Summary

Table of Content

Automotive Fuel Feed Pumps Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Automotive Fuel Feed Pumps Market Size

The market for automotive fuel feed pumps is closely related to the global internal combustion engine vehicles manufactured across the world, as fuel feed pumps are integral parts in internal combustion engine vehicles, including gasoline and diesel engine vehicles. With respect to automobile production statistics, according to the International Organization of Motor Vehicle Manufacturers (OICA), global passenger car production continues to show signs of improvement in 2025. Passenger car production indicated an increase of 5.5 percent in the first three quarters of 2025 compared to the same period in 2024, with more than 50 million passenger cars manufactured.

Automotive Fuel Feed Pumps Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 4.9 Billion

- 2026 Market Size: USD 5 Billion

- 2035 Forecast Market Size: USD 7.8 Billion

- CAGR (2026–2035): 5.1%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: North America

Key Market Drivers

- Rising Global Vehicle Production & Sales.

- Stringent Emission Norms Driving Fuel Injection Technology Adoption.

- Growing Aftermarket Demand Due to Aging Vehicle Fleet.

- Technological Advancements in Electric Fuel Pump Systems.

Challenges

- Rapid Electrification of Automotive Industry.

- High Cost of Advanced High-Pressure Fuel Pumps.

Opportunity

- Expansion in Emerging Markets with Growing Vehicle Ownership.

- Development of Multi-Fuel Compatible Pump Systems.

- Aftermarket Growth in Developed Markets.

Key Players

- Market Leader: Robert Bosch led with over 16.1% market share in 2025.

- Leading Players: Top 5 players in this market include Continental, Delphi, Denso, Hitachi Astemo, Robert Bosch, which collectively held a market share of 47.5% in 2025.

Get Market Insights & Growth Opportunities

The growth of middle-class populations and urbanization in regions such as Asia, Latin America, and Africa are driving passenger car ownership. Gasoline-powered vehicles are the most cost-effective option for these regions' populations, as they are more affordable at the start of use when compared to electric-powered vehicles. The growth of the automotive manufacturing industry in regions such as China, India, Indonesia, and Thailand will continue to drive demand for ICE components such as fuel feed pumps.

Diesel engines in light and heavy commercial vehicles have continued to dominate the transportation industry globally. According to the International Transport Forum, freight activity is likely to increase in the coming decades. This is attributed to the increasing volumes of trade and the expansion of e-commerce supply chains. Fuel feed pumps are critical in the efficient operation of diesel engines, especially in situations where constant pressure is required to transport heavy loads.

However, the rapid growth of electric vehicle sales is slowly but surely changing the future prospects of the automotive fuel feed pumps market. Data from the International Energy Agency revealed that there was a significant rise in the sales of electric cars in the world market due to the introduction of regulations and targets by governments. In general, battery-powered electric cars do not require fuel tanks, thereby eliminating the need for fuel feed pumps. Therefore, as the market for electric vehicle sales grows in all classes of passenger cars, the market size for fuel feed pumps will decline in the future.

In spite of this change, it is expected that ICE vehicles will still remain in demand in some regions where there will not be stringent regulations for zero-emission vehicles. The markets in Southeast Asia, the Middle East, Latin America, and Africa still rely greatly on gasoline and diesel-powered vehicles due to affordability issues. Although some countries, like the European Union, are moving towards stringent decarbonization strategies based on guidelines from the European Commission, developing countries still have to undergo the transition to electric vehicle technology.

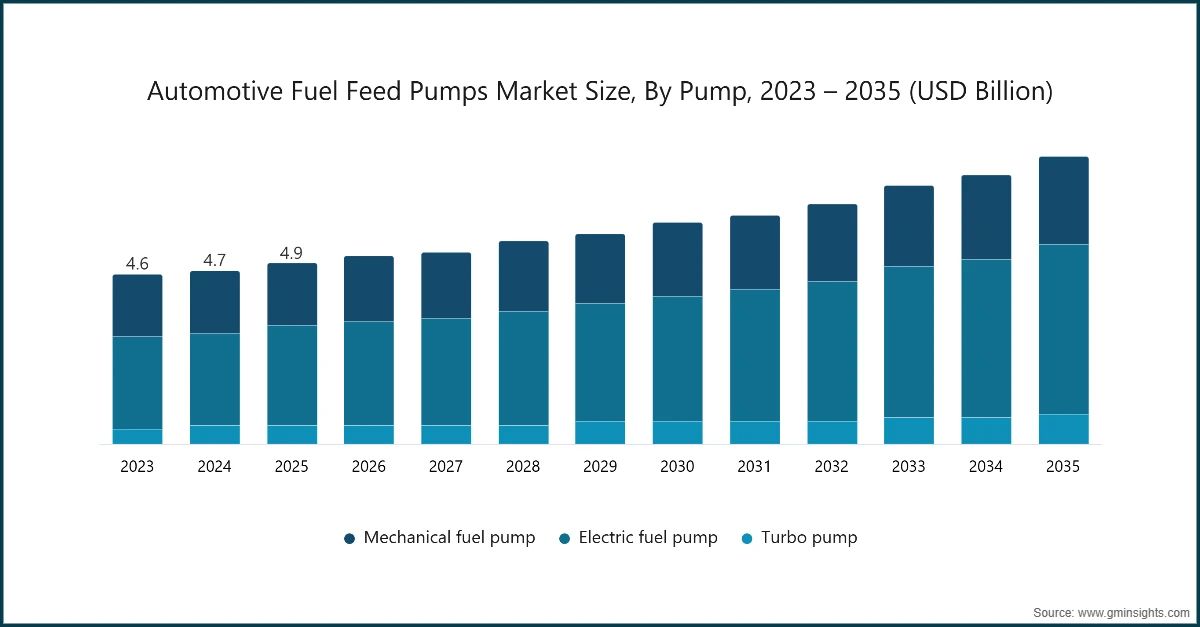

The global automotive fuel feed pumps market was valued at USD 4.9 billion in 2025. The market is expected to grow from USD 5 billion in 2026 to USD 7.8 billion in 2035 at a CAGR of 5.1%, according to latest report published by Global Market Insights Inc.

To get key market trends

Automotive Fuel Feed Pumps Market Trends

ICE production is decreasing slightly due to the adoption of EVs pushed by zero-emission targets and consumer awareness about environment protection. Some regions have already made policies to achieve maximum EV production. However, ICE dominance is still in the regions where such EV policies are not introduced. In these regions, the market is expected to grow.

These fuel feed pumps are an essential component in the overall fuel supply from the tank to the engine in ICE-powered vehicles, whether they be gasoline- or diesel-powered. Even as efficiency improvements have been realized in ICE-powered vehicles, the underlying technology remains largely in need of high-precision, high-durability fuel feed pumps in passenger vehicles, light- and heavy-duty trucks, and commercial vehicles.

Government regulations, like Euro 6/VI in European countries or CAFE regulations in the US, have also influenced the design of ICEs, including fuel feed pumps. Investments in variable pressure pumps and sensor technology have enabled manufacturers to meet the new, even stricter, regulations for limiting NOx and CO2 emissions. According to the Japan Auto Parts Industries Association, fuel consumption can be cut by up to 3% compared to conventional fixed displacement pumps.

Furthermore, there is an increased emphasis on designing lightweight pumps to help in reducing the overall weight of the vehicle. The Automotive Component Manufacturers Association of India (ACMA) found that the usage of advanced materials such as reinforced plastics and aluminum alloys in pump components has increased by 15% over the last three years, thus enabling weight reduction and fuel efficiency in vehicles promoting the market for pumps.

ICE-based platforms have cost advantages in developing countries such as Southeast Asia, Latin America, and Africa, where the overall cost of the vehicles and the service networks are advantageous for petrol and diesel engines. Furthermore, the use in heavy vehicles and off-road applications, where the energy density and fueling rates are advantageous, continues to drive the need for robust fuel feed pumps.

Automotive Fuel Feed Pumps Market Analysis

Learn more about the key segments shaping this market

Based on pump, the market is divided into mechanical fuel pump, electric fuel pump and turbo pump. The electric fuel pump segment dominated the market with market share of around 54.8% and generating revenue of around USD 2.7 billion in 2025.

- Electric fuel pumps have been used mostly for many years. The reason is their ability to offer consistent fuel pressure and delivery, which is paramount for modern internal combustion engines using electronic fuel injection systems. They are also distinct from their mechanical counterparts in that they do not rely on engine speed, thereby offering better fuel efficiency, engine performance, and emission regulations. These factors make electric pumps the best option for OEMs across the globe.

- In modern vehicles, turbocharging, direct fuel injection, and variable valve timing are common, and they require precise control of fuel. Electric fuel pumps can meet this requirement by providing variable pressure and flow rates in real time, matching the engine control unit (ECU) to deliver optimal combustion. This has contributed to their popularity over other types of fuel pumps, including turbo and mechanical fuel pumps, in both passenger and light commercial vehicles.

- Furthermore, the aftermarket segment also supports electric pumps due to their reliability and replaceability. This shows that these pumps are not only in demand in OEM but are also preferred in the aftermarket segment, thus making electric fuel pumps the market leader in 2025.

Learn more about the key segments shaping this market

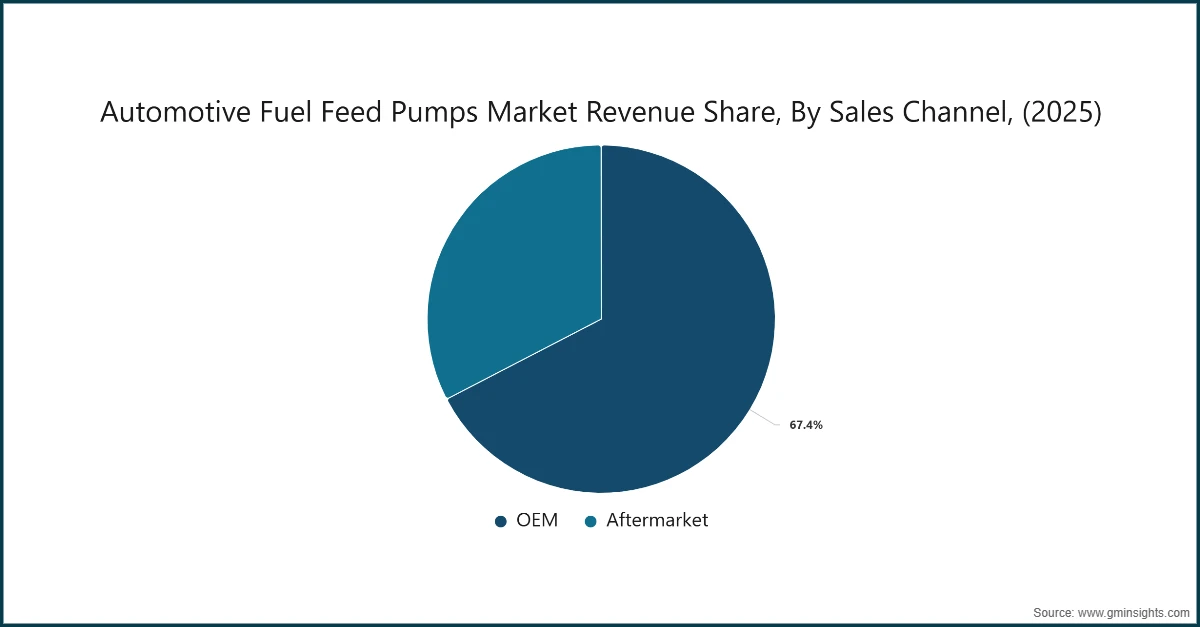

Based on sales channel, the automotive fuel feed pumps market is divided into OEM and aftermarket. The OEM segment accounts for 67.4% in 2025, valued around USD 3.3 billion.

- The vehicle production increases as this also increases the sales channel of the OEMs, which is one of the leading ones. The OEMs provide fuel feed pumps as original equipment, meaning that they are sold directly for the production of new vehicles. This is because, with the advent of ICE technology, the vehicle manufacturers are highly dependent on accurate fuel delivery systems. Hence, they prefer to buy the pumps from the suppliers who are approved by the original equipment manufacturers, increasing the vehicle production for this segment compared to the aftermarket ones.

- The OEM fuel feed pumps are designed and tested to meet various regulatory requirements, including Euro 6/VI, CAFE fuel economy, and local emission regulations. This ensures that the engine is operating at optimal performance, which may not be fully assured in the case of aftermarket products.

- On the other hand, the aftermarket is a segment that holds around 32.6% share in the market for automotive fuel feed pumps, owing to the lower replacement rate for fuel feed pumps, which is generally less than 10% during the life cycle of a vehicle. As the selling price is higher, the revenue contribution makes it also important. With modern electric fuel pumps being more durable and designed to last for the life cycle of vehicles, the overall requirement for fuel feed pump replacements is lower. Although the aftermarket segment caters to this segment, their share is significantly lower compared to OEMs.

Based on pressure, the automotive fuel feed pumps market is divided into low pressure pump and high-pressure pump. The low pressure pump segment is dominant with a market share of around 65.6% in 2025 and is expected to grow at a CAGR of 4.5% between 2026 and 2035.

- The low-pressure pump segment leads the market in 2025. This segment of pumps is largely responsible for the transportation of fuel from the tank to the high-pressure pump or directly to the engine, as seen in conventional fuel injection systems. The majority of internal combustion engine (ICE) vehicles continue to use low-pressure pumps as the initial stage of fuel injection. This makes these pumps essential components of passenger cars, light commercial vehicles, and trucks.

- Cost-effectiveness and simplicity is also the reason for their growth. This is due to the fact that they require fewer precise components and simple control systems compared to high-pressure pumps. This makes them cost-effective, thus making them attractive for conventional ICE platforms. Automotive OEMs use low-pressure pumps in fuel tanks or modules, which makes them reliable with minimum maintenance.

- The high-pressure pumps market is expanding at a faster rate, registering a CAGR of 6.1% between 2026 and 2035. This can be attributed to the increasing demand for direct injection engines and turbocharged ICEs, where precise fuel supply at high pressure is necessary to ensure efficient combustion. These pumps ensure efficient fuel atomization, power output, and reduced emissions, thus meeting stringent global fuel efficiency and emission regulations.

- Moreover, technological advancements in high-pressure pumps, including the integration of sensors and variable pressure controls, have increased their adoption among OEMs in premium passenger cars and LCVs, thus propelling the market segment at a faster rate compared to low-pressure pumps.

Based on vehicle, the automotive fuel feed pumps market is divided into passenger cars and commercial vehicles. The passenger cars segment is expected to grow at the fastest CAGR of 5.3% between 2026 and 2035.

- The passenger cars segment leads the market for automotive fuel feed pumps, considering the huge numbers of internal combustion engine-powered passenger cars being manufactured worldwide. The production of passenger cars has been increasing steadily over the years, and this trend is expected to continue, especially for emerging markets and developed countries where internal combustion engine-powered cars remain cost-effective.

- Furthermore, the dominance of passenger cars also leads to the adoption of fuel-efficient, turbocharged, and direct-injection passenger cars. These cars make use of electric and high-pressure fuel pumps for fuel supply, which are essential for proper combustion, efficient fuel consumption, and emission regulations. The OEMs focus on the proper integration of pumps with passenger cars for efficient performance.

- There are many countries where passenger cars are still being manufactured in large quantities with internal combustion engines. Passenger cars fuel feed pumps also have a strong base in terms of vehicle ownership, urbanization, and rising populations in the important markets such as Asia-Pacific, Latin American, and some emerging markets in Eastern Europe. Passenger cars are leading in terms of new vehicles sold; therefore, they maintain a strong market for fuel feed pumps.

Looking for region specific data?

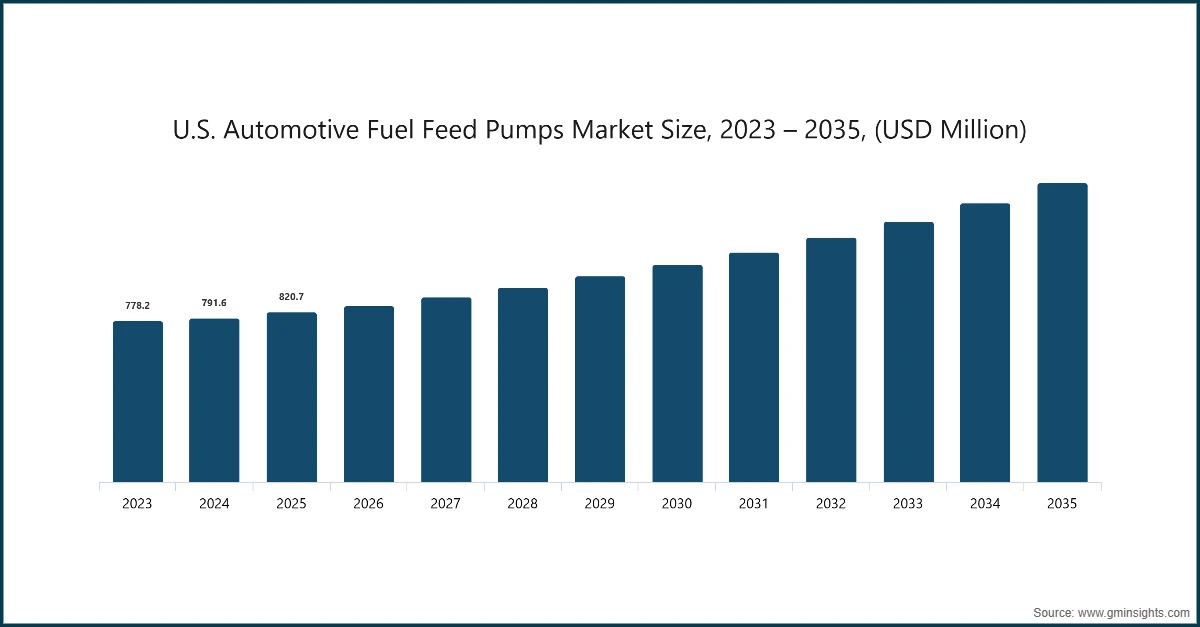

The U.S. automotive fuel feed pumps market reached USD 820.7 million in 2025 and growing at a CAGR of 6.1% between 2026-2035.

- In the United States, the automotive fuel feed pumps industry has been closely linked to the manufacturing and sale of internal combustion engine-powered vehicles. Though the popularity of electric vehicles has been growing in the global market, their share in the total number of vehicles in the United States remains relatively low.

- Therefore, the market for fuel feed pumps in ICE vehicles, including gasoline and diesel-powered vehicles, will continue to exist. North America has been one of the major regional markets, with the U.S. accounting for the majority of the regional market for automotive fuel injection pump.

- The U.S. automotive market has witnessed federal policy changes in fuel economy and emission regulations in recent times. The federal government rolled back some of the stringent fuel economy regulations and challenged state zero emission vehicle regulations, especially in California, which aimed to stop gasoline-powered vehicle sales by 2035.

- The lawsuit by the Department of Transportation against California’s ZEV and greenhouse gas regulations reflects political and legal contention in EV policy and may impede EV adoption in some states, which may indirectly sustain demand for ICE and, in turn, fuel feed pumps.

The North America region is valued at USD 947.5 million in 2025. In terms of volume, the automotive fuel feed pumps market is estimated to exceed 13.4 million units in the same year.

- The lower EV adoption and lack of strict EV policies led the North American region to grow the fastest at a CAGR of 6% between 2026 and 2035. The region continues to be one of the key regions in the market for automotive fuel feed pumps, contributing to a considerable share in the global market in terms of data analysis of the automotive fuel injection market. With a mature automotive industry in the region, there is a healthy demand for fuel feed pumps, especially for low-pressure and electric type pumps used in direct fuel injection systems.

- The dominance of the region can be attributed to the presence of strong ICE products, increasing truck and SUV volumes, as well as services due to the high number of on-road products. Additionally, the region has slower EV adoption rates compared to other regions, as well as a market preference for larger products with traditional powertrains, which directly translates to the need for fuel feed components. Moreover, the level of emission regulations is high, requiring optimum fuel delivery components to meet these requirements without the use of EVs.

The Europe region holds 17.9% of the automotive fuel feed pumps industry share in 2025 and is expected to grow slower at a CAGR of 3.3% between 2026 and 2035.

- Europe’s automotive fuel feed pumps market is characterized by varied regulatory landscapes, economic conditions, and electrification milestones for its member states. The region has traditionally been an important market for automotive fuel feed pumps due to stringent emissions regulations, and high levels of automotive production sophistication.

- Europe, particularly at the EU level, has been at the forefront in setting climate policies for the region. The region had originally targeted a complete ban on sales of new combustion engine cars by 2035, as part of its net-zero emissions objective. However, as a result of policy reconsiderations, the region now plans to have a flexible policy, focusing instead on reducing CO2 emissions rather than banning ICEs.

- The regional incentives, changes in emission testing requirements like Euro 7, and subsidies for cleaner technologies have accelerated technology upgrades for fuel delivery systems, thereby slowing down the natural evolution of ICE technology itself. Additionally, the strong automotive supply chain and manufacturing infrastructure support the demand for fuel feed pumps, even as electrification grows, with a gradual decline forecast over time as ZEVs gain traction.

Germany's automotive fuel feed pumps market is growing quickly in Europe, with a CAGR of 2.8% between 2026 and 2035.

- The country is one of the most prominent automotive hubs in the European region, housing prominent OEMs such as Volkswagen, BMW, and Mercedes Benz. The market for fuel feed pumps in Germany has been traditionally robust, owing to the country’s high automobile and commercial vehicle production with internal combustion and hybrid powertrains. German automobile manufacturers are highly focused on engine performance, fuel efficiency, and emission norms.

- The German government and industry have also announced strong electrification plans, including targets to boost the number of EVs and reduce carbon emissions. There have been discussions about eliminating fossil fuels at fuel stations by 2045. This highlights the decarbonization plans that Germany has in mind. It's not easy, though, as ICEs play a huge role in domestic and export markets, especially in high-performance or luxury segments.

- Similarly, German auto parts suppliers are also adjusting to the new environment by investing in both EV technology and advanced fuel pump technologies that can accommodate turbocharged engines and direct injection technology, which is one of the major areas of innovation in ICE technology. Germany is also an export base for ICE and EV technology.

The Asia Pacific region is expected to grow at a CAGR of 5.3% between 2026 and 2035 in the automotive fuel feed pumps market.

- Asia Pacific leads the global automotive market, making it the most mature region for automotive fuel feed pumps.. The region has been dominant in vehicle production because there is a continuous rise in automobile ownership and strong economic growth. Countries such as China, India, Japan, and South Korea are driving this market.

- Apart from passenger vehicles, the commercial segment in Asia Pacific, including buses, trucks, and two/three-wheelers, still largely uses fuel as a power source and therefore needs a reliable fuel feed pump. Government incentives for cleaner fuels and fuel-efficient vehicles, but not zero-emission vehicles, will also increase the importance of fuel feed pumps.

- Although electrification is taking a rapid pace in countries such as China and Southeast Asia, ICE vehicles still hold a significant share in terms of sales and registration. Hybrid vehicles are playing a vital role in maintaining a balance between emission regulations and consumer demand. They are creating a continuous demand for advanced fuel feed pump systems.

China is estimated to grow with a CAGR of 4.8% in the projected period between 2026 and 2035, in the Asia Pacific automotive fuel feed pumps market.

- The Chinese market leads as the biggest market worldwide for automobiles. The Chinese market has surpassed other Western markets in terms of electric vehicle sales share. It has also surpassed its official NEV targets, with over half of electric car sales coming from China as of 2025. This trend of electric car sales contributes to downward pressure on growth in production of ICE vehicles, hence affecting demand for conventional feed pumps.

- However, in spite of this strong shift towards EVs and new energy vehicles, ICE vehicles still maintain a significant market presence due to their heritage presence and hybrid vehicles. Thus, China’s automotive fuel feed pumps market is still quite significant due to internal demand for traditional fuel delivery systems.

- The Chinese automobile manufacturers are also in global competition, utilizing their robust production capacity and increasing exports of EVs and ICE vehicles. This mutual effect continues to create market demand for fuel feed pumps at home and in other countries where ICE vehicles are dominant. Furthermore, improvements in engine technology and hybrid powertrains ensure that fuel feed components continue to improve.

Mexico is estimated to grow with a CAGR of 5.1% between 2026 and 2035, in the Latin America automotive fuel feed pumps market.

- In the Latin America region, Mexico has its dominance in automobile production. The country comes with considerable automotive assembly and component manufacturing. The policy environment of Mexico for the automotive industry supports the continued production of ICE vehicles, partly due to its integration into the supply chains of the USMCA (United States–Mexico–Canada Agreement) and the demand for light trucks and passenger cars. The support for electrification of vehicles and infrastructure development is not as aggressive as that of other major EV markets.

- The country also has production hubs for commercial vehicles that specifically support logistics and freight transport and also uses diesel and gasoline-based platforms, thus creating demand for fuel feed pumps. The country’s integration with global automotive chains in the automotive industry supports the repair and replacement market for fuel delivery components.

UAE to experience substantial growth in the Middle East and Africa automotive fuel feed pumps market in 2025.

- In the UAE, the market segment for automobiles is highly oriented toward traditional ICE-based vehicles due to the availability of fuel in the past, the preference for high-performance automobiles, and the use of passenger and commercial vehicle fleets running on gasoline or diesel. This has meant that the market segment for fuel feed pumps remains in demand.

- In terms of government initiatives in the UAE, they are slowly starting to address sustainability and emission issues, including investments in cleaner fuels, hybrids, and some EV infrastructure. However, in terms of setting targets for zero-emission vehicles, they are not as aggressive as in other major EV markets. They seem to focus on diversification and environmental considerations.

- This is particularly true for oil and gas in the UAE. While climate commitments exist in the UAE, they are more geared towards overarching energy and climate frameworks, not specific automotive directives. This is good for ongoing use and service for ICE vehicles, including fuel feed pump needs.

- Commercial fleets, such as logistics, construction, and public transportation, continue to rely on fuel-powered vehicles. This also adds to the overall usage and demand for fuel feed pump services. Ongoing growth in tourism in the region also adds to the usage of larger ICE vehicles.

Automotive Fuel Feed Pumps Market Share

The top 7 companies in the automotive fuel feed pumps industry are Aisin, Continental, Delphi, Denso, Hitachi Astemo, Robert Bosch, TI Automotive contributing 53.8% of the market in 2025.

- Aisin makes fuel pumps and modules that move fuel from the tank to the engine. These work with many gasoline and diesel vehicles.

- Continental produces fuel pumps and delivery systems for internal combustion engines. Their products are durable, efficient, and designed for OEM use with modern fuel injection systems.

- Delphi supplies fuel pumps and modules that provide steady fuel flow and pressure. These are made for gasoline and diesel engines and are used in both OEM and aftermarket markets.

- Denso offers electric fuel pumps and in-tank modules. These ensure accurate fuel delivery and stable pressure for internal combustion and hybrid vehicles.

- Hitachi Astemo provides fuel feed units and high-pressure pumps. These are made for gasoline, diesel, and hybrid engines, focusing on durability and energy efficiency.

- Robert Bosch develops fuel pumps and in-tank modules. These manage fuel transfer and pressure control and are designed for OEM use with modern fuel injection systems.

- TI Automotive (TI Fluid Systems) makes fuel pumps and delivery modules. These are efficient, reliable, and work with many vehicle types and fuel types.

Automotive Fuel Feed Pumps Market Companies

Major players operating in the automotive fuel feed pumps industry are:

- Aisin

- Carter Fuel Systems

- Continental

- Delphi

- Denso

- Hitachi Astemo

- Magneti Marelli

- Robert Bosch

- TI Automotive (AVIC)

- Walbro

- Aisin uses its strong OEM connections and Japanese manufacturing skills to make reliable fuel feed pumps. These pumps work well for both traditional and hybrid vehicles.

- Continental offers fuel delivery systems with sensors and pressure controls. Their pumps are quiet, efficient, and customizable, meeting the needs of global OEMs for emission-compliant solutions.

- Delphi, now part of BorgWarner, has a strong presence in North America. They provide high-quality fuel feed pumps that are compatible with older systems and supported by a wide distribution network.

- Denso makes durable fuel feed pumps that work in tough conditions. They have strong partnerships with Japanese OEMs and focus on innovation for hybrid and advanced injection systems.

- Hitachi Astemo creates fuel systems and electric pumps with low electromagnetic interference. They use their experience and research to meet the needs of modern vehicles with complex electronics.

- Robert Bosch makes precise fuel feed pumps with strong vertical integration. Their pumps are emission-compliant and include features like diagnostics and fuel-efficiency improvements, making them popular with global OEMs.

- TI Automotive designs affordable and durable fuel feed systems for high-volume vehicles. They focus on emerging markets and create solutions that handle different fuel qualities well.

Automotive Fuel Feed Pumps Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 4.9 Billion |

| Market Size in 2026 | USD 5 Billion |

| Forecast Period 2026-2035 CAGR | 5.1% |

| Market Size in 2035 | USD 7.8 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Rising Global Vehicle Production & Sales | Increasing global vehicle production and sales fuels demand for reliable fuel feed pumps, driving market expansion and OEM adoption worldwide. |

| Stringent Emission Norms Driving Fuel Injection Technology Adoption | Tight emission regulations push adoption of advanced fuel injection systems, boosting demand for high-efficiency fuel feed pumps across gasoline and diesel vehicles. |

| Growing Aftermarket Demand Due to Aging Vehicle Fleet | Aging vehicles require frequent fuel pump replacements, fueling aftermarket demand and supporting sustained growth in global automotive fuel pump sales. |

| Technological Advancements in Electric Fuel Pump Systems | Innovations in electric fuel pumps enhance efficiency, durability, and performance, accelerating their adoption in modern vehicles and reshaping market dynamics. |

| Pitfalls & Challenges | Impact |

| Rapid Electrification of Automotive Industry | Shift toward EVs reduces reliance on conventional fuel pumps, restraining growth of traditional automotive fuel feed pump market segments. |

| High Cost of Advanced High-Pressure Fuel Pumps | Elevated costs of high-pressure fuel pumps limit adoption, especially in price-sensitive markets, slowing overall market growth despite technological advantages. |

| Opportunities: | Impact |

| Expansion in Emerging Markets with Growing Vehicle Ownership | Rising vehicle ownership in emerging economies presents significant growth potential for fuel feed pump manufacturers and aftermarket service providers. |

| Development of Multi-Fuel Compatible Pump Systems | Multi-fuel compatible pumps enable OEMs to address diverse fuel types, offering growth opportunities in regions with varying fuel availability. |

| Aftermarket Growth in Developed Markets | Mature automotive markets drive aftermarket demand for fuel pump replacements, creating opportunities for suppliers to expand service networks and sales channels. |

| Market Leaders (2025) | |

| Market Leader |

16.1% market share |

| Top Players |

Collective market share in 2025 is 47.5% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest growing market | North America |

| Emerging countries | South Korea, India, Brazil |

| Future outlook |

|

What are the growth opportunities in this market?

Automotive Fuel Feed Pumps Industry News

In December 2025, Stanadyne introduced its new GX Series of gasoline direct injection (GDI) performance fuel pumps. These pumps are an upgrade of the company’s high-flow, high-pressure technology for racing and street use. Unlike modified OE service pumps, the GX Series is designed to handle high flow and pressure safely. It is built to withstand the heavy loads and stresses from modern engines producing more power than stock engines.

In September 2024, BMW announced plans to sell hydrogen-powered cars by 2028. This shows BMW’s support for hydrogen fuel cells as an alternative to electric batteries. Hydrogen-powered cars will need special fuel delivery components, which could change fuel feed pump requirements.

The automotive fuel feed pumps market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) and volume (thousand units) from 2022 to 2035, for the following segments:

Market, By Pump

- Mechanical fuel pump

- Electric fuel pump

- In-tank electric pumps

- In-line electric pumps

- Turbo pump

Market, By Pressure

- Low pressure pump

- High-pressure pump

Market, By Vehicle

- Passenger cars

- Hatchback

- Sedan

- SUV

- Commercial vehicles

- Light commercial vehicles (LCV)

- Medium commercial vehicles (MCV)

- Heavy commercial vehicles (HCV)

Market, By Fuel

- Gasoline/Petrol

- Diesel

- Alternative fuels

Market, By Sales Channel

- OEM

- Aftermarket

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Poland

- Netherlands

- Norway

- Asia Pacific

- China

- India

- Japan

- South Korea

- Australia

- Singapore

- Malaysia

- Vietnam

- Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- MEA

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

What is the market size of the global automotive fuel feed pumps in 2025?

The market size was USD 4.9 billion in 2025, with a CAGR of 5.1% expected through 2035, driven by sustained ICE vehicle production and rising demand in emerging economies.

What is the projected value of the global automotive fuel feed pumps industry by 2035?

The market is expected to reach USD 7.8 billion by 2035, fueled by rising vehicle production, aftermarket demand, and advancements in high-pressure and electric fuel pump technologies.

What is the current automotive fuel feed pumps industry size in 2026?

The market size is projected to reach USD 5 billion in 2026, registering a CAGR of 5.1% over the forecast period from 2026 to 2035.

How much revenue did the electric fuel pump segment generate in 2025?

The electric fuel pump segment dominated the market with a 54.8% share, generating approximately USD 2.7 billion in 2025. Its dominance is driven by consistent fuel pressure delivery, compatibility with modern fuel injection systems, and strong OEM and aftermarket demand.

What was the market share of the OEM sales channel in 2025?

The OEM segment accounted for 67.4% of the market in 2025, valued at around USD 3.3 billion. OEM dominance is driven by direct integration of fuel feed pumps into new vehicle production and compliance with stringent emission regulations such as Euro 6/VI and CAFE standards.

What is the growth outlook for the high-pressure pump segment from 2026 to 2035?

The high-pressure pump segment is expected to grow at a CAGR of 6.1% from 2026 to 2035, driven by rising adoption of direct injection engines and turbocharged ICEs requiring precise fuel supply and efficient combustion to meet global emission regulations.

Which region leads the automotive fuel feed pumps market?

The US automotive fuel feed pumps market reached USD 820.7 million in 2025 and growing at a CAGR of 6.1% between 2026 and 2035.

What are the key trends shaping the automotive fuel feed pumps market?

Key trends include increasing use of lightweight materials like aluminum alloys in pump components, and continued ICE dominance in Southeast Asia, Latin America, and Africa due to affordability and limited EV infrastructure.

Who are the key players in the automotive fuel feed pumps market?

Key players include Aisin, Carter Fuel Systems, Continental, Delphi, Denso, Hitachi Astemo, Magneti Marelli, Robert Bosch, TI Automotive, and Walbro.

Automotive Fuel Feed Pumps Market Scope

Related Reports