Summary

Table of Content

Automotive Fuel Transfer Pumps Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Automotive Fuel Transfer Pumps Market Size

Increasing global vehicle production creates greater demand for automotive fuel transfer pumps as fuel transfer will still be required to get gasoline from the tank to the engine of vehicles with an internal combustion engine. Continuous growth in the manufacture of passenger and commercial vehicles in all major markets continues to create a steady demand for original equipment manufacturer for each industry, whether that is developed or emerging.

For instance, In April 2025, the annual report of the International Organization of Motor Vehicle Manufacturers confirmed that global vehicle production reached about 92.5 billion units in 2024, including 67.7 billion passenger cars and 24.8 billion commercial vehicles, highlighting strong global automotive manufacturing activity.

Automotive Fuel Transfer Pumps Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 18.9 Billion

- 2026 Market Size: USD 19.7 Billion

- 2035 Forecast Market Size: USD 33.9 Billion

- CAGR (2026–2035): 6.2%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: Asia Pacific

Key Market Drivers

- Rising global vehicle production.

- Growing commercial vehicle and logistics fleet.

- Expansion of automotive aftermarket demand.

- Increasing fuel injection system adoption.

Challenges

- Rapid shift toward electric vehicles.

- Fuel price volatility affecting vehicle usage.

Opportunity

- Growth in emerging automotive markets.

- Development of high-efficiency electric fuel pumps.

- Expansion of biofuel and alternative fuel vehicles.

- Increasing demand from off-road and industrial vehicles.

Key Players

- Market Leader: Robert Bosch led with over 19% market share in 2025.

- Leading Players: Top 5 players in this market include Continental Automotive, Delphi Technologies, Denso, Robert Bosch, TI Fluid Systems, which collectively held a market share of 63% in 2025.

Get Market Insights & Growth Opportunities

The growth of global logistics, e-commerce, and transporting freight has continued to increase the total number of commercial trucks and delivery vans that are on the road. Commercial vehicles are typically driven longer distances and therefore require greater durability out of their fuel systems, which has led to growing demand for both OEM installations and aftermarket supply of fuel transfer pumps.

As the global vehicle parc continues to age, there is a growing requirement for the maintenance and replacement of critical components of a vehicle's fuel system, such as fuel transfer pumps. Since the majority of older vehicles are typically exposed to fuel contamination and thermal overload as well as have higher miles driven, these vehicles continue to create intense post-sales demand for replacements in areas where there are large vehicle parc sizes. For instance, in October 2025, more than 600,000 units of automobiles were exported from China, which have contributed to the growth of the global vehicle park and future market demand for aftermarket replacements.

In recent years, the majority of motor vehicles have incorporated some type of electronic fuel injection system (EFI) to enhance fuel economy and fulfill emission standards. An EFI system utilizes high-pressure electric fuel pumps to accurately meter the flow of fuel. These types of pumps have taken the place of previous generation mechanically operated fuel pumps. As a result, the degree of technological sophistication and financial investment has increased for both the automotive sector and the fuel transfer pump market.

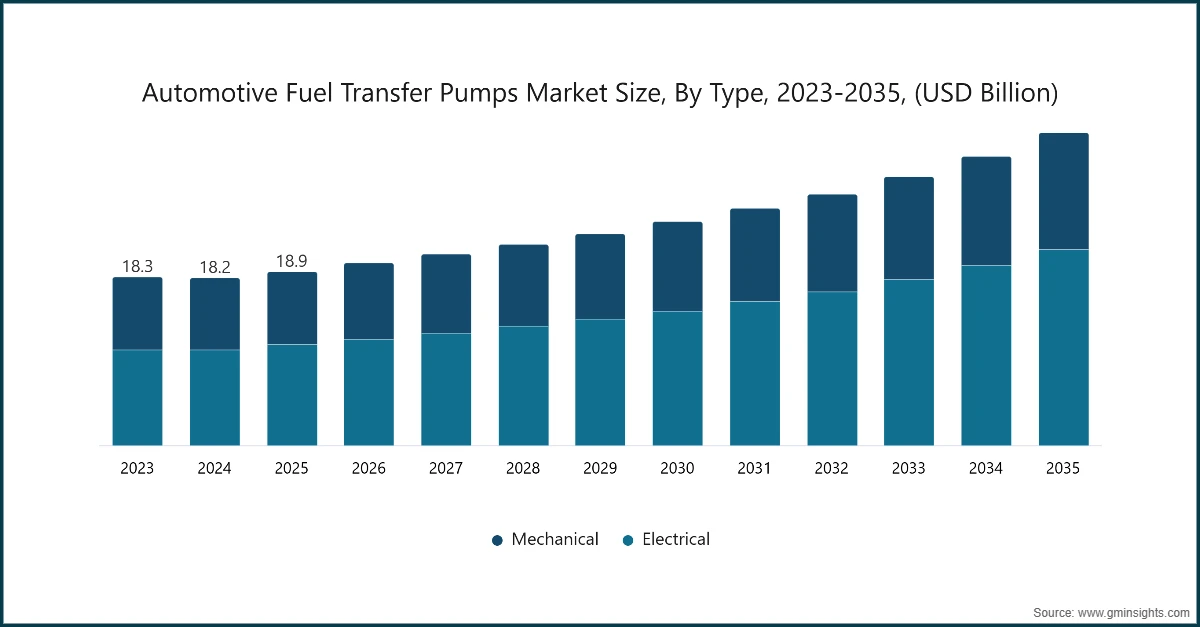

The global automotive fuel transfer pumps market was valued at USD 18.9 billion in 2025. The market is expected to grow from USD 19.7 billion in 2026 to USD 33.9 billion in 2035 at a CAGR of 6.2%, according to latest report published by Global Market Insights Inc.

To get key market trends

Automotive Fuel Transfer Pumps Market Trends

Automakers continue to move away from using mechanical-type fuel pumps and unfueled pumps with electronic fuel pressure delivery and electronics control over both fuel quantities and timing of delivery to increase their performance within engine applications. Electric fueled pumps are now being developed as an alternative method for delivering fuel through the car's fuel system. The functionality of electric fuel pumps can provide vehicle manufacturers with benefits including better overall performance of the engines and controls to eliminate or reduce harmful emissions from the vehicle's internal combustion engine.

Automotive manufacturers are now using integrated fuel pump modules as one complete package, which consists of the actual fuel pump, a fuel filter, a pressure regulator, and sensors within one unit. This integration allows for a reduction in complexity of the overall system, decreased assembly time on the production line, and increased fuel system reliability. This presents additional opportunities for suppliers to provide higher value-added components to vehicle manufacturers through integrated component solutions. In March 2025 automotive production reports stated that vehicle manufacturers are rapidly adopting advanced fuel systems within modern platforms.

Automotive components manufacturers utilize lighter weight polymers/ composites, aluminum and other light-weight corrosion resistant materials to manufacture fuel pumps which will provide greater durability and also a weight reduction to the vehicle. These materials innovations will not only assist in increasing fuel efficiency but will also prolong the life of the fuel pumps and help to improve performance in extreme environmental conditions (extreme temperatures and fuel contamination).

Stricter global emission regulations are forcing automakers to improve fuel delivery precision and engine efficiency. As a result, manufacturers are investing in high-performance fuel pump technologies that provide stable pressure and accurate fuel flow, helping vehicles meet increasingly stringent emission standards and fuel economy requirements.

Automotive Fuel Transfer Pumps Market Analysis

Learn more about the key segments shaping this market

Based on type, the automotive fuel transfer pumps market is divided into mechanical and electrical. Electrical dominated the market, accounting for 58% in 2025 and are expected to grow at a CAGR of 7.1% through 2026 to 2035.

- Electric fuel pumps are becoming standard in modern vehicles with electronic fuel injections, offering precise fuel flow and high pressure, supporting improved engine efficiency, emission compliance, and performance across passenger cars and commercial vehicles.

- Manufacturers are developing electric pumps with enhanced durability, corrosion resistance, and lightweight materials to meet stringent emission regulations, fuel efficiency targets, and longer vehicle lifespans, driving innovation in OEM and aftermarket applications.

- Mechanical fuel pumps are gradually being replaced by electric pumps in modern passenger cars due to limitations in fuel pressure control and efficiency, but they remain in older vehicles and light-duty commercial applications.

- Mechanical pumps continue to be used in classic cars, motorcycles, and small-engine vehicles where simplicity, cost-effectiveness, and reliability are prioritized over high-pressure fuel delivery, maintaining a niche demand segment in the aftermarket.

Learn more about the key segments shaping this market

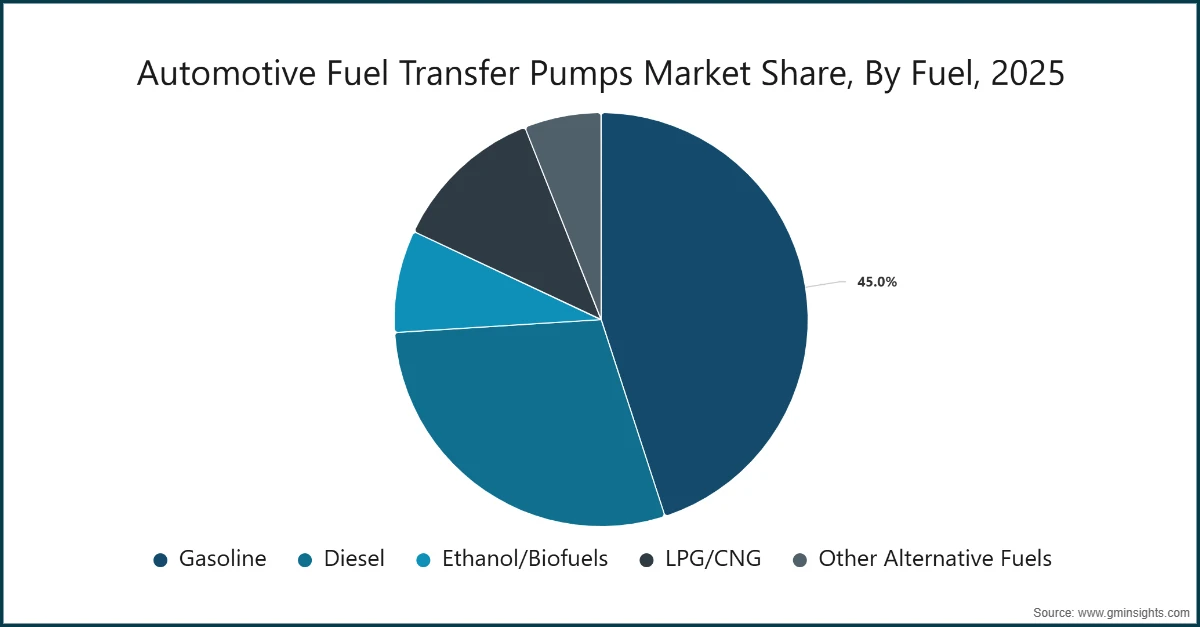

Based on fuel, the automotive fuel transfer pumps market is segmented into gasoline, diesel, ethanol/biofuels, LPG/CNG and other alternative fuels. Gasoline segment dominates the market with 45% share in 2025, and the segment is expected to grow at a CAGR of 6.1% from 2026 to 2035.

- Gasoline-powered vehicles dominate the global passenger car segment. Fuel transfer pumps for gasoline ensure consistent delivery to the engine, supporting fuel injection systems. High production volumes and replacement demand maintain a significant market share in both OEM and aftermarket segments.

- Diesel vehicles, primarily commercial trucks and buses, require robust fuel transfer pumps capable of handling higher viscosity fuels. Diesel pumps support long-duration operations, high-pressure injection systems, and heavy-duty engines, making them critical for commercial and industrial automotive applications.

- Vehicles running on ethanol or biofuel blends require fuel transfer pumps resistant to alcohol-induced corrosion. Pumps must handle variable fuel compositions and maintain efficiency. Adoption is increasing in regions like Brazil, supporting specialized pump production and aftermarket replacement demand.

- LPG and CNG vehicles use fuel transfer pumps designed for gaseous or pressurized fuels. These pumps ensure safe and precise delivery to engines, especially in fleets and urban commercial vehicles, representing a growing niche segment in alternative-fuel automotive markets.

Based on vehicle, the automotive fuel transfer pumps market is segmented into passenger cars, commercial vehicles and two-wheelers. Passenger cars segment dominates the market with 63.7% share in 2025, and the segment is expected to grow at a CAGR of 6.7% from 2026 to 2035.

- Fuel transfer pumps for passenger cars account for the largest market share, as both mechanical and electrical pumps are used depending on the engine's fuel delivery system.

- OEM and aftermarket demand for fuel transfer pumps is expected to remain strong over the next several years due to the increase in total vehicles manufactured worldwide, the rise of hybrid vehicle adoption, and the long-life expectancy associated with automobiles today.

- Commercial vehicles (trucks, buses, and vans) require durable fuel transfer pumps capable of operating at high pressures with extended service intervals. Continuous use and heavy-duty fuel systems create very strong OEM installation and after-market replacement need.

- Fuel transfer pumps for motorcycles, scooters, and mopeds are compact in size and appropriate for use with small engines and low-pressure fuel delivery systems.

- Motorcycles, scooters, and mopeds are predominant in the motorcycle markets of Asia-Pacific and Latin America, which provide an opportunity for both OEM and aftermarket niche fuel transfer pumps, especially mechanical fuel transfer pumps since most developing regions currently have only mechanical fuel transfer pumps.

Based on sales channel, the automotive fuel transfer pumps market is segmented into OEM and aftermarket. OEM segment is expected to dominate the market with a share of 64% in 2025.

- OEM fuel transfer pump demand is driven by new vehicles. Fuel transfer pumps are manufactured for use in assembling ICE and hybrid vehicles, with the types of pumps used based on engine type (ICE or hybrid), type of fuel system (e.g., gasoline, diesel), and emissions requirements.

- This section of the fuel transfer pump market is essential to global passenger vehicle manufacturers' supply chains.

- The aftermarket for fuel transfer pumps is to provide replacement and maintenance needs for older (in terms of age) vehicles.

- As more fleets are reaching older (in terms of age) vehicles, fuel transfer pumps in these vehicles will need to be replaced due to contamination from fuel, exposed to heat from the engine, and have accumulated significant mileage.

- This is creating a continuous need for mechanical and electric fuel transfer pumps regardless of whether the vehicle is a passenger car, commercial vehicle, or motorcycle/scooter/moped.

Looking for region specific data?

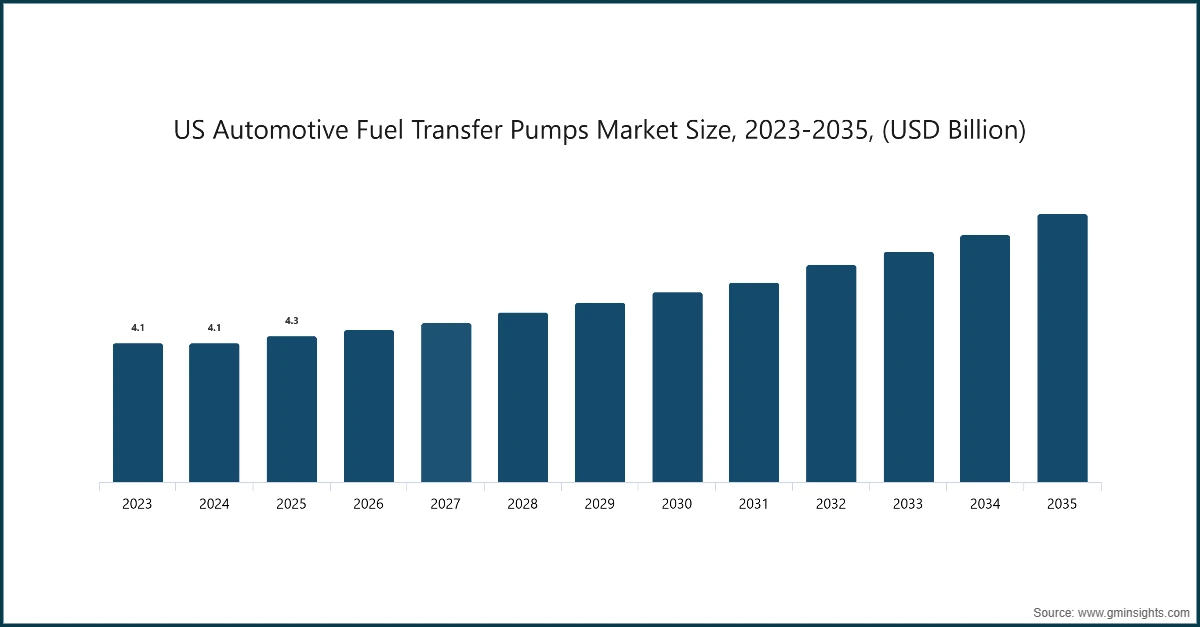

US automotive fuel transfer pumps market reached USD 4.3 billion in 2025, growing from USD 4.1 billion in 2024.

- US economy has both demand for and production of pick-up trucks and SUVs that have internal combustion engines and durable fuel delivery systems. Due to the high volume of production of large automobile types, there is a need for original equipment manufacturer (OEM) fuel transfer pumps as well as vital aftermarket fuel transfer pumps due to extended usage of these large vehicle types.

- US market has one of the largest automotive aftermarket industries as a result of the size of the vehicle parc, as well as the average age of vehicles. As vehicles are used longer, replacement demand for automotive fuel system components such as fuel transfer pumps is increasing in vehicle service centers and repair networks.

- The demand for fuel transfer pumps in the near future will continue to be steady since internal combustion engine vehicles still make up the majority of the vehicle fleet in the US, though electric vehicle adoption is occurring.

- Therefore, there is a continuing demand for fuel transfer pumps used in commercial vehicles and hybrid vehicles, which use normal fuel delivery systems.

North America dominated the automotive fuel transfer pumps market with a market size of USD 5.2 billion in 2025.

- In North America, there is an ever-increasing growth in e-commerce and cross-border trade, which has resulted in increased numbers of trucks and delivery vehicles on the road.

- Reliable fuel transfer pumps are required by these commercial fleet vehicles, which means there will be a long-term after-market replacement opportunity for these fuel transfer pumps.

- Automakers across North America are adopting advanced fuel injection technologies to meet emission regulations and improve engine efficiency. This transition increases the use of electric fuel transfer pumps capable of maintaining consistent pressure and supporting modern fuel delivery systems.

Europe automotive fuel transfer pumps market accounted for a share of 22.2% and generated revenue of USD 4.2 billion in 2025.

- European governments continue implementing stringent emission standards that require automakers to improve engine efficiency and fuel delivery precision. This drives demand for advanced electric fuel pumps capable of maintaining accurate fuel pressure and supporting modern fuel injection technologies.

- Europe has an aging vehicle fleet, with many passenger cars operating for more than a decade. Older vehicles require frequent maintenance and component replacements, increasing aftermarket demand for fuel transfer pumps and other fuel system components across the region.

- Hybrid vehicles are becoming increasingly popular across Europe as governments promote lower-emission mobility. These vehicles combine electric motors with internal combustion engines, sustaining demand for fuel transfer pumps while enabling automakers to meet emission targets.

Germany dominates the automotive fuel transfer pumps market, showcasing strong growth potential, with a CAGR of 6.5% from 2026 to 2035.

- Germany remains one of the world’s leading automotive manufacturing hubs, producing billions of vehicles annually. The presence of major automakers and component suppliers supports strong demand for fuel transfer pumps in OEM applications, particularly in high-performance engines used in premium and luxury vehicles.

- German automakers are investing heavily in high-efficiency internal combustion engines that require advanced fuel delivery systems. This drives the adoption of high-pressure electric fuel pumps and integrated fuel modules designed to meet strict European emission and fuel efficiency regulations.

- Germany is increasingly adopting hybrid powertrains as a transitional technology toward full electrification. Hybrid vehicles still require fuel transfer pumps for gasoline engines, creating ongoing demand for advanced fuel pump technologies even as electric vehicle adoption grows.

The Asia Pacific automotive fuel transfer pumps market is anticipated to grow at the highest CAGR of 7.3% from 2026 to 2035 and generated revenue of USD 7.3 billion in 2025.

- Asia-Pacific region is the world's leading automotive manufacturing region, primarily driven by China, Japan, India, and South Korea. As a result of such high levels of automotive production, there is a lucrative Original Equipment Manufacturer (OEM) market for automotive fuel transfer pumps, particularly for passenger cars and light commercial vehicles.

- The increase in disposable incomes and urbanization in Asia-Pacific countries is leading to an increase in the number of vehicles that are owned. The more people who purchase vehicles, the more there will be an increase in demand for fuel system components, including fuel transfer pumps, across emerging automotive markets.

- Automotive manufacturers located in the Asia-Pacific region are investing heavily in more advanced fuel-efficient engine technologies to meet new, stricter emissions requirements. Such engines require an advanced and precise fuel delivery system, leading to an increase in demand for high-performance electric fuel transfer pumps.

China automotive fuel transfer pumps market is estimated to grow with a CAGR of 8.3% from 2026 to 2035.

- China is the world's largest automotive manufacturing nation. The large-scale production of both passenger cars and commercial trucks creates a significant OEM demand for fuel transfer pumps throughout both domestic and export supply chains.

- China has been experiencing strong growth in the sale of hybrid cars, with many manufacturers providing consumers with the option of either purchasing a traditional internal combustion engine (ICE) vehicle or a fully electric vehicle.

- The Chinese manufacturer of automotive components is expanding its production capacity and technology capabilities to keep up with the increased demand for fuel system components.

Latin America automotive fuel transfer pumps market shows lucrative growth over the forecast period.

- Latin America is witnessing gradual growth in vehicle production, particularly in Brazil and Mexico. Expanding automotive manufacturing facilities support demand for fuel system components used in internal combustion engine vehicles.

- A large and aging vehicle fleet across Latin America drives strong demand for aftermarket automotive components. Fuel transfer pumps are commonly replaced during vehicle maintenance, creating stable demand across repair and service networks.

- Growing logistics, mining, and agricultural activities in Latin America are increasing demand for commercial vehicles. These vehicles rely on robust fuel systems, driving the need for durable fuel transfer pumps.

Brazil automotive fuel transfer pumps market is estimated to grow with a CAGR of 4.4% from 2026 to 2035 and reach USD 0.9 billion in 2035.

- Brazil has a large market for flex-fuel vehicles that run on ethanol and gasoline. These vehicles require specialized fuel transfer pumps capable of handling ethanol-blended fuels, creating unique opportunities for manufacturers of fuel system components.

- These types of vehicles require specially designed fuel transfer pumps capable of transferring ethanol-blended fuels; this creates unique opportunities for component manufacturers in the fuel systems component area.

- Brazil continues to remain the largest automotive manufacturing center in South America. Global automobile manufacturers with vehicle assembly plants in Brazil continue to produce both passenger vehicles and commercial vehicles; the need for fuel transfer pumps means there will be a continued demand for fuel systems components.

- The number of vehicles on the road in Brazil continues to increase, leading to a corresponding increase in the demand for automotive repair and replacement part use. Fuel transfer pumps are among the components that are routinely replaced while servicing vehicles and will continue to lead to steady growth within the aftermarket sector.

Middle East and Africa automotive fuel transfer pumps market accounted for USD 1.07 billion in 2025 and is anticipated to show lucrative growth over the forecast period.

- Many countries in the Middle East and Africa continue to rely heavily on internal combustion engine vehicles due to limited electric vehicle infrastructure. This dependence sustains strong demand for fuel transfer pumps in both passenger and commercial vehicles.

- Infrastructure development and growing trade activities across the region are increasing demand for trucks and buses. These vehicles require reliable fuel delivery systems, supporting growth in the automotive fuel transfer pump market.

- The region imports large volumes of vehicles from global manufacturers. As these vehicles age, the demand for replacement parts including fuel transfer pumps grows within local automotive service and repair markets.

UAE market is expected to experience substantial growth in the Middle East and Africa automotive fuel transfer pumps market, with a CAGR of 2.9% from 2026 to 2035.

- The UAE has a strong market for luxury and high-performance vehicles, many of which use powerful internal combustion engines. These vehicles require advanced fuel delivery systems, increasing demand for high-performance fuel transfer pumps.

- Many imported vehicles and harsh operating conditions create strong demand for automotive maintenance services in the UAE. Fuel transfer pumps often require replacement due to high temperatures and fuel quality variations.

- While electric vehicles are gradually entering the UAE market, internal combustion engine vehicles are still dominating the automotive fleet. This maintains steady demand for fuel transfer pumps in passenger cars and commercial vehicles.

Automotive Fuel Transfer Pumps Market Share

- The top 7 companies in the automotive fuel transfer pumps industry are Robert Bosch, Denso, Delphi Technologies, Continental Automotive, TI Fluid Systems, Mitsubishi Electric and Aisin Seiki, contributing 76% of the market in 2025.

- Robert Bosch is the industry leader in fuel transfer pumps globally by supplying advanced ICE fuel systems (hybrids) and has a very good relationship with OEMs. In addition, Bosch has a large geographical footprint and invests heavily in new product development (R&D), which drives worldwide pump demand for both passenger and commercial vehicle applications.

- Denso leverages the entire Toyota Ecosystem to manufacture and sell high-precision fuel transfer pumps to the automotive industry for ICE/hybrid vehicle applications. Denso’s focus on fuel efficiency, emissions compliance, and dominance in the Asia Pacific enables them to be a major Tier 1 supplier of passenger and light commercial vehicle OEMs that utilize high-precision fuel transfer pump technology.

- Delphi Technologies has traditional and aftermarket fuel pump offerings to the automotive industry, and its fuel pump offerings include electric pumps and high-pressure pumps. Delphi has a unique competitive position with respect to fuel pump technology since the company is owned by strong capabilities in providing both Tier 1 and aftermarket products, has an extensive presence in North America, Europe, and Asia Pacific, and provides a broad spectrum of fuel system component applications supporting the automotive industry.

- Continental Automotive is a manufacturer of electronic fuel management systems and has considerable expertise in integrating hybrid vehicle technology into today’s ICE fuel management systems. Continental has a strong global presence and maintains cooperative agreements with major automotive manufacturers, providing significant volumes of Tier 1 fuel systems and aftermarket opportunities for Europe, North America, and Asia Pacific.

- TI Fluid Systems primarily manufactures brushless and electronic fuel pumps for Tier 1/OEM applications. The company’s integrated fuel delivery systems provide solutions to passenger car and commercial vehicle manufacturers, and these systems utilize technology that has demonstrated efficiency, durability, and regulations concerning regional emissions that follow the regulations of Europe, North America, and Asia Pacific.

- Mitsubishi Electric delivers high-precision fuel pumps compatible with ICE, hybrid, and emerging EV fuel systems. Its advanced pump technologies target both OEM and high-performance vehicles, primarily in Asia-Pacific, Europe, and North America, supporting efficiency and emission compliance.

- Aisin Seiki provides fuel transfer pumps for Toyota and other OEMs, focusing on hybrid and ICE vehicle integration. Its strength in APAC, North America, and Europe enables robust supply of reliable, high-efficiency pumps for passenger cars and commercial fleets.

Automotive Fuel Transfer Pumps Market Companies

Major players operating in the automotive fuel transfer pumps industry are:

- Aisin Seiki

- Carter Fuel Systems

- Continental Automotive

- Delphi Technologies

- Denso

- Mitsubishi Electric

- Pierburg (Rheinmetall)

- Robert Bosch

- TI Fluid Systems

- The worldwide automotive fuel transfer pump market is very diverse, with a broad range of companies involved, which include tier-1 automotive suppliers, specialist component suppliers and aftermarket-focused companies. All these companies exhibit different strategies, based on their position within the marketplace, which means that global tier-1 automotive suppliers are focused on providing comprehensive systems & OEM relationships; regional players are concentrating on aftermarket channel strength and providing more specialized products/solutions, and new entrants target premium performance categories using innovative technologies.

- The competitive landscape continue to evolve, driven by ongoing market consolidation, continual technological advances in relation to alternative fuels & efficiency; transformation of the aftermarket channel; and optimization efforts by leading suppliers within the automotive fuel transfer pump marketplace.

- The high concentration reflects substantial barriers to entry including comprehensive automotive quality system requirements, extensive engineering capabilities necessary for complex vehicle integration, global manufacturing footprint requirements serving international automotive customers, and established long-term OEM relationships characterizing tier-1 automotive supply. Market leadership positions have remained relatively stable over the past decade, though incremental share shifts reflect technology transitions, regional market growth dynamics, and strategic moves including mergers, acquisitions, and business unit transfers

Automotive Fuel Transfer Pumps Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 18.9 Billion |

| Market Size in 2026 | USD 19.7 Billion |

| Forecast Period 2026-2035 CAGR | 6.2% |

| Market Size in 2035 | USD 33.9 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Rising global vehicle production | Increases OEM demand for fuel transfer pumps as every ICE vehicle requires at least one pump. |

| Growing commercial vehicle and logistics fleet | Expanding freight and logistics operations raise demand for durable fuel pumps in trucks and buses. |

| Expansion of automotive aftermarket demand | Global ageing vehicle fleets increase replacement demand for fuel transfer pumps. |

| Increasing fuel injection system adoption | Wider adoption of electronic fuel injection systems boosts demand for advanced electric fuel transfer pumps. |

| Pitfalls & Challenges | Impact |

| Rapid shift toward electric vehicles | Declining ICE vehicle production gradually reduces long-term demand for traditional fuel transfer pumps. |

| Fuel price volatility affecting vehicle usage | High fuel prices can reduce vehicle usage and delay pump replacements in the aftermarket. |

| Opportunities: | Impact |

| Growth in emerging automotive markets | Rising vehicle ownership in developing economies increases both OEM and aftermarket pump demand. |

| Development of high-efficiency electric fuel pumps | Technological advancements enable manufacturers to capture demand for modern fuel-injected engines. |

| Expansion of biofuel and alternative fuel vehicles | Adoption of ethanol, biodiesel, and CNG vehicles creates demand for specialized compatible fuel pumps. |

| Increasing demand from off-road and industrial vehicles | Growth in agriculture, construction, and mining equipment expands applications for fuel transfer pumps. |

| Market Leaders (2025) | |

| Market Leader |

19% market share |

| Top Players |

Collective market share in 2025 is 63% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest growing market | Asia Pacific |

| Emerging countries | India, Brazil, Mexico, Indonesia, Thailand |

| Future outlook |

|

What are the growth opportunities in this market?

Automotive Fuel Transfer Pumps Industry News

- In April 2025, ABC Technologies purchased TI Fluid Systems for $2.3 billion, creating an entity called TI Automotive, with 95 facilities located around the globe. It provides fluid handling and thermal management as well as engineered components and strengthens tier-1 capability on both conventional and electrified vehicle architectures.

- In February 2025, TI Automotive developed a modular thermal management system for battery electric vehicles (BEVs) consisting of a 12-volt electric coolant pump that can enhance thermal performance of the battery by providing coolant to it, electronics, and cabin. The system will also improve vehicle efficiency, help reduce vehicle weight, and help extend range for BEVs.

- In January 2025, PHINIA strengthened its relationship with Alpine Racing by supplying direct injection (DI-CHG) hydrogen injectors for their prototype cars. These injectors will offer very precise delivery of Hydrogen as a gaseous fuel for racing vehicles and will support the continued growth of alternative fuel development beyond battery electric vehicles in both motorsport and prototype.

- In September 2024, Continental will increase its aftermarket offering of high-pressure fuel pumps to 700 new part numbers, including direct injection (DI) fuel systems, by 2025. This increase will involve providing Remote Support digital tools to improve repairs at repair facilities and fulfill the demand for replacement parts of advanced fuel injection vehicles.

The automotive fuel transfer pumps market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) and shipments (million units) from 2022 to 2035, for the following segments:

Market, By Type

- Mechanical

- Electrical

Market, By Fuel

- Gasoline

- Diesel

- Ethanol/Biofuels

- LPG/CNG

- Other Alternative Fuels

Market, By Vehicle

- Passenger car

- Hatchback

- Sedan

- SUV

- Commercial vehicle

- LCV

- MCV

- HCV

- Two wheelers

Market, By Sales channel

- OEM (Original equipment manufacturer)

- Aftermarket

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Nordics

- Poland

- Romania

- Asia Pacific

- China

- India

- Japan

- South Korea

- ANZ

- Vietnam

- Indonesia

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

What was the market size of the automotive fuel transfer pumps in 2025?

The market size was USD 18.9 billion in 2025, growing at a CAGR of 6.2% through 2035. Growth is driven by increasing global vehicle production and demand for efficient fuel transfer systems in internal combustion engine vehicles.

What is the projected value of the automotive fuel transfer pumps market by 2035?

The market is poised to reach USD 33.9 billion by 2035, fueled by advancements in fuel pump technologies and stricter emission regulations.

What is the expected size of the automotive fuel transfer pumps industry in 2026?

The market size is expected to reach USD 19.7 billion in 2026.

What was the market share of electrical fuel pumps in 2025?

Electrical fuel pumps held 58% of the market share in 2025 and are projected to grow at a CAGR of 7.1% through 2035.

What was the market share of the gasoline segment in 2025?

The gasoline segment dominated the market with a 45% share in 2025 and is expected to grow at a CAGR of 6.1% through 2035.

What was the market share of the passenger cars segment in 2025?

The passenger cars segment held a 63.7% market share in 2025 and is anticipated to grow at around 6.7% CAGR through 2035.

What was the valuation of the U.S. automotive fuel transfer pumps sector in 2025?

The U.S. market was valued at USD 4.3 billion in 2025, driven by strong production and demand for pick-up trucks and SUVs requiring durable fuel delivery systems.

What are the upcoming trends in the automotive fuel transfer pumps market?

Key trends include integrated fuel pump modules, lightweight and corrosion-resistant materials, advancements in electric fuel pump technologies, and compliance with stricter global emission regulations.

Who are the key players in the automotive fuel transfer pumps industry?

Key players include Aisin Seiki, Carter Fuel Systems, Continental Automotive, Delphi Technologies, Denso, Mitsubishi Electric, Pierburg (Rheinmetall), Robert Bosch, and TI Fluid Systems.

Automotive Fuel Transfer Pumps Market Scope

Related Reports