development of the business scenario.

Industrial Gas Turbine Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 9.3 Billion

- 2026 Market Size: USD 10.5 Billion

- 2035 Forecast Market Size: USD 27.5 Billion

- CAGR (2026–2035): 11.3%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: Middle East & Africa

Key Market Drivers

- Implementation of government norms to reduce carbon emissions.

- Growing focus on decentralized generation technologies.

- Positive outlook toward gas-based power generation.

Challenges

- Cost competitiveness.

Opportunity

- Industrial process electrification.

- Expansion of cogeneration systems.

- Modernization of aging industrial infrastructure.

- Growth in industrial automation and high‑load facilities.

Key Players

- Market Leader: GE Vernova led with over 12.5% market share in 2025.

- Leading Players: Top 5 players in this market include Siemens Energy, Baker Hughes, GE Vernova, Mitsubishi Heavy Industries, Rolls-Royce, which collectively held a market share of 46% in 2025.

Get Market Insights & Growth OpportunitiesAn industrial gas turbine refers to a high-power generation facility that is used extensively in the industries to provide high-performance output in the form of either mechanical or electrical output. It works on the Brayton cycle, which mixes compressed air and fuel to generate high efficiency rotational energy.

The industry potential is going to proliferate as the combined cycle power plants are adopted even more in accordance with the increasing energy-efficiency requirements and sustainability ambitions. These turbines offer features as good fuel flexibility, sophisticated control system, low emissions and high reliability in operations which in turn will increase adoption of the product.

The growing renewable energy penetration is creating a demand to have large amounts of power that can be rapidly introduced, thus the need to have more gas turbines capable of providing reliable & dispatchable power at the time of solar and wind variability is growing. Furthermore, current coal plant retirements and the presence of brownfield grid interconnections will foster the business environment.

For instance, in 2025, the Federal Electricity Commission (CFE) of Mexico announced a multibillion-dollar investment agenda in its 2025-2030 power generation growth plan. The strategy will see the construction of 12 new power stations, which will contribute about 5,840 MW of power. A major part of this growth revolves around the new combined-cycle gas turbine plants aimed at mitigating emissions and improving the stability of domestic energy delivery.

The industrial gas turbine market was valued at USD 6.3 billion in 2022 and grew at a CAGR of approximately 6% through 2025. The continuous improvement of stream-lined and modular designs of turbine construction in parallel with increased operational flexibility would increase the business momentum.

The trend of growing pace of electrification of transport and heating and growing peak-load volatility is likely to motivate intensified acquisition of flex-fuel gas turbine fleets to provide reliable, multi-hour firm capacity. The business dynamics will be further fueled by the rapid expansion of the data-centers and the building up congestion of the urban grids.

The expansion of hydrogen-preparedness alongside the more evident policy pathways in the direction of low-carbon hydrogen is poised to enhance the uptake of next-generation portfolios of turbines. Moreover, the continued demonstration projects of 100 percent hydrogen and hydrogen-blend operation together with the OEM burner upgrade programs will improve the business prospect.

For instance, in 2024, Canada pledged about USD 360 million in its Smart Renewables and Electrification Pathways initiative in 2024, adding USD 3 billion to the overall budget of the project. This investment is to improve the clean-energy infrastructure and structures, unleash more activities of the private sector and help it in the overall goal of reaching net-zero emissions.

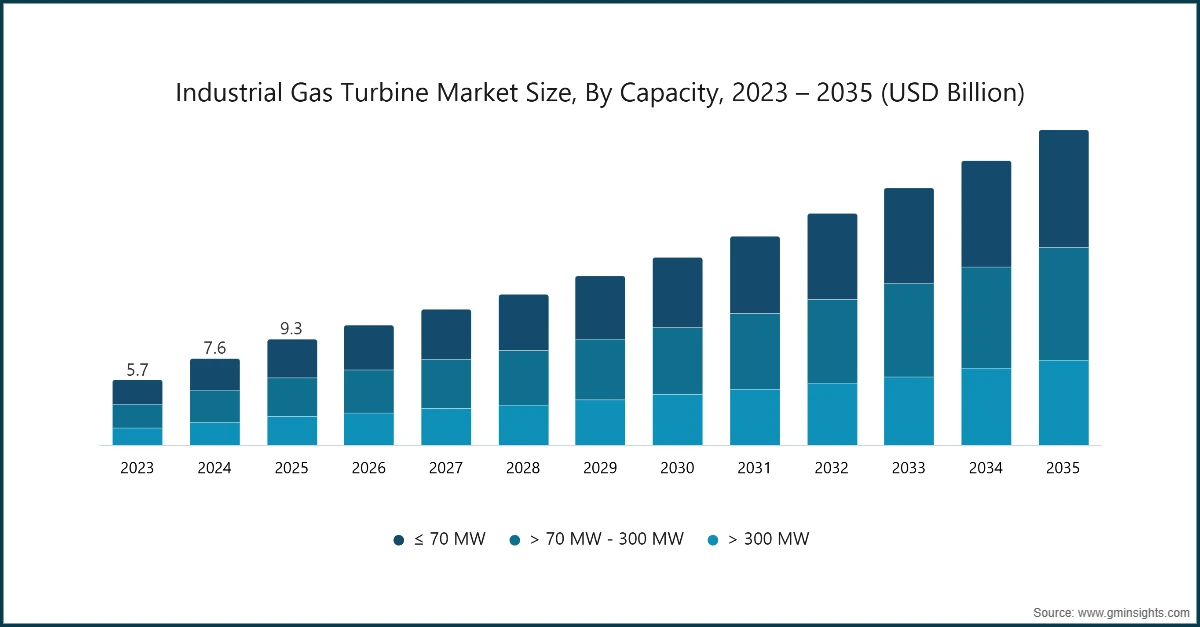

The industrial gas turbine market was estimated at USD 9.3 billion in 2025. The market is expected to grow from USD 10.5 billion in 2026 to USD 27.5 billion by 2035, at a CAGR of 11.3%, according to a recent study by Global Market Insights Inc.

To get key market trends

Industrial Gas Turbine Market Trends

Strict emissions control and carbon-cutting pledges are driving end-users to move off inefficient high-carbon technologies to more efficient turbine systems. Furthermore, the increased use of digitalization and smart turbine monitoring platforms will enhance the movement in the general direction of the industry.

Increasing attention to energy efficiency in both the industrial and utility-scale power systems is producing greater demand for such units. The willpower to waste less of the energy, minimize the waste heat, and lower the operating expenses will further stimulate the industry outlook as industries are moving toward deploying cogeneration and CHP solutions in order to maximize the usage of energy.

The implementation of predictive maintenance, digital twin, and outcome-based service contracts will increase the lifecycle availability, lessen the non-planned downtimes, and enhance the general project bankability. Moreover, stricter dry-low-NOx combustion standards and progressively more severe domestic air-quality standards will enhance the industry trend.

For citation, in March 2025, Partners Group had agreed to purchase a 1.9 GW portfolio of 11 natural gas-fired power plants in California, in addition to current operator, Middle River Power. It also has a portfolio consisting of two combined-cycle facilities and has a valuation of about USD2.2 billion.

Expanding traction towards decentralized power production which is backed by fast improvements in components, design and engineering will result in wider usage. The fact that they can be configured into modules and do not need to be connected to large grid structures is an added benefit to their value propositions, especially in areas where constant and uninterrupted power is needed.

Increased localized power generation of electricity particularly in remote industrial regions and areas with poor grid infrastructure will spur the use of these gas turbines. The increased transition to microgrids and distributed energy systems will continue to improve the industry environment.

The advantages of decentralized power solutions are minimization of transmission losses, increased operational freedom in industrial facilities and increased efficiency and energy autonomy. Improving pressure on quick-start, high-performance generation in cities and off-the-grid environments further supports the business dynamic strategic value of such units as a dependable element and increase in business conditions.

For illustration, in March 2025, GE Vernova introduced AGP XPAND, the next generation of its long-established technology Advanced Gas Path. It is intended to provide significant gains in turbine output and efficiency and can be described as a strategic development of power-generation solutions further optimization alongside the company’s further determination to innovate in their field.

Natural gas is getting a lot of recognition as a strategic transition fuel in the global decarbonization programs which are in turn facilitating growth in the industrial sector. The availability of LNG is increasing, and gas infrastructure continues to be improved, making it very viable and appealing to do more projects on gas-powered generation across the world.

Combining the rapid pace of increasing the world power requirement with the strategic withdrawal of coal-fired plants, is promoting the adoption of high-tech gas turbine technologies that are expected to be a cleaner and much more efficient choice. These turbines comply well with the environmental pledges made by both the developed and developing economies as they have considerably reduced emissions when compared to coal and oil generated power.

These collaborative efforts between turbine manufacturers, energy companies, and technology companies are leading to rapid improvements in the design and operational performance of turbines. These alliances focus on the unification of advanced materials, advanced digital tracking systems and hybrid designs that integrate these units and renewable energy sources together with each other.

Industrial Gas Turbine Market Analysis

Learn more about the key segments shaping this market

Based on capacity, the industrial gas turbine market is segmented into ≤ 70 MW, > 70 MW - 300 MW, and > 300 MW. The ≤ 70 MW segment holds a share of around 30% in 2025, fueled by strengthened governmental initiatives aimed at addressing increasing energy needs and advancing sustainability objectives.

The deployment of ≤ 70 MW units is rising owing to stronger interest in distributed generation models across industries that require flexible power outputs. Companies in manufacturing, remote mining operations, and small utilities prefer this capacity band due to it offers easier permitting, shorter construction cycles, and lower upfront investment.

The > 70 MW - 300 MW segment was valued at USD 3.4 billion in 2025. The business environment will be enhanced by increasing demand by the medium-sized utilities operating between large baseload plants and smaller distributed systems. The increasing demand and need to utilize the units that provide flexible grid support, as well as effective control in the intermediate and peak loads, will also contribute to the further use of products.

For instance, in 2024, the U.S. Environmental Protection Agency (EPA) adopted new emission control regulations of gas-fired combustion turbine, and new performance standards of the assets were introduced. The updated regulations will allow the operators of power plants to better plan and implement superior carbon-dioxide emission reduction systems, reinforcing compliance and long-term decarbonization targets.

The > 300 MW segment will witness a CAGR of over 11% by 2035. The high rate of implementation of large-scale utility projects both in developed and developing economies to assure them of long-term energy supply and incorporation of these projects in the national grid to improve stability and sustain growing populations will greatly improve the business opportunity.

Technological development owing to the high efficiency turbine, enhanced heat rates and advanced emission-control systems have remained to influence the new development of projects. These are innovations that are beneficial to economic competences and improve conformity with more stringent sustainability and environmental standards.

For citation, in 2024, the Canadian government proposed regulations aimed at reducing emissions in the oil and gas sector by 35% by 2030 to become one of the key steps in speeding up the process of decarbonization of one of the most intensive industries of the country. The proposed framework is going to be formally consulted until January 2025, which serves as an indication of its long-term dedication to environmental sustainability and enhanced regulatory supervision.

Learn more about the key segments shaping this market

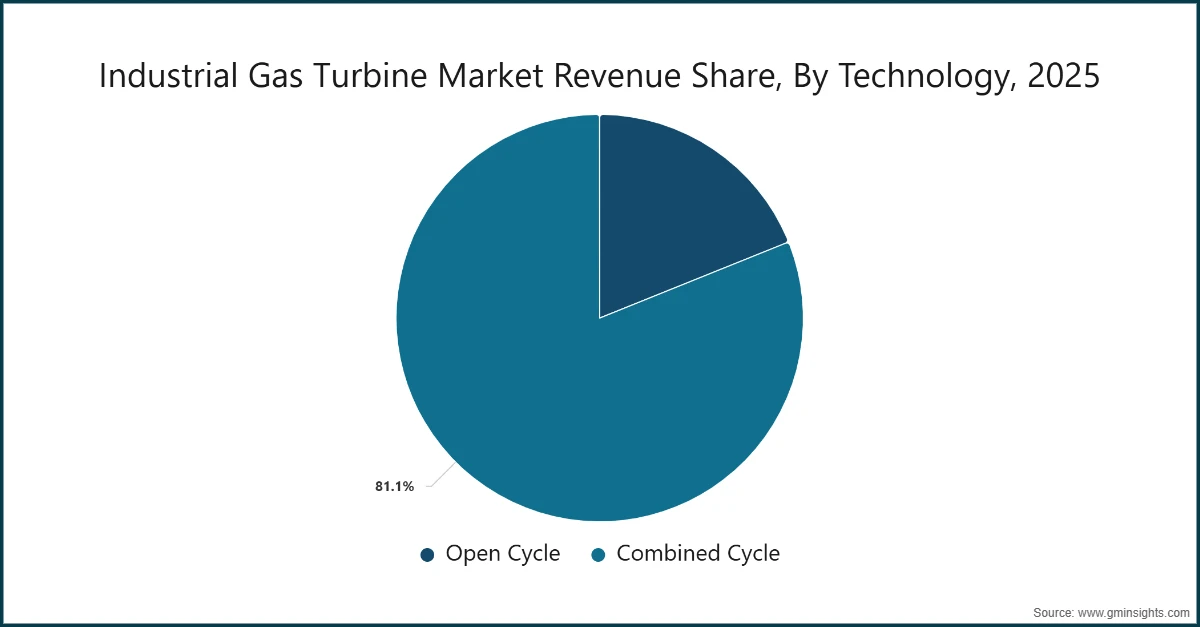

Based on technology, the industrial gas turbine market is divided into open cycle and combined cycle. The combined cyclesegment holds a share of 81.1% in 2025 and is set to surpass USD 21 billion by 2035. The emerging trend of additive manufacturing in conjunction with improved prototyping will present new business opportunities across the industry.

The decarbonization trend in the world and substitution of coal-generating facilities with cleaner generation technologies has increased the adoption of these units. Besides, the fact that they will work effectively with renewable energy systems will intensify the business curve.

The open cycle technology segment will witness a CAGR of over 11.5% by 2035. The increasing interest in grid security, backed by the increasing needs of distributed power solutions in industrial operation will facilitate growth in the businesses. Moreover, constant advancement of turbine engineering, as well as, the efforts of the company to enhance fuel efficiency and adhere to stringent emittance standards will enhance the product perspective.

The simple structure of open-cycle of gas turbines and their mobility make them perfect in use in remote industrial areas, mining enterprises, and remote settlements. These are the places that usually lack effective connectivity to centralized grid facilities, and they necessitate the need to have their own power generation facilities.

For illustration, Mexico introduced a USD 23 billion program to upgrade the electric power industry in 2024. The plan is to focus on enhancing the power of the Federal Electricity Commission and increasing the infrastructure that is already privately operated. Among the priority areas are to increase energy access, enhance grid reliability, and encourage specific investment in the involvement of the private sector to strengthen the energy ecosystem of the country as a whole.

Looking for region specific data?

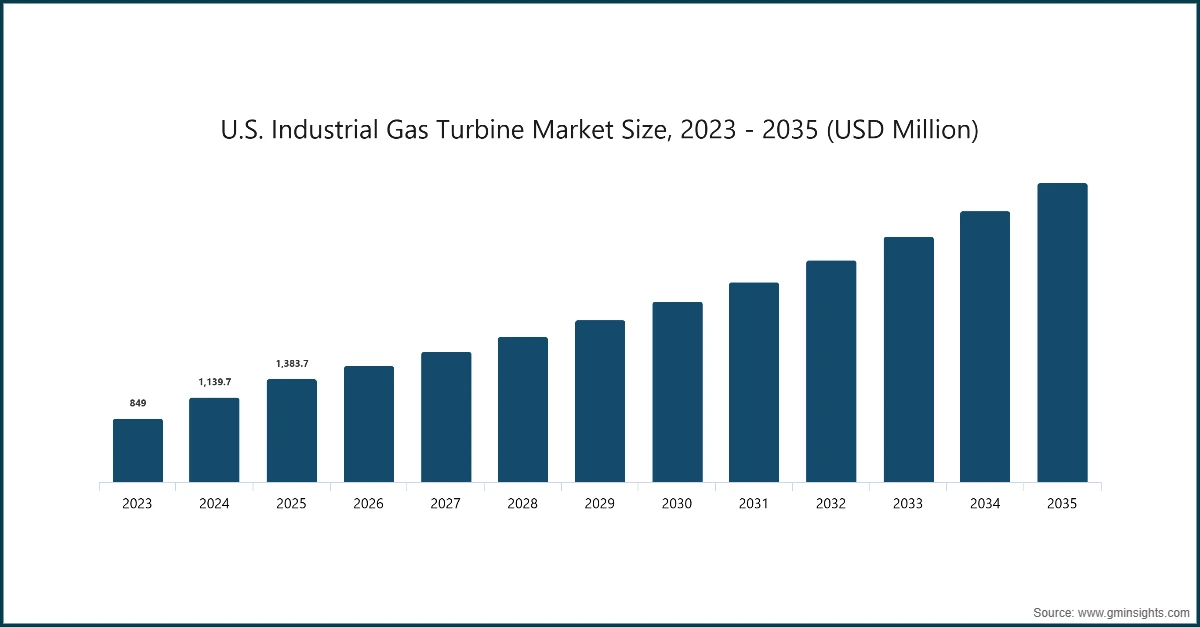

The U.S. dominated the industrial gas turbine market in North America with around 70% share in 2025 and generated USD 1,383.7 million in revenue. Increasing grid stability concerns are causing utilities to consider such systems in order to operate on rapid-response basis so that variable renewable contributions can be smoothly balanced out.

The North America region is projected to surge over USD 4.5 billion by 2035. The retirement of old coal power plants to new gas-fired plants is speeding up, particularly in the areas where strict decarbonization policies are implemented. This has been accompanied by the growing adoption of such turbines to generate power on distributed basis in oil and gas, power plants and super large industrial facilities.

For instance, the USD 7 billion investment that was announced by the U.S. government in September 2024 to expedite the adoption of clean-energy in 16 rural electric cooperatives. Being one of the major federal commitments to date, the initiative is focused on rural electrification through the incorporation of varied portfolio of solar, wind, hydro, and nuclear energy technology.

The Europe industrial gas turbine industry is set to grow at a rate of over 9% by 2035. The dedication to the reduction of carbon emissions and the shift to cleaner energy within the region are driving the rapid market expansion. Efficiency in the turbines is increasing because of tough regulation policies and the attempt to eliminate coal and reduce reliance on the traditional sources of fuels.

Asia Pacific industrial gas turbine industry holds a share of 35% in 2025. The high pace in industrialization is increasing the need for mid capacity turbines in manufacturing and petrochemical sectors. Increased demand in the use of dual fuel turbine systems which have increased operational flexibility with changes in fuel supply is also helping in product adoption.

For instance, in 2024, the Future Made in Australia policy as introduced in 2024, across Australia which would open up the vast resource base of the nation to speed up the clean-energy transition. The project is an indication of a strategic move to use the conventional fossil-fuel resources so that new industry can be created.

Economic diversification, which is on the rise, as well as increased industrial activities are increasing the need to have reliable and flexible power system in the Middle East & Africa. The adoption of the next-generation turbines with better performance and higher emissions-control capabilities is also influenced by the increased interest in energy-efficient and low-emission solutions.

The Latin America region will experience robust growth backed by the robust growth in the investment in the infrastructure of gas and the development of power generation projects. The positive governmental measures towards less dependence on imported fuel and the existence of sufficient natural gas reserves will increase the prospects of the business even more.

For illustration, in 2024, Brazil set the National Policy on the Energy Transition whereby it plans to spend USD 400 billion in green investments in the upcoming decade. This historic program brings together government activities to stimulate the use of clean energy, enhance Brazil in the international renewable-energy system and spearhead the development of low-carbon industry.

Industrial Gas Turbine Market Share

The top 5 players in gas turbine market are Siemens Energy, Baker Hughes, GE Vernova, Mitsubishi Heavy Industries, and Rolls Royce contribute around 46% of the market share in 2025.

The market is changing very fast, with the increasing demand for good efficient and reliable sources of power in the manufacturing, oil & gas industry, and heavy industrial industry. The competitive nature in the industry is intense, with major players in the industry moving the turbine aerodynamics, fuel flexible combustion system and digital performance to enhance up time and operational performance.

Siemens Energy delivers energy technologies that are designed to be highly efficient and with low emissions as well as high operational flexibility. The company focuses on hydrogen-prepared designs, streamlined aerodynamics, and 21st century materials to maximize fluid flexibility and execution. Digital solutions, such as real-time monitoring and AI-based optimization, also assist industrial customers in achieving decarbonization and reliability.

Baker Hughes integrated turbine offerings that are aimed at providing efficiency, durability and fuel flexibility in challenging industrial conditions. Its NovaLT and Frame lines of turbines have low-emission capabilities that are backed by digital diagnostics and predictive maintenance platforms. The business aims at facilitating reliable on-site power generation as well as assisting operators to minimize operational expenses and environmental impact.

GE Vernova offers high efficiency gas turbines designed to be used in hybrid, renewable integrated, and distributed power services. Its portfolio includes sophisticated combustion systems, digital twin technologies, and IoT-driven analytics that make it more reliable and agile in its operations. GE Vernova focuses on the flexible, lower-carbon solutions that can be used by industrial customers to go through the global energy transition.

Mitsubishi Heavy Industries provide a powerful portfolio of turbines that are developed to perform with the best performance and offer fuel flexibility along with high reliability. The company has embraced modern cooling systems, low-NOx based combustion systems and hydrogen ready platforms throughout its turbines. MHI also focuses on lifecycle support, modernization programs and efficiency-enhancement services in order to create maximum value to industrial operators.

Rolls‑Royce is a manufacturer of industrial gas turbines that produce resilience and high efficiency of power in industries like offshore, manufacturing and process industries. Its aero-type derivatives turbine technologies have quick start-up capability, high power-to-weight ratios and great flexibility in fuel consumption. Rolls-Royce supports its hardware with the provision of digital asset management and long-term service solutions in order to achieve the optimization of the performance and the reduction of emissions.

Industrial Gas Turbine Market Companies

Siemens Energy has an annual report of USD 12.1 billion of revenues in the fiscal year 2025 due to its large operations throughout the global energy industry. The net profit of the company is USD 380 million, which is a good performance in terms of cost discipline and operating efficiency. These findings highlight the fact that it is capable of ensuring profitability and providing consistent performance despite changes in market dynamics.

GE Vernova reported revenues of about USD 27.1 billion for the first nine months of 2025. The power segment added USD 14 billion, the Wind segment added USD 6.7 billion and the Electrification segment added USD 6.8 billion in this period. This dispersion highlights the size and diversification of its operations in business units.

Mitsubishi Heavy Industries announced first half year 2025 revenues of USD 13.6 billion and net profits of USD 750 million which indicates the financial positivity of the company in this period. These numbers demonstrate the size of the company activity and its profitability during the reporting period.

Major players operating in the industrial gas turbine industry are:

Ansaldo Energia

Auxitrol Weston

Baker Hughes

Bharat Heavy Electricals

Destinus Energy

Doncasters Group

Doosan Enerbility

Everllence

Flex Energy Solutions

FUJI INDUSTRIES

GE Vernova

IHI Corporation

Kawasaki Heavy Industries

Mitsubishi Heavy Industries

MTU Aero Engines

Rolls Royce

Siemens Energy

Solar Turbines

VERICOR

Wärtsilä

Industrial Gas Turbine Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 9.3 Billion |

| Market Size in 2026 | USD 10.5 Billion |

| Forecast Period 2026-2035 CAGR | 11.3% |

| Market Size in 2035 | USD 27.5 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Implementation of government norms to reduce carbon emissions | The shift toward cleaner energy is driving faster adoption of gas turbines as industries and utilities move away from coal‑based generation. Rising environmental pressures and efficiency requirements further reinforce the transition to gas‑fired technologies. |

| Growing focus on decentralized generation technologies | Deployment of small‑scale aeroderivative turbines is increasing rapidly to support the growth of distributed energy systems. Their high efficiency, modularity, and fast‑start capability make them ideal for decentralized industrial and commercial applications. |

| Positive outlook toward gas-based power generation | Investment in new combined‑cycle and open‑cycle gas turbine projects continues to strengthen, driven by the need for efficient and flexible power generation. These projects are gaining momentum as utilities and industries prioritize reliable, lower‑emission energy systems. |

| Pitfalls & Challenges | Impact |

| Cost competitiveness | Adoption remains limited in cost‑sensitive regions, where gas turbines face competition from lower‑priced renewable and conventional power solutions. The budget constraints and affordability concerns continue to influence technology choices. |

| Opportunities: | Impact |

| Industrial process electrification | Growing electrification of manufacturing and process industries is increasing demand for reliable on‑site power, creating opportunities for industrial gas turbines. Their ability to deliver stable, high‑output energy supports continuous operations in sectors where downtime is costly. |

| Expansion of cogeneration systems | The push for higher energy efficiency is driving adoption of cogeneration systems, where industrial gas turbines simultaneously produce electricity and useful heat. This dual‑output capability helps operators reduce energy costs and improve overall thermal efficiency. |

| Modernization of aging industrial infrastructure | A large base of aging industrial power assets is creating strong potential for turbine upgrades and replacements. New‑generation industrial gas turbines offer enhanced durability, lower emissions, and improved heat‑rate performance, encouraging modernization investments. |

| Growth in industrial automation and high‑load facilities | The rise of energy‑intensive automated manufacturing, data‑heavy industrial operations, and advanced processing facilities is increasing the need for dependable on‑site power sources. Industrial gas turbines provide the high‑load support and operational stability required for these environments. |

| Market Leaders (2025) | |

| Market Leader |

Market Share of 12.5% |

| Top Players |

Collective Market Share of 46% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest growing market | Middle East & Africa |

| Emerging countries | U.S., China, India, Saudi Arabia, UAE |

| Future outlook |

|

What are the growth opportunities in this market?

Industrial Gas Turbine Industry News

In July 2025, GE Vernova signed a major contract with Crusoe, the first fully integrated AI infrastructure developer, to install 29 LM2500XPRESS gas turbine aeroderivative units in the form of LM2500XPRESS. The rapidly growing network of AI data centers will be driven by these turbines to serve Crusoe. The transaction highlights the criticality of GE Vernova in providing scalable low-carbon energy solutions to the high-need digital infrastructure in the rapidly growing AI industry.

In June 2025, IHI Corporation along with GE reported the conclusion of the next-generation large-scale combustion trials plant in Hyogo Prefecture. The plant will be constructed with the aim of developing and testing the latest combustion technologies, with a key target on ammonia, a hydrogen-based, carbon-free fuel. By taking advantage of ammonia in gas turbines, it is possible to achieve zero-net-CO2 generation, thus helping to decarbonize the world and strengthening the shift to cleaner, future-oriented energy products.

In May 2025, Baker Hughes won a big contract with Frontier Infrastructure to provide 16 Nova LT gas turbines to support the new data center projects in both Texas and Wyoming. The turbines will supply up to 270 MW of high-performance and reliable power to frontier to the energy infrastructure behind the meter. In the deal, Baker Hughes will supply its new NovaLT turbine technology and other related systems, such as gear solutions and Brush Power Generation four-pole generators.

In March 2025, Siemens Energy secured contract valued USD 1.6billion with HE in March of 2025 to provide gas turbines and related technology to the Nairyah 2 and Rumah 2 combined gas-fired power stations in Saudi Arabia. The new capacity of 3.6 GW to the national grid brought by the project will have the capacity to serve about 1.5million residences and, to guarantee long-term full operational performance, the project will have a 25-year long-term service agreement.

The industrial gas turbine market research report includes in-depth coverage of the industry with estimates & forecast in terms of revenue (USD Million) & volume (MW) from 2022 to 2035, for the following segments:

Market, By Capacity

≤ 70 MW

> 70 MW - 300 MW

> 300 MW

Market, By Product

Aero-derivative

Heavy duty

Market, By Technology

Open cycle

Combined cycle

Market, By Application

Power generation

Oil & gas

Other manufacturing

The above information has been provided for the following regions and countries:

North America

U.S.

Canada

Mexico

Europe

UK

France

Germany

Russia

Italy

Netherlands

Poland

Asia Pacific

China

Australia

Japan

India

South Korea

Indonesia

Thailand

Malaysia

Middle East & Africa

Saudi Arabia

UAE

Qatar

Kuwait

Oman

Egypt

Turkey

Bahrain

Iraq

South Africa

Latin America

Brazil

Argentina

Peru

Chile

Frequently Asked Question(FAQ) :

What is the market size of the industrial gas turbine in 2024?

The market size was USD 7.3 billion in 2024, with a CAGR of 5.1% expected through 2034 driven by renewable energy integration, coal retirements, and flexible power generation needs.

What is the expected size of the industrial gas turbine market in 2025?

The market is expected to reach USD 7.8 billion in 2025.

What is the projected value of the industrial gas turbine market by 2034?

The industrial gas turbine market is expected to reach USD 12.2 billion by 2034, propelled by hydrogen-readiness, electrification trends, and data center proliferation requiring reliable power.

How much revenue did the ≤ 70 MW capacity segment generate in 2024?

The ≤ 70 MW segment held 38.6% market share in 2024, fueled by distributed power generation and localized demand for industries and communities.

What was the valuation of the combined cycle technology segment in 2024?

Combined cycle technology dominated with 82.5% market share in 2024, favored for its high efficiency and ability to meet decarbonization goals as an alternative to coal.

What is the growth outlook for aero-derivative turbines from 2025 to 2034?

Aero-derivative turbines are projected to grow at over 5% CAGR through 2034, due to their lightweight design, higher efficiency, and flexibility for renewable energy integration.

Which region leads the industrial gas turbine market?

Asia Pacific held 32.5% share in 2024, with rapid industrialization driving demand for mid-capacity turbines in manufacturing and petrochemical sectors across the region.

What are the upcoming trends in the industrial gas turbine market?

Key trends include hydrogen-ready turbines, digitalization with predictive maintenance, multi-fuel capabilities, and integration with renewable energy systems for grid stability.

Who are the key players in the industrial gas turbine market?

Key players include Ansaldo Energia, Baker Hughes, Bharat Heavy Electricals, Capstone Green Energy, Destinus Energy, Doosan, Flex Energy Solutions, GE Vernova, Harbin Electric, IHI Corporation, JSC United Engine, Kawasaki Heavy Industries, MAN Energy Solutions, Mitsubishi Heavy Industries, MTU Aero Engines, Nanjing Turbine and Electric Machinery, Rolls Royce, Siemens Energy, Solar Turbines, Vericor, Wärtsilä

Industrial Gas Turbine Market Scope

Related Reports