Summary

Table of Content

Automotive Control Cables Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Automotive Control Cables Market Size

The rise of the market can be attributed to the growth in production numbers and replacement of cables. In 2024, over 92.5 million passenger and commercial vehicles were produced, resulting in a steady OEM demand for brake, throttle and clutch cables from all manufacturing regions.

Automotive Control Cables Market Key Takeaways

Market Size & Growth

- 2025 Market Size: USD 5.1 Billion

- 2026 Market Size: USD 5.3 Billion

- 2035 Forecast Market Size: USD 7.6 Billion

- CAGR (2026–2035): 4.1%

Regional Dominance

- Largest Market: Asia Pacific

- Fastest Growing Region: Asia Pacific

Key Market Drivers

- Rising global vehicle parc.

- Sustained demand for mechanical systems.

- Increasing average vehicle age.

- Growth in emerging automotive markets.

Challenges

- Shift toward electronic actuation systems.

- Price sensitivity in aftermarket.

Opportunity

- Rising electric vehicle production.

- Expansion of organized aftermarket.

- Localization of component manufacturing.

Key Players

- Market Leader: Hi-Lex led with over 19.6% market share in 2025.

- Leading Players: Top 5 players in this market include Dura, Ficosa, Hi-Lex, Minda, Suprajit, which collectively held a market share of 44.8% in 2025.

Get Market Insights & Growth Opportunities

The average age of vehicles in the USA is increasing, creating need for control cables due to the high rate of failure from wear and tear. The average age of a vehicle in 2023 was twelve and a half years consequently, there will be a higher number of vehicles needing replacement of clutch, accelerator and parking brake cables.

The auto industry continues to have requirement imposed by government regulations to maintain safety by requiring to use control cables to operate manual transmission; approximately 30% of all vehicles on the road are still manual; therefore, the demand for clutch and gear control cables will be steady through demand for all vehicles.

The demand for control cables is not decreasing due to the trend toward 'electrifying,' because although EVs do not have cables to operate their vehicles, they still use cables to operate the parking brake, hood and seat.

In 2023, global sales of EVs exceeded 14 million vehicles therefore, there continues to be a substantial increase in demand for control cable assemblies, even though they typically use more electronics than other vehicles.

The Asia Pacific region is expected to continue leading in automotive control cables because of a higher concentration of manufacturing of vehicles and the size of the existing installed base of vehicles. The production of vehicles in China reached over 30 million in 2024, creating high OEM demand, and with the high density of the number of vehicles in the global market today, the demand for aftermarket continues to be strong.

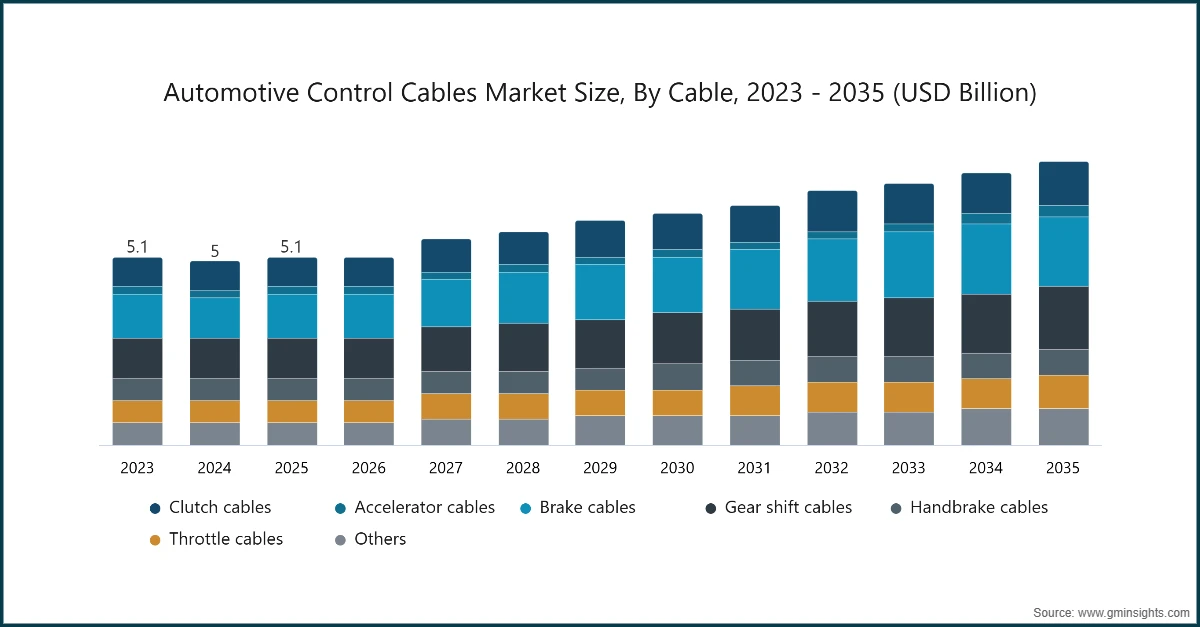

The global automotive control cables market was estimated at USD 5.1 billion in 2025. The market is expected to grow from USD 5.3 billion in 2026 to USD 7.6 billion in 2035, at a CAGR of 4.1% according to latest report published by Global Market Insights Inc.

To get key market trends

Automotive Control Cables Market Trends

The increasing age of vehicles will continue to shape what automotive control cables are replacing. In 2023, the worldwide average vehicle age exceeded twelve years therefore, the failure rates of automotive control cables have been increasing. As a result, replacement parts have accounted for approximately forty percent of the total volume of automotive control cables sold in mature automotive markets.

Even though there is a growing trend toward electronic/automatic transmissions and vehicles that utilize electronic controls have been increasingly used, manual transmissions are still widely utilized. In fact, manual vehicles still comprise almost thirty percent of all vehicles produced worldwide in 2024 and therefore, continue to support stable demand for clutch and gear cables across the passenger and light duty vehicle segments worldwide.

The increase in production of electric powered vehicles is changing the design priorities of the cable industry; this will not reduce the total volume of the cables sold. More than fourteen million electric powered vehicles were sold globally in 2023; this has created an ongoing need for parking brake cables and seat adjustment cables manufactured specifically for use in electric powered vehicles.

OEMs continue to move toward using lightweight materials in their vehicles and this is having an impact on development of control cables. Materials such as aluminum and polymer sheathing will lower the total weight of a vehicle and will help OEMs to meet their efficiency targets. Furthermore, the continued growth in the number of manufacturers adopting lightweight components is contributing to vehicle weight reduction programs of one to two percent across all global platforms in 2024.

In 2024, manufacturers will continue to expand regional/local production capabilities in order to lessen overall production costs and reduce supply chain risks. In 2024, nearly fifty percent of the global production of motor vehicles will occur in the Asia-Pacific region and this will result in regional sourcing of control cables thereby strengthening supplier integration between OEMs and their respective manufacturing facilities around the world.

Automotive Control Cables Market Analysis

Learn more about the key segments shaping this market

Based on cable, the automotive control cables market is segmented into clutch cables, accelerator cables, brake cables, gear shift cables, handbrake cables, throttle cables, and others. The brake cables segment dominates the market with 23.3% share in 2025, and the segment is expected to grow at a CAGR of 5% from 2026 to 2035.

- Brake cables account for over thirty percent of total control cable demand in 2025 driven by mandatory safety regulations and frequent wear replacement across passenger and commercial vehicles globally.

- Clutch cable sales will continue to grow primarily from the large penetration of vehicles using manual transmissions. As of 2024, nearly one-third of all vehicles in the world will be manual vehicles. Consequently, a steady amount of clutch cables will be used in installing clutch cables in both passenger vehicles and light commercial vehicles.

- Accelerator cables and throttle cables will continue to see strong demand even though almost all new vehicles now use electronic throttles. Mechanical systems (cables) for accelerating vehicles will still be found on most price-sensitive vehicles made in Asia and Latin America.

- Gear shift cables will continue to distinguish themselves as there will be more automatic and semi-automatic vehicles on the roads. Growth in the manufacturing of small vehicles will ensure a stable number of gear shift cables will be required, particularly in high-volume manufacturing countries such as China and India.

- Handbrake cables will see a great deal of volume from both gas-powered vehicles and electric vehicles. Although EVs are using mechanically operated parking brake cables, it is estimated that at least 14 million EVs will be sold around the world in 2023.

- All control cables that are not classified above (hood release cables, seat adjustment cables, etc.) will see incremental volumes generated from an increase in vehicle content and an increasing amount of vehicles being produced.

Learn more about the key segments shaping this market

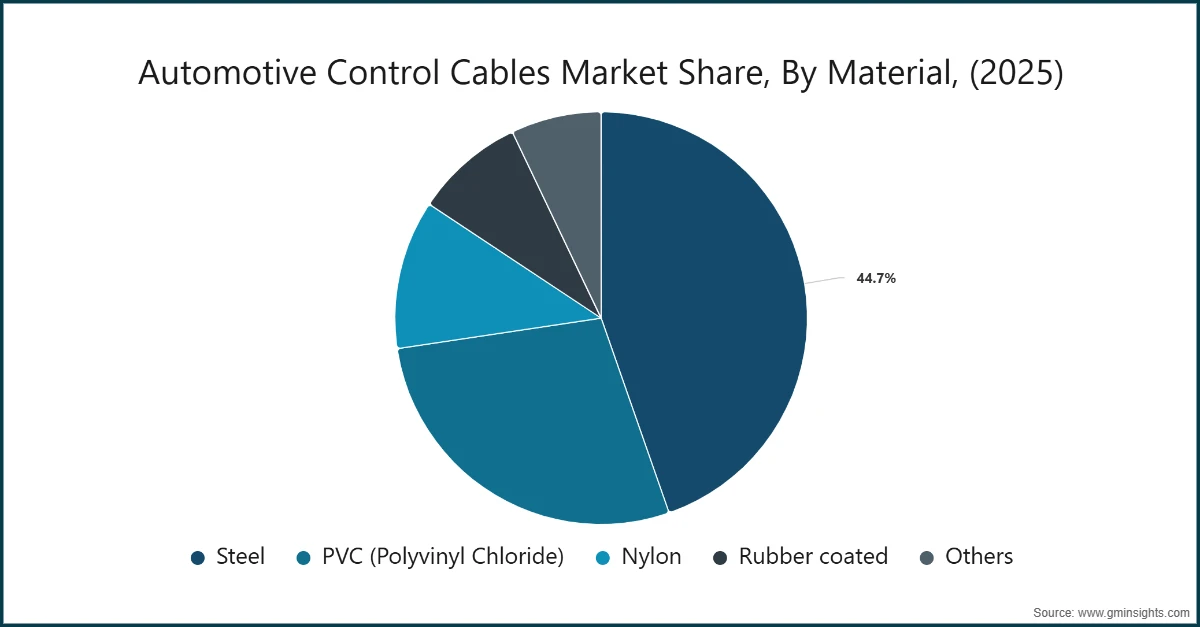

Based on material, the automotive control cables market is divided into steel, PVC polyvinyl chloride, nylon, rubber coated, and others. The steel segment dominates with 44.6% market share in 2025 and is growing at a CAGR of 3.7% from 2026 to 2035.

- Cables made with steel are preferable in applications that have to use a clutch brake or handbrake that require significant tensile strength and load-bearing capability to ensure consistent operation of the vehicle throughout its life cycle. Due to their proven reliability in all types of operating conditions, OEMs continue to choose steel cables for the mass production of vehicles.

- Cables that have a coating of PVC (Polyvinyl Chloride) are very popular among manufacturers to improve the integrity of electrical components by offering insulation and resistance to corrosion. The use of PVC coatings lends itself to smoother operation and a longer service life in damp or dust-filled conditions.

- Nylon is becoming more popular with manufacturers looking to reduce the weight of their cable assemblies. By offering a low coefficient of friction, nylon cables provide smoother operation and less wear and tear on accelerator cables and gear shift cable designs.

- Cables made with rubber coatings provide exceptional vibration damping and noise absorption properties, creating more comfortable driving experience and protecting the cable assembly from external abrasions.

- Cables made with other materials, such as composite coatings or specialty polymers, provide solutions for more specialized applications where enhanced flexibility and thermal resistance, and/or cost savings associated with one type of vehicle platform.

Based on vehicle, the automotive control cables market is segmented into passenger vehicles, commercial vehicles, and two wheelers. The passenger vehicles segment dominates with 58.4% market share in 2025.|

- Passenger vehicle global production is more than 70 million units per year, which means that passenger cars have the largest market share due to the widespread use of clutch, accelerator, brake, and handbrake cables in mass-market vehicles.

- Demand for commercial vehicles will continue to be stable because end users need very durable products. Due to the frequent usage rates and the heavier loads carried by vehicles, brake and clutch cables will need to be replaced on a regular basis in the light-duty and medium-duty fleets.

- Consistent demand exists for throttle, brake, and clutch cables in two-wheeled vehicles. A large installed base combined with relatively short replacement cycles will create a significant aftermarket demand in regions such as India and Southeast Asia.

- The use of control cables will continue to be important to both internal combustion engine (ICE) and electric vehicles. The increased use of electric vehicles will not mean the end of mechanical cables; rather, mechanical cables will still be used to support the functions of parking brakes, throttles, and seats across multiple vehicle categories.

Based on application, the automotive control cables market is divided into engine control, transmission control, braking system, HVAC system, and others. braking system dominates with 26.1% market share in 2025.

- There is a consistent demand for brake cables due to the fact that they facilitate safe parking and emergency braking on all types of passengers, commercial, and two-wheeler vehicles, regardless of their drivetrain configuration.

- As far as engine control applications are concerned, accelerator and throttle cables are used extensively in all types of mechanical actuation systems including those found in vehicles. The very low pricing of these products makes them highly sought after within emerging markets and in lower-cost vehicles, and as such, their demand continues to be very strong, especially with the slower implementation of electronic throttle applications.

- Transmission control cables support clutch actuation and gear changes in both manual and automated manual transmission systems. The presence of so many manual transmission vehicles in existence ensures an ongoing demand for transmission-related cables for the foreseeable future.

- HVAC system control cables are used for controlling air flow and temperature in lower tier level vehicles. In addition to their use in OEM's lower tier vehicles, mechanical HVAC controls are also widely used because of the emphasis placed on cost reduction and reliability by OEM's.

- Other applications where cables are used include hood release cables, seat adjustment cables, and fuel lid release cables. The increased number of features added to vehicles and the growth in the global vehicle parc will continue to result in increased demand for the above applications.

Looking for region specific data?

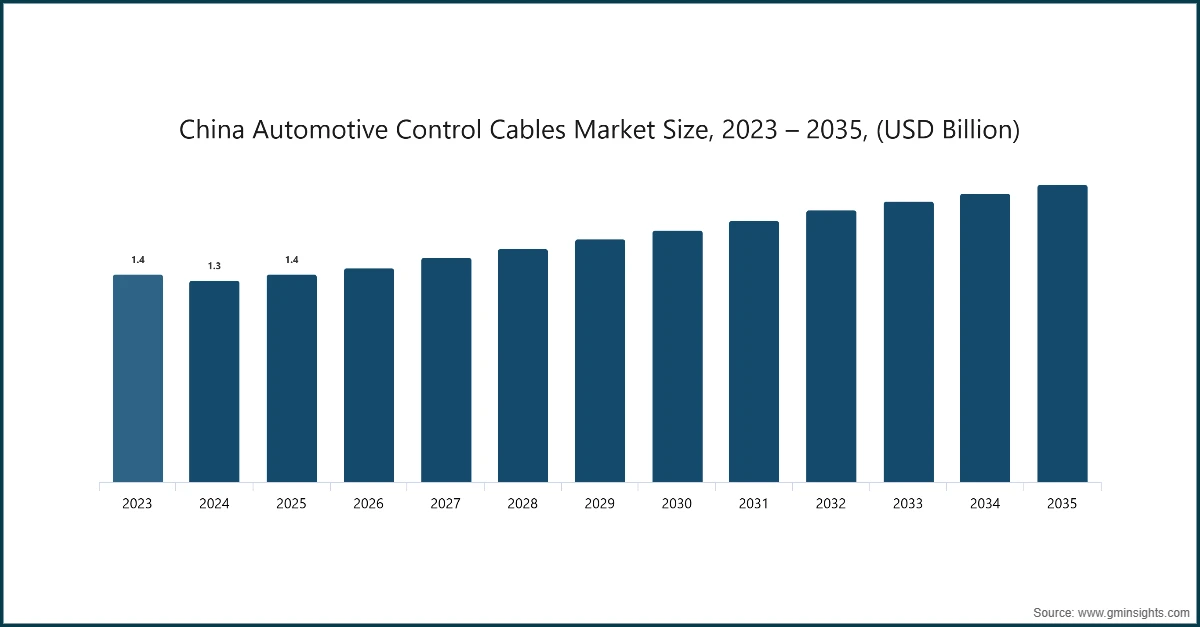

China dominates the Asia Pacific automotive control cables market accounting for 53% and generating USD 1.4 billion in 2025.

- China represents a critical market for automotive control cables driven by large scale vehicle manufacturing and a vast installed vehicle base. High production volumes across passenger vehicles commercial vehicles and two wheelers ensure steady OEM demand for control cable systems.

- The volume of vehicles produced each year (by passenger cars, commercial vehicles, and two wheeled vehicles) creates a constant need for OEM (Original Equipment Manufacturer) supplied control cable systems.

- The frequently used vehicles in urban and semi urban areas create a large volume of replacement parts, as brake, clutch, and throttle cables have been used in a high amount of stop and go driving, thus creating high levels of aftermarket usage through overall vehicle usage.

- The industry has a large amount of cost based domestic productions, so they keep mechanical control systems for clutch control, acceleration control, shift control, and hand brake control, thus establishing a relatively continued demand for control cables, especially in the large buying segments and entry-level segments.

- Electric vehicle acceptance in China is changing the overall make up of the applications being made; however, cables used for parking brakes, hood release systems, and seat positioning will still be used in electric vehicle platforms, so those sales numbers should still be very stable.

- Competitive sourcing and vertically integrated manufacturing are part of the competitive environment in this sector and allow local suppliers to benefit through proximity of their plants, shorter supply chains, and greater overall cost efficiencies, which should support the long-term stability of the Chinese automotive market and the markets for their products.

US dominates North America automotive control cables market growing with a CAGR of 3% from 2026 to 2035.

- One of the primary factors driving the US controls cables market is the size of the aging vehicle fleet, resulting in a strong aftermarket demand for replacement of worn clutch brake and throttle cables across both passenger and light commercial vehicles.

- Passenger vehicle sales generate the majority of demand due to high levels of vehicle ownership, as well as mechanical control systems being utilized in mass-market models. There is also substantial demand for pickup and light duty trucks through the applications of handbrake and brake cables.

- OEM sales have remained consistent due to both domestically manufactured vehicles and localized assembly operations. Control cables are expected to be used in many types of equipment within hybrid and electric vehicles for parking brake and other auxiliary operations as well.

- Aftermarket distribution is highly organized, providing numerous branded suppliers and service networks. This structure supports both consistent quality standards and repeat purchases at independent service centers and authorized repair facilities.

Germany dominates the Europe automotive control cables market, showcasing strong growth potential, with a CAGR of 2.9% from 2026 to 2035.

- In Germany, automotive control cables are produced from a highly advanced and technologically sophisticated production base, combined with a wealth of manufacturing capacity and a broad market that includes a vast number of automobiles or light trucks. In addition, the continuing market for high quality control cable systems is driven by the demand for premium cars and commercial fleets from original equipment manufacturers (OEMs) and aftermarket suppliers.

- New developments in vehicle design that are driven by engineering principles continue to increase the longevity of the most frequently utilized control cables, including durable and precise clutch control cables, brake control cables, gear shift control cables and hand brake control cables. As a result of increased performance requirements from control cable users, manufacturers are producing control cables that have greater longevity and reliability.

- In addition, the ongoing growth in the aftermarket is supported by the long term ownership of passenger vehicles and commercial trucks and a strong maintenance culture. Therefore, the continued use of control cables will exist for some time amongst the majority of automobiles and commercial vehicles, as a result of the use of preventative maintenance practices and regular service intervals.

- Although electrification and hybrids are expected to influence the mix of applications using control cables, they will not influence the total number of applications. Critical examples of applications for control cables in hybrid and electric vehicles are hood release cables for parking brakes and seat adjustment cables.

- The automotive control cables market in Germany is characterized by a competitive landscape that is populated by regional suppliers and large multinational companies. The creation of quality standards and a cooperative relationship with OEMs will help ensure that the automotive control cable market in Germany remains viable over the long term with stable prices.

Brazil leads the Latin American automotive control cables market, exhibiting remarkable growth of 3.3% during the forecast period of 2026 to 2035.

- In Latin America, Brazil is the largest automotive control cable market due to its large vehicle parc and demand for cost-effective platforms. Control cable consumption is dominated by passenger cars and light trucks. The average age of vehicles is relatively old and most vehicles are used intensively which generates demand for replacements. Since brake, clutch and throttle cables have a high level of wear, independent repair facilities and local distributors have excellent aftermarket sales.

- There is still a large demand for clutch and gear shift cables because manual transmissions are still prevalent in Brazil. The cost sensitivity of vehicle segments leads many consumers to choose mechanical control over electronic controls. Additionally, many of these same consumers will also select non-electronic controls in order to save money on parts.

- OEMs purchase Control Cables from manufacturers located in Brazil due to the close proximity to the assembly facilities as well as decreased transportation costs.

- Two-wheelers account for a portion of the overall demand for brake and throttle cables and two-wheelers may make a larger contribution to the overall demand for throttle and brake cables in urban and semi-urban regions of Brazil.

UAE witnessed substantial growth in the Middle East and Africa automotive control cables market in 2025.

- Due to the numerous vehicles registered within the UAE and the high number of registered passenger vehicles compared to the limited number of new vehicle imports entering the country's market, the market for automotive control cables is only growing at a moderate pace. Most demand would be generated through repair and not new vehicle sales, because vehicles are maintained using the aftermarket or repair channel.

- Cable wear is exacerbated by the harsh UAE weather conditions (heat and dust). As a result, brake, clutch, and throttle cables typically have short replacement life cycles and generate ongoing aftermarket demand for these parts.

- Control cable consumption is predominantly for passenger cars, however, there will also be a sizable amount of usage within the logistics, construction and service industries from commercial vehicles (trucks, vans, and/or trailers).

- While EV adoption will not reduce demand for the automotive control cable market, the composition of what types of cables are required for each application regionally will change. (i.e. parking brake, hood release and seat adjust cables used in a EV.)

- Aftermarket distribution channels are primarily found within organized service centers and independent repair facilities. A significant amount of demand is attributed to the high customer preference for reliable and long-lasting automotive control cables across all three channels.

Automotive Control Cables Market Share

- The top 7 companies in the automotive control cables industry are Hi Lex, Suprajit, Minda, Dura, Ficosa, Küster and TSC, contributed around 44% of the market in 2025.

- Hi Lex is a top manufacturer of Automotive Control Cables with a substantial presence in Asia Europe and North America. They utilize various advanced Manufacturing Processes and have long-established relationships with Automotive OEM’s to provide High Precision Clutch Brake Shift Control Systems.

- Suprajit is one of the leading Global Manufacturing companies in India, specializing in multiple products including Clutch Accelerator Brake and Parking Brake Cables. They have an extensive Manufacturing Footprint, strong aftermarket sales capabilities and a large diverse customer base that makes them the market leader by Volume.|

- Minda specializes in Control Cables and other products that are Economically Feasible to produce and they maintain Localized Manufacturing and an Extensive Distribution Network for their products. They are well Established in Emerging Markets and have a Strong Relationship with Mass Market Vehicle Manufacturers (OEM’s).

- Dura is one of the leaders in providing Integrated Control Systems & Cable Assemblies to OEM’s, Globally. They have a Skilled Engineering Team and are known for their Engineering Capability and the Integration of various products at the System Level within the Transmission and brake System Area.

- Ficosa’s Control Cable Product line is one of the components in their Overall Automotive Systems Product line. They have a strong design team and Global Manufacturing Capability to support many different Vehicle Architectures and Regional Requirements.

- Küster products are recognized for their precision-engineered controls that focus on durability and quality. The products are customized to meet strict standards for specific purpose by providing cable solutions to premium and mid-grade vehicles.

- TSC focuses on the supply of mechanical control cables and has inherent capabilities in flexible manufacturing and cost effectiveness. The Company's ability to service the OEM and aftermarket has created consistent demand for TSC's solutions in a variety of vehicle types.

Automotive Control Cables Market Companies

Major players operating in the automotive control cables industry are:

- Atsumitec

- Chuo Spring

- Dura Automotive Systems

- Ficosa International

- Grand Rapids Controls

- Hi-Lex

- Küster

- Minda

- Suprajit Engineering

- TSC

- Automotive Control Cable Market is assisted by the ongoing production of automobiles and a vast vehicle parc requiring continuous replacement of these mechanical control components. Control cables are still an important part of clutch braking throttle and auxiliary functions thereby creating stable continuous demand for OEMs and aftermarket, both in passenger commercial and two-wheeled vehicles.

- Factors affecting the Automotive Control Cable market include aging vehicle fleet, presence of cost-competitive platforms, and continued use of mechanical systems in certain areas. Even with the introduction of electronic actuation, control cables will continue to remain relevant because they will continue to be used on electric and hybrid vehicles creating sustained future demand and maintaining balanced growth within the market.

Automotive Control Cables Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2025 |

| Market Size in 2025 | USD 5.1 Billion |

| Market Size in 2026 | USD 5.3 Billion |

| Forecast Period 2026-2035 CAGR | 4.1% |

| Market Size in 2035 | USD 7.6 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Rising global vehicle parc | Growing passenger and commercial vehicle population increases replacement demand for clutch throttle and brake control cables. |

| Sustained demand for mechanical systems | Continued use of manual transmissions and mechanical actuation supports stable OEM and aftermarket demand. |

| Increasing average vehicle age | Older vehicles require frequent replacement of worn control cables, strengthening aftermarket sales volumes. |

| Growth in emerging automotive markets | Expanding vehicle production in Asia Pacific and Latin America drives higher control cable installations. |

| Pitfalls & Challenges | Impact |

| Shift toward electronic actuation systems | Increasing adoption of electronic throttle and shift by wire systems limits long term demand for certain cable types. |

| Price sensitivity in aftermarket | Intense competition and low differentiation pressure margins for control cable manufacturers. |

| Opportunities: | Impact |

| Rising electric vehicle production | Electric vehicles continue to use parking brake hood and seat control cables, creating new volume opportunities. |

| Expansion of organized aftermarket | Growth of branded service networks improves penetration of standardized high quality control cables. |

| Localization of component manufacturing | OEM focus on localized sourcing benefits regional control cable suppliers. |

| Market Leaders (2025) | |

| Market Leader |

19.6% Market Share |

| Top Players |

Collective Market Share is 44.8% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | Asia Pacific |

| Fastest growing market | Asia Pacific |

| Emerging countries | India, Vietnam, Brazil, Thailand |

| Future outlook |

|

What are the growth opportunities in this market?

Automotive Control Cables Industry News

- In December 2025, Ficosa International announced it had surpassed the industrial milestone of manufacturing 30 million cameras since the inception of its vision business, reporting a record daily production rate of 33,000 units in fiscal year 2024 to support the surge in demand for ADAS and autonomous driving solutions.

- In December 2025, Thai Steel Cable Public Company Limited (TSC) was honored as a "Regional Supplier Quality Award Finalist 2025" in the Body Category and achieved an upgrade to an 'AA' level in the SET ESG Ratings, reflecting its operational excellence in the Southeast Asian supply chain.

- In November 2025, Suprajit Engineering entered into a strategic investment agreement with Blubrake, an Italian technology firm, to collaborate on the development and manufacturing of advanced Anti-Lock Braking Systems (ABS) tailored for e-mobility applications, further diversifying its braking division.

- In June 2025, Minda Corporation signed a Joint Venture agreement with Japan’s Toyodenso Co. Ltd. to manufacture advanced automotive switches and systems in India, aiming to leverage Toyodenso's technology for the growing two-wheeler and passenger vehicle markets in the ASEAN region.

- In May 2025, Suprajit Engineering completed the second tranche of its acquisition of Stahlschmidt Cable Systems (SCS), formally integrating the assets of SCS China and SCS Canada into its global fold, thereby securing critical manufacturing hubs for its light-duty cable division in North America and Asia.

- In January 2025, Hi-Lex inaugurated a new manufacturing facility in Derramadero, Coahuila (Mexico) with an investment of US$15 million, designed to produce window regulators, door modules, and mechanical control cables to meet the increasing localization requirements of North American OEMs.

The automotive control cables market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue (USD Mn) and volume (Units) from 2022 to 2035, for the following segments:

Market, By Cable

- Clutch cables

- Accelerator cables

- Brake cables

- Gear shift cables

- Handbrake cables

- Throttle cables

- Others

Market, By Material

- Steel

- PVC (Polyvinyl Chloride)

- Nylon

- Rubber coated

- Others

Market, By Vehicle

- Passenger vehicles

- Hatchback

- Sedan

- SUV

- Commercial vehicles

- Light Commercial Vehicles (LCV)

- Medium Commercial Vehicles (MCV)

- Heavy Commercial Vehicles (HCV)

- Two-wheelers

Market, By Application

- Engine control

- Transmission control

- Braking system

- HVAC system

- Others

Market, By Sales Channel

- OEM

- Aftermarket

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Norway

- Netherlands

- Sweden

- Asia Pacific

- China

- India

- Japan

- Australia

- South Korea

- Singapore

- Thailand

- Indonesia

- Vietnam

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- Saudi Arabia

- UAE

- Turkey

Frequently Asked Question(FAQ) :

What was the market size of the automotive control cables in 2025?

The market size was USD 5.1 billion in 2025, with a CAGR of 4.1% expected through 2035. Growth in production numbers and cable replacements are driving the market.

What is the projected value of the automotive control cables market by 2035?

The market is poised to reach USD 7.6 billion by 2035, driven by increasing vehicle production and demand for replacement cables.

What is the expected size of the automotive control cables industry in 2026?

The market size is projected to reach USD 5.3 billion in 2026.

How much revenue did the brake cables segment generate in 2025?

The brake cables segment accounted for 23.3% of the market share in 2025 and is expected to grow at a CAGR of 5% till 2035.

What was the valuation of the steel segment in 2025?

The steel segment held a 44.6% market share in 2025 and is set to expand at a CAGR of 3.7% up to 2035.

What is the growth outlook for the passenger vehicles segment?

The passenger vehicles segment dominated with a 58.4% market share in 2025.

Which region leads the automotive control cables industry?

China leads the Asia-Pacific market, accounting for 53% of the regional share and generating USD 1.4 billion in 2025. High production volumes across passenger vehicles, commercial vehicles, and two-wheelers drive steady OEM demand.

What are the upcoming trends in the automotive control cables market?

Trends include growing use of lightweight materials, expansion of regional production to strengthen supply chains, and rising demand for EV-specific cables such as parking brake and seat adjustment systems.

Who are the key players in the automotive control cables industry?

Key players include Atsumitec, Chuo Spring, Dura Automotive Systems, Ficosa International, Grand Rapids Controls, Hi-Lex, Küster, Minda, Suprajit Engineering, and TSC.

Automotive Control Cables Market Scope

Related Reports