Summary

Table of Content

Chiplet Interconnect Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Chiplet Interconnect Market Size

The global chiplet interconnect market was valued at USD 2.17 billion in 2025. The market is expected to grow from USD 2.89 billion in 2026 to USD 12.42 billion in 2031 and USD 41.2 billion in 2035, at a CAGR of 34.4% during the forecast period, according to the latest report published by Global Market Insights Inc.

Chiplet Interconnect Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 2.17 Billion

- 2026 Market Size: USD 2.89 Billion

- 2035 Forecast Market Size: USD 41.2 Billion

- CAGR (2026–2035): 34.4%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: Asia Pacific

Key Market Drivers

- Heterogeneous Integration Demand.

- Advanced Node Cost Optimization.

- AI and HPC Workload Scaling.

- Yield Improvement and Design Flexibility.

- Ecosystem Standardization and Open Interconnects.

Challenges

- Lack of Universal Interoperability.

- Thermal and Power Management Constraints.

Opportunity

- Expansion of AI and HPC-Optimized Chiplet Solutions.

- Development of Open-Standard Interconnect Ecosystems.

Key Players

- Market Leader: Intel Corporation led with over 18.2% market share in 2025.

- Leading Players: Top 5 players in this market include Intel Corporation, Advanced Micro Devices (AMD), NVIDIA Corporation, Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, which collectively held a market share of 56.3% in 2025.

Get Market Insights & Growth Opportunities

The global chiplet interconnect market is expanding, owing to heterogeneous integration demand, advanced node cost optimization, AI and HPC workload scaling, yield improvement and design flexibility, ecosystem standardization and open interconnects.

Heterogeneous integration, where the chiplets, memory, and special IP are packaged together, is a key driver of growth, addressing the shortcomings of traditional scaling, and is capable of modular optimization of performance across applications with edge devices to data centers. Government programs in the industrial sector are gradually moving towards advanced packaging and heterogeneous integration as a strategy to drive innovation, reduce monolithic chip reliance and speed up the time-to-market of complex computing systems. For instance, the European Chips Act initiated in December 2024 the pilot line, Advanced Packaging and Heterogeneous Integration for Electronic Components and Systems (APECS), to facilitate research and development and commercialization of heterogeneous chiplet technologies in Europe.

AI and HPC applications require a high level of computational performance, a high bandwidth and low latency. These needs are motivating the use of chiplet architectures that have enhanced interconnects, since monolithic chips in isolation are not able to scale either economically or physically to satisfy these needs. This strategic need is being recognized by governments and industry associations, who are investing in efforts to ensure scalable silicon diversity and modular architecture. For instance, the Open Compute Project Foundation announced a universal link-layer specification oriented to UCIe in August 2025. This project will address silicon diversity and support reconfigurable AI/HPC clusters, showing how the standards of chiplet interconnect play an important role in the scalability of the next-generation computing workloads.

Chiplet interconnects are high-speed, low-latency communication interfaces which allow multiple semiconductor chiplets to be used as a single system in a single package. These interconnects facilitate data transfer, power transmission, and synchronization between heterogeneous and heterogeneous components, i.e. CPUs, GPUs, accelerators and memory. Chiplet interconnects have higher scalability, yield, cost-effectiveness, and performance than traditional monolithic integrated circuits by providing modular design.

To get key market trends

Chiplet Interconnect Market Trends

- Standardized open die to die interconnects are revolutionizing the chiplet business. These standards make chiplets by different vendors interoperable, which minimizes integration risks and speeds up adoption. In August 2025, the Universal Chiplet Interconnect Express (UCIe) Consortium presented its UCIe 3.0 specification, which also supports increased data rates and a higher level of manageability. This advancement enables scalable system-in-package designs based on multi-chip, which is an important breakthrough towards modular semiconductor ecosystems.

- Chiplet systems continue to embrace the use of high packaging technology, including the 2.5D and 3D integration technology as a way of increasing bandwidth and signal integrity. With these technologies, it is possible to achieve closer interconnections of various chiplets, such as logic, memory, and accelerators, to make compact and high-performance designs. Such developments are essential to be used in artificial intelligence (AI), high-performance computing (HPC) and edge-computing devices. There is still a rise in the need to require approaches such as silicon interposers and hybrid bonding as it goes hand in hand with the wider semiconductor stack.

- AI and HPC workloads are changing the innovation requirements on chiplet interconnects, as monolithic dies are economically and technically constrained to scale in terms of bandwidth, compute and power. On-chip AI inference and training can be customized using modular chiplet architectures, which are facilitated by the latest interconnect technology. This concept provides high performance gain and efficiency of both power and cost over single-die solutions.

- Government programs, including the European Chips Act, are boosting the regional semiconductor ecosystems by financing high-tech manufacturing and pilot lines. Such initiatives facilitate integration technologies, such as packaging and interconnects. Such frameworks under private-public partnerships create capacity and speed up the creation of chiplet interconnects, which is activity enhancing the resilience and expansion of the semiconductor ecosystem in general.

Chiplet Interconnect Market Analysis

Learn more about the key segments shaping this market

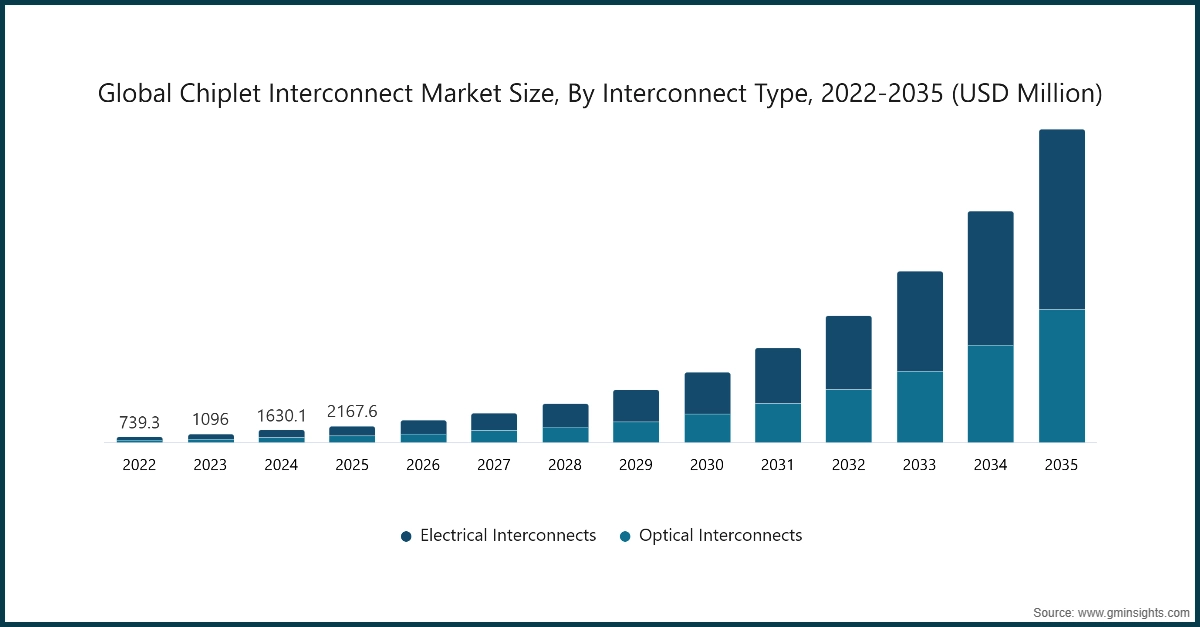

Based on interconnect type, the market is divided into electrical interconnects, and optical interconnects.

- The electrical interconnects segment accounted for the largest market and was valued at USD 1.34 billion in 2025. The current chiplet architectures are dominated by electrical interconnects as they have been shown to be reliable, less complex to implement, and compatible with existing packaging ecosystems and are the choice of early-stage AI, HPC, and server processors.

- Established design equipment, mature manufacturing processes and extensive foundry support make electrical interconnects affordable to scale, providing incentives to use them in data centers, networking equipment, and enterprise computing platforms in large numbers.

- OEMs must maximize power efficiency and bandwidth density of their designs with existing packaging infrastructure in order to fasten time to market on high-volume AI and server applications.

- The optical interconnects segment was the fastest growing market during the forecast period, growing at a CAGR of 35.9% during the forecast period. The use of optical interconnects is gaining traction because AI and HPC workloads are becoming too big to be supported by electrical interconnects in terms of bandwidth and latency and because optical interconnects can support ultra-high-speed data transfer with minimally signal loss over short and medium distances.

- Optical interconnects enable much lower power consumption of data transfer in dense multi-chip systems, which is important in large scale computing systems of very small performance requirements defined by energy consumption and thermal operation.

- Manufacturers should invest in silicon photonics integration and co-packaged optics to position optical interconnect solutions for next-generation AI clusters and exascale computing platforms.

Learn more about the key segments shaping this market

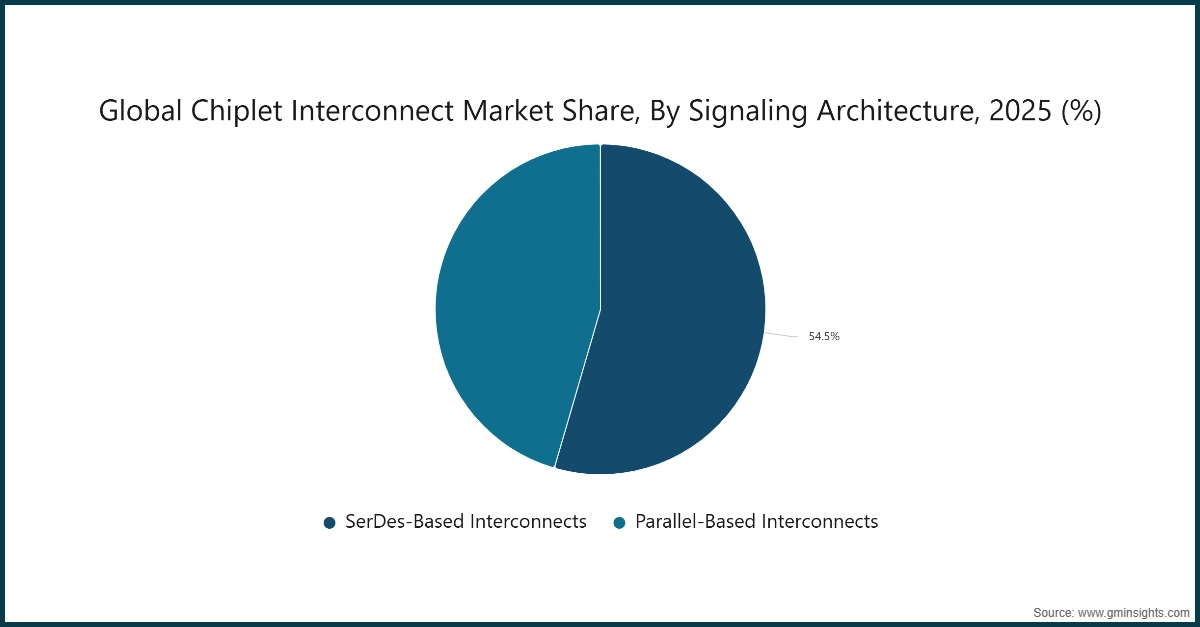

On the basis of signaling architecture, the chiplet interconnect market is divided into SerDes-based interconnects and parallel-based interconnects.

- The SerDes-based interconnects segment accounted for the largest market and was valued at USD 1.18 billion in 2025. SerDes-based interconnects dominate chiplet designs due to their ability to support high-speed data transmission over longer distances, making them ideal for complex multi-die architectures in AI, HPC, and networking processors.

- Strong compatibility with established protocols, design tools, and standards such as UCIe and PCIe enables seamless integration, reducing design risk and accelerating adoption across data center and enterprise semiconductor platforms.

- Manufacturers should enhance SerDes interconnect efficiency through advanced equalization and power optimization while aligning designs with open standards to maintain leadership in high-volume AI and data center markets.

- The parallel-based interconnects segment was the fastest growing market during the forecast period, growing at a CAGR of 36.3% during the forecast period. Parallel-based interconnects are gaining traction for short-reach chiplet communication, offering ultra-low latency and reduced power consumption, which is critical for tightly coupled chiplet architectures and edge computing applications.

- Simpler signaling architecture enables compact layouts and cost-effective integration in advanced packaging, driving faster adoption in emerging chiplet designs where performance-per-watt and space efficiency are prioritized.

- Manufacturers should focus on scalable parallel interconnect designs optimized for short-distance communication, targeting energy-sensitive applications such as edge AI, automotive electronics, and compact accelerator modules.

Based on protocol model, the chiplet interconnect market is divided into open standard protocols, and proprietary die-to-die protocols.

- The proprietary die-to-die protocols segment accounted for the largest market and was valued at USD 1.32 billion in 2025. Proprietary protocols dominate current deployments as they are tightly optimized for specific architectures, enabling superior bandwidth, latency control, and power efficiency in high-performance CPUs, GPUs, and AI accelerators.

- Large semiconductor vendors continue to rely on proprietary interconnects to protect IP, maintain ecosystem control, and ensure seamless integration across internal product portfolios, reinforcing near-term market leadership.

- Manufacturers should continue refining proprietary protocols for performance leadership while ensuring migration paths toward interoperability to remain competitive as open standards gain broader ecosystem acceptance.

- The open standard protocols (UCIe-led) segment was the fastest growing market during the forecast period, growing at a CAGR of 36.7% during the forecast period. Open standard protocols accelerate adoption by enabling chiplets from different vendors to interoperate, reducing integration complexity and fostering scalable, modular semiconductor system design.

- Widespread support from semiconductor alliances and government-led initiatives promotes standardization, lowers entry barriers, and accelerates commercialization of UCIe-based chiplet interconnect solutions.

- Manufacturers should actively adopt UCIe-compliant designs and participate in standards ecosystems to expand market reach, enable multi-vendor compatibility, and capture long-term growth in modular chiplet platforms.

Looking for region specific data?

North America Chiplet Interconnect Market

North America market held a market share of 42.7% in 2025 of the global market.

- A powerful semiconductor ecosystem, advanced R&D, and early access to cutting-edge packaging technologies has allowed North America to dominate the market by enabling high bandwidth, low latency interconnects that are essential to AI and HPC systems.

- The deep innovation centers, governmental incentives, and industry-research partnerships in the United States and Canada favor the revolution of heterogeneous integration and modular chip systems.

- Major packaging investments, particularly in interposer and substrate technologies, improve global competitiveness and resiliency of North America in semiconductor supply chains since they provide scalable chiplet architectures.

- Manufacturer needs to focus on collaboration with the U.S. advanced packaging R&D centers to take advantage of the government incentives and scalable chiplet interconnect solutions that could be offered to the data center and defense markets.

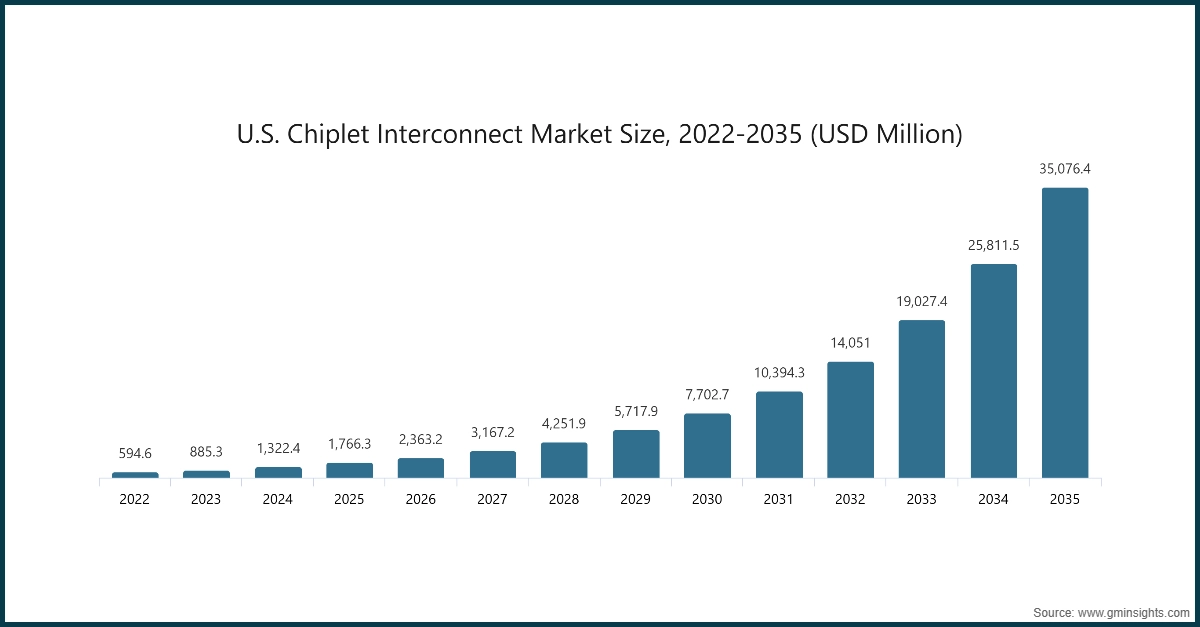

The U.S. chiplet interconnect market was valued at USD 594.6 million and USD 885.3 million in 2022 and 2023, respectively. The market size reached USD 1.76 billion in 2025, growing from USD 1.32 billion in 2024.

- The United States is enhancing its support for advanced semiconductor packaging, a critical element for chiplet interconnect technologies, through federal initiatives aimed at strengthening domestic capabilities and ensuring supply chain resilience.

- For instance, in November 2024, the CHIPS for America program announced funding of up to USD 300 million to establish an interconnect foundry. This initiative seeks to integrate advanced packaging processes with workforce development programs while collaborating with semiconductor fabs and manufacturers.

- This investment is designed to advance research and manufacturing capacity in high-performance interconnects, solidifying the United States' leadership in modular semiconductor systems and heterogeneous integration, which are essential for the future of artificial intelligence, automotive applications, and high-performance computing platforms.

- Manufacturers should leverage CHIPS Act funding opportunities to build domestic interconnect facilities, aligning product development with federal targets for AI and HPC semiconductor ecosystems.

Europe Chiplet Interconnect Market

Europe market accounted for USD 382.9 million in 2025 and is anticipated to show lucrative growth over the forecast period.

- The interconnect trend on chiplets in Europe is determined by the strategic governmental support on resilient semiconductor innovation and advanced packaging infrastructure.

- The APECS pilot line in the EU Chips Act is dedicated to the bridging of application-oriented research with heterogeneous integration and chiplet technologies, scale and system-in-package design development in the automotive, industrial, and computing industries.

- The capability to integrate chiplet interconnect into industrial and edge computing is becoming more common among European manufacturers, with the help of coordinated public R&D funding and public-private alliances.

- Manufacturers must engage with EU Chips Act programs to localize interconnect technology development and scale chiplet solutions for automotive and industrial applications within European supply chains.

Germany dominated the Europe chiplet interconnect market, showcasing strong growth potential.

- Germany is emerging as a key hub for chiplet innovation within Europe’s semiconductor landscape, driven by government‑aligned research infrastructure and industrial collaboration.

- For instance, in March 2025, Research Fab Microelectronics Germany (FMD) unveiled the Chiplet Application Hub, a platform designed to accelerate chiplet technology development and industrial uptake across sectors. The hub works in conjunction with Germany’s participation in Europe’s advanced packaging initiatives, promoting prototyping and heterogenous integration capabilities.

- By blending research excellence with industrial partnerships, Germany is reinforcing its capacity to contribute modular, interoperable interconnect solutions that support high‑performance computing, automotive electronics, and industrial automation.

- Manufacturers need to partner with German R&D hubs like the Chiplet Application Hub to gain early access to advanced interconnect prototypes and industrial integration pathways for European markets.

Asia Pacific Chiplet Interconnect Market

The Asia Pacific chiplet interconnect industry is the largest and fastest growing market and is anticipated to grow at the CAGR of 35.9% during the analysis timeframe.

- The Asia Pacific region has the highest rate of growth in chiplet interconnect usage, driven by strong consumer electronics, automotive and cloud infrastructure demand centers are in China, Taiwan, South Korea and Japan and major semiconductor manufacturing centers.

- Chinese and East Asian domestic policies focus on self-contained advanced-packaging and heterogeneous-integration technologies and, as a result, have made heavy investments in interposer, substrate, and interconnect-R&D.

- The accelerating digitization, industrial automation, and proliferation of 5G/6G networks also contribute to the demands of scalable chiplet architectures.

- Manufacturers need to make investments in manufacturing and process in the advanced packaging supply chain in Asia Pacific to exploit the new demand in the high-performance interconnect solution in both consumer and enterprise markets.

China chiplet interconnect market is estimated to grow with a CAGR of 37.1% during the forecast period, in the Asia Pacific market.

- The trend of chiplet interconnect China is driven by the robust support of the government on the development of the domestic semiconductor capacity and the reduction of reliance on the imported technologies.

- National strategies focus on the development of advanced packaging and heterogeneous integration whereby local companies are able to incorporate interconnect technologies in AI, telecom, and automotive chips.

- The huge electronics market and extensive manufacturing base of China facilitate quick scaling of modular chip architectures, especially in silicon interposer and substrate technologies of high-performance computing.

- Manufacturers should establish R&D to be consistent with the government interests in China in high-end packaging and self-driving semiconductor technology to acquire entry to the market and local supply chain integration of solutions in the interconnect.

Latin American Chiplet Interconnect Market

Brazil leads the Latin American market, exhibiting remarkable growth during the analysis period.

- Brazil's chiplet interconnect industry, though still in its early stages, is experiencing significant growth. This expansion is driven by increasing demand for digital transformation and the growth of the electronics manufacturing sector, particularly in automotive and consumer goods.

- Due to limited domestic semiconductor fabrication capacity, the focus has shifted toward establishing partnerships and importing advanced packaging and interconnect technologies.

- Emerging initiatives are working to connect university programs with the global semiconductor ecosystem, aiming to develop expertise in heterogeneous integration and design methodologies.

- As Brazil continues to expand its cloud infrastructure and adopt artificial intelligence, the demand for high-performance modular microelectronics and interconnect technologies is expected to rise, strengthening the country's digital competitiveness within the region.

Middle East and Africa Chiplet Interconnect Market

South Africa chiplet interconnect industry to experience substantial growth in the Middle East and Africa market in 2025.

- The chiplet interconnect trend is a dynamic process in South Africa, where semiconductor capabilities in an emerging technology ecosystem have been developed.

- Although there is little local fabrics capacity, higher-order electronic design and fabrication education is currently being aggressively promoted by universities and research centers through a capable pool of talent in the future of semiconductor innovations.

- Also, at the regional level, priority is given to developing digital infrastructure, smart manufacturing techniques, and IoT devices. These initiatives are promoting more interest in the modular system design and interconnect technologies.

- South African manufacturers must invest in domestic talent development and cross-border research-related areas to launch chiplet interconnect options into the digital electronics landscape of South Africa.

Chiplet Interconnect Market Share

The chiplet interconnect industry is moderately concentrated, with leading semiconductors and advanced packaging providers collectively holding a significant share of global revenues. Key players such as Intel Corporation, Advanced Micro Devices (AMD), NVIDIA Corporation, Taiwan Semiconductor Manufacturing Company (TSMC) and Samsung Electronics, dominated the competitive landscape and accounted for 56.3% of the total market share in 2025, through extensive semiconductor portfolios, advanced interconnect technologies, and global R&D and manufacturing capabilities.

These companies leverage heterogeneous integration, high-speed die-to-die interconnects, modular chiplet architectures, and standardized protocols such as UCIe to serve AI, HPC, telecom, automotive, and defense applications. Strategic collaborations, pilot programs, and investments in next-generation interconnect solutions strengthen positioning across global semiconductor hubs. Despite this concentration, specialized and regional players remain active, focusing on niche interconnect designs, low-power solutions, and emerging AI/HPC workloads, ensuring ongoing innovation and competitive intensity within the market.

Chiplet Interconnect Market Companies

Prominent players operating in the chiplet interconnect industry are as mentioned below:

- Intel Corporation

- Advanced Micro Devices (AMD)

- NVIDIA Corporation

- Taiwan Semiconductor Manufacturing Company (TSMC)

- Samsung Electronics

- Broadcom Inc.

- Marvell Technology

- Synopsys

- Cadence Design Systems

- Siemens EDA (Mentor Graphics)

- Alphawave Semi

- Rambus Inc.

- Ayar Labs

- ASE Technology Holding

- Amkor Technology

- Intel leads the chiplet interconnect market with an 18.2% share, driven by its comprehensive portfolio of high-performance, heterogeneous integration solutions for AI, HPC, and data center applications. The company emphasizes proprietary and open-standard interconnects, scalable chiplet architectures, and advanced packaging technologies. Intel collaborates closely with cloud providers, enterprise customers, and government research initiatives to expand deployments, ensuring compliance with performance and reliability standards while maintaining superior system integration and efficiency.

- AMD holds an 11.4% share, offering chiplet-based CPU and GPU solutions with high-bandwidth, low-latency interconnects optimized for modular architecture. Its designs focus on performance, energy efficiency, and cost-effective scalability. AMD partners with hyperscalers, OEMs, and AI-focused enterprises to deploy chiplet solutions that accelerate compute workloads while reducing power consumption and operational complexity.

- NVIDIA commands a 10.7% share, focusing on high-speed interconnects for AI accelerators, GPUs, and HPC platforms. Its chiplet solutions emphasize low latency, massive parallelism, and high memory bandwidth. NVIDIA collaborates with cloud providers, AI research labs, and HPC integrators to deliver scalable modular systems that support cutting-edge computing and accelerate deployment of AI-driven workloads.

- TSMC controls 8.6% of the market, providing advanced foundry and packaging services that enable high-density chiplet interconnect integration. Its solutions emphasize heterogeneous integration, 2.5D/3D packaging, and manufacturing reliability.

- Samsung Electronics holds a 7.4% market share, delivering specialized chiplet interconnect and packaging solutions for memory, logic, AI accelerators, and data center platforms. Its offerings focus on high-performance integration, low-power operation, and advanced semiconductor nodes. Samsung collaborates with cloud service providers, industrial electronics companies, and telecom integrators to deploy innovative, scalable, and reliable modular semiconductor solutions.

Chiplet Interconnect Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 2.17 Billion |

| Market Size in 2026 | USD 2.89 Billion |

| Forecast Period 2026-2035 CAGR | 34.4% |

| Market Size in 2035 | USD 41.2 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Heterogeneous Integration Demand | Strengthens market adoption as designers increasingly integrate CPUs, GPUs, AI accelerators, memory, and specialized IP into single packages. |

| Advanced Node Cost Optimization | Drives adoption as chiplet architecture allows performance-critical blocks to leverage cutting-edge nodes while offloading less critical functions to mature, lower-cost nodes. |

| AI and HPC Workload Scaling | Expands demand as next-generation AI and HPC applications require massive bandwidth, low latency, and modular compute solutions. |

| Yield Improvement and Design Flexibility | Enhances market penetration by improving die yields and lowering the impact of defects |

| Ecosystem Standardization and Open Interconnects | Supports broader adoption by enabling interoperability between chiplets from different vendors. |

| Pitfalls & Challenges | Impact |

| Lack of Universal Interoperability | Limits adoption as proprietary interconnects create integration challenges between chiplets from different manufacturers. |

| Thermal and Power Management Constraints | Restricts performance scaling and system efficiency as high-density chiplet integration increases heat density and power consumption. |

| Opportunities: | Impact |

| Expansion of AI and HPC-Optimized Chiplet Solutions | Enables manufacturers to develop modular interconnect solutions tailored for AI training, inference, and high-performance computing workloads. |

| Development of Open-Standard Interconnect Ecosystems | Encourages multi-vendor collaboration and reduces integration complexity, creating opportunities for companies to provide interoperable chiplets, standardized interconnect IP, and design services that accelerate adoption across heterogeneous platforms. |

| Market Leaders (2025) | |

| Market Leader |

Market share of Intel Corporation is 18.2% in 2025 |

| Top Players |

Collective market share in 2025 is 56.3% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest Growing Market | Asia Pacific |

| Emerging Countries | India, China, Brazil, South Africa, and the United Arab Emirates |

| Future outlook |

|

What are the growth opportunities in this market?

Chiplet Interconnect Industry News

- In September 2025, Tata Consultancy Services, a global leader in IT services, consulting, and business solutions, announced the launch of its Chiplet-based System Engineering Services, designed to help semiconductor companies push the boundaries of traditional chip design.

- In June 2024, Intel Corporation’s Integrated Photonics Solutions (IPS) Group demonstrated the industry’s first fully integrated bidirectional optical compute interconnect (OCI) chiplet co-packaged with an Intel CPU and running live data. Intel’s OCI chiplet enables co-packaged optical input/output in emerging AI infrastructure for data centers and high performance computing applications.

- In December 2025, Qualcomm completed its acquisition of Alphawave Semi, a leader in high-speed connectivity IP. This move internalizes critical UCIe (Universal Chiplet Interconnect Express) and SerDes technology for Qualcomm's future data center and automotive platforms.

The chiplet interconnect market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Million) from 2022 to 2035, for the following segments:

Market, By Interconnect Type

- Electrical interconnects

- Optical interconnects

Market, By Signaling Architecture

- Serdes-based interconnects

- Parallel-based interconnects

Market, By Protocol Model

- Open standard protocols

- UCIe

- BoW (Bunch of Wires)

- OpenHBI

- Proprietary die-to-die protocols

Market, By Interconnect IP Layer

- Physical Layer (PHY) IP

- SerDes PHY IP

- Parallel PHY IP

- Optical PHY IP

- Controller & Protocol Layer IP

- Protocol controller IP

- Link & flow control IP

- Coherency engine IP

- Protocol adapter & bridging IP

Market, By Interconnect-Enabling Hardware

- Silicon interposers

- Embedded silicon bridges

- Organic interposers & fan-out RDL

Market, By End-use

- High-performance computing (HPC)

- Artificial intelligence / machine learning accelerators

- Data center & cloud infrastructure

- Networking & switching ASICS

- Automotive electronics

- Consumer computing

- Industrial & edge computing

- Others

The above information is provided for the following regions and countries:

- North America

- U.S.

- Canada

- Europe

- Germany

- UK

- France

- Spain

- Italy

- Netherlands

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

Frequently Asked Question(FAQ) :

What is the chiplet interconnect market size in 2025?

The market size for chiplet interconnect is valued at USD 2.17 billion in 2025. Increasing adoption of heterogeneous integration and advanced node cost optimization supports market growth.

What is the market size of the chiplet interconnect industry in 2026?

The market size for chiplet interconnects is projected to reach USD 2.89 billion in 2026, reflecting robust growth driven by AI and HPC workload scaling.

What is the projected value of the chiplet interconnect market by 2035?

The market size for chiplet interconnect is expected to reach USD 41.2 billion by 2035, growing at a CAGR of 34.4%. This growth is fueled by advancements in modular compute solutions, yield improvement, and ecosystem standardization.

How much revenue did the electrical interconnects segment generate in 2025?

The electrical interconnects segment accounted for USD 1.34 billion in 2025, making it the largest segment. Its dominance is attributed to reliability, ease of implementation, and compatibility with existing packaging ecosystems.

What was the valuation of the SerDes-based interconnects segment in 2025?

The SerDes-based interconnects segment was valued at USD 1.18 billion in 2025. Its leadership is driven by the ability to support high-speed data transmission over longer distances, ideal for AI, HPC, and networking processors.

What was the market size of the proprietary die-to-die protocols segment in 2025?

The proprietary die-to-die protocols segment was valued at USD 1.32 billion in 2025. These protocols dominate due to their optimization for specific architectures, offering superior bandwidth, latency control, and power efficiency.

Which region leads the chiplet interconnect market?

North America led the market with a 42.7% share in 2025. Its dominance is driven by advancements in AI, HPC, and server processors, along with strong adoption of electrical interconnects.

What are the upcoming trends in the chiplet interconnect industry?

Key trends include the development of open-standard interconnect ecosystems, modular interconnect solutions for AI and HPC, and increasing adoption of interoperable chiplets. Ecosystem standardization and yield improvement are also driving market growth.

Who are the key players in the chiplet interconnect market?

Key players include Intel Corporation, Advanced Micro Devices (AMD), NVIDIA Corporation, Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, Broadcom Inc., Marvell Technology, Synopsys, Cadence Design Systems, and Siemens EDA (Mentor Graphics).

Chiplet Interconnect Market Scope

Related Reports