Summary

Table of Content

Automotive AI Processors Market

Get a free sample of this report

Form submitted successfully!

Error submitting form. Please try again.

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Request Sectional Data

Thank you!

Your inquiry has been received. Our team will reach out to you with the required details via email. To ensure that you don't miss their response, kindly remember to check your spam folder as well!

Form submitted successfully!

Error submitting form. Please try again.

Automotive AI Processors Market Size

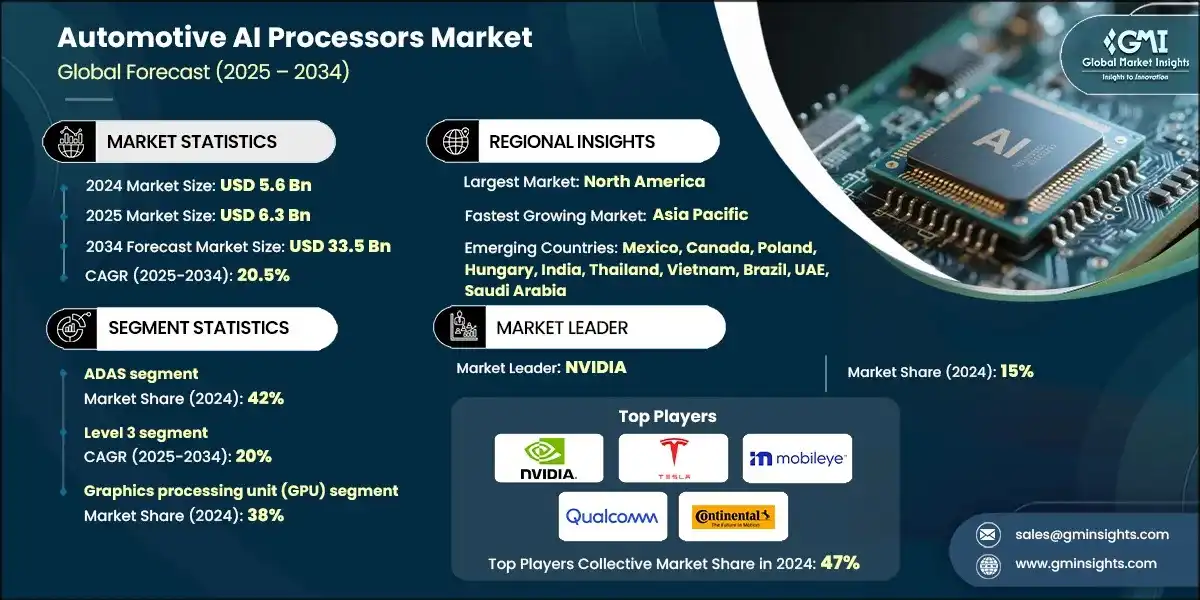

The global automotive AI processors market size was valued at USD 5.6 billion in 2024. The market is expected to grow from USD 6.3 billion in 2025 to USD 33.5 billion in 2034 at a CAGR of 20.5%, according to latest report published by Global Market Insights Inc.

Automotive AI Processors Market Key Takeaways

Market Size & Growth

- 2024 Market Size: USD 5.6 Billion

- 2025 Market Size: USD 6.3 Billion

- 2034 Forecast Market Size: USD 33.5 Billion

- CAGR (2025–2034): 20.5%

Regional Dominance

- Largest Market: North America

- Fastest Growing Region: Asia Pacific

Key Market Drivers

- Growing adoption of ADAS and autonomous driving.

- Rise in connected and electric vehicles.

- Edge AI and on-vehicle data processing.

- OEM and semiconductor collaboration.

Challenges

- High development and integration cost.

- Limited standardization and interoperability.

Opportunity

- Emergence of software-defined vehicles (SDVs).

- Expanding EV production In Asia-Pacific.

- AI-based predictive maintenance & fleet management.

- Development of automotive-specific AI toolchains.

Key Players

- Market Leader: NVIDIA led with over 15% market share in 2024.

- Leading Players: Top 5 players in this market include NVIDIA, Tesla, Mobileye (Intel), Qualcomm, Continental, which collectively held a market share of 47% in 2024.

Get Market Insights & Growth Opportunities

AI processors perform the real-time-speed computing for advanced driver-assistance systems (ADAS), autonomous driving, predictive maintenance, and in-vehicle infotainment systems. Combining power efficiency with high-performance processing, automotive AI processors ensure low latency and real-time decision-making which impact vehicle safety and automation.

As automakers scale the deployment of AI and machine learning (ML), the need for processors supporting large-scale data training and inferencing is expanding. Most advanced chipmakers have invested resources to enable developers with automotive-grade SDKs, AI tool chains, and certification programs that assist OEM and Tier-1 suppliers in designing and developing systems that work with AI. Examples include the NVIDIA Drive Developer Program and Qualcomm's AI Engine Toolkit that empower automotive engineers to accelerate ADAS and cockpit AI application development.

The growing use of connected and electric vehicles is fueling demand for AI processors which are capable of real-time data including sensors, cameras, and LiDAR. These processors are embedded into hybrid on-vehicle and cloud AI architectures that provide compliance, scalability, and increased vehicle intelligence. Hybrid architectures appeal especially to verticals like logistics and public transportation, where AI optimization for the entire fleet is a requirement for safety compliance.

Self-learning algorithms, over-the-air (OTA) model updates, and no-code AI configuration toolkits are also opening the usage to a richer set of teams beyond the core engineering teams. This democratization allows automotive OEM and suppliers to make use of AI across the departments, from predictive maintenance to user experience design, expanding the adoption within the ecosystem.

The North American market is the market leader based on its rich autonomous vehicle ecosystem, large share of AI chip suppliers and strong R&D spending by the OEM and chip suppliers. Asia Pacific is anticipated to be the fastest growing market due to national initiatives for smart mobility, increase in EV manufacturing and government supported AI innovation in China, Japan, South Korea and India. Emerging markets are exhibiting larger development due to increasing vehicle safety regulations as they adopt AI enabled safety and assisted driving systems.

To get key market trends

Automotive AI Processors Market Trends

The integration of AI/ML and generative AI into automotive systems is transforming automakers approach towards vehicle intelligence and data-driven decision-making. OEM are increasingly leveraging processors that are optimized for the on-vehicle model training, edge inference and neural network acceleration. This shift is fueled by the pursuit of AI-driven cockpit experiences (e.g., more immersive cockpit or interaction experience), autonomous driving (or varying levels of automation), and preventative maintenance. Major vendors like NVIDIA or Qualcomm are providing generative AI capabilities for real-time interpretation of driving scenes, predicting driver's intentions and personalization of in-vehicle infotainment, thus, changing the occupants' experience inside vehicles.

The use of domain-specific AI processor architectures is becoming more commonplace, with designs tailored to specific vehicle segments such as ADAS, EVs, and autonomous fleets. This trend emerged as automakers demanded processors that balance functional safety (ISO 26262) and low-power, high-efficiency performance. Mobileye and Tesla are continuously pushing for and have gained market-share by leveraging an automotive AI chip designed for that specific, and market-driven use-case in vehicles. Each vendor introduces differentiation in vehicles classes and provides OEM an easier alignment of hardware towards the use-case specific AI workloads, thus a disruption of the previous notion 'one chip to rule them all.'

The developer and certification ecosystems are beginning to serve as competitive differentiators as semiconductor companies offer training and toolkits to simplify automotive AI deployment. NVIDIA's Drive Developer Program and Qualcomm's AI Engine SDK are examples of structured learning pathways to address the complication of deploying AI in vehicle platforms. Taking together, the potentiality of workforce enablement and ecosystem maturation is progressing in a way that, eventually, will help automakers scale from pilots to production, with long-term vendor loyalty.

Hybrid and centralized computing architectures are reshaping vehicle design paradigms as AI processors are shifting to become the primary processor support zonal and centralized E/E architectures, propelled by the demand for real data fusion, software-defined vehicle platforms, and multi-domain processing within a single control unit. As automotive manufacturers see the need for scalable AI computing frameworks, this architecture trend is expected to dominate through 2027–2028, especially among global OEM targeting L3+ autonomy and connected vehicle ecosystems.

Automotive AI Processors Market Analysis

")

Learn more about the key segments shaping this market

Based on processor, the automotive AI processors market is divided into graphics processing unit (GPU), central processing unit (CPU), application-specific integrated circuit (ASIC), field programmable gate array (FPGA), system on chip (SoC). The graphics processing unit (GPU), segment dominated the market with 38% share, due to its superior parallel processing capabilities, enabling rapid computation for perception, sensor fusion, and autonomous navigation.

- OEM are increasingly utilizing GPU-based AI processors to faster deep learning, computer vision and autonomous navigation workloads. This is primarily the result of the need for parallel processing capability interpreting data streams coming from a multitude of sensors, while allowing for real-time decision making in autonomous driving systems. GPUs are required to obtain higher model accuracy, speed up inferencing times and decrease time-to-market for advanced driver-assistance based applications.

- At the same time, companies supplying automotive OEM are producing higher performance, automotive-rated CPUs so that they can provide the control driven, sequential processing that is required for vehicle reliance and safety. This is because there is a greater need for balanced computing architectures, in which CPUs are responsible for system-level control, decision logic, and coordinating tasks between AI accelerators. CPUs will continue to play a role in controlling safe operations of software-defined vehicles, providing embedded OS functionality, and managing mixed workloads in multiple domains across the vehicle subsystems.

- Finally, automotive manufacturers and semiconductor manufacturers are looking towards custom ASIC based AI processors for optimized performance-per-watt, as well as meeting stringent automotive safety qualifications. This movement sprouted from the desire to reduce latency, power, cost and a willingness to create careful processors for specific AI workloads such as perception, sensor fusion, or path planning.

- For instance, Tenstorrent and BOS Semiconductors announced the "Eagle-N" automotive chiplet AI accelerator, which employs chiplet technology to optimize cost and provide customization for automotive in-vehicle infotainment and autonomous driving applications. The Eagle-N chips are expected to be in production by late 2026, and they will be demonstrated for the first time at CES 2025.

Learn more about the key segments shaping this market

Based on application, the automotive AI processors market is segmented into advanced driver-assistance systems (ADAS), autonomous driving, predictive maintenance, in-vehicle infotainment and navigation & telematics. The ADAS segment dominates the market with 42% share due to its widespread adoption across passenger and commercial vehicles.

- ADAS continues to dominate automotive AI processor demand as OEM integrates lane-keeping, adaptive cruise control and collision avoidance systems. Increasing regulatory mandates concerning vehicle safety and consumer popularity for semi-autonomous features are driving OEM to adopt these systems at an increasing level. AI processors are a key component that enable real-time sensor fusion, perception, and decision-making related to ADAS systems, providing safer and more intelligent driving experiences.

- The autonomous driving segment is vastly advancing the development of Level 3+ and fully autonomous vehicles. AI processors will become a key platform for high-speed computation of LiDAR, radar, and camera data as well as navigation and path planning, in real-time. OEM investment into AI processors and partnerships with semiconductor companies will lead to further deployment of autonomous driving features and technologies.

- Predictive maintenance capabilities and adoption continue to grow in stature and coverage as fleet operators and OEM leverage AI processors for perpetual vehicle health monitoring. Real-time analysis of sensor data will enable earlier detection of component wearing and failure, leading to lower vehicle downtime and less operational cost. Growing connected vehicle footprints and Internet of Things (IoT) integration is accelerating the use of AI computing at the edge.

- In May 2025, Penske Truck Leasing employed a telematics device-based AI system (Fleet Insight and Catalyst AI) to scan over 300 million data points daily. This proactive approach allows for the early identification of mechanical problems, which leads to minimization of downtime and allow Penske to enhance fleet performance for its customers, including Darigold and Honeyville.

Based on vehicle, the automotive AI processors market is segmented into passenger cars and commercial vehicles. The passenger cars segment is expected to dominate the market, due to the rapid integration of AI-driven features such as ADAS, infotainment, and autonomous capabilities. Growing consumer demand for safety, connectivity, and smart cockpit experiences drives widespread adoption of high-performance AI processors in passenger vehicles globally.

- Passenger vehicles are progressively incorporating AI processors to enable advanced driver assistance systems (ADAS) functions like lane-keeping, collision avoidance, and adaptive cruise control. Increased safety regulations and consumer preference for semi-autonomous features are creating new opportunities for real-time perception, decision-making, and safer driving experiences in a wider range of mass-market vehicles.

- AI processors are being deployed in passenger vehicle infotainment and connected cockpit systems to deliver personalized experiences, voice- and gesture-based controls, and real-time analytics. Cloud connectivity for personalized user engagement, remote updates, and generative AI applications to car owners will create an additional incentive for passenger vehicle interiors to make AI computing a clear and key distinction.

- Commercial vehicles are increasingly using AI processors to offer predictive maintenance, monitor sensors, and analyze fleet health indicators. By moving more processing to real-time edge locations (in comparison to telematics), AI processors will minimize vehicle downtime, lower operational costs, and optimize route efficiency, driving AI adoption in logistics, trucking, and public transit solutions.

- AI processors are advancing semi-autonomous capabilities in commercial vehicles with adaptive cruise, lane assist, and platooning features already being developed or tested. The desire for safer operation, to comply with regulations, and drive operational efficiencies in long-haul trucks and any delivery fleet businesses will drive further capital investment in high-performing AI technology dedicated to real-time process factors.

Based on deployment level, the automotive AI processors market is segmented Level 1 (driver assistance), level 2 (partial automation), level 3 (conditional automation), level 4 (high automation), level 5 (full automation). The level 2 (partial automation) segment is expected to dominate the market, due to its widespread adoption in passenger and commercial vehicles. OEM increasingly implements AI-powered lane-keeping, adaptive cruise control, and traffic jam assist features, driving high demand for processors capable of real-time sensor fusion and decision-making.

- Level 1 systems, including lane departure warnings and basic cruise control, continue to expand globally as entry-level safety features. The addition of AI processors improves the interpretation and reaction time of sensors while improving driver awareness. Original equipment manufacturers (OEM) still pursue cost-effective methods to implement foundational AI capabilities to satisfy regulatory safety standards while still offering legitimate safety features with gradual automation advances.

- Level 2 automation, using lane centering features with adaptive cruise control, is the most prevalent due to consumer acceptance. AI processors allow vehicles to combine multi-sensor readings in real-time and act accordingly with semi-autonomous driving. Regulatory forces and consumer preferences for safer vehicles help push Level 2 systems, making it the automation level deemed most popular for both passenger and commercial vehicles.

- Level 3 is growing at a CAGR of around 20% , with its conditional automation that allow vehicles to perform specified driving tasks autonomously under certain conditions. AI processors will manage complex workloads related to perception, prediction, and control decisions free of the human driver. The gradual rollout of Level 3 systems places the technology in pilot status usually in premium vehicles and operators have worked with regulators in collaboration to assure proper spheres of autonomy that allow safe transfer of control from the vehicle back to human drivers.

- Level 4 systems will allow the vehicle to perform fully autonomous driving only in limited applications defined by a geofenced area, such as urban zones or campus-like environments. AI processors will push the computer hardware to record performance feedback, sensor readings, path planning, and have shared decision-making.

")

Looking for region specific data?

The US automotive AI processors market reached USD 2 billion in 2024, growing from USD 1.8 billion in 2023.

- In North America, the US currently leads the way, as OEM and Tier-1 suppliers quickly embrace vehicles powered by AI, autonomous solutions, and connected car technologies. The presence of significant semiconductor players like NVIDIA, Intel, Qualcomm, and Mobileye enhances the development and deployment of AI processors for both passenger and commercial vehicles.

- The US market is recognized as the leading market given its established automotive R&D ecosystem, its developed applications of AI/ML in Advanced Driver-Assistance Systems (ADAS) and autonomous driving, its numerous testing/pilot projects, and its better collaboration/speed at which chipmakers, OEM, and software developers work collectively to integrate and test AI processors to all vehicle platforms.

- The US automotive AI processors market still has substantial growth potential as EVs, autonomous and semi-autonomous, predictive maintenance, and connected fleet solutions continue to accelerate AI processor adoption into vehicle platforms. With an increased focus on edge computing, AI toolchains, automotive-grade chipsets and safety systems compliant with regulations, OEM and suppliers can accelerate innovation, improve performance, and lower costs.

The North America automotive AI processors market dominated market share of 38.7% in 2024.

- The high demand for automotive AI processors in North America is fueled by OEM digital transformation initiatives and adoption of connected vehicles and autonomous vehicle technologies. Companies are investing primarily to develop AI-enabled safety, predictive maintenance, and infotainment systems for both passenger and commercial vehicles to respond to altering regulatory and consumer needs.

- The Canada Automotive AI processor market is expanding rapidly at an anticipated CAGR of 16.8%, driven by a growing adoption of electric vehicles, autonomous driving projects, and deploying AI/ML applications. The primary modernization trends include edge computing, increased performance AI chips, safety-compliant architectures, and workforce development toward vehicle-level AI innovation and deployment.

- There is increasing adoption of complex AI capabilities such as Original Equipment Manufacturers (OEM) and Tier-1 suppliers implement real-time sensor fusion, predictive analytics, fleet management, and autonomous decisions. AI-based operational efficiencies and driver assistance systems designed for automotive have been on the rise to enhance moving forward with smarter, safer, and connected mobility.

Europe Automotive AI processors market accounted for USD 1.2 billion in 2024 and is anticipated to show lucrative growth over the forecast period.

- In 2024, Europe was ranked as the second largest market, growing at a CAGR of 18.1%. This growth is fueled by adoption of AI/ML in vehicles, government-backed AV efforts, ongoing safety regulations and increasing deployment of connected and electric vehicles across a variety of segments.

- Germany, France, and the United Kingdom continue to lead the rest of Europe: the countries benefit from existing automotive R&D ecosystems, ample IT infrastructure, and growing demand for AI-enabled vehicle platforms. Germany distinguishes itself by creating mobility technology that focuses on the banking and financial services industries. The UK focuses on analytics-driven smart mobility and EV integration, while France is focusing on hybrid commuter-focused computing and integrating AI processors into their passenger and commercial fleets.

- Central and Eastern Europe is a developing market with high growth opportunity. Countries such as Poland, Hungary, and the Czech Republic are investing for vehicle AI R&D work, connected and autonomous vehicle infrastructure, and fleet AI solutions.

Germany dominates the automotive AI processors market, showcasing strong growth potential, with a CAGR of 16.9%.

- Germany leads the market of automotive AI processors in Europe, with their sophisticated automotive and technology ecosystem, high degree of digital maturity, and early adoption of AI technologies for key domains of mobility, manufacturing, and logistics. The growing demand for processing real-time sensor data continues to grow in AI processors deployed for applications such as predictive maintenance and autonomous driving.

- Enterprises of automotive organizations and service providers invest consistently in authoritative AI processor platforms, edge computing capabilities, and software toolchains. These investments are enabled by industry-wide regulatory compliance, standards for autonomous driving testing and digital transformation initiatives to drive scalability, safety, operational efficiencies, and widespread adoption of AI technologies for use in passenger and commercial vehicles.

- Germany is focusing on innovation and Industry 4.0 initiatives to support the accelerated adoption of AI processors and platforms to implement real-time analytics, predictive vehicle maintenance, and deploy autonomous driving models in vehicles. There are vendor groups that are bundling services which include professional consulting, optimizations, and managed support to secure enterprise adoption and support advanced decision making, AI-enabled fleet management, and intelligent vehicle operations across multiple sectors.

The Asia Pacific Automotive AI processors market is anticipated to grow at the highest CAGR of 23.2% during the analysis timeframe.

- The Asia-Pacific market is the fastest-growing region in the world, due to rapid growth of connected vehicles, EVs, autonomous driving programs and use of AI/ML in vehicle systems. OEM and Tier-1 suppliers are investing heavily in high-performance AI processors to support needs for real-time computation and predictive analytics in vehicle systems.

- After China, India and Japan present some of the largest market opportunities; both have individual characteristics. China leads in large volume adoption of autonomous and electric vehicle platforms supported by government actions. India positive growth is due to SMEs and mid-market automakers adopting cost-effective AI solutions and edge computing.

- The ASEAN bloc, and in particular, Thailand, Indonesia, and Malaysia, are supporting strong regional growth as automakers up-date AI processor availability in connected vehicle platforms, fleet management, and semi-autonomous driving applications. The use of hybrid and edge-computing solutions are managing sensor data, support AI workloads, and enhancing operational efficiency across automotive manufacturing, logistics, and mobility sectors.

China is estimated to grow with a CAGR of 23.7%, in the Asia Pacific automotive AI processors market.

- China leads the Asia-Pacific market as the country use autonomous driving systems, electric vehicle (EV) manufacturing and large-scale AI capabilities across the automotive value chain. Domestic original equipment manufacturers (OEM) and technology companies are rapidly developing AI-enabled systems for perception, navigation, and driver assistance to enhance vehicle safety and performance.

- Automotive businesses are moving quickly to invest in data-centric vehicle architectures that are fully capable of profitable AI systems by leveraging edge AI processors, centralized computing platforms and chip-on-sensor architectures and devices to provide better awareness of context, decrease latency, and provide predictive decision-making. Key product priorities include: power efficiency, sensor fusion, and advanced driver-assistance workloads.

- China is expected to further bolster its automotive AI processors leadership position by 2025, supported by state-led strategy such as the "Intelligent Vehicle Innovation Development Strategy." Partnerships between automakers (e.g., BYD, NIO and XPeng) and semiconductor companies (e.g., Horizon Robotics, Huawei, NVIDIA) are accelerating the automotive deployment of AI chips at large scale.

Latin America automotive AI processors market accounted for USD 485.8 million in 2024 and is anticipated to show lucrative growth over the forecast period.

- The Latin America market is projected to grow at a CAGR of 20.8%, this is because of rapid digital transformation, cloud adoption and increased AI/ML collaboration within the automotive and mobility sectors. The demand for real-time analytics and predictive intelligence is leading to adoption of advanced AI processors across the Latin America region.

- Mexico and Argentina are main contributors in region. Mexico's established industrial base, growing automotive manufacturing ecosystem, and swift penetration of cloud-native and hybrid lake house architectures are spurring demand for AI-enabled automotive systems. In contrast, Argentina leverages an emerging regional digital ecosystem with regulatory alignment with international standards and increasing enterprise investment in modernization and AI infrastructure.

- Countries in emerging areas like Chile, Colombia, and Peru have great growth potential. Urbanization, participation of small and medium-sized enterprises (SMEs) and investment into data ecosystems all support the use of AI in the adoption of AI in automotive manufacturing and in connected mobility solutions. Vendors with partnerships in place, and service models built to scale, stand to harness opportunity in these emerging and fragmented markets that are gaining traction.

- The automotive sector in Latin America is further supported beyond AI processors by the emergence of cloud marketplaces, managed AI services, and AI ready development platforms. Movement toward low-cost infrastructure like AWS, Azure, and GCP is enabling organizations to tackle modernizing vehicle data architectures, harmonizing analytics capabilities, and building operational intelligence to make decisions faster and reduce complexity.

Brazil is estimated to grow with a CAGR of 18.5%, in the Latin America automotive AI processor market.

- The market in Brazil is experiencing strong growth as businesses implement hybrid and multi-cloud architectures to balance data security, regulatory compliance, and scalability of AI deployment. These architectures allow for integration of on-premises systems and cloud systems, which supports real-time analytics, AI/ML workloads, and enterprise data access across automotive manufacturing, connected vehicle systems, and industrial operations.

- Enterprises in Brazil are deliberately using lakehouse platforms to fuel AI-driven innovation. The quest for predictive intelligence, personalized customer experiences, and optimization is driving the integration of AI processors into connected vehicle systems, and into the production processes in the automotive industry. In those ways, lakehouse infrastructures are emerging as a core driver of digital transformation in the automotive ecosystem, across sectors such as: BFSI, manufacturing, and retail, that facilitate the functioning of the automotive ecosystem and operational financing.

- Adoption is being accelerated through partnerships between IT services suppliers, automotive OEM, and providers of cloud services that can offer managed services, consulting and AI deployment assistance. These partnerships help businesses streamline their AI deployment, improve infrastructure efficiencies, and leverage as much data as possible in order to make decisions faster and develop operational agility.

- In 2025, Mercedes-Benz Brazil worked with Aquarela Analytics, to implement an AI analytics system to the enterprise, consistent with the need to integrate historic source data into previously independent silos for insightful real-time/data driven decisions. As the foundation was built on open-source software (OSS), it demonstrates Brazil’s growing focus on isolated development of a cost-effective, independent AI network, which can open innovation and opportunity within connected and intelligent vehicle development.

The Middle East and Africa accounted for USD 333.3 million in 2024 and is anticipated to show lucrative growth over the forecast period.

- The MEA automotive AI processors market represented 6% of the global market in 2024, underpinned by accelerating digital transformation, cloud adoption, and the growth of AI/ML-enabled analytics demand across BFSI, telecom, manufacturing, and retail sectors. Increased regional momentum for cloud or cloud-native architecture is starting to encourage advanced AI adoption along the automotive value chain that supports data-driven decision-making, operational intelligence, and predictive maintenance.

- Growth in the region is also supported by the modernization of aging IT infrastructure as organizations look to improve their management of growing enterprise data. Organizations seek out cloud-native/hybrid architectures to consolidate data silos, improve analytics and AI readiness, and scale analytics and data activity laying the groundwork for AI processors with wider adoption across connected vehicle systems and automotive production settings.

- The UAE and Saudi Arabia dominate the regional market, supported by enterprise ecosystems with high value, substantive government digitalization programs, and established IT and cloud infrastructure. The UAE landscape will continue to develop with a focus on AI-driven analytics, autonomous mobility applications, and smart infrastructure developments, while Saudi Arabia develops multi-cloud environments and implements AI into manufacturing, mobility, and governance, as highlighted in its Vision 2030.

- The other regional markets progress in the AI adoption stage, is increasing AI adoption in South Africa and Qatar being affirmed by public-private collaborations, developing national AI strategies and programs, and the growth of automotive and mobility-related applied AI R&D, which only strengthens MEA's position in the global automotive AI landscape.

UAE to experience substantial growth in the Middle East and Africa Automotive AI processors market in 2024.

- The market in UAE is growing at a fast pace at a CAGR of 21.2%, driven by the country's digital transformation initiatives and growing adoption of AI-driven analytics in organizations. The government is strongly supporting projects like the UAE National AI Strategy 2031, which advocates the adoption of new data processing technologies, including AI processors, across the automotive, industrial, and transport sectors.

- Organizations in the UAE are increasingly leveraging cloud-native and hybrid architectures to support real-time analytics and AI/ML workloads, as well as data-driven decision-making. These actual deployments enable full integration of on-premises computing infrastructure with cloud environments, and allow organizations to manage regulatory compliance, data sovereignty, and performance optimization.

- The market is also underpinned by strategic partnerships with global cloud providers (including, AWS, Microsoft Azure, and Google Cloud) as well as regional enablement of system integrators providing managed services, consulting, and AI infrastructure support. These partnerships ease the deployment and governance of AI, while ensuring scalability and operational efficiency, and accelerating the time to market for intelligent automotive solutions such as autonomous driving systems, connected vehicle platforms, and predictive maintenance systems.

Automotive AI Processors Market Share

The top 7 companies in the automotive AI processors industry are NVIDIA, Tesla, Mobileye (Intel), Qualcomm, Continental, Robert Bosch and Huawei Technologies, contributing 57% of the market in 2024.

- NVIDIA is at the forefront of the automotive AI processors market, with a market share of 15.3 %. Its automated self-driving platform, the DRIVE platform, incorporates GPU, CPU and AI accelerators for all autonomous driving and ADAS applications. It provides a fully scalable hardware-software ecosystem for automakers, delivering real-time perception, simulation, and data processing capabilities, ultimately enabling automakers to build smarter, safer, and energy-efficient vehicles leveraging high-performance computing capabilities.

- Tesla develops its own silicon-based AI processors such as the FSD (Full Self-Driving) AI chip, which drives real-time perception and driving decision making for self-driving applications. The company's vertical integration around hardware and AI software provides full optimization of performance, learning, and power for its fleet of connected electric vehicle products.

- Mobileye, owned and operated under Intel, provides vision-based AI processors and SoCs for ADAS and autonomous driving. The EyeQ product family incorporates both AI acceleration with perception algorithms to deliver object detection, mapping, and situational awareness capabilities, and positions Mobileye as a lead supplier of AI hardware for safety-centric automotive applications.

- Qualcomm Snapdragon Ride platform provides scalable AI compute solutions for automated and connected vehicles. The architecture merges CPU, GPU, and AI cores and caters for sensor fusion and real-time perception, and adaptive intelligence for driving. Qualcomm then leverages its connectivity expertise to optimize vehicle-to-everything (V2X) communications and to enable next-generation automotive digital architectures.

- Continental takes the focus on the sensors a step further by integrating AI processors into its intelligent mobility systems supporting ADAS, autonomous driving and in-vehicle computing solutions. Continental has partners at the chip level and also relies on the development of its own software to meet the needs of energy-efficient, real-time AI applications designed to improve road safety, vehicle awareness and connected mobility performance.

- Robert Bosch merges sensor tech with AI processors and embedded computing so that ADAS and autonomous mobility systems can be powered by AI-driven ECUs and system-on-chip applications that support real-time perception, sensor fusion, and predictive analytics capability in ADAS and autonomous driving systems so that automakers can deploy safe, dependable, and energy-efficient driver assist and autonomous driving technology.

- Huawei maximizes its artificial intelligence processors, Ascend AI processors, and cloud-edge computing platforms for intelligent vehicle systems, ADAS, and smart cockpit applications, respectively. Huawei's AI hardware portfolio emphasizes high-performance, low-power computing in automotive applications to support real-time decision-making and direct intelligent mobility systems in China's rapidly evolving intelligent mobility ecosystem.

Automotive AI Processors Market Companies

Major players operating in the automotive AI processors industry are:

- Aptiv

- Baidu

- Continental

- Horizon Robotics

- Huawei Technologies

- Mobileye (Intel)

- NVIDIA

- Qualcomm

- Robert Bosch

- Tesla

- Aptiv centers its work around artificial intelligence-enabled ADAS and autonomous driving platforms and focuses on integrating processors for sensor fusion and real-time decision-making processes. Similarly, Baidu also emphasizes its Apollo platform, which uses in-house AI chips for autonomous mobility, and focuses on perception, mapping, and workloads deep learning to advance the development of intelligent vehicles in China. Both Aptiv and Baidu are engaged in delivering advanced connected mobility.

- Continental is engaged in delivering AI processing capabilities as part of their intelligent mobility systems for ADAS features, vehicle perception, and connected services. Horizon Robotics focuses on developing edge AI chips, as well as its autonomous driving solutions, both of which are optimized for real-time and low power processing. Both companies incorporate hardware and software to enable AI scaling across OEM and mobility platforms about AI processing capabilities.

- Huawei incorporates its Ascend AI processing capabilities as part of its solutions for in-vehicle intelligence, smart cockpits, and ADAS for intelligent mobility as cloud to edge solutions. Mobileye (Intel) delivers vision-based AI SoCs for perception and mapping for autonomous driving. Both companies provide a driving force for creating AI-enabled vehicles, balancing high-performance computing ability alongside advanced sensor technological integration for the global automotive markets.

- NVIDIA is propelling the market with the DRIVE platform for autonomous driving, generating AI processing ecosystems by pairing GPUs, AI accelerators, and real-time analytics into a single platform. Qualcomm's Snapdragon Ride is a platform designed to provide AI compute capabilities for vehicle perception, V2X Socket, and sensor fusion cloud and edge solutions. Both the NVIDIA and Qualcomm platforms are enhanced capabilities for scalable, high-performance processing enabling OEM to embed capabilities of intelligent and connected vehicle processing.

- Robert Bosch is implementing AI processors into electronic control units (ECUs) as a component of ADAS and predictive analytics framework for autonomous systems and is developing platform solutions that support safety and operational efficiencies. Tesla designs its own architecture of AI chips to facilitate its full self-driving (FSD) system, which secures reliability and operational performance of perception and real-time decision-making features.

Automotive AI Processors Market Report Attributes

| Key Takeaway | Details |

|---|---|

| Market Size & Growth | |

| Base Year | 2024 |

| Market Size in 2024 | USD 5.6 Billion |

| Market Size in 2025 | USD 6.3 Billion |

| Forecast Period 2025 - 2034 CAGR | 20.5% |

| Market Size in 2034 | USD 33.5 Billion |

| Key Market Trends | |

| Drivers | Impact |

| Growing adoption of ADAS and autonomous driving | Drives large-scale demand for high-performance AI processors to enable real-time perception, navigation, and safety decision-making. |

| Rise in connected and electric vehicles | Expands AI processor integration across infotainment, energy optimization, and telematics systems, boosting unit shipments. |

| Edge AI and on-vehicle data processing | Enhances safety and latency performance by allowing faster, localized AI inference without cloud dependency. |

| OEM and semiconductor collaboration | Accelerates AI innovation cycles and strengthens vendor-OEM ecosystems for faster commercialization of autonomous capabilities. |

| Pitfalls & Challenges | Impact |

| High development and integration cost | Limits adoption among cost-sensitive OEM, slowing down mass-market penetration of advanced AI processors. |

| Limited standardization and interoperability | Creates integration hurdles between hardware and software ecosystems, delaying platform scalability and partnerships. |

| Opportunities: | Impact |

| Emergence of software-defined vehicles (SDVs) | Opens recurring revenue streams for AI chipmakers through upgradable, reprogrammable processor platforms. |

| Expanding EV production In Asia-Pacific | Creates significant volume-driven opportunities for AI processor suppliers catering to large EV manufacturers. |

| AI-based predictive maintenance & fleet management | Increases processor demand for analytics workloads that reduce operational costs and downtime for fleet operators. |

| Development of automotive-specific AI toolchains | Enhances ease of AI deployment, attracting OEM seeking compliant, scalable, and low-development-time solutions. |

| Market Leaders (2024) | |

| Market Leaders |

15% market share |

| Top Players |

Collective market share in 2024 is 47% |

| Competitive Edge |

|

| Regional Insights | |

| Largest Market | North America |

| Fastest growing market | Asia Pacific |

| Emerging countries | Mexico, Canada, Poland, Hungary, India, Thailand, Vietnam, Brazil, UAE, Saudi Arabia |

| Future outlook |

|

What are the growth opportunities in this market?

Automotive AI Processors Industry News

- In April 2025, Aptiv partnered with Baidu to localize smart driving solutions in China. This collaboration uses Aptiv’s AI cockpit platform along with Baidu’s autonomous driving technologies, while providing Freenow’s service capabilities to support autonomous ride-hailing.

- In April 2025, Horizon Robotics and Bosch entered a MOU outline to further advance their collaboration around smart driving offerings. The strategy behind their relationship is to combine Horizon’s AI processors with Bosch’s automotive solutions to enhance ADAS and autonomous driving through an approach focused on increasing intelligence capability and safety features.

- In September 2025, Huawei announced a new partnership model with automakers that would allow for more control in making plans for the building of vehicles. As part of this strategy, automakers would have more control in design of vehicles and innovations in a manner that is compliant with regulations while also enabling the introduction of Huawei’s AI technologies by the market and expectations from consumers.

- In September 2025, Qualcomm collaborated with Harman to deploy Qualcomm’s Snapdragon Cockpit Elite platforms in Harman's automotive product line. This collaboration helps to provide enhanced AI functionality in vehicles for in-car experiences by integrating advanced driver assistance systems (ADAS), infotainment, and connectivity features to drive the momentum toward software-defined vehicles.

- In November 2024, Mobileye presented their latest AI methodologies at the Driving AI event focusing on state-of-the-art technology in regard to autonomous vehicle functionality. Mobileye provided updates about the AI applications that are under development for both assisted and fully autonomous vehicles with a focus on safety, efficiency, and scalability in the automotive industry.

The automotive AI processors market research report includes in-depth coverage of the industry with estimates & forecasts in terms of revenue ($ Mn/Bn) and volume (Units) from 2021 to 2034, for the following segments:

Market, By Processor

- Graphics processing unit (GPU)

- Central processing unit (CPU)

- Application-specific integrated circuit (ASIC)

- Field programmable gate array (FPGA)

- System on chip (SoC)

Market, By Application

- Advanced driver-assistance systems (ADAS)

- Autonomous driving

- Predictive maintenance

- In-vehicle infotainment

- Navigation & telematics

Market, By Vehicle

- Passenger cars

- SUV

- Hatchback

- Sedan

- Commercial vehicles

- LCV (Light commercial vehicle)

- MCV (Medium commercial vehicle)

- HCV (Heavy commercial vehicle)

Market, By Deployment Level

- Level 1 (Driver assistance)

- Level 2 (Partial automation)

- Level 3 (Conditional automation)

- Level 4 (High automation)

- Level 5 (Full automation)

The above information is provided for the following regions and countries:

- North America

- US

- Canada

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Russia

- Nordics

- Poland

- Asia Pacific

- China

- India

- Japan

- South Korea

- ANZ

- Vietnam

- Thailand

- Latin America

- Brazil

- Mexico

- Argentina

- MEA

- South Africa

- Saudi Arabia

- UAE

Frequently Asked Question(FAQ) :

What is the market size of the automotive AI processors in 2024?

The market size was USD 5.6 billion in 2024, with a CAGR of 20.5% expected through 2034. The growth is driven by advancements in ADAS, autonomous driving, and in-vehicle infotainment systems.

What is the projected value of the automotive AI processors market by 2034?

The market is poised to reach USD 33.5 billion by 2034, fueled by the adoption of AI/ML, generative AI, and domain-specific processor architectures.

What is the expected size of the automotive AI processors industry in 2025?

The market size is projected to reach USD 6.3 billion in 2025.

How much revenue did the GPU segment generate in 2024?

The GPU segment generated approximately 38% of the market share in 2024, led by its superior parallel processing capabilities for perception, sensor fusion, and autonomous navigation.

What was the market share of the ADAS segment in 2024?

The ADAS segment dominated the market with a 42% share in 2024, owing to its widespread adoption across passenger and commercial vehicles.

Which region leads the automotive AI processors sector?

The United States leads the market in North America, reaching USD 2 billion in 2024.

What are the upcoming trends in the automotive AI processors market?

Trends include AI/ML and generative AI integration, domain-specific processors, hybrid computing frameworks, and AI training ecosystems like NVIDIA Drive and Qualcomm AI Engine SDK.

Who are the key players in the automotive AI processors industry?

Key players include Aptiv, Baidu, Continental, Horizon Robotics, Huawei Technologies, Mobileye (Intel), NVIDIA, Qualcomm, Robert Bosch, and Tesla.

Automotive AI Processors Market Scope

Related Reports